IBP - Installed Building Products: Declining Q3'23 Revenue Growth Impacting Valuation Multiples

2023-11-30 08:11:16 ET

Summary

- Installed Building Products reported a 1.8% decline in revenue in 3Q23, but net income and net income per share grew by over 10%.

- IBP has consistently improved its margins, including gross, operating, and net margins, since 2018.

- I expect strong growth in multifamily housing and increased volume due to the rise in single-family starts, supporting its future growth outlook.

Investment action

Based on my current outlook and analysis of Installed Building Products (IBP) stock, I recommend a buy rating. Although its 3Q23 reported revenue fell year-over-year, it was only down 1.8%. On the other hand, its net income and net income per share all grew by more than 10%. This impressive feat was not just shown in 3Q; in fact, it has been consistently doing that since 2018, when all its margins, such as gross, operating, and net, grew. Moving into the next quarter and onwards, IBP expects multifamily housing to have another strong year as its current strong backlog supports it. On top of the anticipated robustness in multifamily, IBP’s volume has been strong due to the recent increase in single-family starts. All of these drivers bolstered my growth outlook for IBP.

Basic Information

IBP is a company that operates in the insulation industry, providing a variety of installation services for residential and commercial buildings, including insulation, waterproofing, fireproofing, and garage door installation.

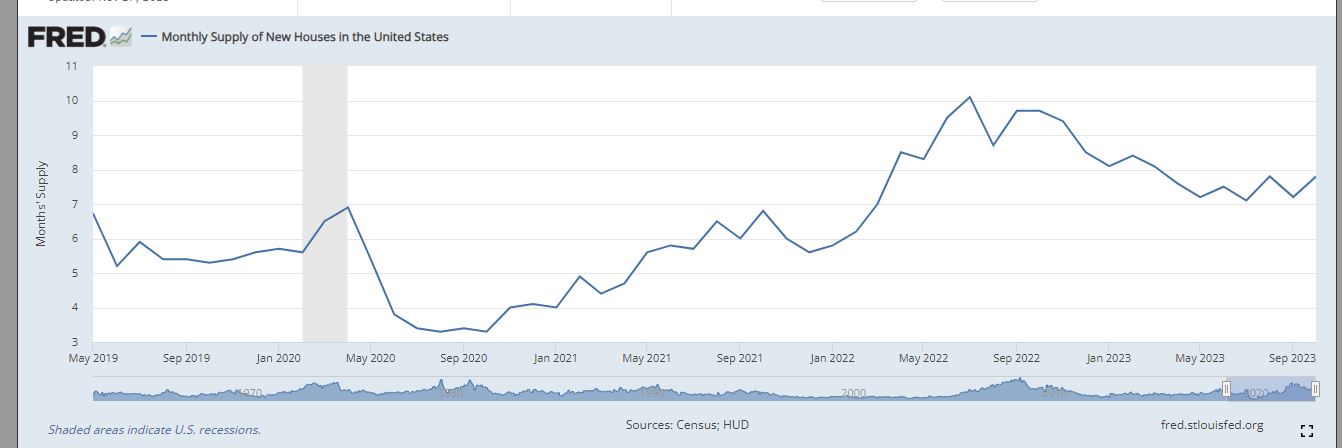

From 2018 to 2022, IBP’s revenue has had its ups and downs. Before COVID, it reported revenue growth of ~13% in 2019, but in 2020, it declined to ~9%. In 2021 and 2022, it reported growth of ~19% and ~35%, respectively. This growth rate is in line with the supply of new houses in the U.S., which moves in line with the interest rate as it determines mortgage rates.

{kind=link}

In terms of margins, IBP managed to improve all of them throughout the years [2018–2022). Gross margin improved from ~27% to 31%. Its operating margin also improved from ~7% to ~12%. The most impressive part would be its net margins, which improved from ~4% to ~8%. This is due to its effective cost management. Throughout this same period, SG&A fell from ~18% to ~16%, while COGS fell from ~72% to ~69%.

Review

In my view, IBP reported robust 3Q23 results despite revenue falling 1.8% year-over-year. The reason behind my view is that although revenue fell, it managed to improve its net income by 11.5% year-over-year. In addition, adjusted EBIITDA also improved to a record of $130.5 million. To top things off, net income per share on a diluted basis improved by 11.2%. This is very impressive in my view, and it speaks volumes about management’s cost management ability.

In my opinion, its ability to maintain the increase in profitability over the previous few quarters is really impressive. After increasing by roughly 1.5% to 2.6% in the previous three quarters, gross margin continued to grow, and it increased by 3.5% year over year in 3Q. The management underlined the following as key drivers: First, normalizing build times makes increased efficiencies possible. Secondly, after two years of high inflation, price-cost dynamics are improving. Thirdly, multi-family volumes are contributing positively to IBP. Lastly, commercial margins have turned from headwind to tailwind after 2022's weakness. Looking ahead, IBP believes that these dynamics will continue into the following years. As such, I think it's very possible for IBP to achieve the same gross margin in 2024. In addition, wage inflation has decreased, further bolstering my outlook.

