IIIN - Insteel Industries Is Offering A Good Entry Point

2023-04-12 08:54:37 ET

Summary

- Demand is slowing down due to high customer inventories and rising interest rates after strong fiscal 2021 and 2022.

- Profit margins have been heavily impacted by declining steel prices and lower demand.

- The company's balance sheet is very robust thanks to its zero-debt position and high inventories.

- The fixed dividend is safe, but don't expect more special dividends until current (and potential) headwinds ease.

- The recent share price decline represents a good opportunity to start averaging down.

Investment thesis

The current fiscal 2023 is beginning with many complications in the operations of Insteel Industries ( IIIN ) as the impact of rising interest rates caused a decline in the company's net sales in residential-related markets during the first quarter. Net sales also declined in non-resident markets during the quarter as steel prices declined (and thus product prices) and customers are loaded with very high inventories due to extended lead times in past quarters. Furthermore, profit margins have also plummeted during the past quarter as a result of declining volumes and declining average selling prices as competitive pricing pressures remained strong, which translated into much lower cash from operations.

Despite this, the company enjoys a debt-free balance sheet and very high inventories as the company replenished them at depressed raw material prices earlier in 2022, which provides it with enough resources to withstand current headwinds. In addition to these headwinds, the fear of a potential recession is also having an important weight in the current fall of the share price, which has already accumulated a decline of 38.26% from all-time highs reached in May 2021, but high inventories will also serve the company to cushion the impact of a potential recession if it finally materializes. In this article, I am going to explain why Insteel Industries represents a good opportunity at current share prices, and also why investors interested in the company's shares should opt for averaging down as the ideal investment strategy.

A brief overview of the company

Insteel Industries is the American largest manufacturer of steel wire reinforcing products for concrete construction applications. The company manufactures and sells prestressed concrete strand and welded wire reinforcement, including ESM, concrete pipe reinforcement, and standard welded wire reinforcement. It was founded in 1953 and its market cap currently stands at $528 million, employing almost 1,000 workers.

{kind=link}

During fiscal 2022, 85% of net sales were provided by sales of concrete products to other manufacturers for non-residential construction, whereas 15% were related to residential construction. Although the current fixed dividend yield on cost at current share prices stands at just 0.44% due to a very conservative fixed dividend of $0.03 per share, the company pays very generous special dividends when cash from operations is high, which makes it worthwhile to hold its shares over the years, but due its cyclical nature, it is necessary to wait for an uncertain economic landscape that triggers pessimism among investors in order to achieve a high (special) dividend yield on cost or, failing that, high capital gains when prospects are strong enough again by taking advantage of a pick-up in optimism and sell the shares at a price significantly above the purchase price.

Currently, shares are trading at $27.48, which represents a 38.26% decline from all-time highs of $44.51 on May 04, 2021. This represents a significant decline in the share price as lower steel prices, inflationary pressures, strong competition, and decreasing demand due to rising interest rates and high customer inventories are impacting the company's profit margins on the brink of a potential recession that could further impact demand for the company's products, and although part of the potential impact that a recession could have on the company's operations is reflected in the share price, its materialization could sink the share price even more, so I suggest investors opt for a conservative strategy based on averaging down from current share prices. First of all, I would like to mention the most recent acquisitions, which have allowed the company to expand its production capacity over the past few years.

Recent acquisitions

In August 2014, the company acquired the prestressed concrete strand business of American Spring Wire Corporation for ~$36 million. A few months later, it closed the acquired company's facility located in Newnan and moved its production to existing facilities in order to achieve around $3 million in cost savings.

In November 2017, the company acquired certain of the assets of Ortiz Engineered Products for the manufacturing process of welded wire reinforcement, which was already manufactured by the company at six facilities across the United States.

And the latest acquisition took place in March 2020 when the company acquired Strand-Tech Manufacturing, a leading manufacturer of prestressed concrete strand for concrete construction applications generating $29.0 million in sales in fiscal 2020, for $22.5 million, and sold Strand-Tech's manufacturing facility in order to move production to three existing manufacturing facilities in order to leverage operating costs and optimizing manufacturing capabilities.

