INOD - Innodata: Strong Guidance On New Customer Deployments Ramp Appears Imminent

2023-12-08 10:00:51 ET

Summary

- Innodata is an undiscovered AI data engineering company with strong Q3 2023 results and projected revenue growth of over 50% in 2024 and 30%-plus in 2025.

- The company's revenue growth is re-accelerating, with Q3 2023 revenues up 20.2% YoY and expected Q4 revenues of $24.50 million or higher.

- Innodata has now secured major business agreements with five out of the ten largest technology companies, indicating a significant presence in the tech sector.

- The company's white-label program appears to be ramping at a significant pace.

Today, I am reiterating a "buy" rating on Innodata Inc. ( INOD ) with an initial price target of $22.70 on the company's strong Q3 2023 results. This rating reiteration and new price target builds on my establishing article which was published on the 10th of October, 2023.

Thesis

Innodata continues to be an undiscovered artificial intelligence ((AI)) data engineering company whose revenues are set to double as major contract wins accelerate and deploy. With revenues projected to grow by over 50% in 2024 and another 30+% in 2025, the company's forward price to sales ((P/S)) ratio is now only 1.26, which is significantly below the valuations of comparable private AI data engineering companies like ScaleAI .

Financials Re-accelerating

In my view, a key factor contributing to the suppressed performance of Innodata shares in recent quarters has been the superficial comparison of revenues between the first half (1H) of 2023 and 1H 2022. At first glance, this comparison suggests a stagnation in the company's revenue growth. However, this is a partial view. In 2022, Innodata's quarterly revenues saw a notable increase, primarily due to contributions from a major social media company, which I believe to be Twitter. This boost was temporary, as the social media company halted its funding following a 'significant management change' coinciding with Elon Musk's takeover and immediate decision to not pay vendors and landlords. This cessation of funds from this key customer significantly impacted Innodata's year-over-year (YoY) revenue growth in the first two quarters of 2023. Nonetheless, discounting the revenues from this specific customer, Innodata achieved an approximate 12% increase in its revenues in the first half of 2023 compared to the same period in 2022.

In Q3 2023, the company's underlying business has finally outgrown the unfortunate loss of the social media company and has now eclipsed its 2022 revenue levels.

Innodata Public Filings, Q4 Guidance

The company's revenue growth is now re-accelerating with Q3 2023 revenues up 20.2% over the same period in 2022, with management expecting Q4 revenues of $24.50 million or higher, a year-over-year increase of 26.5%.

Innodata Public Filings, Q4 Guidance

The Q4 guidance now puts the company's expected FY 2023 revenues at $85.20 million or higher, marking a 7.8% increase over FY 2022. In my view, this resurgence in the company's revenue growth is just the start. It establishes a strong foundation for significant future growth. Over the past year, Innodata has achieved important strategic milestones in collaboration with some of the world's largest technology companies. Many of these partnerships have yet to substantially impact the company's revenue, suggesting potential for further growth.

Innodata Public Filings, Earnings Presentations, Projections are Author's Calculations

The company has also seen significant financial improvement on an adjusted EBITDA basis, with the metric increasing 101% over Q2 2023. If Innodata achieves its adjusted EBITDA guidance of $3.7 million in Q4, it would represent an increase of 362% since Q1 this year, demonstrating impressive operating leverage gained on revenue growth of 30% in the same period.

