INVZW - Innoviz: Reaching An Inflection Point In 2024

2023-12-19 07:41:06 ET

Summary

- The transition of the BMW Gen1 program to SOP marks a significant milestone for Innoviz and differentiates the company from competitors.

- Innoviz is looking to expand its opportunity with Volkswagen, with advanced discussions ongoing for exploring multiple platforms within the Volkswagen Group.

- More than half of the 10 to 15 programs in the pipeline are in the RFQ stage, with three progressing well into the final stage.

- Capital raise was a key factor in accelerating these three RFQs into the final stage, along with extending the financial runway.

- Management expects the current cash position to bring Innoviz well into 2025, with additional $150 million to $250 million in NREs, the RFI and RFQ pipeline will further extend the runway.

Innoviz Technologies ( INVZ ) once again showed why it deserves a place in the portfolio.

I am amazed by the level of execution that management has demonstrated since listing, which adds to the conviction level I have in the company.

First SOP

Innoviz hit a rather significant milestone in 3Q23 as it transitioned the BMW Gen1 program into SOP phase.

This met management's target of getting the BMW program to SOP in the second half of 2023, which adds to the credibility of management's targets and execution.

This was achieved in the first few weeks of the third quarter, with the components being shipped to Magna for final assembly, before it is then delivered to BMW for installation on the 7 Series.

On top of that, Innoviz also managed to deliver the final SOP-ready version of its perception software in the 3Q23 quarter, which will be installed in the 7 Series vehicles.

The BMW Gen1 program reaching SOP is a huge milestone given it is the first SOP for Innoviz involving InnovizOne.

While I did have some uncertainties as to whether the company was able to achieve this milestone when it first listed, the fact that management was able to achieve this on target and according to the timeline does suggest that the competence of the team at Innoviz.

Also, other OEMs that may or may not yet be customers of Innoviz may then look at this and have greater confidence in the company being able to reach SOP and achieve their targets. Given that Innoviz is one of, if not the first, LiDAR player to reach SOP, this does differentiate the company from the competition. For reference, Luminar ( LAZR ) is another company that is expected to SOP soon with Volvo Cars in 2024.

With this BMW Gen1 program transitioned to steady state manufacturing, this gives management more time and energy to focus on converting the RFI and RFQ pipeline into actual program wins.

SOP of the Shuttle program

Innoviz will be moving the full Level 4 Shuttle program into the SOP stage at the end of 2023.

The significance of this customer is that it is a full Level four program, thereby providing Innoviz with a customer in the autonomous shuttle market that is likely to gradually replace legacy public transportation in some areas.

Given that the Shuttle program is a Level 4 program, it can deploy anywhere between three to six LiDARs per vehicle.

For this Shuttle program, the initial plan was to incorporate four LiDARs per vehicle, but that has since moved towards a six LiDAR configuration, with two more LiDAR units on the sides of the Shuttle for a wider field of view.