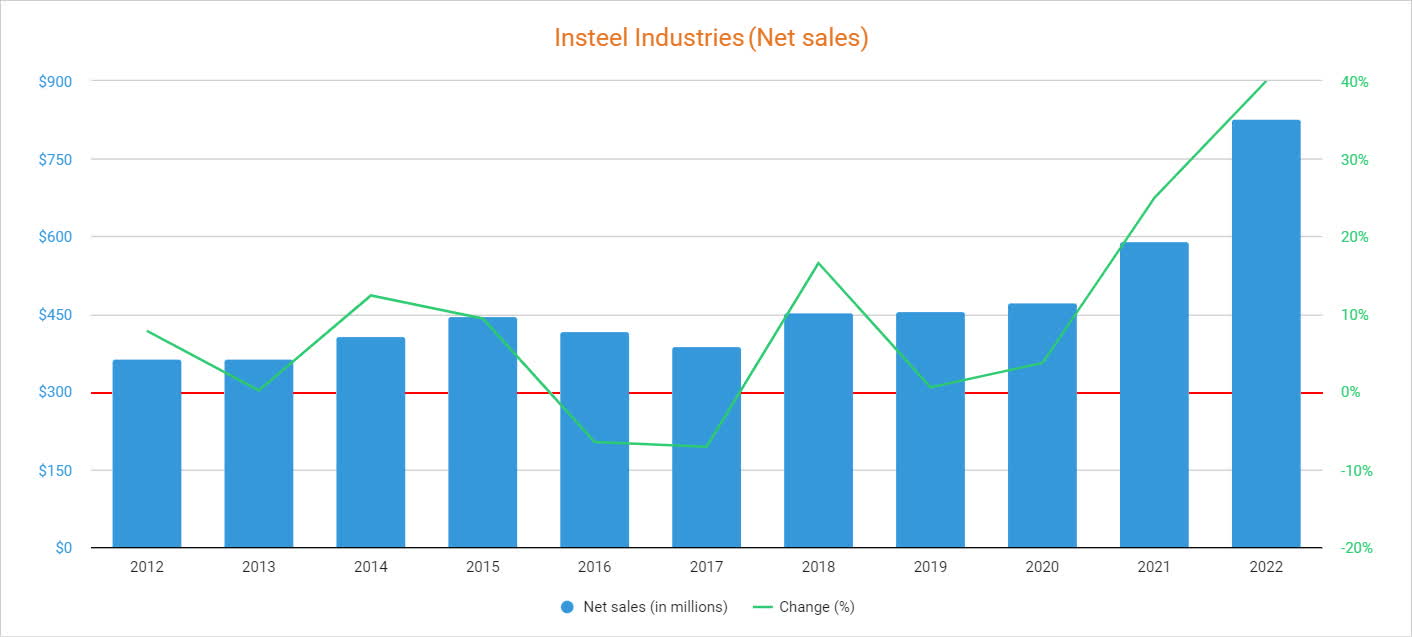

Net sales are deflating after a strong fiscal 2022

The company's net sales have remained stagnant for the majority of the past decade but closed 2020 with record-high net sales. Thereafter, net sales skyrocketed following the lifting of coronavirus pandemic restrictions as they increased by 24.96% in fiscal 2021, and increased again by 40.00% in fiscal 2022, both increases boosted by increasing steel prices.

{kind=link}

As for fiscal 2023, net sales declined by 6.48% year over year during the first quarter (shipments actually declined by 10%, but price increases of 3.9% on average softened the impact), and by 19.76% quarter over quarter (as a consequence of a 12% decline in shipments and an 8.8% decrease in average selling prices) as residential-related markets began to weaken due to recent interest rate hikes. Net sales for the non-residential market also weakened as a consequence of customer inventory destocking after a few quarters of abnormally long lead times. In this regard, the company's customers are no longer concerned about potential order delays and are thus depleting their reserves, which means net sales could stay depressed for some more quarters.

