INMD - InMode: A Niche Medical Aesthetic Devices Player With Solid Financials

2023-11-07 04:52:04 ET

Summary

- InMode Ltd's share price fell by 25% in October due to the Israel-Hamas conflicts and lowered revenue guidance.

- The company operates in a niche market between plastic surgery and laser procedures, giving it a competitive advantage.

- InMode is well-positioned to benefit from the growing global medical aesthetic market and increasing demand for weight-loss drugs.

- The stock trading at low valuations could suggest it is undervalued and presents a great "Buy" opportunity for value investors.

Investment Thesis

Oct 2023 hasn't been an excellent month for InMode Ltd's investors, with share price tumbling by a whopping 25% in the space of just one month thanks to the onset of the Israeli-Hamas conflict, lowering forward revenue guidance for Q4 2023, as well as uncertain macroeconomic conditions against a high-interest rate backdrop. Subsequently, this has resulted in much disdain from Wall Street and investors, causing a massive sell-off. The share price of INMD is now trading at a near 52-week low.

Nevertheless, upon researching the company, I think the fear has been grossly magnified and way overblown. For one, more than 80% of INMD's revenue comes from the US and Europe, while war-torn Israel accounts for only 1% of the company's total revenue. For another, the management team reassures investors that the war won't cause significant interruption to production. Inventory levels globally and in Israel are sufficient and include component and sub-assembly for the next three quarters. Thus, I think InMode would likely navigate through the Middle East War.

InMode enjoys secular industrial tailwinds, including the robust growth trajectory of the medical aesthetic market and increasing demand from baby boomers and Gen X for medical aesthetic treatment as they age older. Furthermore, InMode operates in a niche market between plastic surgeries and laser procedures that no competitors compete in. This creates a wide competitive moat for InMode Ltd.

Looking at things from a financial perspective, I think InMode Ltd enjoys a robust balance sheet. In Q3 2023 , it sits with more than $675.8 million in cash reserves, which accounts for 40% of the current market cap. While revenue and earnings were underwhelming in Q3 2023, it generated $123.1 million of revenue, up 2% YoY. Non-GAPP EPS was slightly down, falling to $0.61, compared to $0.65 in Q3 2022 due to seasonality sales. Nonetheless, INMD has epitomized a long-term resilient growth track record of revenue and earnings over the past 5 years. Given its short-term headwind, I still rate INMD as a "Buy".

Business Overview

InMode Investors Presentation (InMode Investors Presentation)

{kind=link}

To those unfamiliar with the company, InMode Ltd. (INMD) is an Israeli aesthetic beauty company established in 2008 that specializes in producing and selling aesthetic medical products using its proprietary radiofrequency technologies to customers in the US and around the world. It provides skin treatments and enhancements to the Human Face, Body, Hair Removal and Women's wellness using its capital equipment.

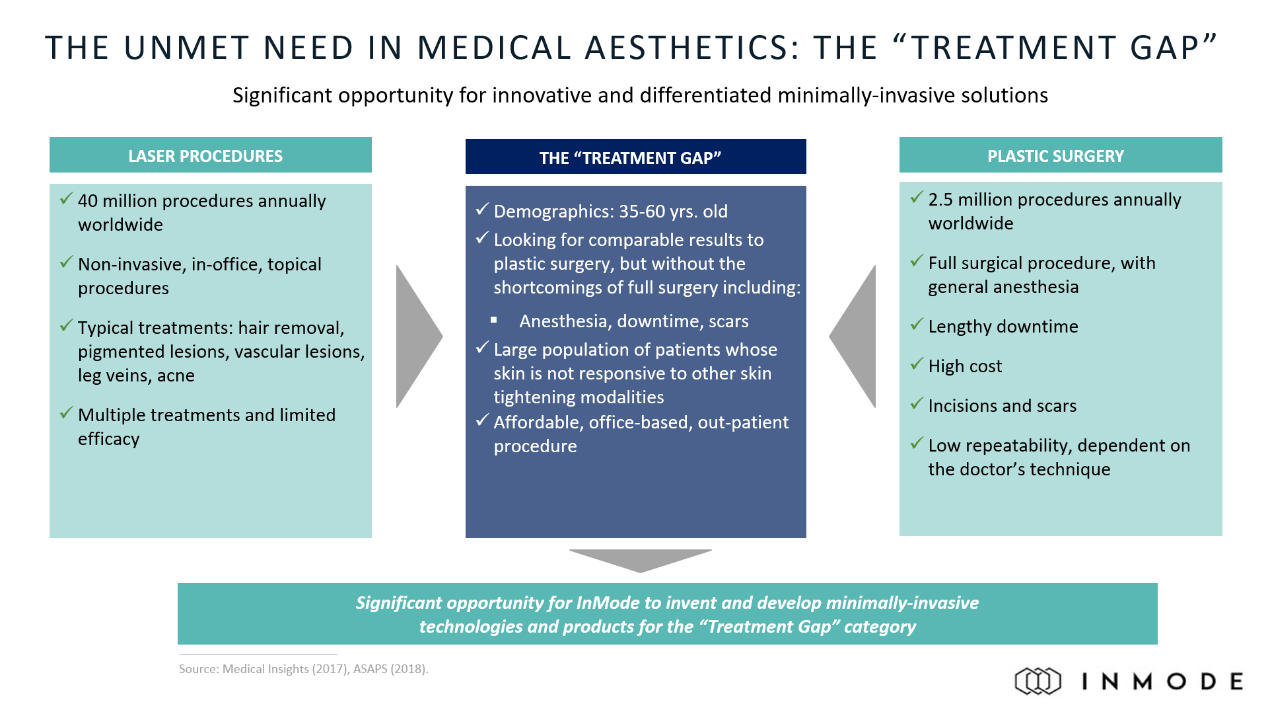

The medical proposition of InMode Ltd differentiates itself from its competitors. INMD slides in between the "Treatment Gap" between laser procedures and plastic surgeries. On one hand, Traditional laser aesthetic procedures are often non-invasive to the skin, but patients are required to take multiple treatments that often come with limited efficacy. On the other hand, plastic surgeries have higher efficacy but at the expense of high costs and incisions or scars on the patient's flesh, which makes it not appealing to the patients too.

As a result, the "Gap" creates an underpenetrated and substantial addressable market for INMD to exploit. InMode Ltd develops minimally invasive capital equipment using radiofrequency technologies to improve skin appearance that provides comparable results to plastic surgery but comes with minimal to no scars and incisions on patient's skin, which minimizes bacteria infection and makes it more aesthetically pleasing.

In fact, INMD now owns 10 patents for its proprietary technologies. This makes it formidable for its competitors to copy, which I think creates an economic moat around the business.

