INGN - Inogen: Still Struggling But Very Cheap - Upgrading To Buy

2023-07-13 22:13:15 ET

Summary

- Inogen’s Q1 2023 results disappointed the market, despite management’s confirmation that previously issued FY23E guidance remained unchanged.

- New product launches, including Rove 6 distribution in Europe, should provide a modest boost to revenue in coming quarters.

- With a debt-free balance sheet, and ~70% of the company’s market capitalization supported by cash and investments, Inogen is a potential acquisition target.

- Inogen is unlikely to return to satisfactory levels of profitability until at least 2H24E, but for patient investors who are not averse to risk, the stock is a Buy.

Introduction

Inogen, Inc. ( INGN ) released 1Q23 results in early May 2023. The company’s shares were trading in the high $13’s prior to the update, but rapidly declined to below $11 as the market digested the new information. In this note I’ll look over the 1Q23 materials and discuss positive and negative factors that are relevant to INGN’s investment case. With the share price now hovering close to $10, it’s almost impossible to believe that the stock briefly traded above $200 in 2018 and peaked again to almost $80 in early August 2021. For further background on the company, I direct readers to my previous INGN notes published in January 2022 and March 2023 .

1Q23 Positives

Key positives reported in the 1Q23 materials are summarized and discussed below:

- Despite a soft revenue performance in 1Q23, management left FY23E guidance unchanged (revenue to increase by low to mid-single digits, EBITDA to move into positive territory in 4Q23E). I lack confidence in management’s ability to provide reliable guidance, but it is slightly encouraging that the CEO and CFO haven’t lowered the FY23E forecasts previously given at 4Q22.

- Supply chain pressures regarding semiconductor chips have eased and this factor ought not to be a constraint regarding sales volumes moving forward.

- Rental revenue was strong, coming in at +25.4% Y/Y. Rental revenue has grown materially – from $5.3m in 1Q20 to reach $16.3m in 1Q23. Two new private healthcare payers were added to coverage in the quarter.

- Recent product launches provide potential for growth in future sales. Rove 6 (weight 4.8 pounds, producing 1,260 ml per minute of oxygen output, 37 dBA, battery life 6.25 hours single battery and up to 12.75 hours on double battery) was released in Europe in late 2022 and was granted reimbursement status in Germany during 1Q23. A further reimbursement approval is expected during 2Q23 in France. US FDA approval has been granted for Rove 4, with a launch to follow in the second half of FY23.

- DTC (direct-to-consumer) sales representative productivity increased ‘in the teens’. I would like to see management provide detailed statistics regarding sales representative productivity (for both units and revenue), and without such it is difficult to gain confidence that the new sales management initiatives are working.

1Q23 Negatives

Key negatives reported in the 1Q23 materials are summarized and discussed below:

- 1Q23 Y/Y sales revenue growth came in at -17.1%. Looking back a further year, 1Q23 sales revenue was down by -27.5% relative to 1Q21. Management say that 1Q23 revenue (overall, including rental revenue) was in line with expectations, but this is still a disappointing outcome.

- Domestic B2B sales were up by ~147% in 1Q22, but 1Q22 was abnormally low. If we look back at 1Q21, the 1Q23 outcome was down by -59% relative. This sales channel does not seem likely to improve in the near future.

- DTC (direct-to-consumer) sales representatives fell in 1Q23. Management commentary suggests that this was due to the delivery of a ‘new sales management discipline’, but that is hard to verify. The net impact was a fall in DTC sales.

- Management continues to talk about the ambition for portable oxygen concentrators to address other respiratory conditions beyond CPD. Whilst some may see this as a positive, at present I would much prefer INGN to ‘stick to their knitting’ and improve the current business rather than seeking to expand into new areas.

- Material restructuring and related charges of -$1.8m were incurred.

- Despite reporting a 1Q23 revenue outcome that was below analyst expectations, management would not be drawn during the Q&A session into providing further detail regarding the expected profile of revenue growth recovery for FY23E. There is a sense of ‘trust us’ in the management messaging, but this management team does not have a track record that can readily promote such trust.