Performance by Segment

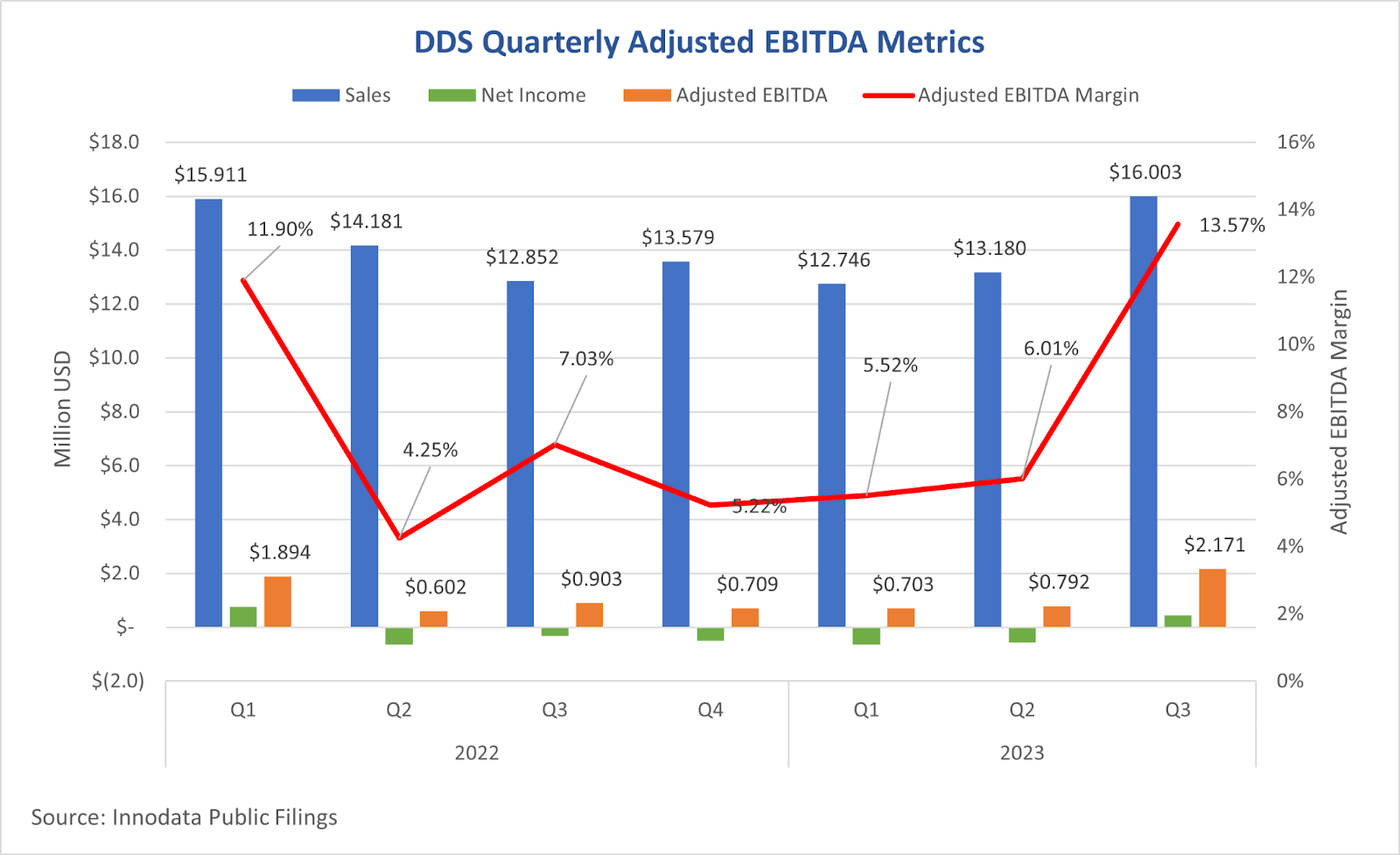

In Q3 2023, Innodata's Digital Data Solutions ((DDS)) segment contributed an impressive 72% of the quarterly revenues, up from 67% in Q2 2023. The DDS segment is the core of Innodata's AI-focused operations. Through DDS, Innodata offers AI data preparation services, including the collection and creation of training data, data annotation, and AI algorithm training. This segment, particularly important for the company's dealings with its 'Big Five' customers, is a key area of growth and strategic focus for Innodata.