InMode Product Ecosystem (InMode Q3 2023 presentation)

{kind=link}

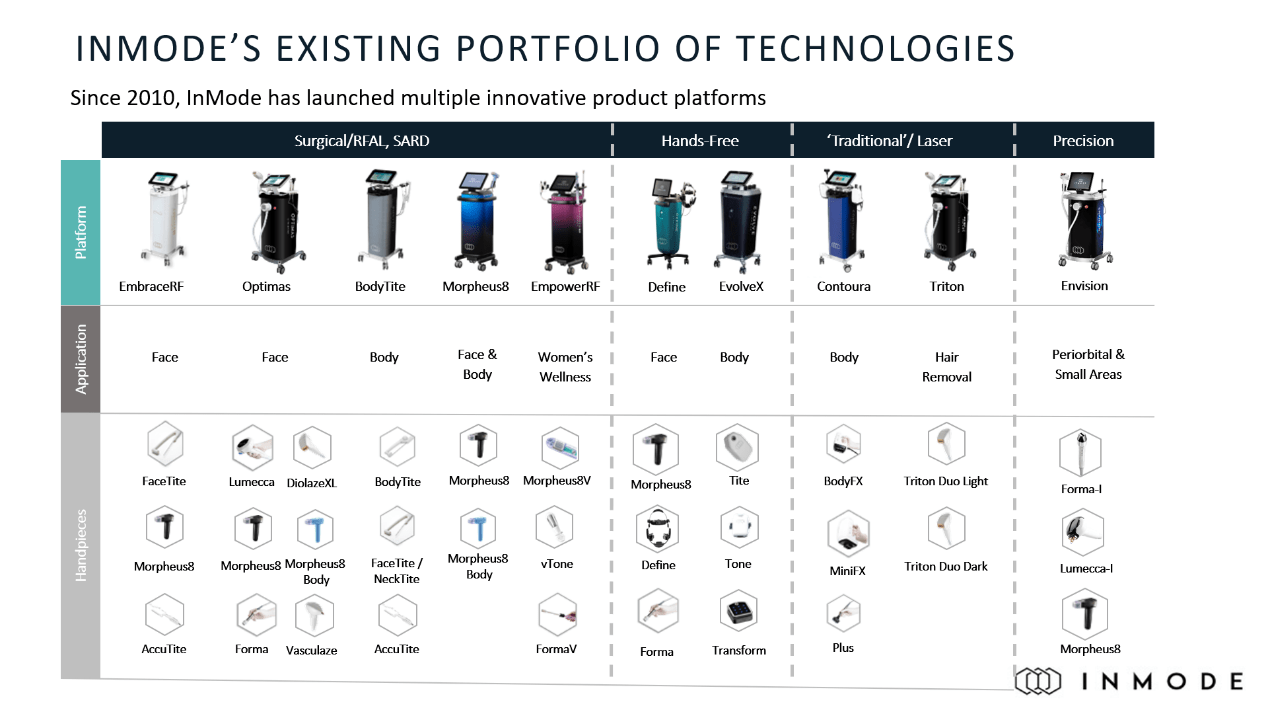

InMode Ltd.'s revenue streams are divided primarily into 2 segments, which are namely the capital equipment and the consumables & services segment.

The Capital Equipment segment includes the sale of non-invasive, hand-free, and minimal invasive minimal-invasive aesthetic medical products (including BodyTite, Optimas, Votiva, Contoura, Triton, EmbraceRF, EvolveX, Evoke, Morpheus8 and EmpowerRF) to clients in both the US and other customers in Europe, Asia & Australia etc. Its US Segment and International segment accounts for $67.9 million and $37.2 million, respectively, which contributes 85% of InMode's total revenue in Q3 2023.

The Consumables and service segment accounts for 15% of InMode's total revenue, with an estimated $17.9 million of revenue in Q3 2023. It generates sales from consumables and extended warranty services. The management team indicates that the sale of consumables and extended warranties is expected to increase over time as the installed base continues to grow.

