ISPOW - Inspirato: Will This Business Really Work?

Summary

- Like so many de-SPAC mergers, Inspirato has disappointed since going public.

- At reasonable multiples to revenue and gross profit, and with some potential for growth, ISPO can't be written off.

- But the macro environment presents an obvious source of pressure, and structural concerns surround the important Pass product.

- Below $2, the core question is whether an investor believes in this business. Right now, I personally can't quite get there.

Earlier this year, a few market participants realized that:

-

de-SPAC mergers (in which companies go public via a merger with a so-called special purpose acquisition company) were closing with absurdly high redemption rates.

-

Those redemptions in turn led to exceptionally low floats immediately after the company came public.

-

And so there was an opportunity to (let's be honest) manipulate these stocks, at least in part by pushing a “short squeeze” narrative onto retail traders that could lead to steep, if unsustainable, near-term gains.

As a result, a number of thin-float de-SPACs, including luxury travel platform Inspirato ( ISPO ), went crazy. Redbox Entertainment, whose merger closed in October 2021, was one of the wilder examples. Even after the company agreed to sell itself to Chicken Soup for the Soul Entertainment ( CSSE ) for less than $1 per share in CSSE stock, traders still were trying to create a meme stock-style short squeeze , claiming (without evidence) nefarious manipulation from Wall Street.

Inspirato got caught up in this trend. Ahead of its SPAC merger, which closed in February, an incredible 98.5% of shares were redeemed . Three days after the merger closed, ISPO gained 648% in a single session. Fellow de-SPAC Cepton ( CPTN ), whose tie-up had closed a couple days earlier, went up more than 700% the same day.

That gain skews the performance of ISPO stock, which is down 98% from its all-time high of $108. But with shares down more than 80% from their merger price, that nutty rally aside the stock still clearly has struggled (even by de-SPAC standards).

At these levels, the stock does look cheap relative to revenue and gross profit. Top-line growth has impressed since the company's 2011 founding, and the business model at the least is intriguing. The core question, however, is how that business model will perform in what should be a very different environment. Personally, I'm not quite confident enough in mid-term success, but reasonable investors at this point can see it differently.

The Inspirato Model

Inspirato is a travel platform that focuses on luxury experiences. As of the end of the second quarter (Inspirato has not yet reported Q3 results), the company offered over 700 properties.

Unlike online travel agencies like Booking Holdings ( BKNG ), or platforms like Airbnb ( ABNB ) or Expedia Group ( EXPE ) unit Vrbo, Inspirato actually controls and operates the houses it offers to users. The company leases the properties (average term of four years) and then furnishes the homes, adding an on-site concierge for a truly high-end experience.

At its founding in 2011, Inspirato charged a monthly fee simply for the right to book its residences. In 2019, the company launched the Inspirato Pass, a subscription plan that for $2,500 a month (the price will increase 2% on January 1st) allows users to book stays with no incremental costs. Even taxes and fees are covered. (Users are responsible for flights, rental cars, and incidental spending).

Growth So Far

The Club offering has been a success, at least from a revenue standpoint. In Q2, subscription revenue was $36 million, 43% of the total. Pass subscriptions totaled 3,600, an increase of 75% year-over-year and up from zero three years earlier.