Rising net sales (despite the recent decline) along with declining share prices have caused a drop in the P/S ratio to 0.661, which means the company currently generates net sales of $1.51 for each dollar held in shares by investors, annually.

This ratio is 38.97% lower than the average of 1.083 for the past decade and represents a 65.84% decline from decade-highs of 1.935, which means that investors are placing less value on the company's sales. This pessimism is, in my opinion, due to three main factors: firstly, net sales are expected to decrease (by 10.60% in fiscal 2023 followed by a partial recovery of 9.07% in fiscal 2024) after the boost experienced in fiscal 2021 and 2022 due to lower demand and steel prices. Secondly, there is the fear of a potential recession, which would most likely lead to a further decline in net sales, and finally, we have depressed profit margins as a result of declining volumes, declining product prices, and increased operating costs due to inflationary pressures.

Profit margins dropped abruptly as the gap between raw material prices and product prices declined while operating costs increased

The company achieved positive gross profit and EBITDA margins during the past 10 years, which has made it possible to achieve positive cash from operations year after year. In this regard, the trailing twelve months' gross profit margin currently stands at 21.19% and the EBITDA margin at 19.67%, but they are showing strong signs of contraction due to declining product prices, increased production costs, and lower volumes.

More specifically, the gross profit margin dropped to 10.66% during the first quarter of fiscal 2023 as shipments declined by 12% quarter over quarter and average selling prices by 8.8%. This represents an 840 basis points decline in profit margins quarter over quarter, which is a very significant drop. In this regard, the spread between average selling prices and raw material costs has narrowed significantly while plant operating costs remained higher than usual due to declining volumes. The recent decline in the price of iron ore, which is used for the production of steel, has eliminated the tailwind that the company enjoyed during the rally experienced in the second half of fiscal 2020 and the whole of 2021, in which it could continually raise the price of its products and thus recover the higher replacement costs for raw materials while depleting lower cost inventories at higher product prices.

Iron ore commodity price (Tradingeconomics.com/commodity/iron-ore)

{kind=link}

Therefore, profit margins are expected to remain depressed as long as the price of iron ore remains low and product demand remains weak. And for demand to come back strong, interest rates should first fall, and for this to happen, a moderation of current high inflation rates will first be necessary. But if the interest rate hikes carried out to moderate said inflation rates cause a recession, the demand would continue to be depressed until the recession is overcome. That is why the company will most likely need to make use of its inventories to face any of the scenarios that arise: high interest rates and/or a potential recession.

The balance sheet is strong thanks to zero debt and high inventories

One of the company's strongest points is that its balance sheet is totally debt free. In addition, it has cash and equivalents of $42.64 million and high inventories of $171.19 million.

These inventories have been filled thanks to the abnormally low prices experienced during fiscal 2022 as the company took advantage to produce products at a low cost, but a new fall in the price of steel is once again devaluing the company's inventories, which is driving profit margins to abnormally low levels. In this regard, the company is operating in a macroeconomic context marked by high volatility in the commodity markets, and that is why profitability is plummeting after strong fiscal 2021 and 2022.

The fixed dividend is safe as the cash payout ratio is very low, but don't expect special dividends in the short term

The company's dividend policy is very conservative. It pays a fixed quarterly dividend of $0.03 per share, which represents a fixed dividend yield of 0.44% at current share prices, and distributes its excess cash to shareholders in the form of special dividends when possible, which gives the management a high degree of adaptability based on the company's profitability each year. In the following graph, you can see the special dividends that the company has issued in the past decade.

