TNET - Insperity: Current Pricing Doesn't Inspire Confidence

Summary

- Financial performance achieved by Insperity has been impressive lately, helping to push shares of the business higher.

- Long term, the picture for the company is likely favorable, and the same holds true for the rest of this year if management is correct.

- But with risks in the broader economy and how shares are priced today, the company isn't a great prospect.

As companies grow, it can be a wise financial decision to start relying on other firms to provide various functions that don't relate to the core operations of the enterprise in question. An example of this can be seen by looking at Insperity ( NSP ) and its business model of providing human resource services such as payroll and employment administration services, employee benefits services, workers compensation activities, government compliance, and a variety of other offerings, to the companies that it works with. Recently, financial performance achieved by the company has been incredibly robust. Having said that, shares of the company don't exactly look cheap. When you factor in the current economic conditions we are dealing with and what that might morph into in the next couple of quarters, I am not feeling particularly bullish about the enterprise. In fact, I would even go so far as to say that a 'hold' rating, (reflecting my belief that it should generate returns that more or less match the broader market) for the enterprise feels perfectly appropriate.

Great performance… for now

The last time I wrote an article about Insperity was in June of this year. At that time, I saw the company as a player that had done well to grow both its revenue and profitability over the prior few years. Fundamentally, I felt like the company was doing a solid job and I believed then and believe now that its long-term outlook should be favorable. Having said that, I mentioned that short-term pain may come into play because of the state of the economy. And on top of that, I also noticed that shares were not particularly cheap. Though I also would not go so far as to say that the stock was overvalued either. At the end of the day, I ended up rating the company a 'hold', but financial performance since then has helped to push shares off higher, with a stock rising by 13.1% compared to the 1.4% achieved by the S&P 500 over the same window of time.