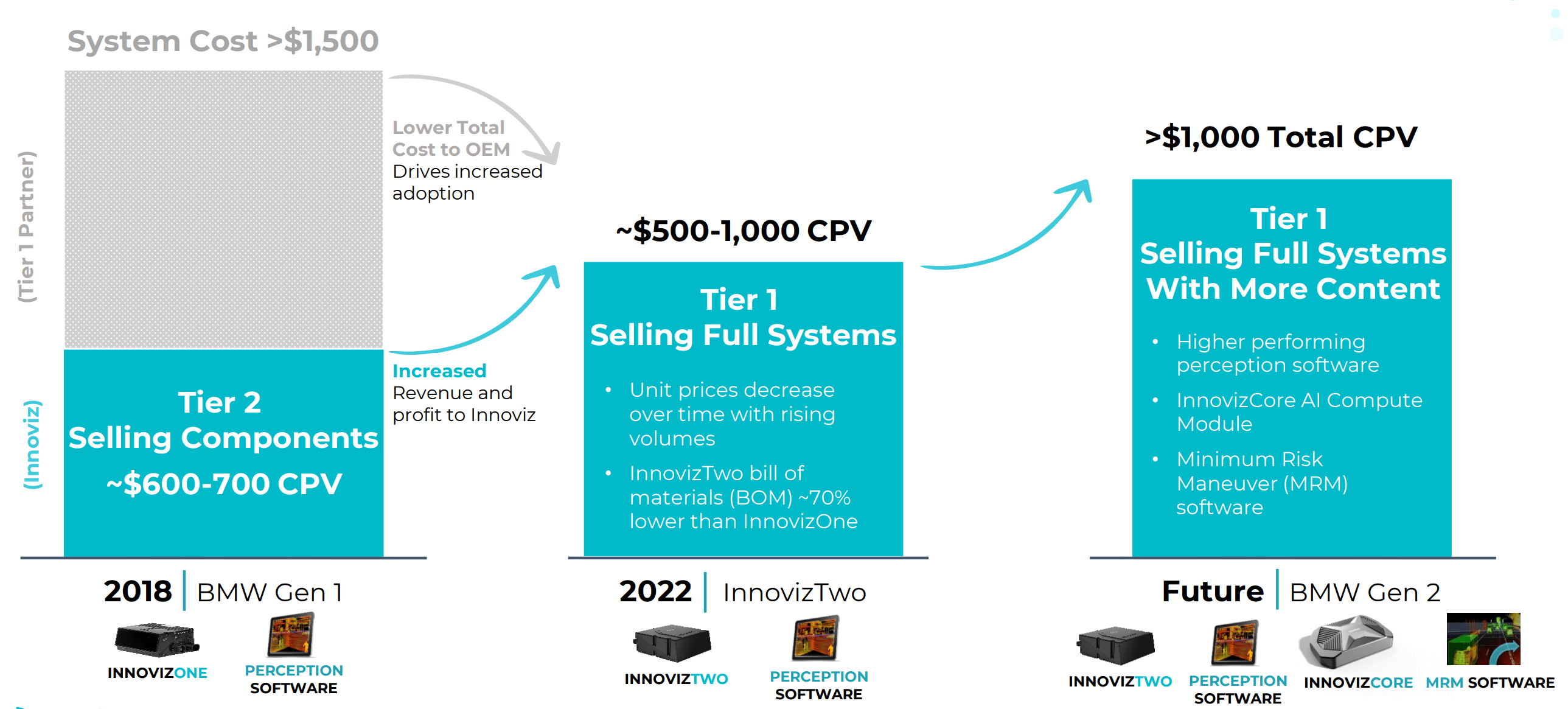

Improving content per vehicle and margins with the BMW Gen2 program

Innoviz is now working on the BMW Gen2 program, which started development last quarter.

This naturally is built around InnovizTwo and also the AI-enabled perception software.

I think the BMW Gen2 program is a good example to show how Innoviz can improve both the margin profile of its business and the content per vehicle over time.

For BMW Gen1 program, this win was contracted a long time ago in 2018, when Innoviz was operating as a Tier-2 supplier. As a result of the old Tier-2 structure, Innoviz sells the components to Magna, and Magna then integrates it into a finished LiDAR to BMW. As a result, this involves an intermediary, that is Magna, and Innoviz only captures a part of the total system value.

Today, Innoviz is a Tier-1 supplier, meaning that it not only improves the economics by ensuring it sells the full systems, but it also increases the non-recurring revenues that is available to the company.

For the BMW Gen1 program, Innoviz was capturing a portion of the total system value, approximately $600 to $700 per vehicle.

As BMW Gen2 program moves from InnovizOne to InnovizTwo, the bill of material for InnovizTwo is 70% lower than InnovizOne due to multiple breakthroughs in technology and engineering.

As a result of this massive reduction in cost, this also led to more design wins and pipeline activity for Innoviz as the lower costs meant higher LiDAR adoption.

The key here is that with the pivot to being a Tier-1, along with other higher value and higher margin offerings like the perception software, the Minimum Risk Maneuver software and the InnovizCore AI Compute Module, Innoviz sees a path to bring content per vehicle from $600 to $700 per vehicle in the BMW Gen1 program, to more than $1,000 per vehicle in the future.

This is also achieved by improving the margin profile of the business given the higher software mix.

