INGN - Inogen: Downside Appears Limited Upgrade To Hold

2023-03-06 13:46:43 ET

Summary

- Supply chain issues caused major problems for Inogen in FY22, and continued headwinds are expected in FY23.

- Management expects operational performance to improve in late FY23 but indicates that returning to profitability is a medium-to-long-term endeavor.

- The share price has fallen by over 50% since my Sell call and downside risk now appears low given the high level of balance sheet cash relative to market capitalization.

- Further share price weakness could make Inogen an attractive acquisition target.

Introduction

I first published on Inogen, Inc. ( INGN ) in early January 2022 ; at the time INGN’s share price was ~$34. The January 2022 Sell/Bearish call proved to be a money-maker, as INGN’s share price drifted lower, landing at slightly below $20 by the end of calendar year 2022. Shareholders enjoyed a much more positive start to 2023, with the stock reaching $26 by early February. But the 4Q22 result on 23 February triggered a big sell-off, pushing the price down below $16, where it currently remains at the time of writing. In this note I refresh my initial work on the company and provide an updated view regarding the stock’s valuation appeal.

Inogen – Quick Overview

For the benefit of readers who are new to the stock, let’s start with a quick refresher of what INGN does and the market that it aims to serve. INGN describes itself as a medical technology company. Adding the word ‘technology’ to a company’s description is a handy way to give a stock’s P/E a boost. I prefer to describe INGN as a medical device manufacturer and distributor. The company is primarily focused on designing, building and distributing (both via sale and rental) portable oxygen concentrators (POCs) which are used to deliver long-term oxygen therapy to patients suffering from chronic respiratory conditions, and in particular, chronic obstructive pulmonary disease (COPD). For oxygen therapy patients who are mobile and able to leave home, POCs are a much more convenient solution than traditional oxygen tanks/cylinders. INGN also argues that POCs can have advantages over stationary oxygen concentrator systems for in-home use.