{kind=link}

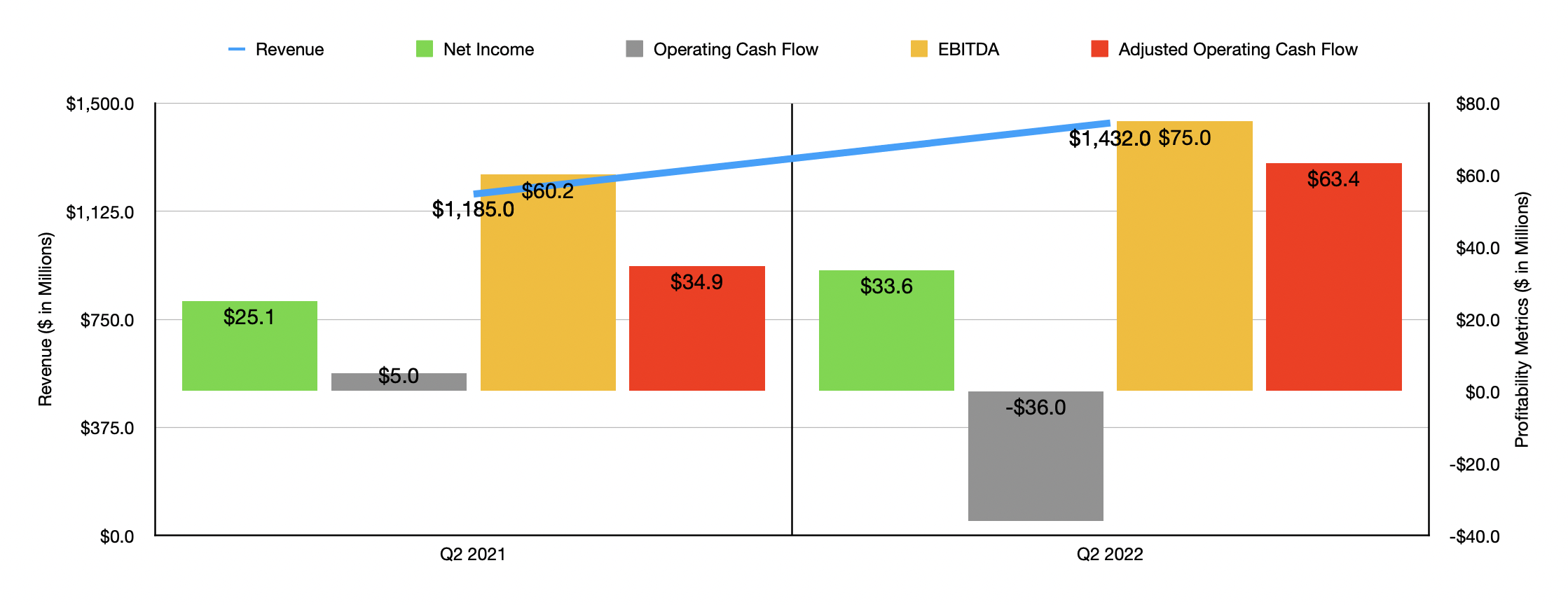

Judging by the performance figures of the company alone, this upside probably was warranted. Consider, for instance, that revenue in the second quarter , which is the only quarter for which we now have new data that we didn't have data when I last wrote about the firm, came in at $1.43 billion. That represents an increase of 20.8% over the $1.19 billion generated in the second quarter of 2021. This rise in revenue was driven largely by a 19.4% increase in what management calls WSEEs (or worksite employees). This number, as of the end of the second quarter, came in at 290,507. One year earlier, that number was at 243,270. On top of seeing the actual number increase, the company also benefited from a higher amount than it collected as a result of each WSEE. Per month, the revenue collected per WSEE came out to $1,643. This is 1.2% higher than the $1,624 per month collected the same time one year earlier.

In addition to seeing revenue rise, profits have also risen. Net income of $33.6 million beat out the $25.1 million seen one year earlier. But this is not to say that every profitability metric performed well. For instance, operating cash flow in the second quarter of 2021 came in at $5 million. The company experienced a net outflow in the second quarter of this year in the amount of $36 million. If, however, we were to adjust for changes in working capital, we would have seen this metric rise from $34.9 million to $63.4 million. And over that same window of time, we also would have seen an increase in EBITDA from $60.2 million to $75 million.