Innodata Public Filings Innodata Public Filings Innodata Public Filings

{kind=link}

After overcoming the decline in DDS revenue following the Twitter-related slump, Innodata is experiencing a resurgence in this segment. In Q3, we observed a re-acceleration in DDS revenues, which increased by approximately 21% over Q2 2023. Additionally, the segment's adjusted EBITDA margin saw a remarkable increase of around 126%. In my view, this demonstrates the beginning of the operating leverage in the DDS segment, which I believe will be a key aspect of the bullish investment thesis for the company moving forward.

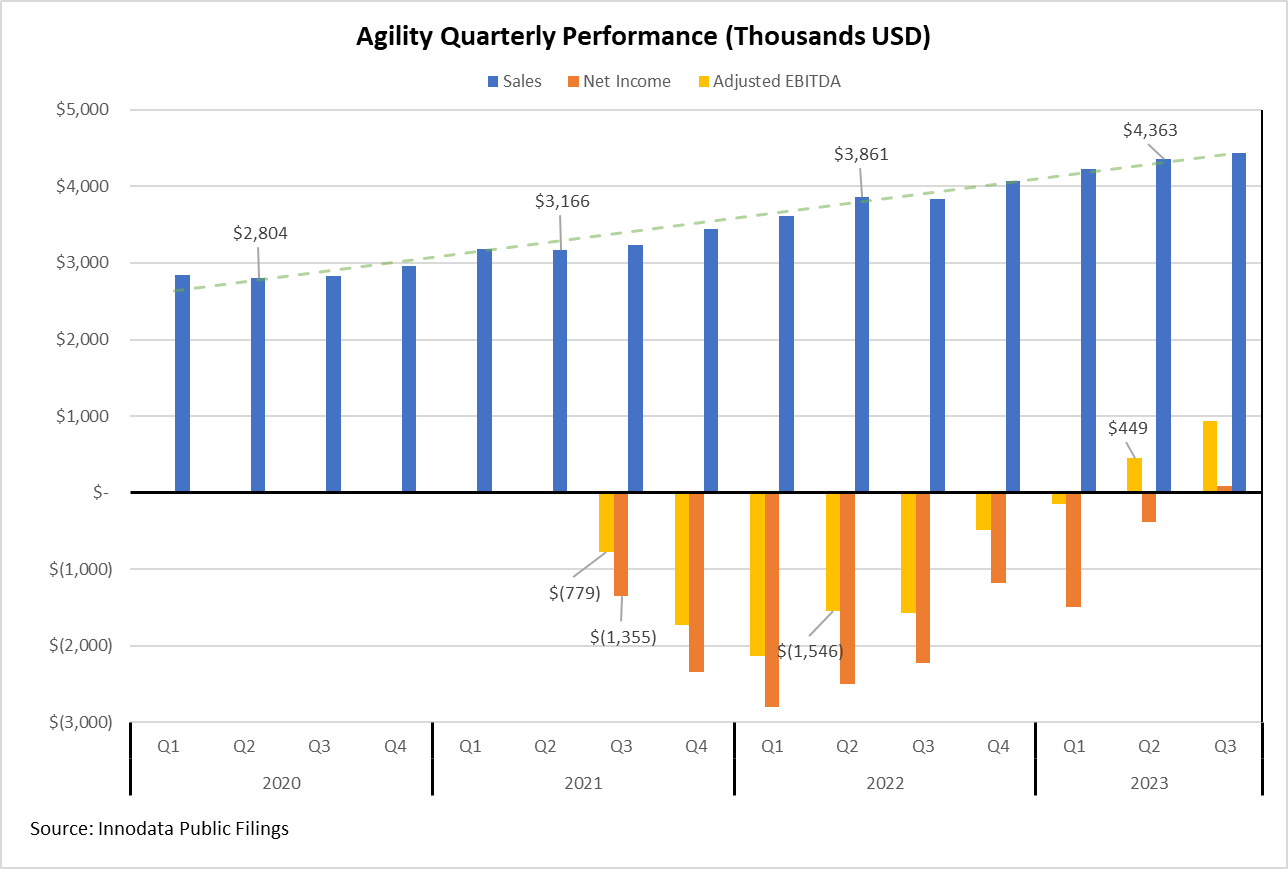

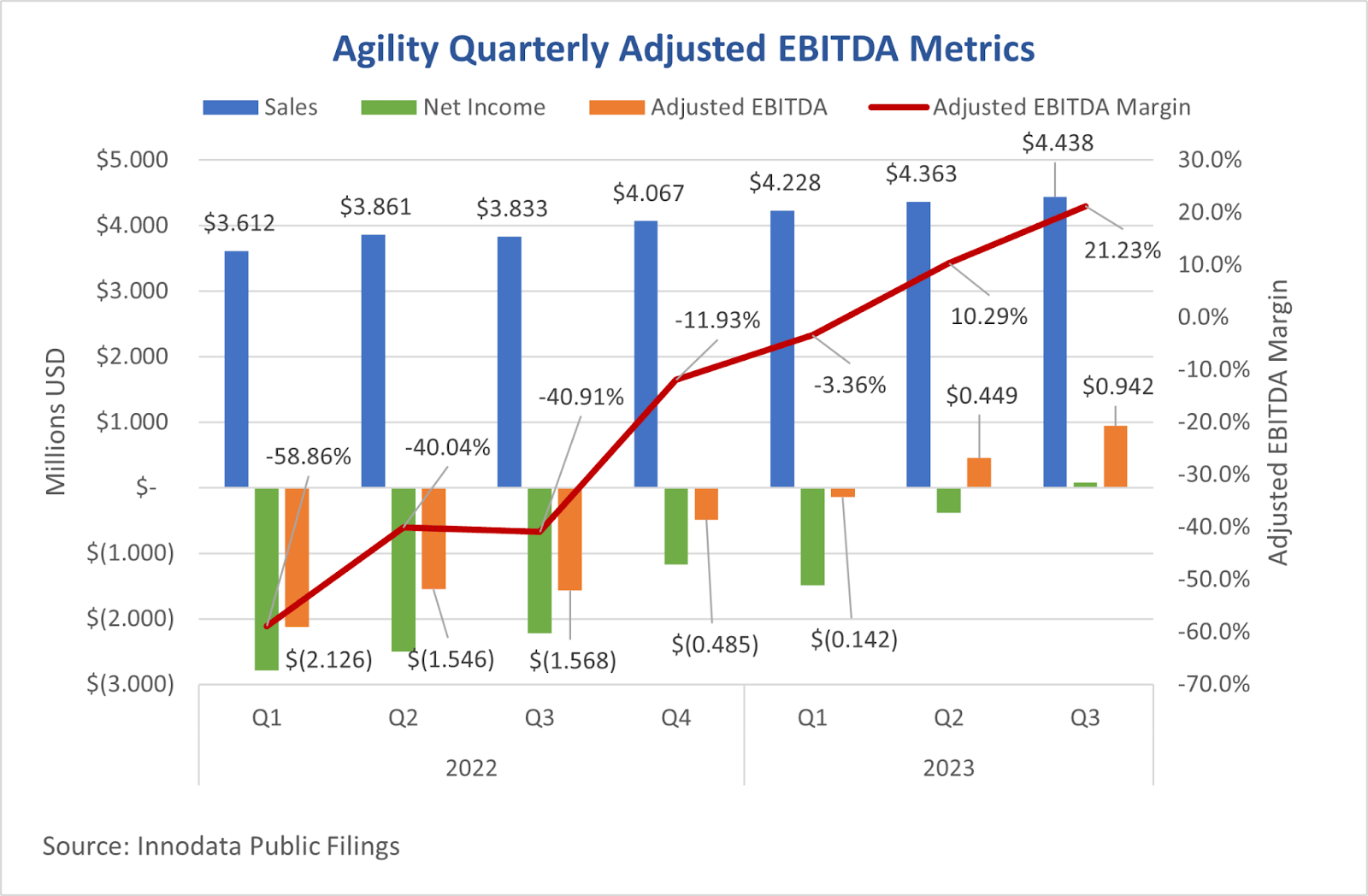

Innodata's second major revenue contributor is its Agility platform, catering to marketing and public relations professionals by offering tools for audience targeting and content distribution. This segment has not only grown but also achieved positive net income in the quarter. Furthermore, it has maintained a positive adjusted EBITDA for two consecutive quarters.