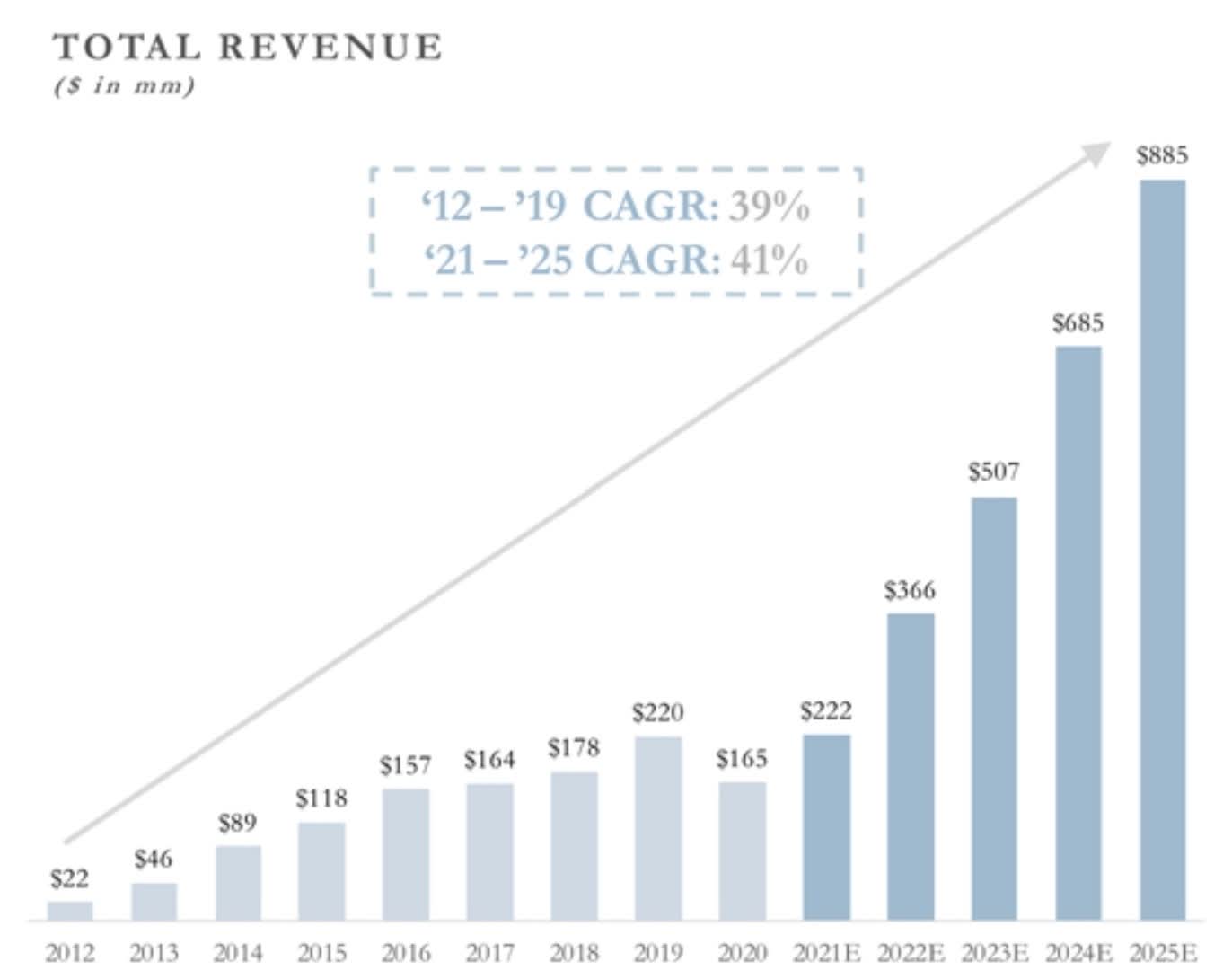

That growth underpins a still-impressive top-line profile. As of Q2, Inspirato was guiding for full-year revenue of $350 to $360 million. The midpoint of the range implies a 51% increase year-over-year. While the outlook is a modest disappointment against the projection made when the merger was announced last June, it still suggests a solid acceleration of growth against pre-pandemic performance:

{kind=link}

ISPO Valuation

As with so many de-SPACs, the out-year projections need to be taken with a shaker, not a grain, of salt. And it's worth noting that Inspirato is not yet profitable: Adjusted EBITDA is guided to a loss of $15 million to $25 million this year. With the figure running at -$17.7 million year-to-date, including a $14 million-plus loss in the seasonally weaker Q2, investors probably should be looking toward the weaker end of the range.

But Inspirato at least through the first half maintained the full-year outlook. And with $107 million in net cash at the end of Q2, cash burn (negative $31 million through the first half) should be manageable assuming losses moderate. That's the most recent expectation from management: chief executive officer Brent Handler said on the Q2 conference call that Inspirato expected to be EBITDA-positive in 2023 .

In that context, valuation at least is in the range of reasonable. Fully-diluted market capitalization sits at $233 million; with $107 million in net cash, Inspirato's enterprise value sits at $126 million. Against 2022 expectations, that implies an EV/revenue multiple of about 0.35x; EV/gross profit should come in at a little over 1x.