{kind=link}

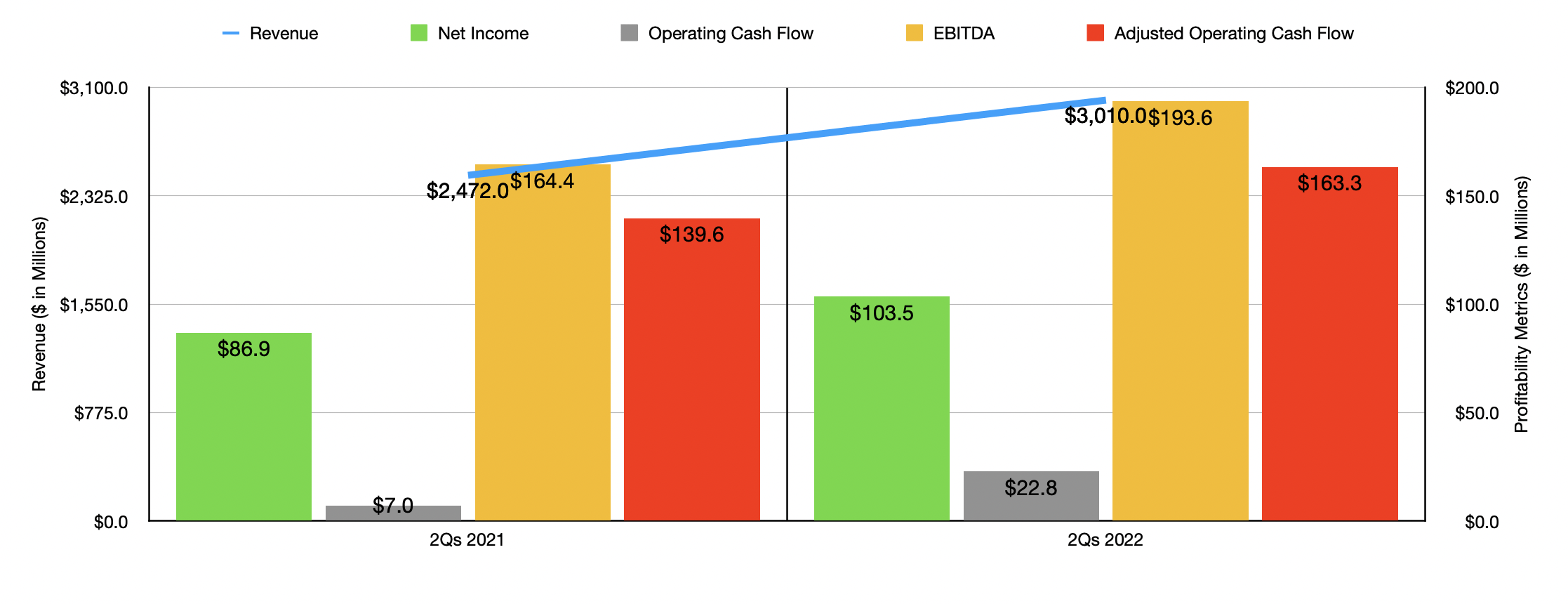

This strong performance on both the top and bottom lines helped results for the first half of the company's 2022 fiscal year as a whole. Revenue in this window of time totaled $3.01 billion. That compares to the $2.47 billion generated the same time one year earlier. Net income also increased, rising from $86.9 million to $103.5 million. Operating cash flow grew from $7 million to $22.8 million, while the adjusted figure for this expanded from $139.6 million to $163.3 million. Meanwhile, we also would have seen an increase in EBITDA, with the metric climbing from $164.4 million to $193.6 million.

Although there is significant uncertainty about the near-term outlook of the economy, management remains bullish about the firm. They see average WSEEs for the 2022 fiscal year as a whole coming in at between 17.5% and 18.5% above what they were last year. Earnings per share should be between $4.68 and $5.25, with a midpoint reading giving us net income of roughly $188.8 million. Meanwhile, EBITDA for the company should be between $305 million and $335 million. If we take the midpoint figure for that and apply it to the operating cash flow of the company, then we should anticipate a reading there of $262.1 million on an adjusted basis.