Increasing content per vehicle (Innoviz)

{kind=link}

Expanding the opportunity with Volkswagen

To even have Volkswagen as a customer is a huge deal for any LiDAR company, much less have multiple wins across the entire Volkswagen Group, given it is the second largest in terms of number of vehicles sold, with 8 million vehicles sold in 2022.

The current program with Volkswagen is expected to work towards a mid-decade launch, and it is progressing well, as it is currently within the B-Sample stage, looking to unlock better performance and functionality using the second-generation custom ASIC.

Innoviz is currently in advanced conversations with Volkswagen to explore the addition of multiple platforms, that will bring upside to the initial win.

It does seem management is optimistic enough to suggest that they may have something to share on this front in the next few quarters.

Anton Stippler, Head of LIDAR and Camera development at Volkswagen's CARIAD had this to say about Innoviz:

For future automated driving functions, we selected Innoviz as our LiDAR partner not only because of their automotive experience and technological expertise, but also for the flexibility and creativity that their team brings to the table.

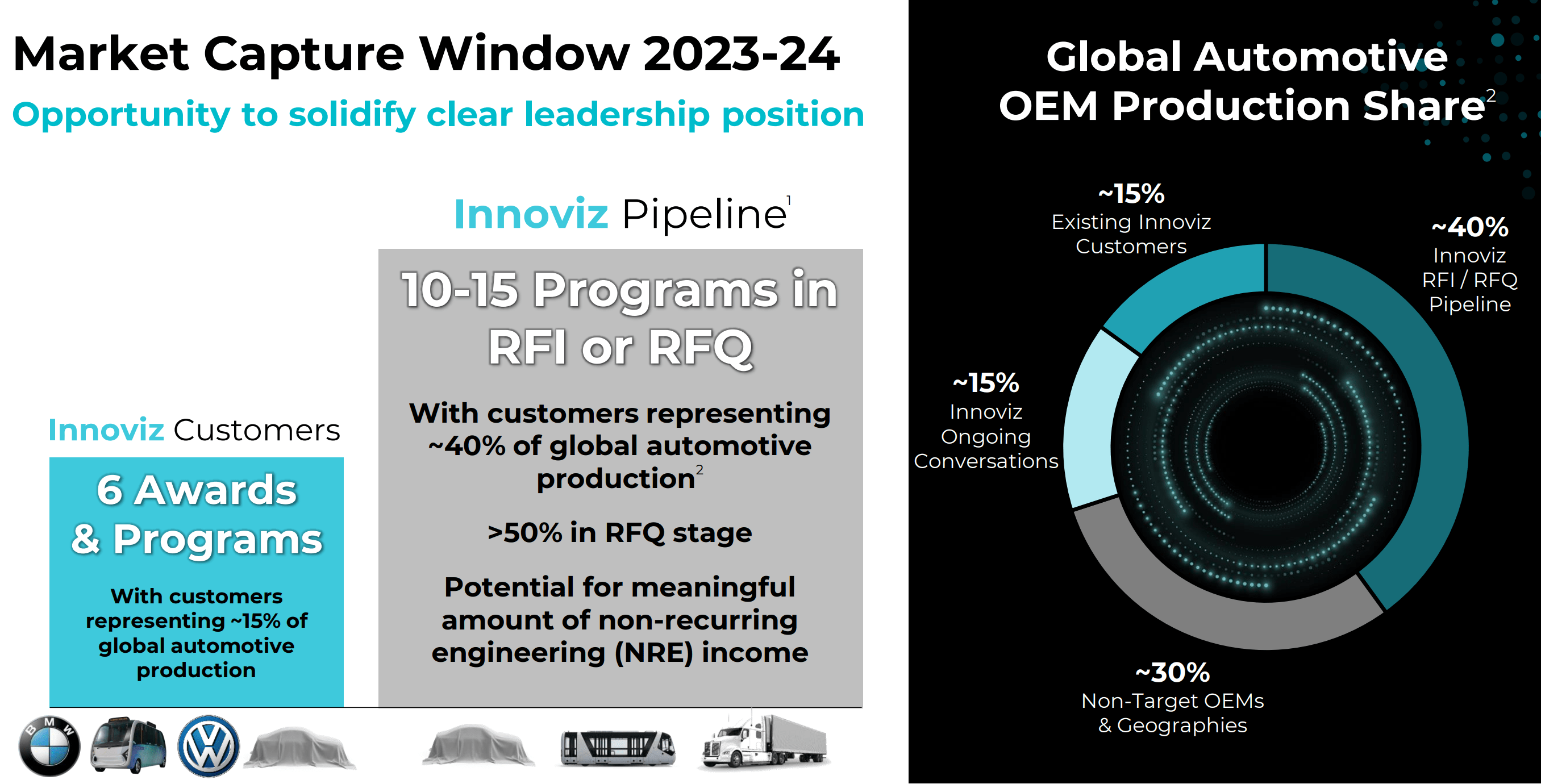

Pipeline

Innoviz's pipeline continues to strengthen in the quarter.

Recall that in 1Q23, the company had a record number of programs move from the RFI stage to the RFQ stage.

For those unfamiliar with the difference between the two, RFI stands for Request for Information, and RFQ stands for Request for Quotation.

As the name suggests, at the RFI stage, OEMs may just be testing the systems, but there is no real commitment to the program yet and there are programs that stay in the RFI stage for very long and yield no positive outcome.

In the RFQ stage, however, OEMs transition into this stage when they have made a decision to go forward with the program, commit to a certain timeline for production, made the decision to go into series production and thus, its vehicles will include the LiDAR.

To add to that, when transitioned to the RFQ stage, the OEM will also be more committed to the program by investing resources to the program, which includes engineering, supply chain, product management and finance teams being onboarded to the process.

Today, more than half of the 10 to 15 programs in the pipeline are in the RFQ stage, and that is a very big deal and implies not only that there is interest in Innoviz, but also that a decision could be imminent, and a favorable outcome is more probable.

Innoviz customers and pipeline (Innoviz)

{kind=link}

Also, Innoviz has already targeted OEMs amounting to 70% of the global OEM production share, including current customers, those in the pipeline and those who are having ongoing conversations with the company.