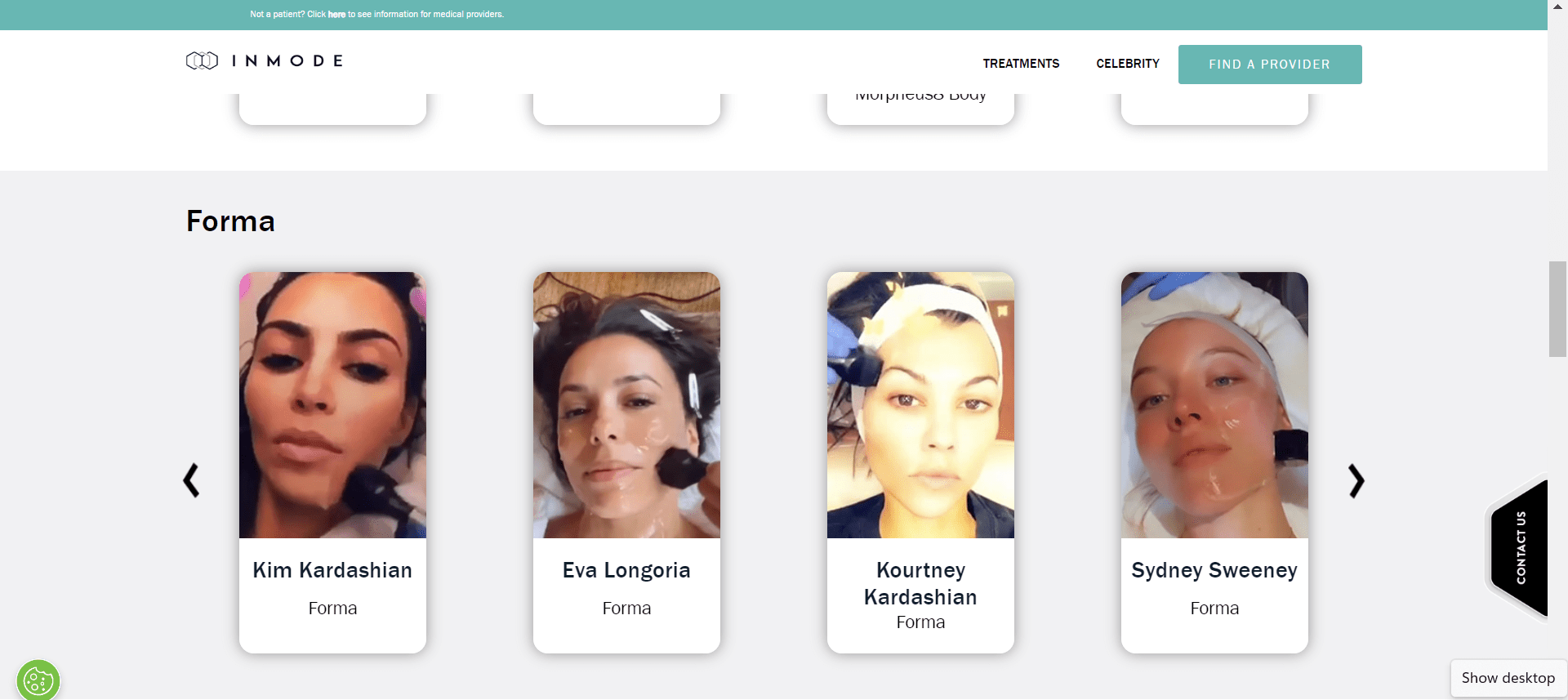

Wide retail and celebrity adoption of treatment

I consider when a celebrity uses a medical aesthetic treatment, and this creates a herd effect among retail customers to follow the bandwagon and also try out their products and treatment to enhance their self-image and external appearance. This will expand InMode's customer base.

As we can see, InMode's products and treatment services are widely adopted by celebrities, including Kim Kardashian, Bella Throne, Jessica Simpson, and Sydney Sweeney . This illustrates the popularity of InMode's product solutions among clients with positive feedback.

Wide Celebrity Adoption (InMode Website) InMode Distribution Network (Q3 2023 Investors Presentation)

{kind=link}

{kind=link}

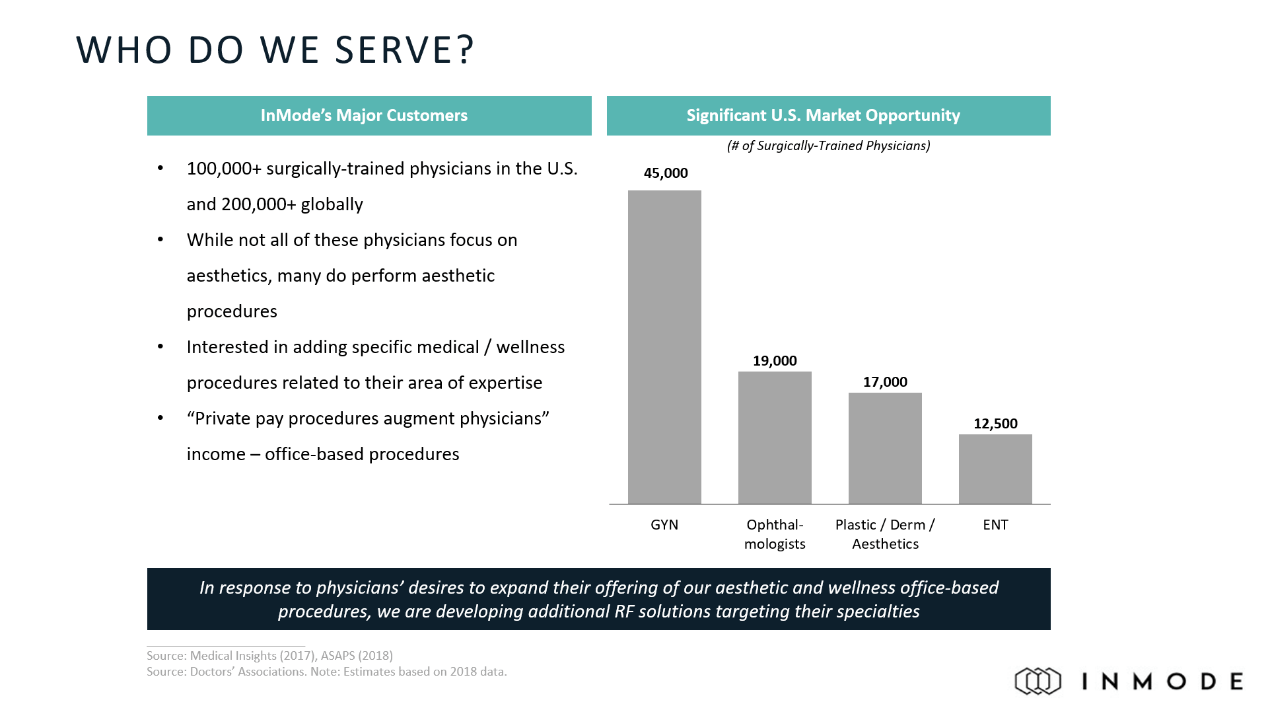

InMode's products and solutions also enjoy wide retail and medical adoption. As we can see, it sells or leases its products to more than 100,000 trained physicians in medical clinics in the US and 200,000 globally, spreading across 93 countries in Asia, Europe, the Middle East and Australia. This raises InMode's brand recognition among retail customers and physicians, which I think could potentially create a strong product ecosystem and ecosystem stickiness in the future.

Weight loss drugs creates synergies with skin-tightening treatment

While InMode is not a weight loss company, I firmly believe that InMode could benefit from the weight loss trend in the coming future. Here's why:

First, while prescription weight-loss drugs, including Novo Nordisk's Wegovy, has created a manic around investors and the public, arguing that they are conducive to controlling body weight by 10%-15%, this creates another problem of loosen skin among patients. Thus, those patients are going to need some sort of skin tightening procedure in a minimally invasive way that minimizes scars and incision on their skins.

And this places InMode a really good place to take advantage of the trends. INMD is one of the best companies to provide skin tightening solutions through an array of services, including Evolve X and Morpheus8 Body etc., that coagulate subcutaneous tissue and stimulate patient's underlying skin muscles. I therefore expect a wider retail adoption of medical aesthetic products in the future thanks to the synergies and domino effects created by weight-loss pills.

Skin Tightening Morpheus8 Body (InMode Website)

{kind=link}

Industry tailwind: Growing demand for medical aesthetic market in the US and globally