Innodata Public Filings Innodata Public Filings

{kind=link}

{kind=link}

Much like with DDS, Agility's operating leverage is beginning to be realized, with the segment's adjusted EBITDA margin increasing by 106% while revenues increased by 1.72% in the same period.

Business Agreements

As mentioned earlier, Innodata's successful major business agreements with the world's largest technology companies serve as a key validation of our investment thesis. Before the Q3 2023 earnings release, Innodata announced its collaboration with four out of the five largest technology companies by market capitalization. This impressive achievement allows us to infer that Innodata had secured business with all but one of the following giants: Apple Inc. ( AAPL ), Microsoft Corporation ( MSFT ), Alphabet Inc. ( GOOG ), (GOOGL), Meta Platforms, Inc. ( META ), and Amazon.com, Inc. ( AMZN ).

To illustrate this point, a slide from Innodata's 1H 2023 investor presentation effectively showcases the company's track record in securing program agreements with these 'Big Five' technology firms.

Innodata 1H 2023 Investor Presentation

Interestingly, the company changed this exact slide in its most updated investor presentation to now include the 10 largest global technology companies by market capitalization.

Innodata 2H 2023 Investor Presentation

I am inclined to assume that Innodata expanded its customer list to protect the privacy of its clients, which could now include all of the 'Big Five' tech companies. This is speculative, but if accurate, it would indicate that Innodata has established relationships with each of the top technology firms. This speculation aligns with the recent announcement on the Q3 earnings call of a master services agreement for AI development with "another of the world's largest tech companies." Such developments, if confirmed, would underscore Innodata's significant presence in the tech sector.

White Label Ramp

The white-label service provided by Innodata through an existing 'Big Five' customer, referred to as "the cloud hyperscaler," remains an overlooked aspect of Innodata's future revenue potential. This program enables Innodata to offer its AI data annotation and Large Language Model (LLM) fine-tuning services to the hyperscaler's extensive customer base. Last quarter, it was announced that nine end customers had started pilot programs through this service. At that time, Innodata's management expressed high confidence that these pilots would likely evolve into substantial business agreements.

A quarter later, we are witnessing the program's expansion. During its Q3 2023 earnings call, Innodata reported an expected revenue of approximately $330,000 from the white-label program, involving six won or late-stage opportunities. Additionally, management provided insights into the program's potential growth into 2024. They mentioned several million dollars in pipeline opportunities slated to close in Q1, including two major deals valued at $2 million and $1 million, respectively.

While this marks just the onset of a potential surge in white-label contract revenues, the anticipated increase from $330,000 to at least $3 million in a brief period suggests a significant growth trajectory that may surpass many expectations. Moreover, I had not factored the revenue from this program into my initial financial model for Innodata. The development of this program in the upcoming quarters is something I am keenly looking forward to, and as its growth rate becomes clearer, I will incorporate it into my future financial projections for the company.