{kind=link}

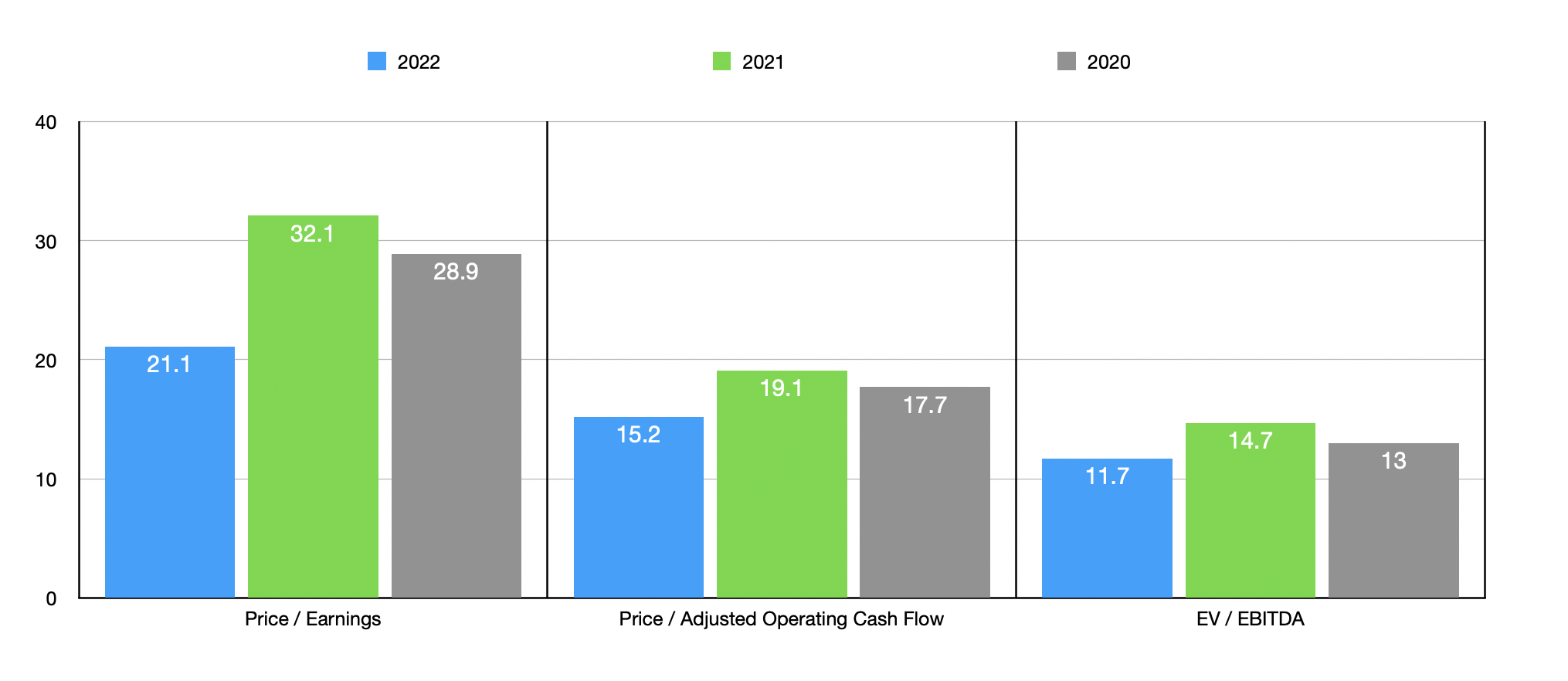

Using these figures, we can see that the company is trading at a forward price-to-earnings multiple of 21.1. The price to adjusted operating cash flow multiple should be 15.2, and the EV to EBITDA multiple should come in at around 11.7. If, instead, we were to use the data from the 2021 fiscal year as a more normal year, then these multiples would be 32.1, 19.1, and 14.7, respectively. Though if we drop back to the 2020 fiscal year, these numbers would be slightly lower at 28.9, 17.7, and 13, respectively. If we were to use the data from the 2021 fiscal year to price against five similar firms, we would find that shares are quite expensive at this moment. Those five firms are currently trading at price-to-earnings multiples of between 9 and 14.4. And they are trading at EV to EBITDA multiples of between 4.4 and 10.5. In both cases, Insperity is the most expensive of the group. If we use the price to operating cash flow approach, the range for these firms is between 6.1 and 36.3, with four of the five being cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Insperity |

| 32.1 |

| 19.1 |

| 14.7 |

| ManpowerGroup ( MAN ) |

| 9.0 |

| 8.1 |

| 5.6 |

| ASGN ( ASGN ) |

| 11.1 |

| 36.3 |

| 10.5 |

| Korn Ferry ( KFY ) |

| 8.1 |

| 6.1 |

| 4.4 |

| TriNet Group ( TNET ) |

| 13.3 |

| 9.4 |

| 7.7 |

| Kforce ( KFRC ) |

| 14.4 |

| 11.6 |

| 10.3 |

Takeaway

At this point in time, I can appreciate the business model and historical performance of Insperity. Having said that, shares don't look particularly appealing to me. They are definitely pricey relative to similar players and don't look exactly cheap on an absolute basis. I definitely believe that there are better prospects, including companies in this space, that are more appealing than it. I wouldn't go so far as to rate the company a 'sell', because shares don't look that pricey and because it is a quality operator that should continue to grow over the long run. But this definitely makes for a 'hold' in my opinion.

For further details see:

Insperity: Current Pricing Doesn't Inspire Confidence