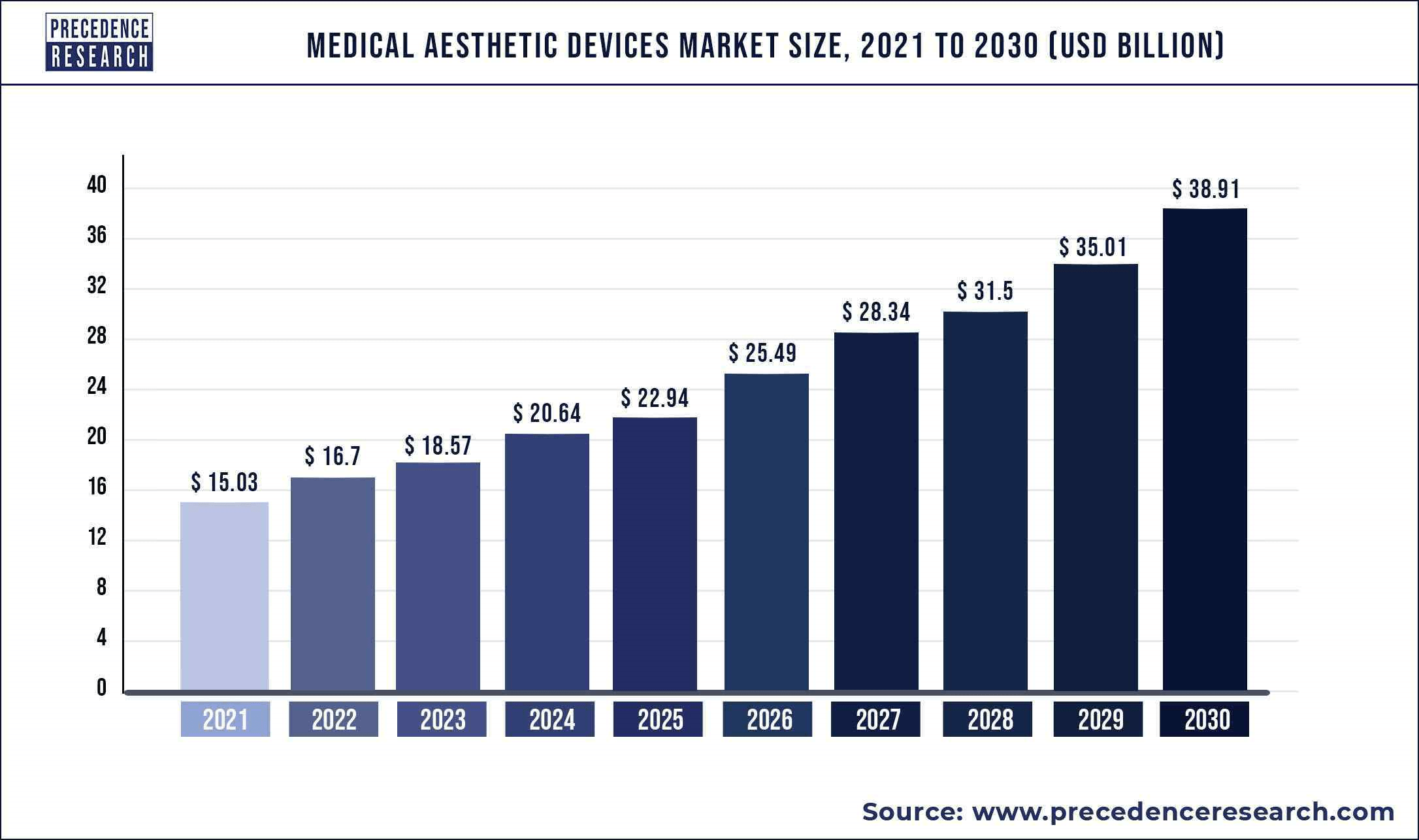

Growth in global medical aesthetic devices market (Precedence Research)

{kind=link}

As we can see from the above, according to Precedence Research , the global medical aesthetic devices market will likely more than double in size for the next 8 years, escalating from $18.6 billion in 2023 to $38.9 billion in 2030, which is expected to grow at a CAGR of 9.6% for the coming decade. I think this will create an enormous addressable and untapped market for InMode to grow and benefit in the future, which will serve as a revenue growth catalyst.

{kind=link}

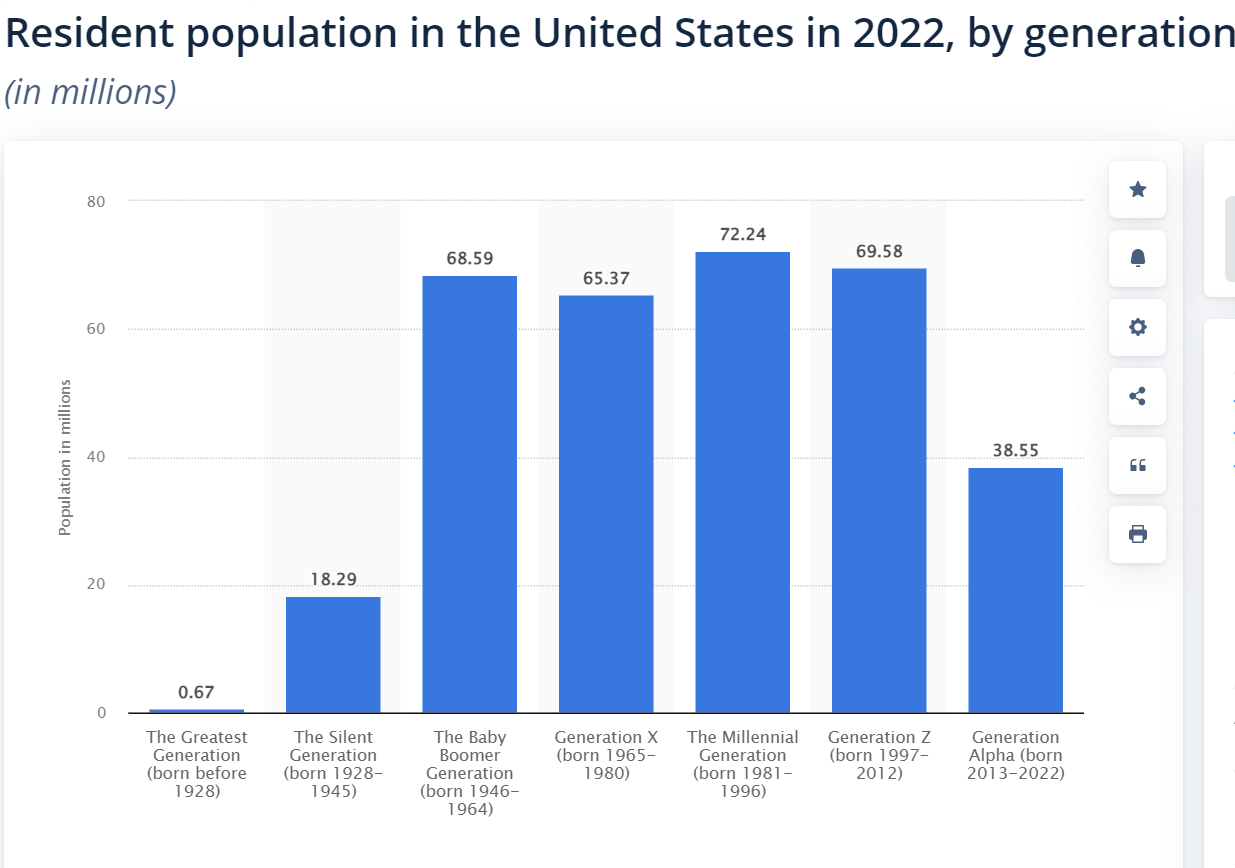

To add on, according to Statista, the total number of Baby Boomers, Gen X, and Millennials in the US have reached a total population of 206.2 million in 2022 (68.59 Mn, 65.37 Mn, and 72.24Mn, respectively). This favourable ageing population demographics will likely benefit INMD in the future as this raises the total addressable customer base for InMode Ltd in the US. As more Gen X and Baby Boomers approach retirement age, they will have greater demand for more aesthetic medical treatments to make them look younger and more appealing in terms of external appearance.