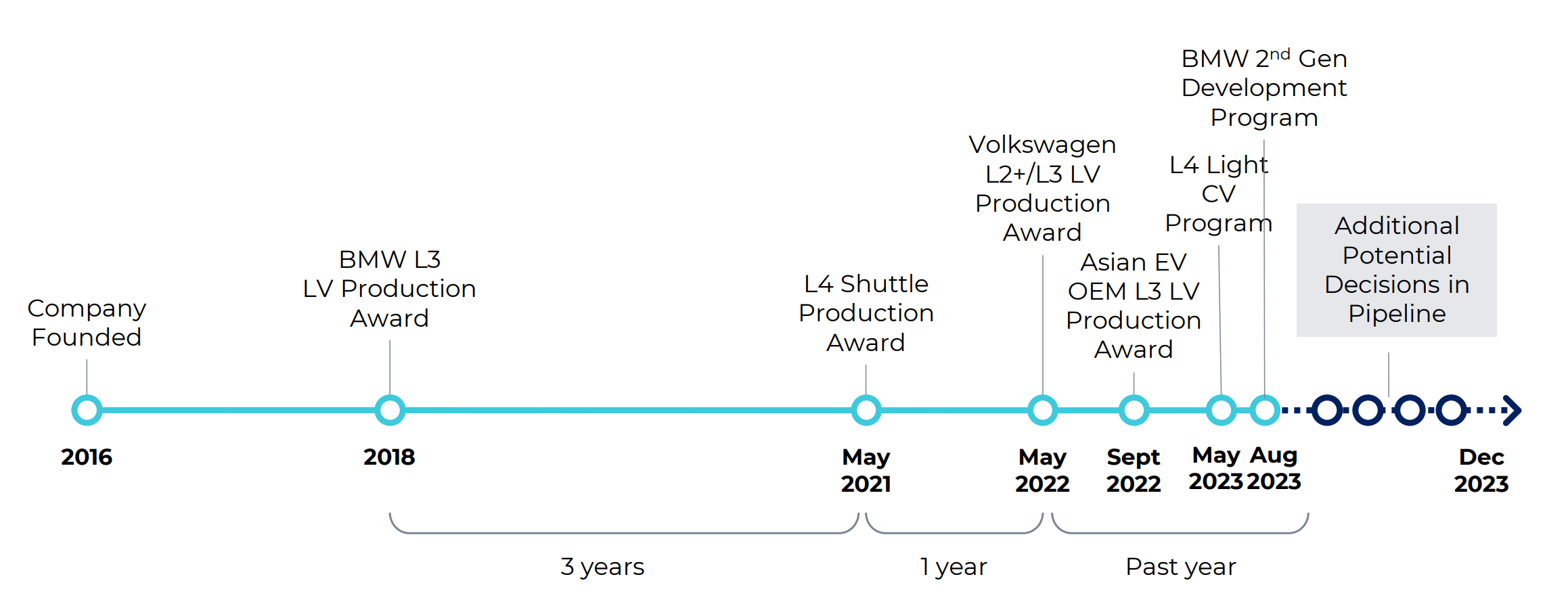

In terms of the progress that Innoviz has made, we can see that program wins have been accelerating lately, with the flywheel effect in full force.

Since founding in 2016, the first production award was won in 2018, and it then took another three years before the second production award was won for the L4 Shuttle program. In the past year, Innoviz won four other production awards, including the BMW Gen2 program, amongst others.

{kind=link}

In 3Q23, the main progress was that within the multiple RFQs it has today, there are three that are advancing at a faster pace and in the quarter, went through the financial audit and certification of high-volume manufacturing stage.

Thus, for these three programs, they have moved to the final stage that involves definitive price negotiations and detailed planning of the post-nomination milestones.

I am pleased with the pipeline updates for 3Q23. I don't think we can expect a program win each quarter, but rather, I will want to see continued and steady progress.

On that front, I think the three programs that are in the final stage signifies this progress and that there will therefore be announcements made in the near-term from these programs.

Within the three programs that are in the final stage, management expects that at least two of these three may make a decision by this year.

For the other RFQs in the pipeline, management also shared that they may make a decision between 1Q24 and 2Q24 .

Clearly, these are catalyst rich times for Innoviz.

Capital raise was necessary

Management also explained that the capital raise that brought in an additional $65 million in cash was essential for the progress that it has made, especially with the three programs that are moving faster and are in the final stage.

The capital raise was a necessary move for Innoviz because it needs to show these potential customers that it has a sufficient cash runway.

For Innoviz, its main competitors in these RFQs are actually not other pure-play LiDAR companies, but rather the more established Tier-1s. While these Tier-1s compete on their long operating history and stability, Innoviz competes on its technology.