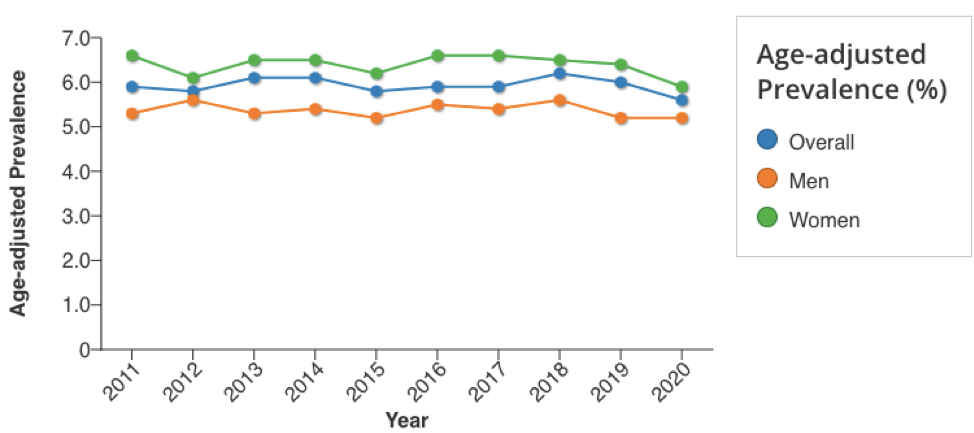

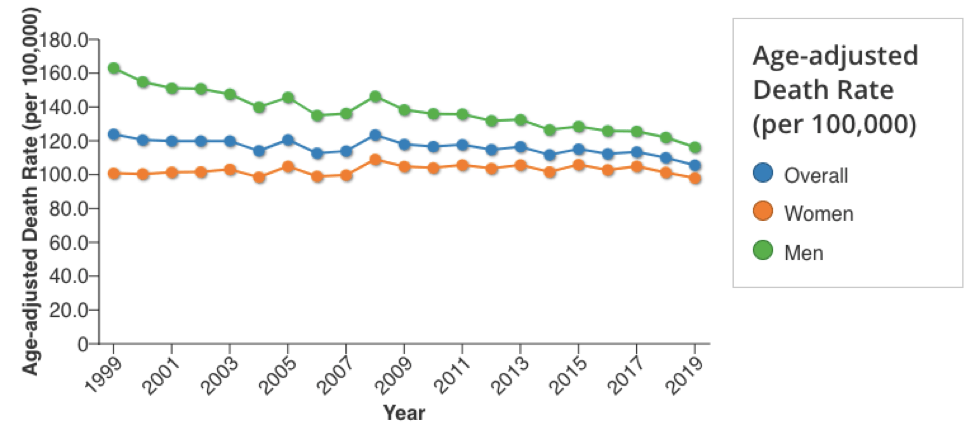

COPD is a highly prevalent medical condition in the US. Exhibit 1 shows that the age-adjusted COPD prevalence rate for US adults is around 6%. The prevalence rate has been relatively stable over the period captured by the data. Exhibit 2 looks at age-adjusted COPD death rates for US adults aged 45 and above. Overall death rates have shown a modest decline over the decade to 2019 driven by improved outcomes for males. According to the Centers for Disease Control and Prevention, chronic lower respiratory disease, primarily COPD, was the fourth leading cause of death in the US in 2018. In INGN’s 4Q22 Form 10K (page 3), the company references a 2022 publication stating that COPD is the sixth leading cause of death in the US.

Exhibit 1:

Age-adjusted prevalence of COPD among US adults aged ? 18 years, 2011–2020

{kind=link}

Source: Centers for Disease Control and Prevention

Exhibit 2:

Age-adjusted death rates for COPD among US adults aged ? 45 years, 1999–2019

{kind=link}

Source: Centers for Disease Control and Prevention

The charts above support the view that the demand for the types of products that INGN manufactures can be expected to remain robust. Further, as depicted in Exhibit 3, within the long-term oxygen therapy market, INGN says that there is significant potential for increased penetration of POCs from the current level of ~22%. I note that INGN constructed this chart by taking 2021 traditional fee-for-service Medicare data and applying certain assumptions regarding the overall market structure – without clarity regarding the assumptions and adjustments made, it is hard to form a view on how reliable INGN’s POC penetration estimates are. That being said, I am certainly willing to accept the view that POC market penetration is likely to increase over the coming years – although the rate of increase is impossible to predict with confidence.

Exhibit 3 – estimated penetration of POCs:

Source: INGN Strategy Presentation, February 2023, slide 5.

It should come as no surprise that a large and robust market for long-term oxygen therapy has attracted high levels of supplier competition. Indeed, according to page 9 of the INGN 4Q22 Form 10K, INGN’s expectation is that the industry will become increasingly competitive in the future. So, whilst I view the demand outlook for INGN’s key products as a positive for the investment case, this enthusiasm is somewhat dampened by the already high and increasing level of competition in the marketplace.

Challenging Conditions in FY22

Slightly over a year ago I concluded that the near-term outlook for operating earnings was rather bleak for INGN, mainly due to ongoing supply chain problems. It’s therefore not surprising that FY22 turned out to be a very tough year for the company. Supply chain issues blew up in a big way early in the year and INGN suspended production for six weeks in 1Q22 due to a shortage of semiconductor chips. Whilst it is true that many companies have struggled to deal with disruption in the semiconductor chip market, the fact that INGN was forced to shut down production for six weeks raises questions about the competence of INGN’s management of supply chain risks and the ability of the company to quickly adapt to changing market conditions.

