DOOR - Installed Building Products: A More Cautious Approach Makes Sense

Summary

- Installed Building Products has had a great run in recent months, with shares roaring higher due to strong sales, profit, and cash flow growth.

- Shares look quite cheap right now and are fairly cheap compared to similar firms.

- Given changes in the space and because of the share price move higher, a more cautious approach to the business would not be unwise.

It's always great to re-evaluate your investments in order to see whether they still make sense to hold. This is especially true for companies that have experienced a tremendous amount of upside. And what better time to do this than when a company has just announced financial results for its most recent quarter? One such firm that just reported financial results for the final quarter of its 2022 fiscal year is Installed Building Products ( IBP ). With shares up significantly over the past few months, and the market in which the firm operates (insulation installation, waterproofing, rain gutters, etc…) rapidly changing, I can understand why investors might be a bit cautious. In the near term, we could see a decent deal of pain for the company. While I have no doubt that the long-term outlook for the company will be positive, I do think we have gotten to the point, from a valuation perspective, that a more cautious approach to the company might very well be warranted.

Building value

Things have been going very well for investors in Installed Building Products over the past couple of months. When I last wrote about the company in early December of 2022, I talked about the robust organic growth and acquisition-fueled growth that the company was experiencing. I did acknowledge at the time that the future offered some uncertainty because of the impact that inflation and rising interest rates would have on the housing and general construction markets. But because of how cheap shares were and how rapidly the company was continuing to expand both its top and bottom lines, I felt as though a ‘buy’ rating was still appropriate. Since then, the company has easily delivered on that. While the S&P 500 is down 0.2%, shares of Installed Building Products have seen upside for investors of roughly 30.5%.