IBP expects multifamily housing to have another strong year despite fierce competition. IBP's multifamily share is less than that of single families by about 10%, so there are still opportunities for share-gain, and the current strong backlog supports such activity through 2024. Nevertheless, management also recognized that, after backlogs are cleared, the multifamily segment will face challenges in 2025. After seeing significant improvement in heavy commercial, IBP is now concentrating on expansion in this area to capture growth. The management welcomed the strong bidding activity, especially in the manufacturing sector. In 2024, I predict a slight improvement in the commercial sector with growth in the heavy sector, somewhat offsetting softer trends in the light sector. Therefore, I believe the sustained strong multifamily housing demand, potential market share increases in multifamily, growth in heavy commercial areas, and a gradually improving commercial sector are key factors poised to drive IBP's future growth.

According to management, October's volumes were the highest of the year, which is consistent with the recent increase in single-family starts. In the long run, I anticipate that IBP will perform better than the overall market, particularly as large production builders gain market share and ancillary products become more widely available. As bidding has accelerated in tandem with record sales in October—a stark contrast to the underlying weakness in that end-market—heavy commercials should also contribute to growth. IBP put a lot of effort into stabilizing and increasing profitability last year, and both higher productivity and lower prices contributed to this. Lastly, multi-family backlogs remained steady through the third quarter, indicating roughly constant volumes through 2024 as gains in share counterbalanced the slowdown in starts. In addition, considering the possibility of increased material prices in addition to other expenses, I anticipate the price mix to be a slight tailwind. As production builders account for a greater share of sales over the next 12 months, these factors, in my opinion, should more than offset the negative mix shift. Thus, in 2024, I anticipate that volumes will drive the top line.

Valuation

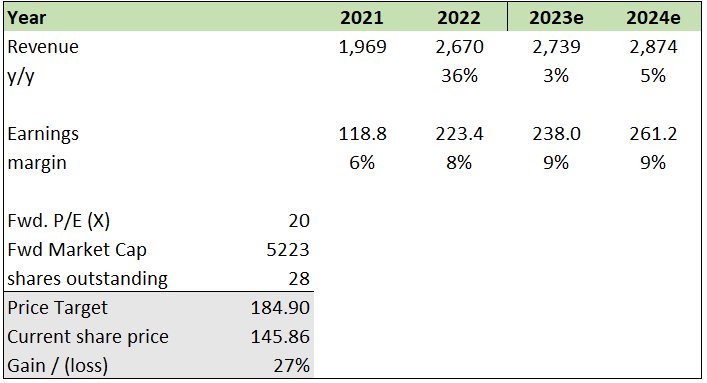

I believe IBP can grow by 3% in 2023 and 5% in 2024 because of the following factors: Although IBP reported a slight decline in its revenue, it managed to improve its net income and adjusted EBITDA. This demonstrates its strong cost management and operational efficiency.

On top of improving net income and adjusted EBITDA, it has also reported improvements in its gross margins. The factors driving this improvement are improved price-cost dynamics, more effective building processes, and encouraging trends in both the multifamily and commercial sectors.

Furthermore, IBP expects multifamily housing to have another strong year, and its benefits are expected to continue into 2024, driving IBP’s growth outlook. In terms of volume, IBP also reported its highest level of the year. With tailwinds from strong volumes and price mix, it also further supported my growth outlook for IBP.

{kind=link}

IBP is currently trading at ~14x forward P/E. Its peers are trading at a median of 15.55x. Given that IBP’s 17.41% EBITDA margin is higher than peers median of 9%, gross margin of 31% vs. peers’ median of 24%, EBIT margin of 12.94% vs. peers’ median of 7%, and net margin of 7.98% vs. peers’ median of 6%, I believe IBP should be trading at a higher forward P/E. In terms of the 2024 growth outlook, they are mostly in line. Peers’ median is 6%, while IBP is expected to grow 5%. With a similar growth outlook and better margins, I believe IBP should be trading at 20x forward P/E with a gain of 27%. Therefore, I am recommending a buy rating for IBP.

{kind=link}

Risk and final thoughts

Inflation will determine the growth outlook of IBP. As it operates in the insulation sector, its revenue is tied to housing demand. House demand is heavily impacted by the interest rate as it determines housing mortgage rates. If inflation were to rise again, it might prompt central banks to raise interest rates to combat inflation. In addition, higher inflation and mortgage rates not only dampen demand for housing but also reduce individuals' spending power. Lower spending power will also have a negative impact on IBP.

Despite a slight drop in revenue, IBP's strong 3Q23 results, which included robust improvements in its net income and adjusted EBITDA, showcase its excellent cost management. These improvements did not just occur in the current quarter. In fact, IBP has been showing this trend since 2018. In my opinion, I believe IBP is well-positioned for long-term growth that is supported by steady gross margins. The factors that drive my outlook are based on its better price-cost dynamics, effective building procedures, and favorable trends in the multifamily and commercial sectors.

In addition, I believe IBP is well positioned for growth due to strong expectations in multifamily housing supported by a solid backlog. This is accompanied by promising prospects in the heavy commercial sector, particularly in manufacturing, with overall growth expected to be bolstered by high volumes and positive market dynamics.

For further details see:

Installed Building Products: Declining Q3'23 Revenue Growth Impacting Valuation Multiples