INGXF - Innergex: Very Weak Q4 But Shares Still Look Undervalued

Summary

- Innergex's Q4 and 2022 results were lower than expected, mainly due to weak hydro energy production.

- Free cash flow has been growing at a ~13% CAGR, and the company has visibility as to where most of the growth will come from to reach the 2025 target.

- Shares are trading at ~13.7x estimated FY2025 free cash flow, which we believe is a very attractive valuation.

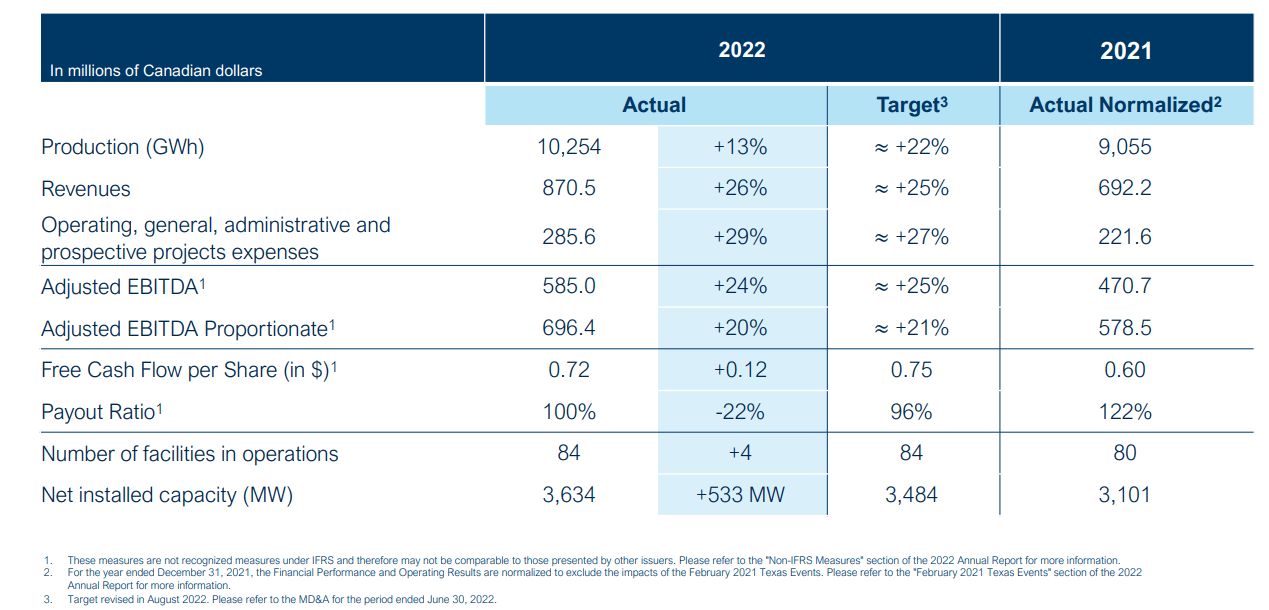

Innergex ( INGXF ) just reported an extremely weak Q4, with energy production decreasing ~9% y/y, which sent shares down by a significant amount. Disappointing energy production was mainly the result of exceptionally low hydrology levels in British Columbia during the fourth quarter. It also didn't help that maintenance costs at some of its hydro facilities were higher, and that other segments also had lower than expected generation in Q4, and for the year as a whole, compared to the long-term average .

Despite these headwinds, the company delivered growth in 2022 compared to 2021. Production was up 13% and revenues up 26%, mostly as a result of acquisitions. These included the remaining 50% interest in Energia Llaima and San Andres, Lican and Aela in Chile, as well as Curtis Palmer in the US. The increase was also the result of the commissioning of the Griffin Trail and Hillcrest facilities, among other factors.