Balance Sheet Underpins Value

In previous publications I have discussed the lack of visibility regarding INGN’s future earnings. Questions asked during the 1Q23 Q&A session suggest that sell-side analysts also lack confidence regarding the near and medium-term outlook for the company. My interpretation of management’s responses in the Q&A session is that the leadership team themselves do not have much in the way of clarity regarding INGN’s future operational performance.

My preferred approach to valuation is to apply a normalized earnings framework, but as things stand today, I cannot form a robust view on the level of sustainable earnings that INGN should be able to generate – there are simply too many uncertainties in play. In such situations, it can be helpful to look at what the company’s market capitalization is telling us about market expectations for future earnings.

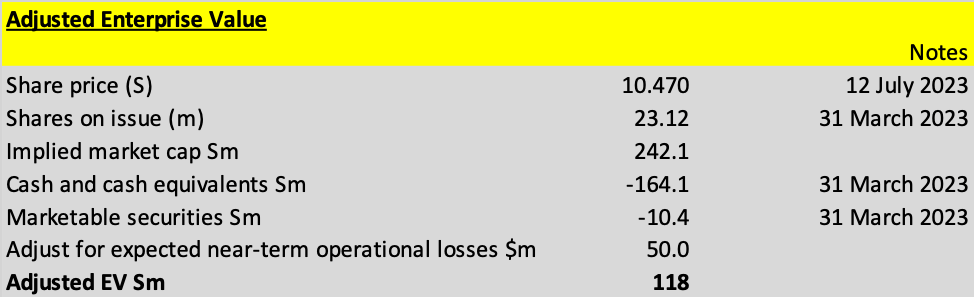

The strongest positive that INGN has from an investment case perspective is that the company has a very healthy balance sheet. INGN has no debt, and 1Q23 cash, cash equivalents and marketable securities (US Treasury notes) totalled ~$175m. The value of 1Q23 cash and investments therefore represents ~72% of INGN’s current market capitalization (based on the 12 July 2023 market close share price of $10.47 per share). Exhibit 1 sets out my calculation of an adjusted enterprise value for INGN that captures an allowance for estimated future operational losses.

Exhibit 1:

{kind=link}

Source: author’s calculations based on INGN quarterly reports.

Based on this analysis, the sum of INGN’s cash and investments, less expected future operational losses comes to $124.6m, representing ~51% of the current INGN market capitalization. If my estimate of future operational losses is increased by 50%, then the revised loss-adjusted cash and investments value falls to ~31% of the current INGN market capitalization.

Conclusion & Rating

For a stock in the healthcare sector, I would typically consider an EV/EBIT multiple of ~20x as representing fair value. Given my concerns around the outlook for INGN and the quality of the company’s management, a materially lower EV/EBIT multiple is warranted. Using a multiple of 16x, the adjusted EV (described above) of $118m aligns with an EBIT of ~$7.3m pa. INGN’s FY22 total revenue was $377m. The company has guided FY23E revenue growth of ‘low to mid-single digits’; if I assume revenue growth of 2%, then I get to FY23E revenue of ~$385m. EBIT of $7.3m on revenue of $385m gives an implied EBIT margin of 1.9%. If INGN was in good operational shape, my view is that an EBIT margin of 5% would be achievable. On that basis, the market appears to be baking in rather pessimistic assumptions regarding INGN’s future profitability.

INGN is clearly managing through a difficult period in the company’s history. Some of the problems being dealt with relate to external factors, but some are due to internal factors and management decisions. I would certainly not be willing to apply the label ‘high quality’ to INGN at present. For investors willing to buy companies that aren’t in good shape, the question to ponder is whether or not INGN is now cheap enough to take a chance on.

The strength of INGN’s balance sheet ought to be seen as a valuable asset for a potential acquirer (especially one that could take advantage of cost synergies), and I think that the company could attract a bid if the share price falls below $10. A significant improvement in operational performance in FY24E appears unlikely at this stage, but it is certainly not impossible for INGN to be generating an EBIT margin in the range of 3% in FY25E – at which point the stock price would likely receive a boost from the benefits of both margin recovery and an earnings multiple expansion. This is not a stock for risk averse investors, but at the current price level of low $10’s, I’m willing to upgrade INGN to a Buy rating.

For further details see:

Inogen: Still Struggling, But Very Cheap - Upgrading To Buy