IBP - Installed Building Products: Good Example Of Financial Stability And Growth

Summary

- Installed Building Products has shown top-line and bottom-line growth for the last 8 years.

- The company added over $100 MM from 10 acquisitions in 2022 and has similar plans for coming years.

- I would rate IBP stock as Buy.

Since its introduction to the secondary markets, Installed Building Products, Inc. ( IBP ) has been experiencing an upward trend. The company's net revenue, adjusted EBITDA, and net income have all grown at impressive compound annual growth rates of over 20%, 33%, and 40% , respectively, since 2014. IBP has also been actively pursuing expansion through acquisitions, having completed 10 in the past year, and planning to continue expanding in the future. Additionally, the company has implemented strong share repurchase programs and has started distributing cash dividends. Based on the fact that IBP's intrinsic valuation is slightly higher than its current market value, I would rate IBP a Buy.

About the company

Installed Building Products, Inc. and its affiliated companies are among the top installers of residential insulation in the continental United States. In addition to insulation, IBP offers installation services for various other products, such as fire-stopping, waterproofing, fireproofing, window blinds, shower doors, rain gutters, garage doors, closet shelving, and mirrors. The company also provides cellulose, fiberglass, and spray foam insulation products. IBP also focuses on air filtration and waterproofing products. With more than 230 branch locations, IBP serves a diverse customer base that includes homebuilders, homeowners, multi-family and commercial construction companies, and contractors.

Recent performance

In 2022, IBP experienced continued growth in both revenue and income, marking another consecutive year of success. At present, the company's revenue has reached an all-time high. Throughout 2022, IBP completed eight acquisitions, which contributed more than $100 million in annual revenue. Additionally, the company's EBITDA for 2022 increased to $439 million, a 54% rise compared to the previous year. IBP also exceeded EPS estimates for all four quarters and showed positive growth potential. Moreover, the company was able to generate $278 MM in cash flow from its operations during the current year, which is a significant increase from the $138 MM generated in the previous year.

Strengths

What appeals to me initially about IBP is its impressive financial stability and growth since its initial public offering ((IPO)) in 2014. Except for 2020, when the COVID pandemic impacted the market, the company has consistently achieved double-digit revenue growth. This suggests that IBP is led by a competent management team that has made sound decisions to expand the company and that they are likely to continue doing so in the future. The company's successful track record and growth are also reflected in the value of its stock, which has delivered returns of over 780% in just nine years.

IBP not only rewards its investors through its stock but also through dividends and share repurchases. In 2021, the company began distributing dividends and has already demonstrated an 80% increase in annual payout growth in 2022 by distributing $63MM in cash dividends. In 2022, IBP bought back 1.5 million shares at $138 million, and the board of directors approved an additional new share repurchase program. These actions demonstrate IBP's commitment to rewarding its investors and increasing its earnings per share ((EPS)). The management appears confident about the future of the company and believes that the stock is undervalued.

In 2022, IBP achieved success in acquiring 8 companies, including 3 in the last quarter, which contributed over $100 million in revenue. The company intends to continue with its robust acquisition strategy and capitalize on opportunities in the years ahead. During its recent earnings report , IBP announced its plans to acquire at least $100 million in revenue again in 2023. This indicates the potential for further revenue growth, providing even greater possible returns to investors.

IBP focuses on not just long-term growth but maintains sound short-term stability as well. With current and quick ratios of 2.7x and 1.91x respectively, the company ensures it has enough liquidity to fund its day-to-day operations and meet its short-term obligations. IBP’s cash and equivalents make up to 70% of its current liabilities.

Weaknesses

As noted earlier, IBP operates exclusively within the US market, which makes the company heavily dependent on the state of the US economy. This presents a significant weakness for the company as it is beyond IBP's control. Currently, with rising inflation and interest rates, consumers have less disposable income, which may potentially reduce demand for IBP's products and services.

Moreover, IBP's focus on homebuilding products makes it highly reliant on the performance of the housing market. According to money.com , the housing market is predicted to experience a downturn in demand in 2023, potentially due to higher mortgage rates, rising monthly payments, and reduced purchasing power. This may further impact IBP's business and the returns the investors are expecting.

Looking forward

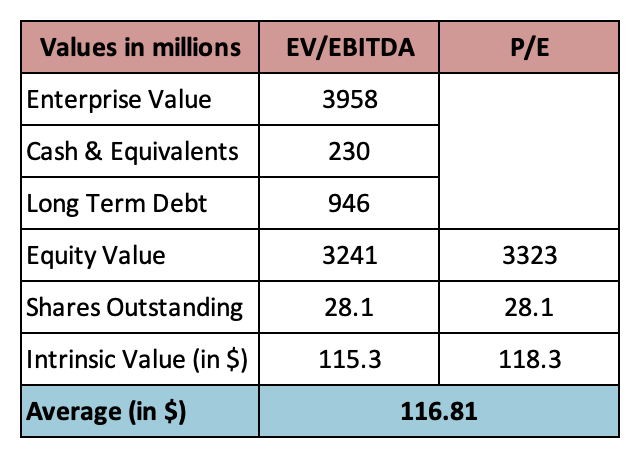

During the calculation of intrinsic valuation, I used multiples like EV/EBITDA and P/E to determine whether the current market price is overvalued or undervalued. An average value of $116.81 has been established compared to the current stock price of $114.42. This suggests that the stock is rightly valued in the market right now and the intrinsic value is still 2% above the current market value. The following assumptions were utilized in these valuations:

P/E Multiple - A sector median P/E multiple of 15.28x was considered compared to IBP's 14.90x.

EV/EBITDA - A sector median EV/EBITDA multiple of 10.47x was used in comparison to IBP's 9.43x.

Intrinsic Valuation (Created by author using data from Seeking Alpha)

{kind=link}

Conclusion

The solid growth of IBP impresses me. The fact that IBP not only generates returns for investors through stock price movements but also through dividends and share repurchase programs indicates that the investors may have multiple opportunities to benefit from IBP. Additionally, my current valuation suggests that IBP is accurately valued at the moment. Despite the news that 2023 may be a slow year for the housing industry, IBP’s current acquisition and future plans indicate that it may still be able to generate returns for its investors. Therefore, I would rate IBP as Buy.

For further details see:

Installed Building Products: Good Example Of Financial Stability And Growth