For female in the Millennials generation, they will also have a higher demand for aesthetic medical treatments to look healthier and to enhance their self-image by improving their external appearance. As such, this will derive more demand for medical aesthetics devices for InMode. I expect this would generate ample business opportunities and, thus more revenue and cash flows for years to come for INMD.

Financial Analysis

1. Secular growth in revenue and bottom-line

INMD Financials (InMode Investors Presentation)

{kind=link}

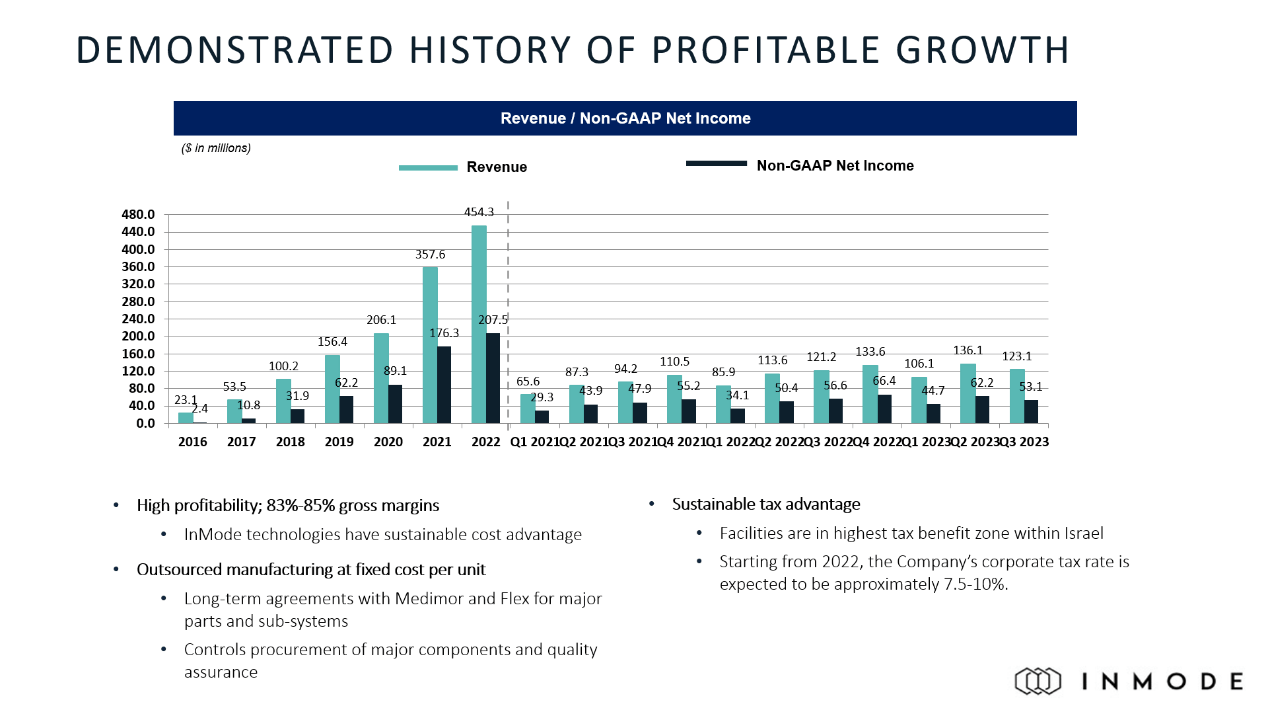

Overall, Q3 2023 has not been a fruitful quarter for InMode. Its total revenue only grew slightly by 2% YoY from $121.2 million in Q3 2022 to $123.1 million in Q3 2023. Its Non-GAPP net earnings also slid by 6% YoY from $56.6 million in Q3 2022 to $53.1 million in Q3 2023. The underwhelming results could be attributed to 2 factors: first, the cyclical nature of revenue, as most customers don't prefer having medical aesthetics treatments in the summer due to not wanting to and being exposed to the sun on their vacation. Second, the high-interest backdrop has dampened physicians' interest in leasing medical capital equipment at an elevated interest rate of 14%-15%, which has resulted in scaling back of CapEx from medical clinics.

While short-term headwinds remain slightly concerning, things look much brighter over the long term. Revenue has demonstrated a robust growth trajectory, jumping nearly 20-fold from $23.1 million in 2016 to $454.3 million, compounding at a CAGR of 64%. The bottom line has also seen resilient growth, jumping nearly a hundred-fold from $2.4 million in 2016 to $207.5 million in 2022, registering an impressive CAGR of 86%.

Valuation Score (Seeking Alpha)

{kind=link}

Seeking Alpha currently ranks InMode's profitability score as an A+, which I thoroughly agree with. The margins of InMode look impressive either. Gross Margin reached nearly 83%-85%, outperforming the sector median of 56%. This indicates strong pricing power and reasonable production cost control from INMD.

InMode also achieved operating margins and net margins of 40.96% and 36.18%, respectively, which significantly trumps the sector median and industrial average. This indicates the fact that the company is a profitable machine.

Another great thing about the business is the solid operating efficiency it possesses. Return on Invested Capital ((ROIC)) and Return on Equity ((ROE)) have reached 20.61% and 29.3%, significantly higher than their counterparts that are still unprofitable businesses. This makes InMode Ltd a stand-out market leader in the global medical aesthetic market.