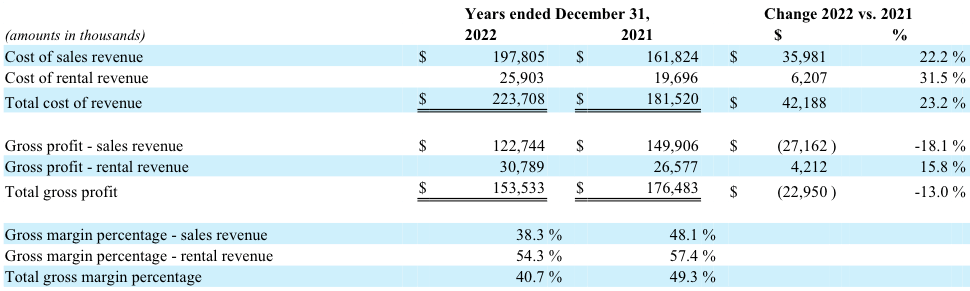

Exhibit 4 shows that the revenue outcome in FY22 was not too bad, with total revenue growth of 5.4%. If we exclude rentals revenue, the aggregate sales component also achieved revenue growth in FY22, however this overall sales result was driven by growth in the lower margin international sales bucket, with declines in the higher margin domestics sales channels. In Exhibit 5 we can see very clearly that the higher cost of sales in FY22 caused a collapse in INGN’s gross margin, particularly on the sales revenue side. The main driver of the crunch in the sales revenue gross margin was higher costs associated with semiconductor chip purchases.

Exhibit 4:

{kind=link}

Source: INGN 4Q22 Form 10K, page 74.

Exhibit 5:

{kind=link}

Source: INGN 4Q22 Form 10K, page 75.

Ambidextrous Leadership?

FY22 was a miserable year for INGN. FY22 operating income came in at a loss of -$85.2m, as compared with FY21 operating income of $9.2m. If we exclude the large New Aera intangible asset write-off (discussed below), the adjusted FY22 operating income becomes a slightly less painful loss of -$33.1m. Prior to the pandemic, INGN reported operating income of $37.9m in FY18 and $19.8m in FY19. Despite this very disappointing FY22 outcome, CEO Nabil Shabshab opened management’s discussion of the FY22 result in a rather self-congratulatory tone:

2022 has been a testimony of the team's ambidextrous leadership, as evidenced by our ability to progress the needed transformation while delivering revenue growth, despite the multiple challenges, including macroeconomic and inflationary headwinds that presented themselves during the back half of 2022.

Source: INGN 4Q22 Transcript , page 3.

I’ve thought about this for a while now and I’m still not sure what ‘ambidextrous leadership’ actually means, but whatever it is, Shabshab seems rather proud of it. Thank goodness the company can use its left and right hands equally well; who knows how bad the FY22 operating income loss might have been without this skill.

New Aera Intangible Write-Off

In my previous note I referred to the acquisition of New Aera in 2019 as being a disappointment. That view has proven accurate. In 4Q22 INGN wrote off an intangible asset of $52.16m relating to TAV technology acquired in the New Aera acquisition. To put this in context, just three years after completing the New Aera deal, INGN has written more than 50% of the total acquisition cost down to zero. Given that the New Aera acquisition has been a big failure, I was concerned to see that further acquisitions could well be on the agenda.

Lastly, as we advance our innovation strategy to serve patients beyond COPD, we remain open to potential acquisitive growth opportunities that would support our aspiration for Inogen becoming a more comprehensive respiratory care company.

Source: INGN 4Q22 Transcript, page 5.

Guidance for FY23E

CFO Kristin Caltrider outlined INGN’s FY23E guidance in the 4Q22 management speech:

I will now turn to our financial outlook. As Nabil mentioned earlier, we are providing annual revenue guidance for 2023. We are expecting total company revenue to grow in the low- to mid-single digits. As we continue to drive towards profitability, we anticipate reaching a positive adjusted EBITDA by the fourth quarter of 2023.

Source: INGN 4Q22 Transcript, page 8.

As we have seen in FY22, revenue growth is not INGN’s main challenge. The company needs to urgently improve its gross margin. Management’s ambition to return to a positive adjusted EBITDA position by 4Q23E is perhaps comforting, but I flag two points: a) there is a significant amount of uncertainty regarding achievement of this goal, and b) with depreciation and amortization running at around -$24m pa, the 4Q23E EBIT outcome is still likely to be well into negative territory.

Valuation

My preferred approach to valuation is to apply a normalized earnings framework. A weakness of this approach is that it can provide unreliable value signals when there is a high degree of uncertainty regarding the level of earnings that a company can generate on a sustainable basis. At present, given the lack of visibility regarding INGN’s future earnings, I am hesitant to apply my preferred valuation method. In such cases, it is often helpful to look at what a company’s market capitalization is telling us about market expectations for future earnings.