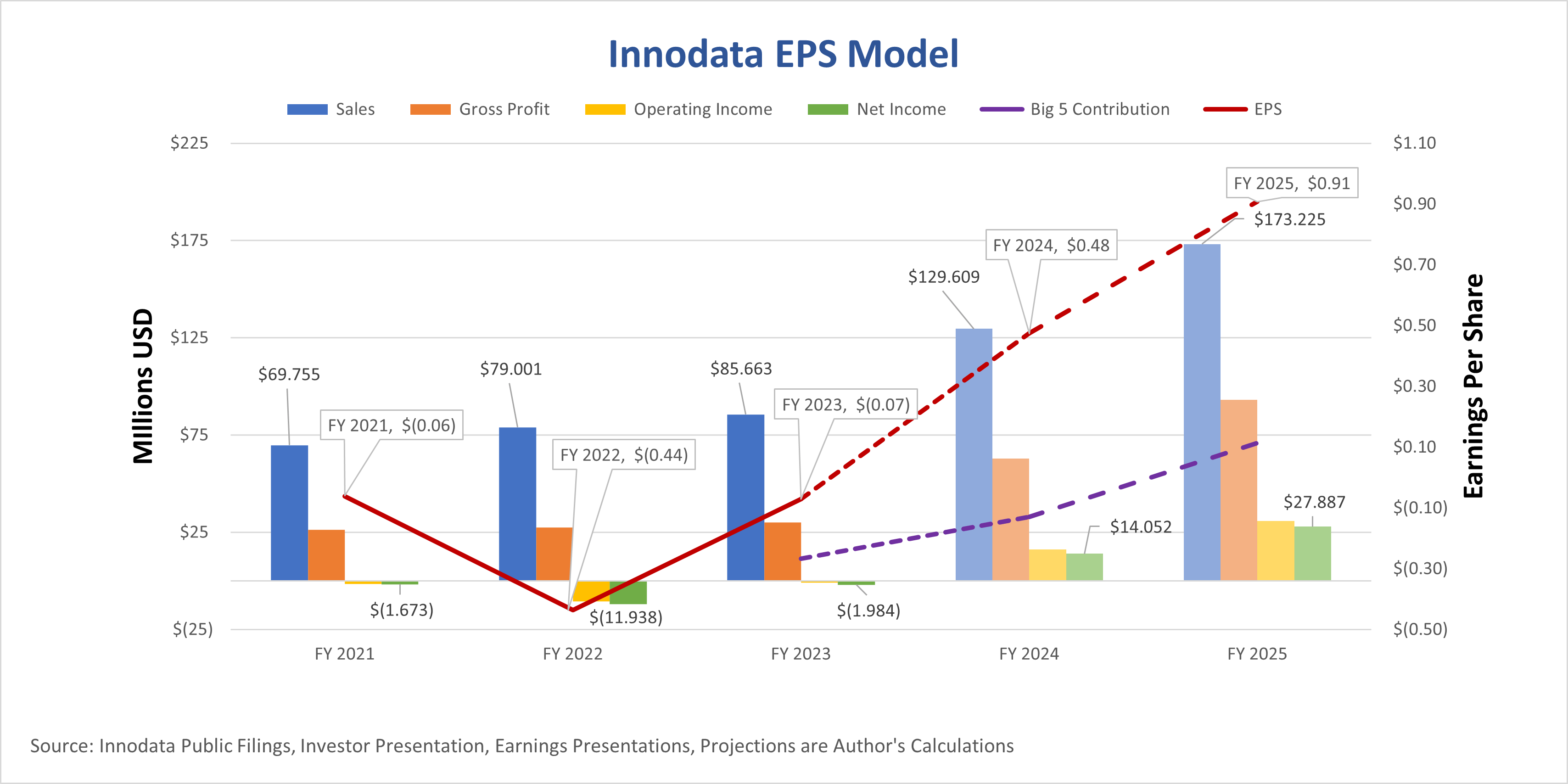

EPS Model

Considering that the company has recently emerged from a period marked by revenue growth volatility, largely due to the loss of Twitter as a client, I believe it's prudent to approach the FY 2024 and FY 2025 Earnings Per Share ((EPS)) estimates in a conservative and high-level manner initially. This approach allows for a gradually refined forecast as more concrete guidance emerges from the company, particularly regarding the revenue growth expected from contracts with the "Big Five" tech firms. As we receive more detailed projections from the company, expect these EPS estimates to gain increasing clarity.

Innodata Public Filings, Investor Presentations, Earnings Calls, Projections are Author's Calculations

{kind=link}

In the development of this EPS model, I have relied on a set of assumptions that draw from the company's past performance, its potential for future growth, and the financial guidance provided for Q4. The excerpt below details the methodology I used to arrive at the financial projections shown above. It's important to note that these projections are based on my analysis and interpretation of available data, and are not official forecasts issued by the company.