Innoviz has been told often by its customers that its technology is better, so that is one tick in the box for Innoviz, and with the capital raise, this is another tick in the box for the company, which is then better able to compete on bids with Tier-1s given the longer cash runway.

The fact that Innoviz has been able to win customers like BMW and Volkswagen while Tier-1s have lost out suggests very strongly that the company has a very strong value proposition.

With the capital raise done, while it did bring some short-term volatility in the stock price, it did enable Innoviz to move into the final stage for the three RFQs mentioned above.

As a sign of confidence in the long-term potential of Innoviz, the management team, including the CEO and co-founder, and Chairman of the Board participated in the transaction and are thus invested alongside investors.

Product and technological improvements

Innoviz is on an innovation path and has been focused on its technology as its main advantage.

One example is its second-generation custom ASIC , which finished tape-out last quarter and it not only supports a much higher resolution, but also unlocks a configuration that would bring about a higher maximum detection range of 450 meters, up from 300 meters. On top of that, the more powerful chip can process two times the total number of points per second than the earlier generation, thus powering a higher density point cloud with improved resolution.

With small improvements like this more powerful chip in both its sensor and software suite, this helps further differentiate its technological advantage and advance the conversations that it has with OEMs.

3Q23

Innoviz ended 3Q23 with $164 million in cash in its balance sheet.

As the company's cost structure is relatively mature, its operating cash outlays have been stable during the quarter, and it has remained flat since the second half of 2022. The majority of the growth in the cost structure was a result of the transitioning from a Tier-2 to a Tier-1 in 2022.

