INSM - Insmed's Arikayce: A High Flyer With A Heavy Load

2023-10-15 10:58:47 ET

Summary

- Insmed shows strong Arikayce sales but is financially strained due to surging R&D expenses and increasing operational costs.

- A diversified but high-risk R&D portfolio raises sustainability concerns, making the company's long-term financial stability questionable.

- Investment Recommendation: Adopt a "Hold" stance on Insmed stock; monitor clinical trials and non-dilutive financing avenues given operational and financial risks.

At a Glance

In this follow-up analysis to my 2019 review of Insmed ( INSM ), a dual narrative continues to unfold. Since my previous assessment, Insmed has largely met my sales expectations for Arikayce while making strides in securing a portion of the U.S. refractory market. Clinically, Insmed is gaining significant ground with Arikayce, targeting an underserved patient population with unmet medical needs. However, robust revenue growth in Arikayce is now counterbalanced by a surge in R&D expenses aimed at high-risk therapeutic areas, inflating operational costs and long-term debt. Share dilution also persists, signaling potential cash-flow challenges ahead. Despite a current ratio indicative of short-term financial stability, Insmed’s elevated monthly cash burn against its cash reserves suggests looming capital infusion needs within the next year. Investors should still eye forthcoming clinical trial readouts as key inflection points. Collectively, these evolving factors renew questions about Insmed’s strategic agility to maintain its clinical milestones and financial integrity, without a more focused realignment.

Financial Insights

Insmed's Q2 2023 financials offer a dichotomy: revenue growth is countered by a ballooning operating loss. Revenue at $77.2M, up from $65.2M YoY, suggests a robust market demand for their products. Conversely, the spike in operating expenses, especially a more-than-double YoY increase in R&D to $196.9M, puts significant pressure on profitability. Operating loss escalated to $235.5M from last year's $88.3M. Share dilution further dilutes shareholder value with outstanding shares rising to 137.5M from 119.6M YoY.

Examining the balance sheet , cash reserves and marketable securities total $917.8M, offset by a concerning $1.14B in long-term debt. The current ratio of 5.15 suggests short-term liquidity is not a pressing issue. However, the debt-to-asset ratio of 0.9 indicates a leveraged financial structure that may necessitate additional capital or debt restructuring in the near term. Cash runway, calculated from a $44.85M monthly burn rate, stands at approximately 23 months.

Here's the rub: despite its cash cushion, Insmed's high cash burn and escalating long-term obligations suggest a likely need for additional capital within a year. Existing reserves can cover short-term obligations but don't ameliorate concerns over long-term debt and escalating operational costs. The financial trajectory, in its current state, implies a growing necessity for either financial restructuring or fresh capital infusion.

Market Sentiment

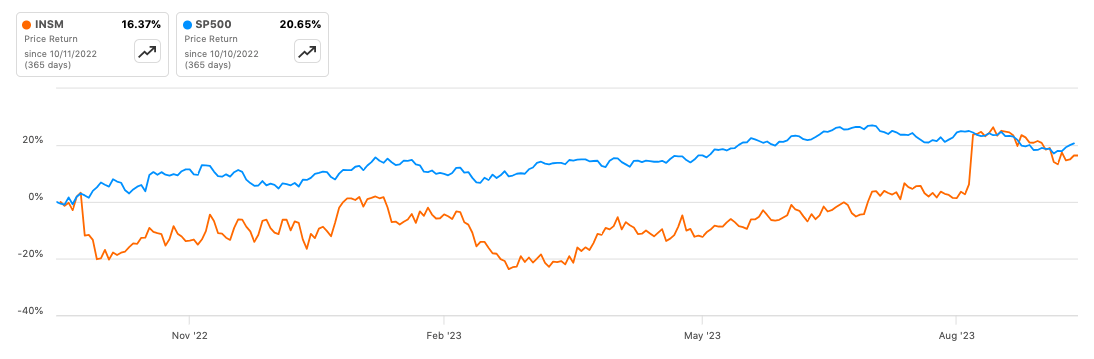

According to Seeking Alpha data, Insmed's market cap of $3.52B appears reasonable in light of its financial and clinical prospects. The projected revenue for FY2023 is $303.7M, up by 23.78%, with a respectable 3-year CAGR of 18.01%, highlighting strong growth prospects. Compared to the S&P 500, Insmed's stock has outperformed in shorter timeframes (3M and 6M) but lags in the 1Y, signaling stock-specific momentum rather than systemic trends. A 9.63% short interest points to moderate bearish sentiment.

{kind=link}

Institutional ownership stands at a staggering 98.84%, with Vanguard, BlackRock, and T. Rowe Price among key holders. New institutional positions tally 3,299,847 shares, while sold out positions account for 1,328,992 shares, indicating more bullishness among institutional investors. Insider activity in the past year shows a net accumulation of 460,086 shares, although no new open market buys were reported in the last three months, creating a mixed signal for the stock.