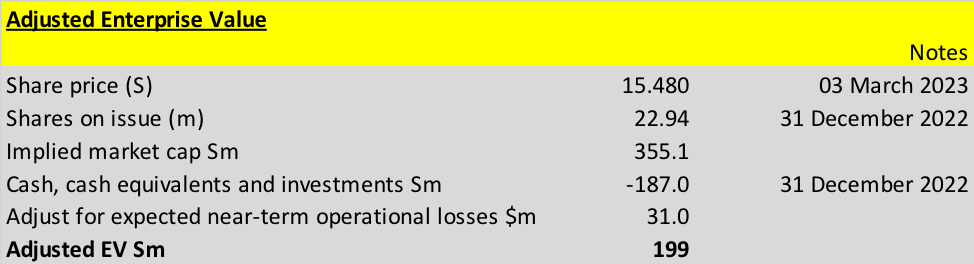

As discussed above, there are several negative issues to consider regarding the investment case for INGN. On the other side of the coin, the company does have one rather strong positive – INGN’s balance sheet is solid. The company has no debt and reported a 4Q22 cash balance of $187m. This cash balance represents ~53% of INGN’s current market capitalization (based on the 03 March 2023 market close share price of $15.48 per share). Given such a high cash balance, it can be argued that the downside risk for INGN’s share price is quite low. I would modify this analysis slightly by taking into account the potential for INGN to incur operational losses in FY23E and possibly into FY24E. Exhibit 6 sets out my calculation of an adjusted enterprise value for INGN that captures an allowance for estimated future operational losses.

Exhibit 6:

Source: author’s calculations based on INGN quarterly reports.

{kind=link}

The adjusted cash value of $156m (allowing for expected future operational losses) represents ~44% of the current INGN market capitalization. For a stock in the healthcare sector, I would typically regard an EV/EBIT multiple of ~20x as being around fair value. On that basis, the adjusted EV of $199m aligns with an EBIT of ~$10.0m pa. Given my concerns around the outlook for INGN, I would feel more comfortable with a lower EV/EBIT multiple. Applying a multiple of 16x, the adjusted EV of $199m aligns with an EBIT of ~$12.4m pa. Relative to INGN’s FY22 total revenue of $377m, EBIT of $12.4m would represent an EBIT margin of only 3.3%. Given the volatility in INGN’s historical earnings, it is difficult to say what level of EBIT margin the company is capable of achieving on a sustainable basis, but something north of 5% does not appear to be a huge stretch.

Summary and Conclusion

There is a lot more going on with INGN than I have touched on in this note. For example, the company is currently focused heavily on its direct-to-consumer strategy and is seeking to develop a more patient-centric model, leveraged via deeper relationships with prescribers. Shabshab appears to be placing more strategic emphasis on new product innovation and developing devices targeted at conditions other than COPD. These strategy initiatives are interesting and have potential to improve INGN’s operating performance over time, however successful execution is far from guaranteed and the company’s recent history leaves me unwilling to place much weight on such upside scenarios.

FY23E is going to be another difficult year for INGN. Supply chain issues, mainly relating to semiconductor chips, will once again be a drag on operational performance. Management commentary points to the first half of 2023 being particularly tough, with an expected recovery in the latter part of the year. In the 4Q22 management speech, CFO Kristin Caltrider provided guidance that the company anticipates reaching positive adjusted EBITDA in 4Q23, but I feel that it is difficult to have confidence regarding that outcome. Investors hoping for a quick turn-around in INGN’s earnings are likely to be disappointed given the company’s consistent comments that a return to profitability will be a medium-to-long-term endeavor.

INGN has plenty of cash, and it is rather tempting to conclude that the stock is too cheap at current levels of around $15.50 per share. A risk to such a conclusion is that this cash support could quickly evaporate if the company makes an acquisition or two. On the other hand, it is also certainly feasible that INGN’s low share price could make it an acquisition target. If an acquiring company could quickly solve INGN’s supply chain issues around semiconductor chips, the deal metrics would probably look very compelling.

On balance, for less risk averse investors I think INGN stock is probably a Buy. However, given my lack of confidence in the level of sustainable earnings that INGN will be able to generate, I conclude this review with a Hold rating.

For further details see:

Inogen: Downside Appears Limited, Upgrade To Hold