{kind=link}

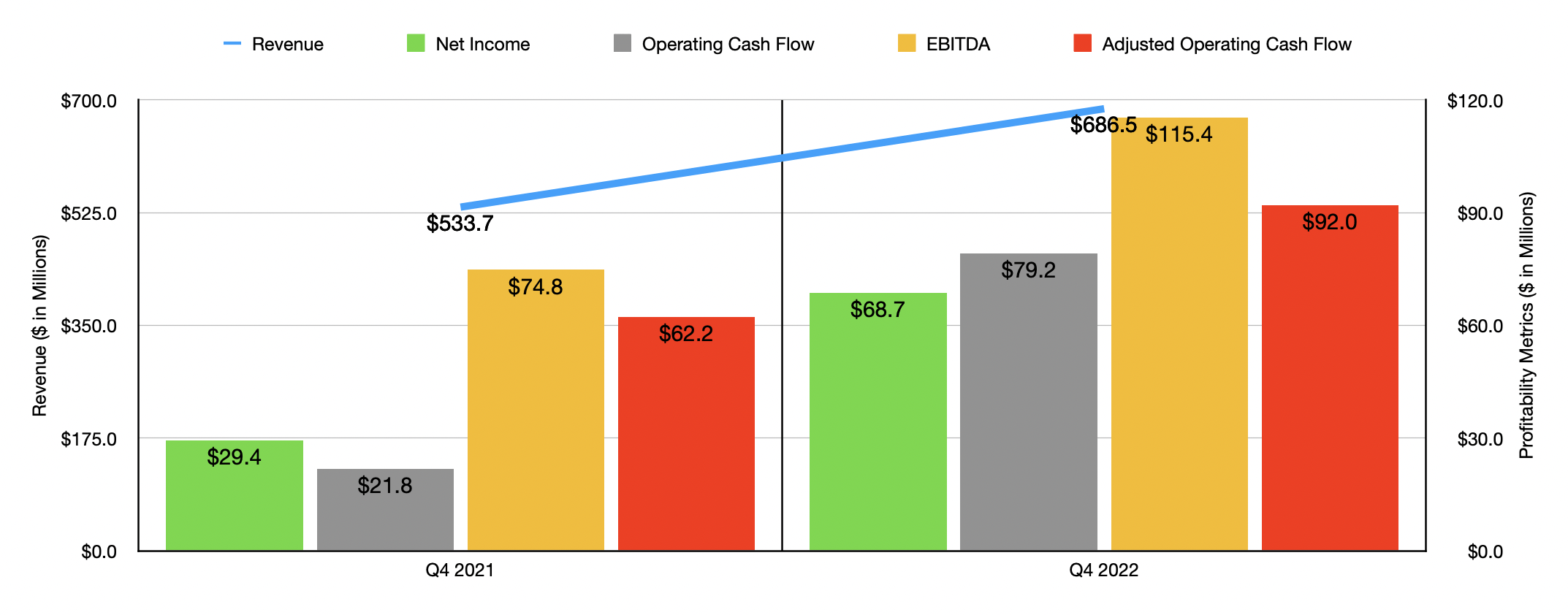

This massive return disparity was driven in large part by continued growth achieved by the business. For the final quarter of its 2022 fiscal year , for instance, the firm reported revenue of $686.5 million. That's 28.6% higher than the $533.7 million the company reported only one year earlier. It also beat analysts' expectations by roughly $5.3 million. Installation revenue for the company during this time spiked 22.7%, driven by strong growth across the company's residential new construction exposure. Revenue associated with the firm's manufacturing and distribution operations, meanwhile, jumped by $35.5 million year over year, thanks to both robust organic growth and acquisitions that the company had made.

Speaking of acquisitions, throughout 2022 as a whole, the company acquired other businesses that should collectively bring it annualized revenue of $109 million. That exceeded the $100 million in acquired revenue the company was aiming for. Subsequent to the end of the quarter, in February, the company purchased a residential installer of fiberglass and spray foam insulation with operations in Maryland and West Virginia. Revenue from that acquisition alone should add another $3.9 million to the company's top line moving forward.

On the bottom line, the company also did better year over year. Net income grew from $29.4 million in the final quarter of 2021 to $68.7 million the same time of the 2022 fiscal year. Total earnings per share for the company came in at $2.42. That beat what analysts expected to the tune of $0.52 per share. On an adjusted basis, earnings beat forecasts by $0.23 per share. In addition to seeing revenue grow, the company also benefited from a reduction in costs. Its gross profit margin, for instance, expanded from 29.3% to 31.7%. Even better was the improvement that the company saw in its selling and administrative costs. These declined from 18.2% of sales down to 15.3%. A big portion of this improvement, however, was temporary, caused by gains on acquisition earnouts totaling $15.1 million. Adjusting for this and other items would bring this change from 17.4% of sales to 16.7%. Other profitability metrics followed a similar path. Operating cash flow, for instance, shot up from $21.8 million to $79.2 million. If we adjust for changes in working capital, it would have risen from $62.2 million to $92 million. Meanwhile, EBITDA rose from $74.8 million to $115.4 million.