In the following table, I have calculated what percentage of the cash from operations the company dedicated each year to cover dividends (both fixed and special). I have decided to use cash from operations as the base data since in this way we can assess the sustainability of the dividend using the cash generated through actual operations.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $29.23 |

| $35.77 |

| $54.54 |

| $20.84 |

| $53.97 |

| $6.61 |

| $56.22 |

| $69.88 |

| $5.67 |

| Dividends paid (in millions) |

| $2.19 |

| $2.21 |

| $20.86 |

| $26.01 |

| $21.33 |

| $2.31 |

| $2.31 |

| $31.29 |

| $41.16 |

| Cash payout ratio |

| 7.50% |

| 6.18 |

| 38.25 |

| 124.81 |

| 39.53 |

| 34.96 |

| 4.11 |

| 44.78 |

| 725.96 |

As we can see in the table, the company's cash payout ratio (for both fixed and special dividends) remained low over the years thanks to high cash from operations, but fiscal 2022 closed with a whopping 725.96% cash payout ratio as a result of very low cash from operations of $5.67 million. Still, inventories increased by $118.7 million compared to fiscal 2021 and accounts receivable by $13.7 million while accounts payable declined by $2.6 million. In this regard, fiscal 2022 was actually a very profitable year thanks to the increase in inventories (which is due in large part to the revaluation of its inventories throughout the year) and accounts receivable, although these inventories are losing value again as iron ore prices can't take off.

As for the first quarter of fiscal 2023, cash from operations was $33.0 million, but inventories declined by $26.5 million quarter over quarter and accounts receivable by $12.8 million while accounts payable declined by $16.0 million. As a result, investors' pessimism is growing as the company reported net earnings of $11.1 million (although $3.3 million is attributable to the sale of property, plant, and equipment) compared to $23.1 million a year ago. For this reason, further special dividends should not be expected until steel prices stabilize, demand picks up again, and a potential recession is out of the macroeconomic scenario, for which patience will be needed, almost certainly, for quite more quarters.

Risks worth mentioning

Although I consider Insteel Industries' risk profile to be low thanks to a debt-free balance sheet and very high inventories, there are certain risks to shareholders that I would like to highlight.

- Just as the company enjoys very high inventories, its customers' inventories are also at very high levels. This could force the company to deplete its inventories at prices below current ones, which would have a significant impact on the company's ability to convert such inventories into actual cash. Furthermore, the company could have trouble depleting its inventories if demand continues to drop and the company is unable to reduce its production capacity without affecting its profit margins due to less utilization of its workforce.

- It should also be noted that if steel prices keep falling the company's profit margins could remain depressed for longer than expected by investors, leading to a further share price decline and a more gradual subsequent recovery.

- A potential recession could have a double impact on the company's profit margins. First, lower demand would result in a reduction in volumes, and second, a potential fall in the price of steel to levels below current ones would result in reduced profit margins as the company would be forced to sell higher-cost products at lower prices.

- Another risk that I would like to highlight is share dilution. In this regard, the total number of shares outstanding increased by 7.94% during the past decade, which means that each share represents an ever-smaller portion of the company as it virtually doesn't perform share buybacks.

Conclusion

Insteel Industries' share price has not fallen in vain. Fiscal 2023 began with a significant net sales decline as a result of lower demand and an average selling price below that of previous quarters. This has caused a significant impact on profit margins, which will likely force the company to empty part of its inventories in the coming quarters in order to generate positive cash from operations. The problem is that customer inventories are also high as they stockpiled products in previous quarters as a result of supply chain issues that lengthened the time it took for orders to arrive.

Despite this, we must not forget that the company enjoys a debt-free balance sheet and relatively high cash and equivalents and that inventories will serve as a safety net against current headwinds and a potential recession, and therefore, I consider that the recent fall in the share price represents an opportunity for those investors focused on the long term who wish to obtain a high fixed (and special) dividend yield on cost, and also for those whose intention is to sell when the company's prospects improve and optimism returns to the surface among investors. Nevertheless, the possibility of a potential recession finally materializing suggests that it would be a wise idea to keep at least one bullet in the chamber as such a scenario could plunge the share price significantly below current prices, opening the window to the opportunity of acquiring shares at even better prices.

For further details see:

Insteel Industries Is Offering A Good Entry Point