INGN - Inogen: Time To Be Greedy When Others Are Fearful

2024-01-01 08:47:05 ET

Summary

- Inogen's price performance has been poor this year, but a closer look at the numbers suggests that the market's negativity may be unwarranted.

- Management is actively taking steps to address the company's issues.

- I'm issuing a Buy rating, but suggest holding Inogen in a well-diversified portfolio more so than as a single issue.

Investment thesis

If you want to see first hand what a tough place the market can be, look no further than the price performance of the common stock of Inogen, Inc. (NASDAQ: INGN ).

Shares of this health care enterprise have come down like a New Years rocket post detonation in the past year (down ~70%):

{kind=link}

With price action like that, even the most bullish analysts tend to get scared away. Indeed, the most recent coverage on Seeking Alpha was a rating downgrade .

But then again, these are the kind of circumstances that create buying opportunities I like: A security in distress that the market has left behind.

Distressed securities can't be just blindly bought, though. It's not like buying your average blue chip, high-yield stock that probably will do at least somewhat well in the foreseeable future.

With distressed securities, understanding the issue at hand and examining quantitative factors are key to proper stock picking.

In this analysis, I examine why shares of Inogen have dropped off so much. As my approach to equity research is based on screening for quantitative factors that hint at future outperformance, I share some key metrics that do just that.

I also evaluate steps management has taken to address the issues that are clearly present at Inogen.

Based on my findings, I'm issuing a Buy rating for Inogen. I suggest holding it in a portfolio of similar issues for risk diversification.

Why Inogen has performed poorly

As is so often the case with stocks that have performed badly, the initial "blitz drop" came following the announcement of results missing consensus estimates.

The stock dropped from about $23 to about $16 in late February following a dissappointing earnings announcement . Inogen actually beat on EPS but missed on revenue.

Over the year, results have continued to vary and have often been out of line with consensus: In May, Inogen missed both EPS and revenue targets. In August, EPS beat estimates while revenue missed. In November, EPS missed but revenue beat.

Following the mixed bag of results, Inogen has basically been unable to recover throughout the year - and much of the poor performance seems attributable to this mismatch between expectations and performance rather than more fundamental adversities.

A look at the numbers suggests Mr. Market is too negative

On a statistical level, Inogen is curiously cheap: It trades at an EV/R ratio of just 0.06. The EV/R ratio (enterprise value to revenue) measures how much a buyer for control would have to pay to buy all equity and all bonds at market.

In other words, it's what a buyer would have to pay to own the company's assets cleared of all equity and bond claims in relation to what those assets turn over.

I use the EV/R ratio on distressed equities because I find it more appropriate than conventional metrics like P/E and PFCF (price to free cash flow), since distressed companies often don't produce earnings or free cash flows as they are navigating whatever adversity they are working through. Therefore, you need some other metric that measures the "price tag" the market is putting on what the company produces.

Inogen trades at a market cap of ~$130 million. That makes it a small cap company. I think small caps are more likely to trade below intrinsic value for longer than other stocks - and I think the market is more likely to exaggerate its reaction to temporary adversities. So the simple fact that Inogen is a small cap - combined with the low EV/R ratio - are indicators to me that the stock is undervalued.

As much as the mixed reporting in 2023 might have you thinking that Inogen's is on a sliding path nowhere, it has actually managed to grow respectably over the years. Here's a 5 year chart of its revenue:

Inogen investor presentation

As I'll discuss in the following, Inogen seems intent on continuing to advance its business.

Management is taking action

It's been all numbers so far. While you can buy issues based on statistics not knowing what the business actually does, it's nice to know what you're getting yourself into.

Inogen is in the business of making portable oxygen concentrators . It's a medical device designed to provide oxygen therapy to people who require greater oxygen concentrations than the levels of ambient air.

That's good for customers. So what about the shareholders?

One of Inogen's main actions to drive shareholder value and stabilize the mixed performance is to attempt to expand margins. In doing so, management has pointed to three short term actions :

Inogen investor presentation

As seen, the short term actions primarily relate to cutting costs ("Executing selective [Sales, General & Administration] reductions" and "Reducing facilities footprint").

The company also pointed to the following medium term actions which focus on growing revenue:

Inogen investor presentation

Inogen has launched and will launch a variety of products in 2023/2024 to help drive that revenue growth:

Inogen investor presentation

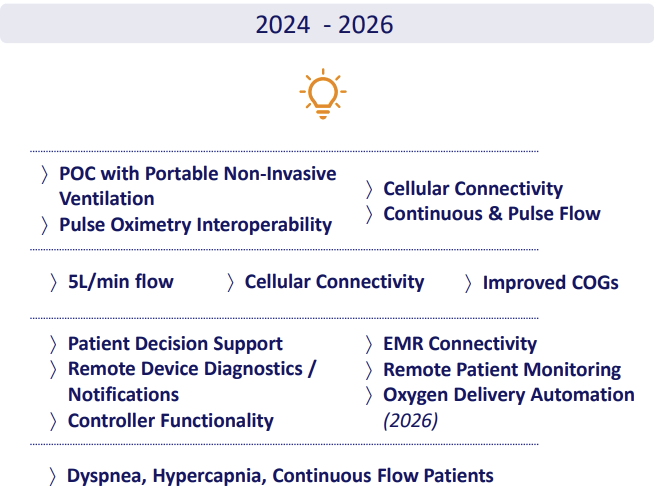

Further to the short term pipeline, Inogen maintains a pipeline that extends well into the decade. Between 2024 and 2026, Inogen appears to focus on improving the capabilities of its products in particular:

{kind=link}

Inogen investor presentation

In summary, Inogen is focused on improving margins, growing revenue and innovating to remain competitive and reward shareholders.

On a final note, I'd like to highlight Inogen's financial position: Inogen has ~$225 million in current assets. That's including $138 million in cash and equivalents. That compares to just ~$113 million in total liabilities. None of the liabilities are long-term, interest-carrying debt, so all of it will be accounts payable, leases, taxes etc. In other words, Inogen would hold ~$112 million in ready cash if all liabilities were paid and all accounts receivable recovered. Compare this to Inogen's market cap of ~$130 million. You're paying almost nothing for the actual business.

Risks

I've covered several stocks that are technically or fundamentally in distress. I find opportunities in this field to be intriguing because they often display substantial upside that others will gladly leave behind to do something "safer". Investing in this field does come with obstacles, though: Any given distressed issue may not work out. Distressed securities often end in bankruptcy, and sometimes with a 100% loss resulting from that. But a stock can't go lower than that - while it can potentially move up hundreds of percent. That's the statistical advantage in buying securities with substantial upside. In order to achieve a range of results that represent an average of such upside potential, I suggest using fairly wide diversification. It's all about managing the risk while maintaining the upside potential on average. I believe adhering to this is the most relevant risk management strategy when it comes to investing in an issue like Inogen.

Key takeaways

Inogen is a health care company that makes portable oxygen concentrators. Its stock has traded off substantially during 2023 and is down ~70 %.

This presents a buying opportunity since the market in its fear seems to neglect the fact that Inogen is now very cheap: It trades at an EV/R ratio of just 0.1.

Inogen's management seems to appreciate the need to continue to innovate and reward shareholders: The company has a potent product pipeline and expects to expand margins. Its solid financial position should support that.

I suggest holding Inogen in a portfolio of other distressed equities that show similar quantitative properties. I'm issuing a Buy rating with that caveat in mind.

For further details see:

Inogen: Time To Be Greedy When Others Are Fearful