{kind=link}

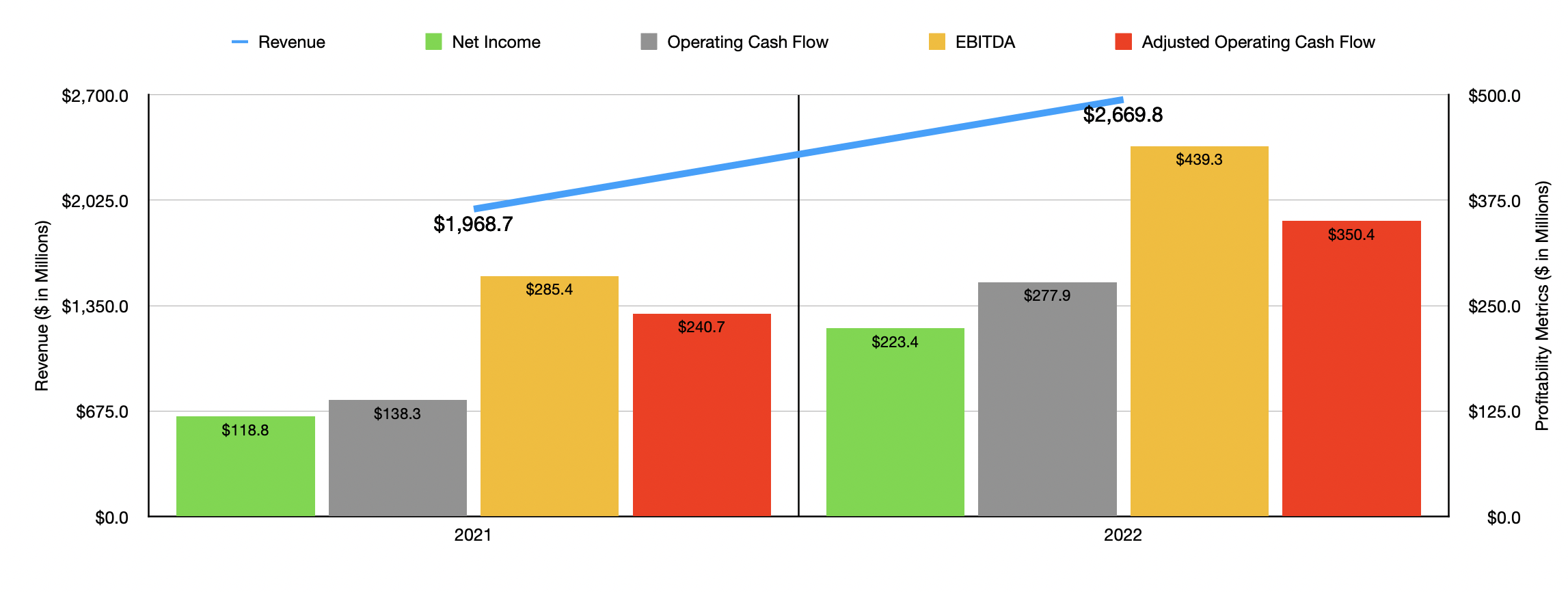

When it comes to the 2022 fiscal year in its entirety, the company did quite well. Revenue of $2.67 billion was 35.6% higher than the $1.97 billion reported one year earlier. This allowed the company to see a surge in net profits from $118.8 million to $223.4 million. Operating cash flow more than doubled from $138.3 million to $277.9 million. On an adjusted basis, it grew from $240.7 million to $350.4 million. And finally, EBITDA for the company expanded from $285.4 million to $439.3 million. In addition to engaging in various acquisitions throughout the year, the company also spent a great deal of money buying back stock. Throughout the 2022 fiscal year in its entirety, the business bought back over 1.5 million shares at a total cost of $137.6 million. This left the company with $162 million under its original stock buyback program. However, the top brass at the business decided to authorize a new stock repurchase program to replace the old one, allowing the company the ability to purchase up to $200 million of outstanding stock between the time it was implemented and early March of 2024.