Given ongoing losses, neither multiple makes ISPO a growth play, certainly. But both are low enough to suggest some potential optimism for investors who believe the business model can work long-term.

The Case For ISPO

Indeed, below $2 the debate over ISPO comes down essentially to the question of whether this model can work. The stock is cheap enough to gain nicely if it does; the balance sheet is just stretched enough that concerns can arise in the mid-term if it doesn't.

What makes ISPO interesting is that there isn't really a precedent for the model. This isn't Airbnb or Expedia, but rather something relatively new in the space, and without a real direct peer among publicly traded companies. We haven't seen this model work before — but we also haven't seen it fail.

The case for ISPO is that, since founding, the business has worked, at least from a revenue standpoint. In eleven years, Inspirato has gone from zero to ~$350 million in revenue — and on roughly $85 million in raised equity capital. The business isn't profitable now, but Inspirato is spending up this year to add new properties, which depresses margins in the near term as demand ramps. Adjusted EBITDA and cash flow both were positive in 2019 and 2020, per the Q2 conference call.

There seems to be the potential for value here. Inspirato continues to add high-end hotels to its Club offering, who benefit from monetizing potentially lost rooms without actually disclosing pricing. (Pass subscribers use so-called "Pass Days" for their bookings; dollar rates aren't disclosed.) The control of vacation home properties allows Inspirato users to receive a guaranteed high-end experience, unlike the " vacation roulette ", as Handler has termed it, offered via Airbnb and other sites.

Those users seem relatively happy. Per Handler at the time of the merger, an annual retention in the pay-as-you-go Club product was 87% from 2017 to 2019. There are rules that prevent a user from using the platform 365 days a year (or anything close). But even with those restrictions it does appear from reviews that there are ways to find real value from a Pass subscription, even at a $30,000 annual price tag.

It seemingly doesn't take that much to go Inspirato over the hump to the sustainable profitability that can justify the $200 million-plus enterprise value required to drive upside in ISPO from here. (That rough $200M figure assumes some residual cash burn along the way.) Even the company's seemingly aggressive 2025 revenue projection only requires ~25,000 subscribers. That base would, per the company, support Adjusted EBITDA of $154 million, greater than the current enterprise value. At maturity, Inspirato estimated Adjusted EBITDA near $300 million, which in turn would suggest a multi-billion-dollar business, and massive upside in ISPO stock.

Macro And Demographics

Obviously, those projections don't have a ton of predictive value, given how few de-SPACs have even neared the projections they made at the time of the merger. And there is a real case that this model, though it grew revenue before the pandemic, is going to struggle notably afterwards.

The first risk is clearly the macroeconomic environment. A recession is not guaranteed, and Inspirato's high-income customers seemingly would have some protection against macro weakness. But for the Pass, a price tag which will exceed $30,000 in 2023 (and likely gets to $50K-plus when including travel and incidental expenses) means the external environment matters.

That's particularly true given that the company has cited "work from home" as a potential tailwind and (surprisingly) said at the time of the merger that only ~two-thirds of users had a household income over $250,000. That other one-third no doubt consists of retirees and childless users who may blanch a bit at the price tag if recession and/or inflation become larger, intractable problems. More generally, it's no doubt easier to sell a high-end product in a benign macro environment (as was the case pre-2020) and a time of rising asset prices (as may not necessarily be the case in 2023 and beyond).

A more structural risk is the addressable market. That addressable market here is consumers who:

-

can afford to spend a minimum of $20,000 annually on high-end travel (including off-platform spend and the fact that Club members are paying $7K-plus simply for the right to then pay cash);

-

and , for the important Pass product, are willing to poke around a website to find the best deal, and then adjust their travel plans based on the options available;

-

and have the available free time to use the platform multiple times a year.

It winds up being a relatively small demographic. There’s clear value for high net worth retirees; well-paid remote workers; some families; and maybe well-to-do DINKs (dual income, no kids).

But the nature of Pass Days, in particular, requires quite a bit of work. Booking a trip several months out minimizes usage on the pass until that point; booking a trip on short notice creates fewer choices and less flexibility. As a Pass holder told The Points Guy, the plan " does take effort ... and there is a little bit of a stress factor that I have to pay attention to."