Innodata Public Filings, Earnings Calls, Investor Presentations, Calculations and Assumptions are Author's

With revenues now accelerating and significant new contributions expected from the Big Five contracts in the next year, I project a conservative yearly growth rate of 12.78% for the company, excluding the Big Five contracts. Additionally, I anticipate revenue contributions from the Big Five contracts to be $33 million in 2024 and $71 million in 2025. This leads to our revenue estimates of $129 million for FY 2024 and $173 million for FY 2025, representing increases of 51% and 34% over FY 2023 and FY 2024, respectively. The company's cost of revenues has historically increased by an average of 13% annually. I've projected a 20% yearly increase to support the expected growth, resulting in the gross profit figures outlined in the accompanying table. Operating expenses, as a percentage of revenues, have decreased by an average of 2.9% sequentially since Q1 2022. Using an average of recent quarters, operating expenses amount to approximately 36% of revenues. After accounting for operating expenses, tax provisions, non-controlling interests, special items, and share count increases, we reach the net income and EPS figures displayed in the chart above. Based on these results, I estimate an FY 2025 forward price-to-sales P/S ratio of 1.26x and a price-to-earnings ((P/E)) ratio of 8.87x. This P/S ratio of 1.26 is compared to ScaleAI, a private company believed to be valued at 29.2x sales. Applying a 25x P/E multiple to a company expected to grow its revenues by over 100% through 2025 seems reasonable. This calculation leads to a target share price of $22.7 or a P/S of 4.02, representing an increase of 184% over the current closing price of $8.05.

Risks

Though the business and its prospects appear stronger than ever, the risks surrounding Innodata have not changed and should be considered by investors. The following risk section is quoted from my October 10th establishing article on the company.

Competition: Innodata has demonstrated a strong competitive advantage thus far, having been selected and validated by the Big Five tech companies from a large pool of competitors. Innodata must continue to leverage and expand upon its first-mover advantage while also continuing to demonstrate that its data engineering and applied AI program is superior.

Termination or loss of business from the Big Five: As the most significant drivers of revenue growth over the next year or so, any loss of these contracts would pose a threat to the bullish thesis on Innodata.

Contract sustainability: I believe a key focus for investors must be contract sustainability. These large deals are transformative, but how these agreements will expand beyond the initial work must be monitored closely.

Opportunities

Revenue Ramp: The expected revenue contribution from the company's major contracts is still being underestimated by investors. Moreover, the company's white label program, not included in my financial projections, could start significantly impacting revenue as early as the first half of 2024. This program has the potential to surpass my current revenue estimates.

Under the Radar: Currently, the company remains relatively unnoticed by many investors, analysts, and institutions. Despite its low profile, the company's shares seem attractively priced, especially when considering the substantial growth anticipated in 2024 and 2025, along with the valuations of comparable companies.

Conclusion

Innodata presents a compelling investment opportunity, characterized by its strong growth prospects and undervaluation in the market. The company's recent emergence from a period of revenue volatility, primarily due to the loss of a major client, has set the stage for a robust return to growth. This resurgence is further bolstered by the significant revenue potential from contracts with the world's largest technology companies, the "Big Five." Additionally, the white-label program, which is yet to be factored into my projections, holds the promise of boosting revenues as early as the first half of 2024.

Despite these positive indicators, Innodata remains largely under the radar of many investors and analysts, offering an attractive entry point for those looking to capitalize on the company's growth trajectory. With the company trading at a modest price-to-sales ratio compared to its private sector counterparts and showing promising signs of revenue growth and operational efficiency, the outlook for FY 2024 and FY 2025 is notable. The company's strategic positioning, coupled with its expanding market presence and the anticipated ramp-up in contract revenues, positions Innodata as a potentially undervalued stock with significant upside potential.

For further details see:

Innodata: Strong Guidance On New Customer Deployments, Ramp Appears Imminent