{kind=link}

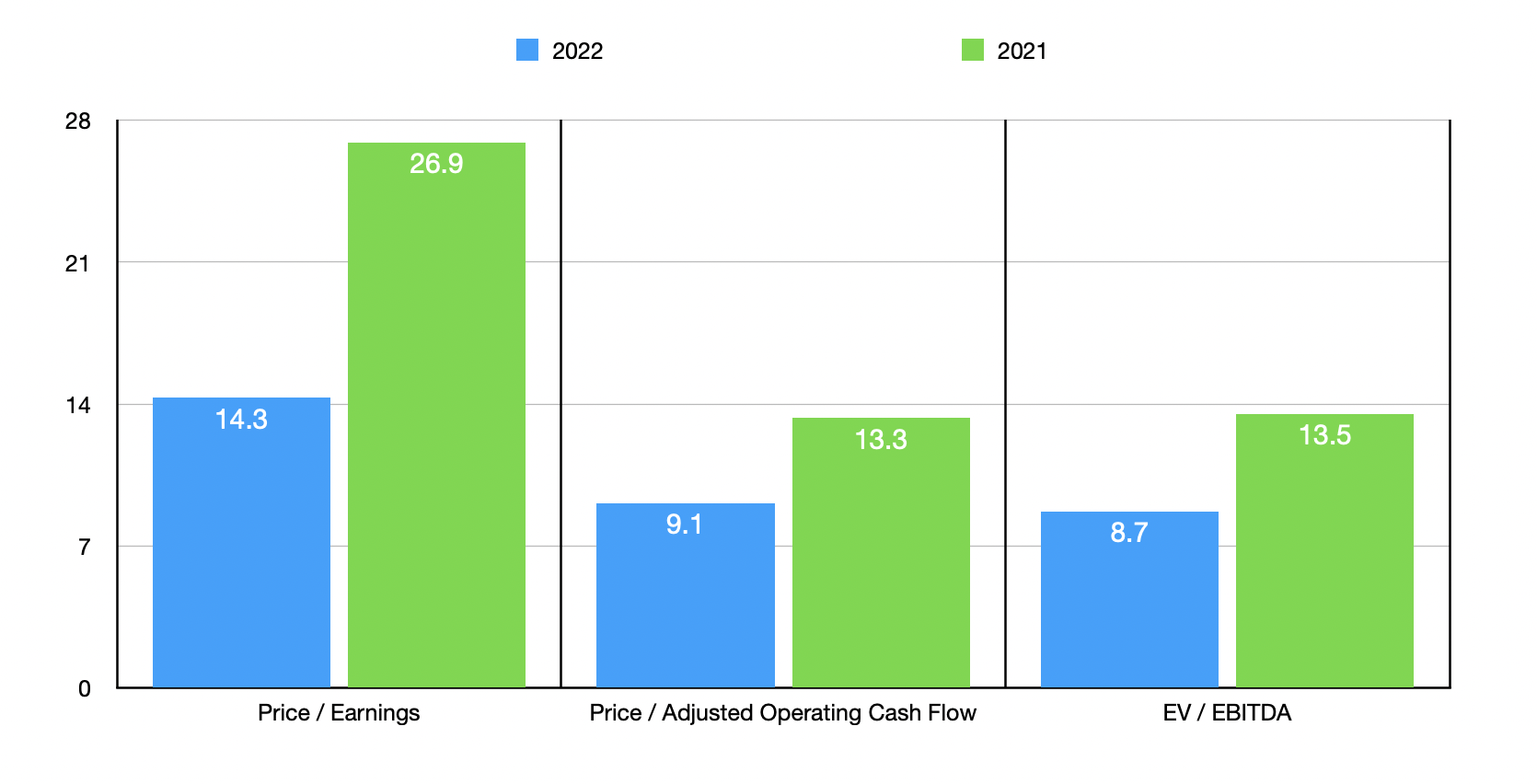

When it comes to the 2023 fiscal year, management acknowledged that there is uncertainty in the market. But they have not gone so far as to give us any real forecasts for the year. However, the company did say that they don't expect any downside experienced to last for multiple years. Instead of making any forecasts about the future, I decided to value the company based on results from 2021 and 2022. These can be seen in the chart above. In short, shares are cheaper if we use data from 2022. But they aren't unreasonably priced if we look at 2021 data either. In fact, they are just low enough to be optimistic about. As part of my analysis, I did also compare the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 6.5 to a high of 25. Two of the five companies I looked at are cheaper than Installed Building Products. Using the price to operating cash flow approach, the range was from 9 to 26.3. And when it comes to the EV to EBITDA approach, we get a range of between 7 and 15.1. In both of these cases, only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Installed Building Products |

| 14.3 |

| 9.1 |

| 8.7 |

| Masonite International Corporation ( DOOR ) |

| 12.2 |

| 14.0 |

| 7.0 |

| CSW Industrials ( CSWI ) |

| 25.0 |

| 26.3 |

| 15.1 |

| Griffon ( GFF ) |

| 6.5 |

| 9.0 |

| 9.2 |

| JELD-WEN Holding ( JELD ) |

| 22.6 |

| 25.7 |

| 8.9 |

| Gibraltar Industries ( ROCK ) |

| 19.4 |

| 22.1 |

| 11.8 |

Takeaway

Truth be told, I am somewhat on the fence regarding Installed Building Products at this time. Fundamentally speaking, the business is in really great shape. Sales, profits, and cash flows have all risen nicely year over year. Shares also look quite cheap on an absolute basis and they are cheap relative to most of their peers. Having said that, I do see this market growing worse and I believe that management is correct in saying that there is uncertainty when it comes to 2023. Because of how much shares have moved up and because of the uncertainty that lies ahead, I do think a more prudent approach would be to downgrade the company from a ‘buy’ to a ‘hold’ with the understanding that if we start to see evidence of a bottoming out in its market, then an upgrade could very well be warranted.

For further details see:

Installed Building Products: A More Cautious Approach Makes Sense