The target market here is wealthy people who want a lot of luxury travel, but will tolerate "a stress factor" to gain a discount in the process. It's seemingly quite a narrow niche.

The Structural Question

The size of that niche, combined with the risk of a weaker macro environment going forward, raises the question of whether there's an eventual ceiling on revenue growth. But perhaps more importantly, it raises significant questions about the potential profitability of the business long-term.

Platform businesses generally have attractive economics. This is why Uber ( UBER ) was so dearly valued by venture capital investors, and why it still holds a $50 billion-plus market cap despite being unprofitable. Incremental revenue in a platform business is enormously profitable — once the platform is built, each added customer costs relatively little to service — and so revenue growth can drive swift, sharp margin expansion.

Though Inspirato compared itself to the likes of Airbnb and Expedia when it announced plans to go public, this actually is not that kind of business. Again, Inspirato itself manages and leases most of the properties being offered. As a result, gross margins are rather low: just under 35% in 2021.

That in turn means that incremental margins too are rather low. And so we're not likely to see massive, quick margin expansion even assuming revenue growth continues.

This problem is amplified by the fact that Inspirato needs to keep expanding its supply to match demand. The company has even offered a sale-leaseback program, Inspirato Real Estate , through which investors can buy a home from the company and then enter a lease agreement to be part of the Inspirato network. Handler said after Q2 that a higher interest rate environment might help as well, as existing owners or new buyers may not have as many options elsewhere to monetize their properties.

Inspirato can get the supply, but it has to walk a relatively fine line. Add too many properties on expensive leases, and margins plunge and cash burn piles up. (The company can exit most of its leases within a year, per past commentary, but it's still an expensive 12 months.) Add too few, and Pass and even Club subscribers become disgruntled.

Finally, for Pass, there's the adverse selection problem. Subscription programs benefit both from platform economics and from the fact that some users sign up and forget to cancel.

The latter trend seems exceptionally unlikely to benefit Inspirato much, given the price tag even for Club. But what can happen here is that the users who are getting the most value out of the Pass — and thus costing Inspirato the most to serve — will stay, while those who can't quite make the economics work leave.

That latter group, of course, would be the most profitable for Inspirato, whether those customers are reserving hotels or leased properties. And so the risk here is not just that the demographics put a ceiling on revenue, but on margins: the only customers who are multi-year users of Pass are those who will provide the least financial benefit to Inspirato.

On The Sidelines

Below $2, fundamentally the stock is tempting. There's a convincing argument that if Pass, in particular, works, the upside is multiples of the current stock price. A market confident in the success of Inspirato Pass could pretty easily assign a 2x or 3x EV/GP multiple here, which in turn suggests a double or better as that gross profit grows.

Given some levers to pull if the program disappoints, and new initiatives (a plan to provide corporate incentives does sound promising), downside probably is somewhat manageable over a 12- to 24-month period. Barring a disastrous economic situation, current cash should suffice. (The delay in Q3 financials, due to a pending restatement of past periods, is a modest concern. But Inspirato has said in a filing that the restatement should be relatively immaterial ; from here, the delay looks more like growing pains from a newly public company than a massive risk. That said, the fact that the accounting issues surround the treatment of leases for a company that leases all of its properties means that some investors could see it very differently.)

With an unproven business model (at least at the scale required to be a public company), that risk/reward could be seen as attractive. Quite honestly, no one knows how Pass will work out. At the merger price of $10, that uncertainty was a huge risk, and a key reason why the SPAC, Thayer Ventures, brought the merger valuation down during negotiations (see p.128) and shrunk the PIPE (private investment in public equity) to $100 million from $200 million. It's why 98%-plus of SPAC shareholders redeemed rather than choosing to own Inspirato post-merger.

Below $2, however, the same uncertainty seemingly skews the odds in the favor of bulls. If an offering that works gets the stock to $8 and one that doesn't gets it to $1, the odds of success don't need to be very high.

I'm tempted by that case, somewhat, and by the product itself. In fact, I fully expect I'll be a subscriber myself at some point in the future. But between the external risks to the business and the potential structural flaws in the Pass model, I can't quite get over the hump to being a shareholder. I'm fascinated to see how ISPO plays out, but for now I'm content to watch that process from the sidelines.

For further details see:

Inspirato: Will This Business Really Work?