2. Strong Balance Sheet with minimal debt

I n

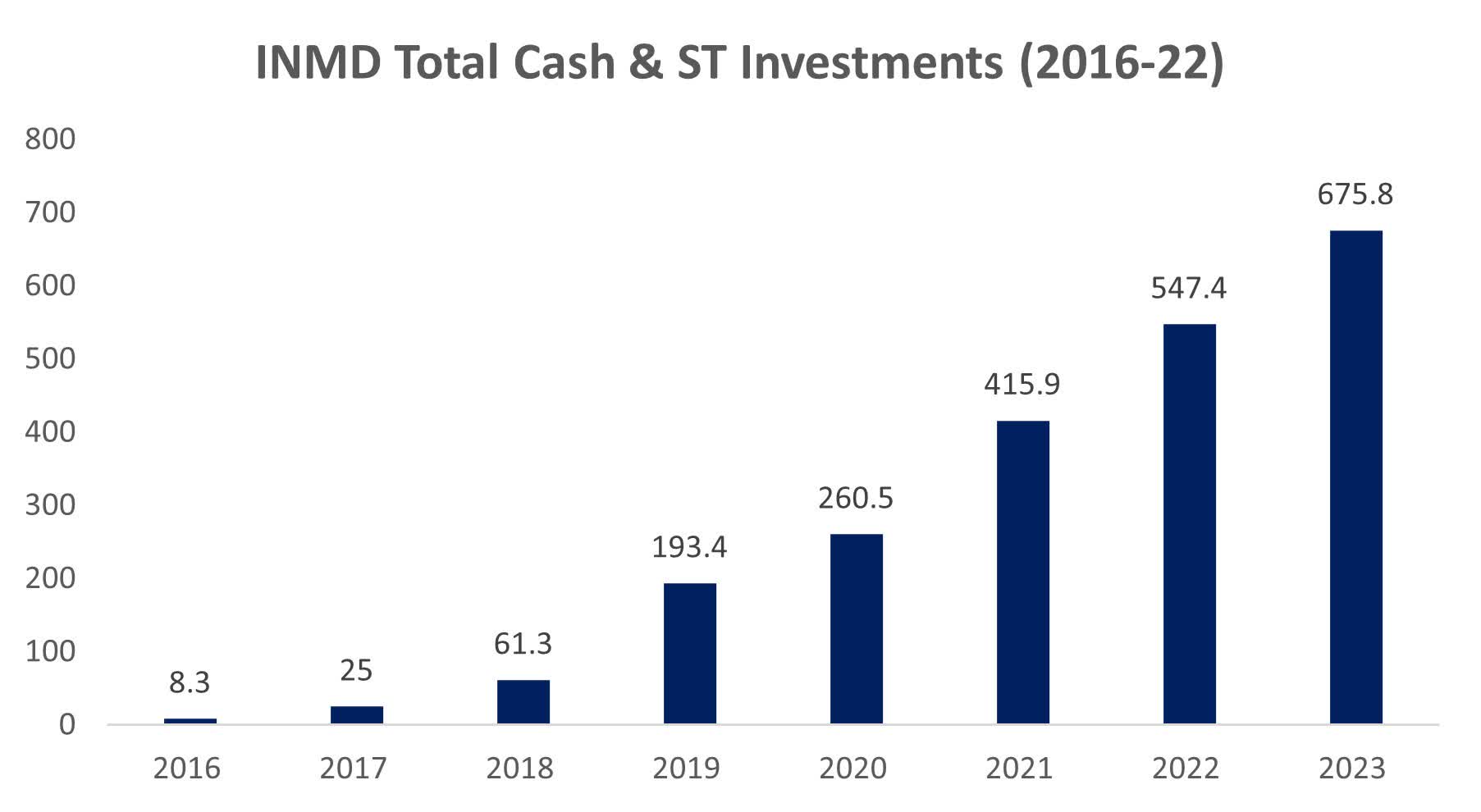

INMD Cash & Cash Equivalents (KL Research)

{kind=link}

Another thing I like about InMode Ltd is the shareholder-friendly balance sheet it possesses. Its Cash buffer has accumulated over the past year, snowballing from $8.3 million in 2016 to $675.8 million in Q3 2023, which accounts for nearly 40% of the current market cap.

While the management team was hesitant to use its cash to buy back shares and distribute dividends, as stated during the Q3 earnings call. The management plans to use its huge cash reserves to look for M&A targets to expand its market share and create synergies within the business. However, I think it would be most shareholder-friendly for the management team to use those cash reserves to return value back to shareholders through share buybacks or dividend distributions.

Another highlight of its shareholders-friendly balance sheet is the company has Little to No Debt at all. InMode Ltd has only $3.58 million in debt. This leaves the company at an enterprise value of just $1.12 billion. The company is self-sufficient enough to finance its daily operations through its cash reserves, which minimizes its external dependence on leverage.

Enterprise Value of INMD (Seeking Alpha)

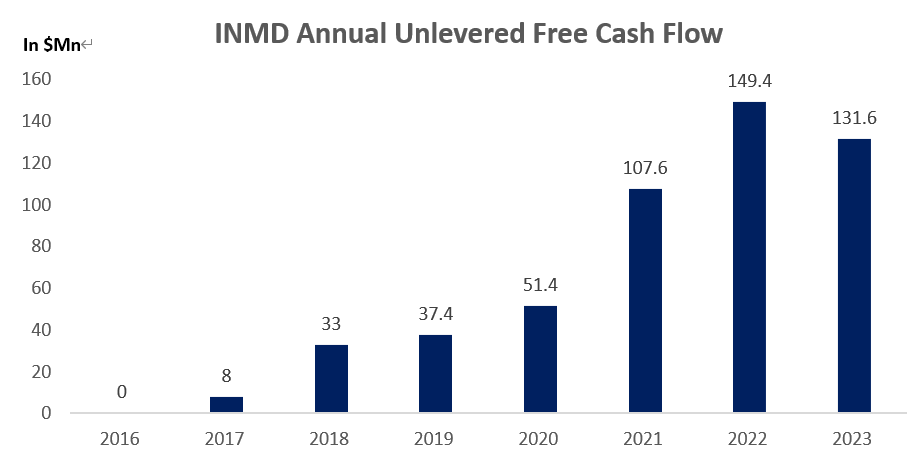

To provide another perspective, INMD has grown its annual free cash flow consistently over the past six years. Unlevered Free Cash Flow skyrocketed from just $8 million in 2017 to over $131.6 million in 2023. This illustrates the fact that the company can generate more cash every year, which is a positive sign for a value stock. As a result, the cash buffer has been trending upward over the past six years.

{kind=link}

As a value investor looking to invest in a company over the long term, I like to own companies with maximum cash buffer and minimal external leverage dependence on their balance sheet to avoid the risk of the company going bankrupt, especially against the high-interest backdrop at current levels.