Insmed's R&D: A Diverse Yet Risky Portfolio

Insmed's pipeline , while diversified, raises concerns about the sustainability of their heavy R&D expenditures, particularly in light of the high-risk segments they're entering. While Arikayce is an approved asset for refractory MAC lung disease, its lifecycle management could be a resource-intensive effort for uncertain incremental gains.

The multiple applications of brensocatib, their DPP1 inhibitor, seem promising but the reality is they are tackling complex neutrophil-driven inflammatory conditions like non-CF bronchiectasis and cystic fibrosis [CF], areas notorious for high R&D attrition rates.

Their venture into additional rare pulmonary diseases, with compounds like treprostinil palmitil inhalation Powder, suggests a further dispersion of R&D resources without a guaranteed ROI. Specialized conditions like PH-ILD and PAH, while underserved, are no slam-dunks in drug development .

Their early-stage investments in gene therapies such as INS1201 for Duchenne Muscular Dystrophy [DMD], along with exploratory work on deimmunized therapeutic proteins, are undoubtedly high-stakes endeavors. The gene therapy space is highly competitive and fraught with clinical and regulatory hurdles, making it a risky avenue for a company primarily rooted in respiratory diseases.

In summary, Insmed seems to be casting a wide net with its R&D spend, running the risk of overextending itself in areas with inherently low odds of success. The revenue generated from the mature assets may not suffice to offset the financial risks associated with their diversified but precarious pipeline.

Insmed Breaks the Ceiling with Arikayce Sales

In Q2 2023, Arikayce achieved a record-breaking $77.2 million in quarterly sales, an 18% YoY growth. This robust performance led the company to revise its full-year revenue guidance for Arikayce to a range of $295-305 million. The sales growth was globally diversified, with contributions from the U.S., Japan, and Europe. Insmed is also actively involved in post-marketing trials, specifically the ARISE and ENCORE studies, targeting patients with newly diagnosed or recurrent Mycobacterium avium complex [MAC] lung infections. Topline data from the ARISE study met its primary endpoint, while the ENCORE study aims for a 250-patient enrollment by year-end.

The MAC market is fraught with challenges, being the leading cause of nontuberculous mycobacterial (NTM) lung disease. Limited treatment options and a high rate of treatment failure, relapse, or reinfection—up to 40%—make Arikayce a recommended adjunct to guideline-based therapies for treatment-resistant MAC lung disease. Clinical studies and real-world applications suggest that Arikayce (aka "ALIS") enhances culture conversion rates and offers targeted drug delivery, minimizing systemic toxicity. However, it's associated with a higher incidence of respiratory adverse events compared to standard treatments.

To quantify the market opportunity, a study in the Annals of the American Thoracic Society estimated the prevalence of NTM lung disease in the U.S. to be around 86,244 cases. Given that MAC accounts for about 80% of all NTM lung disease cases, an estimated 69,000 patients in the U.S. could be diagnosed with MAC lung disease. Narrowing it down to those with treatment-refractory MAC lung disease ( ~20% of MAC population ), approximately 13,800 patients could be candidates for Arikayce treatment. Available information suggests an annual cost of nearly $130,000 for Arikayce. Assuming it reaches 33% of its target market, this could net as much as $600M per annum.

However, investors should also consider the challenges outlined in the company's recent financial disclosures. These include billing complexities with third-party payers like Medicare and regulatory audits. These factors introduce a level of risk that could materially affect the company's revenue streams and financial stability.

My Analysis & Recommendation

In the wake of the Q2 2023 financials, Insmed’s narrative of progress, underscored by Arikayce’s sales growth, is tainted by a ballooning operational cost structure, chiefly driven by an aggressive R&D outlay in high-risk therapeutic realms. While the diversified R&D agenda mirrors a quest for sustainable revenue channels beyond Arikayce, the financial prudence of such a strategy is debatable given the high attrition rates in targeted disease segments. The mounting long-term debt and a foreseeable need for capital amidst a rising share count flag liquidity concerns, despite a healthy current ratio.

Investors in the near term should closely monitor the company's execution on clinical milestones, particularly the outcomes of ongoing trials and any strategic realignment to rein in operational costs. The escalating OpEx necessitates a more scrutinized allocation of resources to ensure the firm doesn't compromise its financial footing. An eye on institutional ownership trends and insider activity could provide cues on market sentiment around Insmed’s strategic direction.

Mitigation of investment risk could be anchored on a diversified portfolio approach, buffering against sector-specific volatilities. Additionally, a cautious stance on capital allocation towards Insmed, pending clearer visibility on its R&D efficacy and debt management, would be prudent.

Given the confluence of financial health, clinical focus amidst market dynamics, competitive positioning, and the risk profile, a "Hold" stance is merited. The anticipation is that, with a stringent operational and financial re-evaluation, Insmed could navigate the rough waters, ensuring the promise of Arikayce and other pipeline assets doesn’t dissolve in a quagmire of financial exigencies.

For further details see:

Insmed's Arikayce: A High Flyer With A Heavy Load