Innergex Investor Presentation

{kind=link}

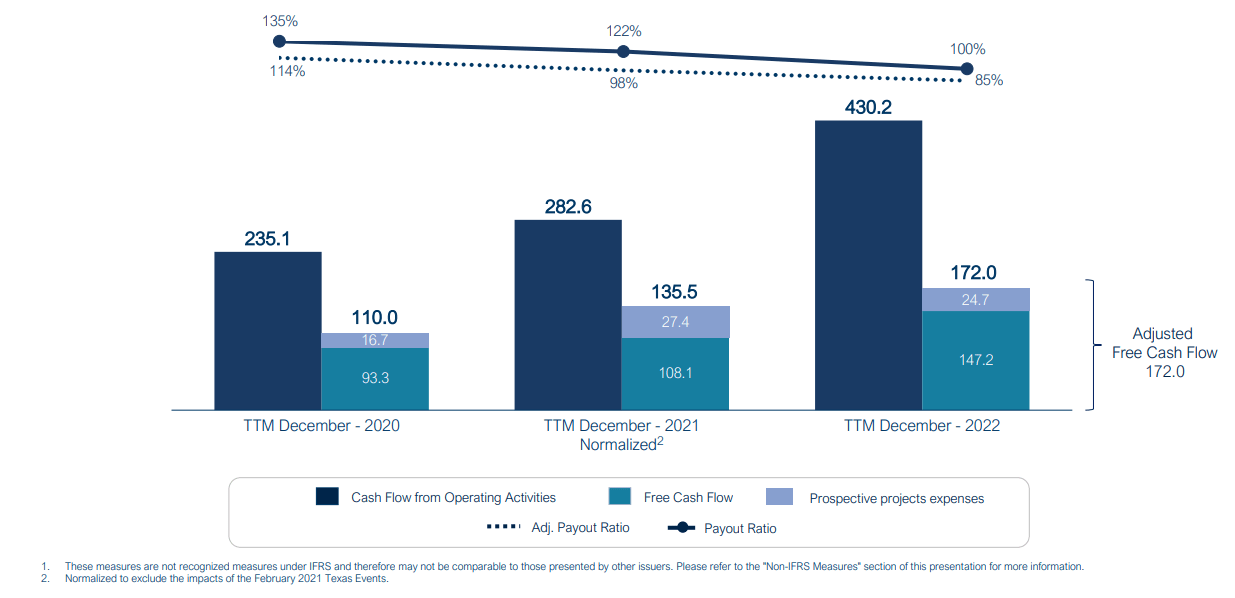

One of the most interesting comments during the earnings call , in our opinion, resulted from an analyst asking what the payout ratio would have been assuming production in 2022 had been closer to the long-term average. While management did not respond directly to the payout question, it did provide an idea of how much higher revenues could have been. We can compare these amounts to the C$147 million in free cash flow it generated in 2022, and it seems that the extra revenue would have very meaningfully improved the payout ratio.

I guess just approximately, like if we had like work to the long-term average, and using just a very rough average pricing range, obviously it depends on which area you produce, but we'd have probably something more in the $40 million to $50 million more revenues if we had hit the long-term average.

Payout Ratio

Something that many investors like about Innergex is that it pays an attractive dividend. Read our previous coverage on INGXF here. It pays a quarterly C$0.18 dividend, or roughly $0.13 in US dollars, which at current prices yields approximately 5.2%. The dividend is increasingly well-covered, though the payout ratio remains quite high at ~100%. It would have been lower had the company produced energy in 2022 closer to its long-term average. The adjusted payout ratio is a bit lower at ~85%, and it basically adds back ~$24 million of prospective project expenses. Still, it is good to see that despite the headwinds in 2022, the payout ratio is trending in the right direction.

Innergex Investor Presentation

{kind=link}

2025 Free Cash Flow Target

One of the key metrics for Innergex is free cash flow per share. During the most recent earnings call the company reiterated its C$1.01 per share free cash flow target for 2025.

This means that the company has to add ~C$0.29 per share to what it delivered in 2022 to achieve its target. It expects ~C$0.24 per share to come from recent acquisitions, inflation adjustments to its power purchase agreements, and projects under construction and under development. The company currently has 368 MW of projects under construction, and 85 MW of battery systems that should come online soon. The projects currently under construction are expected to be in service by the end of 2024, some even in 2023. The remaining C$0.05 per share is expected to come from existing advanced stage greenfield developments, or new M&A activity.

Balance Sheet

Innergex remains committed to maintaining a Fitch investment grade credit rating of at least BBB-. Only around 8% of its consolidated debt has floating interest rates, but there will be an impact from rising interest costs, mostly on refinancing and on the revolving credit facility. CFO Jean Trudel explained the potential impact of higher rates on the revolving credit facility during the Q&A session:

So we have about $400 million that's unhedged on the corporate facility. So right now, we're expecting rates, I mean, we've expected rates as we've seen them in, I guess, since November. So it hasn't moved much upward. But of course, if rates were to increase, while you can do the math like [rate], every 1% would be a $4 million headwind to us.

Something we appreciate is that the debt is relatively well matched to the average power purchase agreements' remaining life. The company said that its weighted average debt maturity equals the weighted average PPA remaining life of ~13 years, versus a weighted average useful life of 37 years for its assets.

Regarding the useful life of its assets, the company shared some interesting details. It believes its hydro assets to have a useful life of ~75 years, solar assets ~35 years, and wind assets about 30 years. The company also believes that these assets will retain some value even after this period of time.

Guidance

Innergex did not provide guidance for 2023, instead asking investors to focus on the 2025 target. The ~330 MW Boswell project is going to be a significant contributor to cash flow, and is going to come online in 2024, and the battery projects are also expected in late 2024. This year the company does not have many projects commencing operations, which is why the company is not putting much emphasis in 2023. Still, the company did say that if they have an average year in terms of production, without any unforeseen events, the payout ratio should be slightly better than it was in 2022.

Valuation

Despite the disappointing results for Q4 and 2022, we still believe shares are meaningfully undervalued. Shares are currently trading at roughly C$13.85, or ~$10.12. Shares are therefore trading at ~13.7x estimated FY2025 free cash flow. We believe this is a very attractive valuation for a company that is growing free cash flow at a ~13% CAGR.

Innergex Investor Presentation

Risks

As Q4 results showed, Innergex is exposed to energy production variability due to weather and other uncontrollable factors. In theory this should be compensated with other years producing energy at above average rates.

The company also has very significant debt and leverage. This risk is mitigated by the fact that the company has power purchase agreements that roughly match the debt duration.

Conclusion

Fourth quarter and 2022 results were lower than expected in terms of production. Hopefully hydro conditions don't signal a trend, and were just an anomaly. Importantly, the company reaffirmed its 2025 free cash flow per share target of C$1.01. Despite the weak results, we believe that shares are currently undervalued trading at ~13.7x estimated FY2025 free cash flow. Free cash flow has been growing at a ~13% CAGR, and the company has visibility as to where most of the growth will come from to reach the 2025 target. While we are disappointed with the recent results, taking a longer term view we are reaffirming our 'Buy' rating.

For further details see:

Innergex: Very Weak Q4, But Shares Still Look Undervalued