DCF Valuation: Decent upside potential despite conservative assumptions

{kind=link}

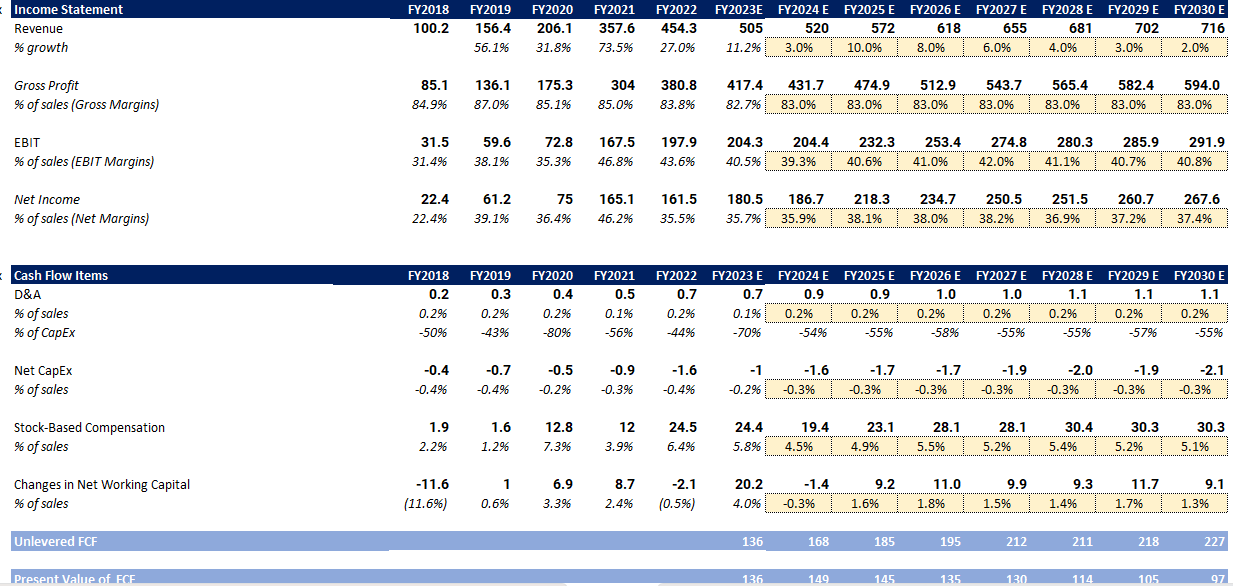

To make my forecast more down-to-earth, I have made relatively conservative estimates.

Based on my assumption, InMode's revenue in 2023 is expected to be around $500-510 million, in line with management's forward guidance. In 2024, I expect its revenue to grow by a disappointing 3% against the high-interest rate backdrop.

As the Fed cuts rates more aggressively in 2025, I expect INMD's revenue to re-accelerate to double-digit growth on par with the industrial average in 2025 and decrease linearly to 2% in 2030 (i.e., $716 million), which reflects the growing demand for INMD's aesthetic medical products.

As for its Operating Margins, I predict INMD's operating margins to be around 39-40%, which is in line with the company's historical track record and historical average.

After subtracting the ~ $1.5 - 2 million of capital expenditures and ~$ 20 - 30 million of shareholder-unfriendly stock-based compensation program annually, which dilutes existing shareholders' interest, and around $10 million of changes in Net Working Capital (NWC), we're left with $136-227 million of annual unlevered free cash flow for the business for the next seven years until 2030.

Using a conservative Discount Rate of 13% and a perpetual growth rate of 2%, I have arrived at an Enterprise Value for InMode, Ltd of around $2 Billion. By adding back the $675.8 million of cash while subtracting its total debt of $3.6 million and dividing it by the total amount of outstanding shares of 83.7 million shares, I have arrived at an Intrinsic Value of INMD for around ~ $30.6 per share, implying a comfortable minimal 40% upside at least!

Intrinsic Value of INMD (KL Research)

{kind=link}

Multiples Valuation: Still Looks Undervalued.

{kind=link}

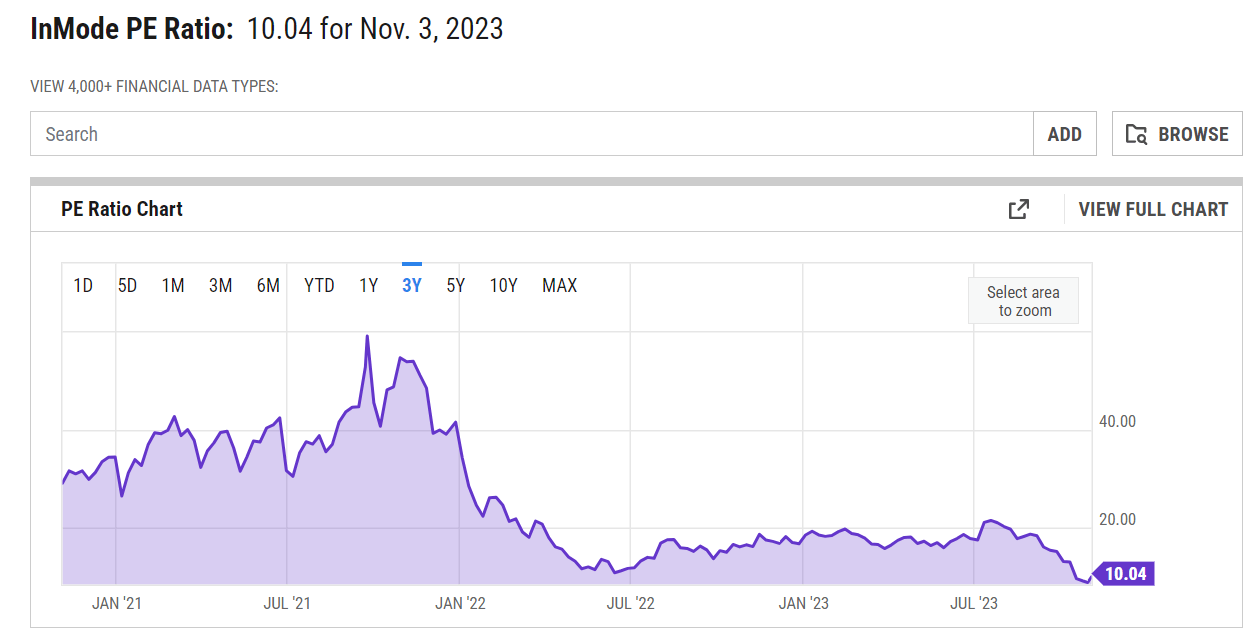

As we can see, the P/E ratio of InMode Ltd has been trending downwards and is now trading at nearly 10x earnings, which remains well below the 3-year average of around 20x. This presents an exciting buying entry point for long-term value investors.