As it has fully transitioned to being a Tier-1, the cost structure is expected to remain relatively stable and flat. One example that management gave was that the headcount that was previously used for the SOP of the BMW Gen1 program can now be transitioned to work on either the SOP of the BMW Gen2 program or the RFQ pipeline, thereby making its cost structure relatively flat.

Revenue in 3Q23 came in at $3.5 million, up 300% from the prior year and 138% from the prior quarter.

Operating expenses in 3Q23 came in at around $28 million, a decrease of 11% from the prior year. R&D expenses came in at $21 million, a decrease of 14% from the prior year. In the quarter, $3 million of R&D expenses were deferred to future quarters and will be matched to future NRE revenues and recognized as COGS.

Guidance

In my opinion, Innoviz has had a great 2023 and it just shows how well it is executing relative to the industry.

It has raised guidance twice in 2023, when others have found it challenging to meet theirs.

In 1Q23, Innoviz raised the high end of its guidance range as a result of additional programs from existing customers after it announced the light commercial vehicle program.

In 2Q23, Innoviz raised the revenues guidance as a result of improved visibility into higher volumes and NRE revenues. The net new NRE bookings range was also raised at the higher end as there was progress in the RFQ pipeline.

Management also guided that in 2023, revenues will trough in 1Q23 but that would improve sequentially as a result of SOP of the BMW program and more NRE revenues. Likewise, this was achieved as 2Q23 revenues grew 45% sequentially and 3Q23 revenues grew 138% sequentially.

In 3Q23, management chose to reiterate their 2023 targets, which includes a revenues guidance of $15 million to $20 million for 2023, representing a 150% to 230% growth.

For reference, taking into account the full year guidance of $15 million to $20 million, and the year-to-date revenue of $6 million as of 3Q23, this implies that 4Q23 revenue should come in between $9 million to $14 million.

Thus, 4Q23 revenue alone is expected to be not just larger than the first three quarters of 2023, but also, larger than any other quarter and other full-year revenue.

Runway

The current cash on the balance sheet is expected to be able to bring Innoviz well into 2025.

On top of that, the growing revenue base will also help to increasingly offset expenses.

In the current RFI and RFQ pipeline, there is a potential NRE of $150 million to $250 million to be received as cash payments from customers.

Of course, if Innoviz wins more programs, there will be more NREs to be earned.

All that ensures that Innoviz has a very sustainable business model with ample of financial runway.

Valuation

I am rolling forward the 5-year financial forecasts to 2028 and incorporate only existing program wins into the model.

For context, the inflection in revenues and also margins should come mid-decade, sometime in 2025 and after, given when that is when majority of the current existing customer wins are targeting.

My 1-year price target is $6.90, implying 12x 2024 P/S respectively.

Given its strong growth profile, solid management execution and near-term catalysts, I think that the multiple is more than justified for Innoviz.

Clearly, the stock looks really undervalued here and I expect that with more positive news come 2024, we will see these drive the multiple and share price higher.

Conclusion

Innoviz once again continued to execute well and in accordance with the management's guidance and targets.

The BMW Gen1 program transitioning to SOP is a huge milestone for the company, differentiating itself from other LiDAR companies which have not yet reached the milestone.

The company also is looking to expand into other programs within the Volkswagen Group, which is in advanced conversations, while the team started development for the BMW Gen2 program, which will feature the InnovizTwo and lead to an improvement in the content per vehicle.

As a result, Innoviz has a clear strategy to increase the content per vehicle and also improve the margin profile of the business as it starts to integrate more software revenues into the mix.

Innoviz has a strong balance sheet today after the capital raise not only helped to extend its financial runway, but also aid the company in advancing RFQs into the final stages.

There are three RFQs that are in the final stages, with at least two expected to make a decision by this year. For the other RFQs in the pipeline, management expects some of those to make a decision by 1Q24 or 2Q24. The rich pipeline is starting to be a rich catalyst for Innoviz in the coming months.

All in all, this was a positive quarter for Innoviz as the company continues to execute well and deliver on its targets.

For further details see:

Innoviz: Reaching An Inflection Point In 2024