Valuation Score (Seeking Alpha)

{kind=link}

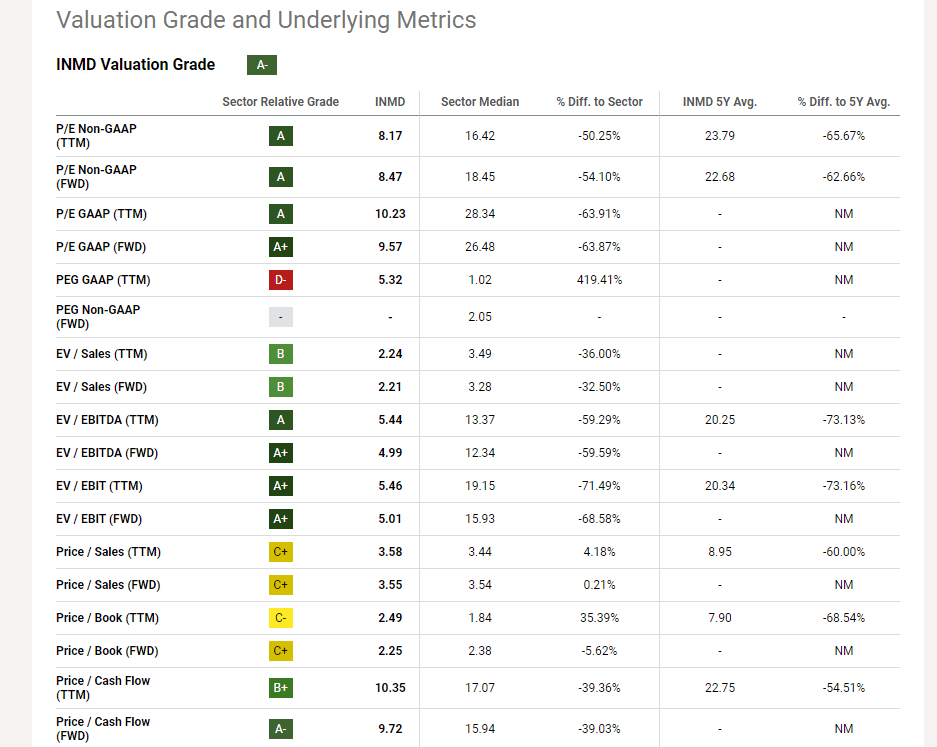

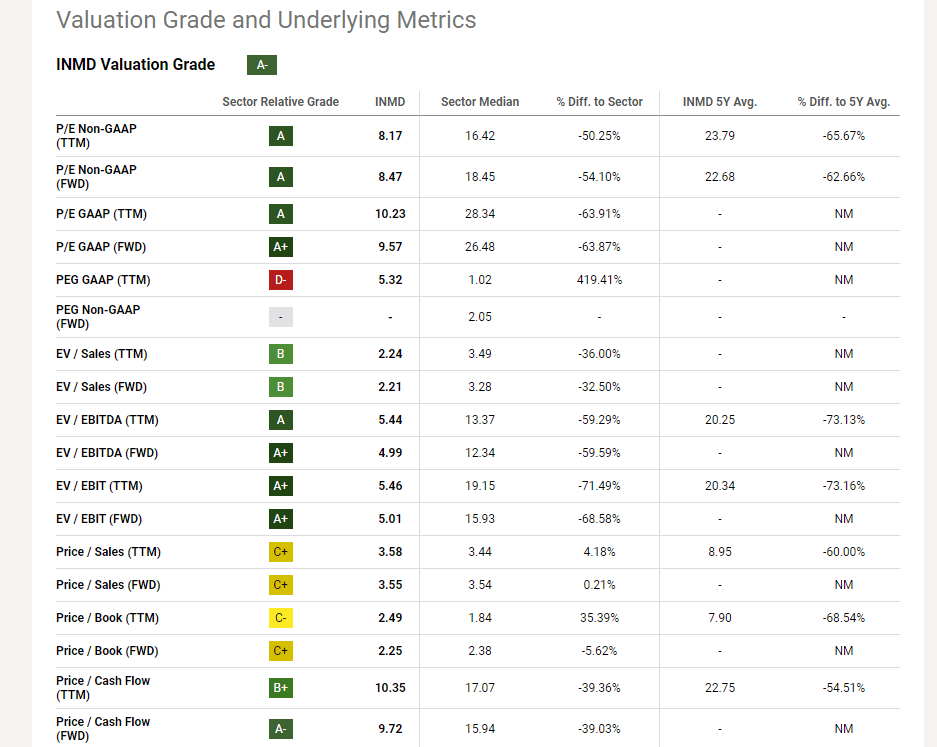

Furthermore, it's still trading at a considerable discount in all multiples relative to its peers. For example, it trades at a GAAP P/E multiple of 10x earnings, well below the peer average of 28x. In addition, its P/Cash Flow ratio is sitting at a whopping 9.72x, which remains undervalued compared to the industrial average of 15.9x. This provides an excellent buying opportunity for investors seeking exposure to value play.

Potential Risks

Despite its solid financials and underappreciated valuation, there are still some underlying risks behind the business that are worth considering before you invest.

1. "Higher for Longer" Interest Rate narrative

First, the high-interest rate backdrop has already hammered InMode's Q3 revenue. The higher interest rate (14-15%) makes it implausible for physicians and medical clinics to finance the leasing or purchasing InMode's aesthetic equipment. As a result, most physicians have cut back on their capital spending. Worse still, the tightening of credit conditions in Europe and the US makes it more arduous for clinics to borrow money from banks to finance their purchases. These headwinds will inevitably lead to a slowdown of growth in revenue in 1H 2024, as expected.

However, despite the " Sea Change " high-interest narrative suggested by Bill Ackman and Howard Marks, I still think that the Federal Reserve will cut rates starting from 2H 2024 to alleviate the unsustainable high borrowing costs. With the eventual normalization of interest rates in 2025, I expect InMode to eventually rediscover its growth lustre, given its strong product ecosystem and robust distribution network.

2. Questionable Management

While I appreciate the fact that the management team has the depth of experience working in the Medical Aesthetic Industry for more than 2 decades long of experience on average. However, whether the company has a shareholder-friendly CEO remains questionable; for example, the management team hesitated to repurchase shares and return value to shareholders via dividend payouts . Lamentably, stock-based compensation and the number of share counts have increased gradually over the past few years.

While I think the company is superb both in terms of growth prospects and financials, the management team is the most significant internal risk that I would contemplate as a value investor.

Conclusion

Upon researching the company's fundamentals, I think that InMode Ltd is undervalued apparently and remains well-positioned for future growth, supported by the company's secular revenue and earnings growth over the past 5 years, alongside its solid balance sheet with ample amount of cash and no debt. I also love the fact that the company can grow its free cash flow almost every year, making the company a strong cash cow.

Given its trading at a 3-year low P/E multiple, with a modest 40 % upside potential despite super conservative assumptions, I rate InMode Ltd as a great "Buy", offering a solid risk-to-reward perspective.

For further details see:

InMode: A Niche Medical Aesthetic Devices Player With Solid Financials