INTA - Intapp: A Solid Balance Between Innovation Growth And Profitability

2023-09-06 09:16:08 ET

Summary

- Intapp is a software company that mainly serves the $3.5 trillion digitally-lagging financial services industry.

- The company is poised to sustain its impressive revenue growth trajectory over the long-term.

- According to my valuation analysis, the stock looks fairly valued.

Investment thesis

Intapp ( INTA ) is a rapidly growing business that aims to contribute to the digital transformation of a $3.6 trillion financial services industry. The company invests heavily in R&D and marketing, which helps to win big clients at a very impressive pace. Given positive secular trends for the company and its commitment to innovation, I have a high conviction that Intapp is able to sustain double-digit revenue growth over the long term. As the revenue grows, the company is highly likely to benefit from the economies of scale effect, substantially expanding profitability metrics. My valuation analysis suggests the stock is approximately fairly valued, but businesses with such an aggressive growth profile and massive secular tailwinds should trade with a premium. All in all, Intapp is a "Buy" for me.

Company information

Intapp is a provider of industry-specific, cloud-based software solutions for the global professional and financial services industry. Intapp offers a comprehensive platform that covers multiple clients' operation domains, including relationship management and client engagement lifecycle.

Intapp's latest earnings presentation

{kind=link}

Intapp's fiscal year ends on June 30 with a sole operating segment. According to the latest 10-K report , about 30% of the total sales are generated outside the U.S.

Financials

Intapp went public relatively recently, in the summer of 2021. We have a short history of publicly available earnings and financial performance. But we can see some trends already. For example, revenue is compounding at a massive 24% CAGR, which looks promising for the company. As a young business, the company invests heavily in innovation and marketing. That said, the operating margin is still negative. On the other hand, the gross margin above 60% is wide enough to be optimistic regarding the operating margin as the business will continue to scale up and is likely to bring the economies of scale effect.

Author's calculations

It is crucial to mention that, despite being negative, the free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] is not that much below zero. Therefore, there is a high probability that the company will start generating positive ex-SBC FCF in the near future. A low cash burn is why the company's balance sheet looks solid. Intapp is in a substantial net cash position, and the leverage level is very low.

Seeking Alpha

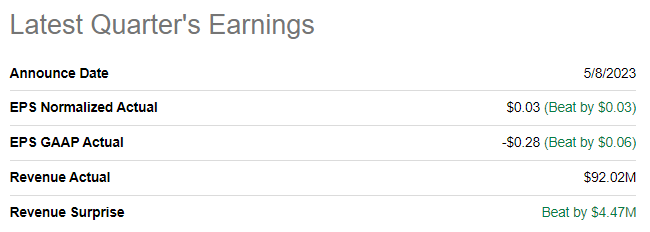

The latest quarterly earnings were released on May 5, when the company topped consensus estimates. Revenue demonstrated solid growth momentum with a 32% YoY growth. The adjusted EPS followed the top line and improved notably from -$0.47 to -$0.28. Profitability metrics improved substantially. The gross margin expanded by more than six percentage points, and the operating margin expanded even more notably, from -41% to -21%. It is important to underline that the operating margin expansion was due to the decreased SG&A to revenue ratio and not at the expense of R&D.

{kind=link}

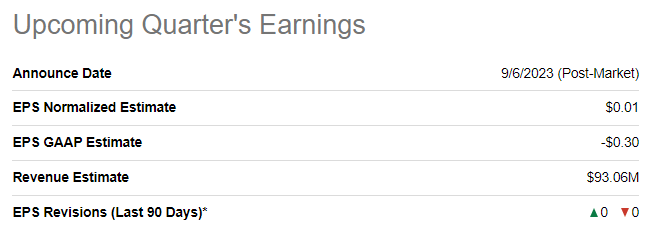

The upcoming quarter's earnings are scheduled on September 6, post-market. Quarterly revenue is expected by consensus at $93 million, indicating a solid 23% YoY growth. It is important to emphasize that the adjusted EPS is expected to turn positive for the first time.

{kind=link}

I think that the company operates in a promising niche. Most financial services companies in the developed world have vibrant histories tracing decades or even centuries ago. Financial services companies are mostly conservative, and data privacy and safety are one of the major concerns for this industry. That said, the pace of digitalization in the financial services industry has been lagging in recent years. However, disruptive fintech companies force traditional financial service companies to accelerate innovation. Industry leaders set the tone, and we see that JPMorgan Chase ( JPM ) and Bank of America (BAC) are allocating more than $10 billion in their annual IT budgets . That said, secular shifts are favorable for Intapp. It is also important to understand that IT spending is not a cost for customers but an investment. Digitalization helps streamline internal processes and improve operating efficiency, meaning that customers are unlikely to cut on this spending even during times of challenging environment.

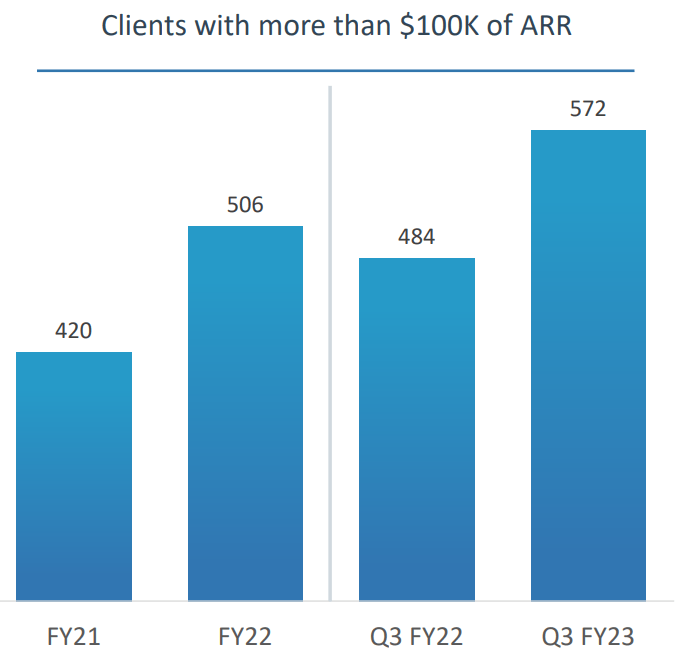

Yes, the overall competition in the software industry is fierce. However, Intapp focuses mainly on the very specific financial services industry, where competitors must understand the customer's needs well. Based on the dynamics of the number of clients with annual recurring revenue [ARR] of more than $100,000, it is highly likely that Intapp is good at understanding how to deliver value to its customers. The company targets a massive $3.5 trillion financial services industry, where almost a million businesses operate across the U.S. The addressable market is huge and digital transformation in the industry has started just recently. That said, I have a high conviction that Intapp will be able to sustain double-digit revenue growth over multiple years.

Intapp's latest earnings presentation

{kind=link}

Wide gross margin, together with a positive trend in the SG&A to revenue ratio, also suggests that the economies of scale effect will be massive for the business, and there is a high probability that Intapp will generate substantial profitability metrics over the long term.

Valuation

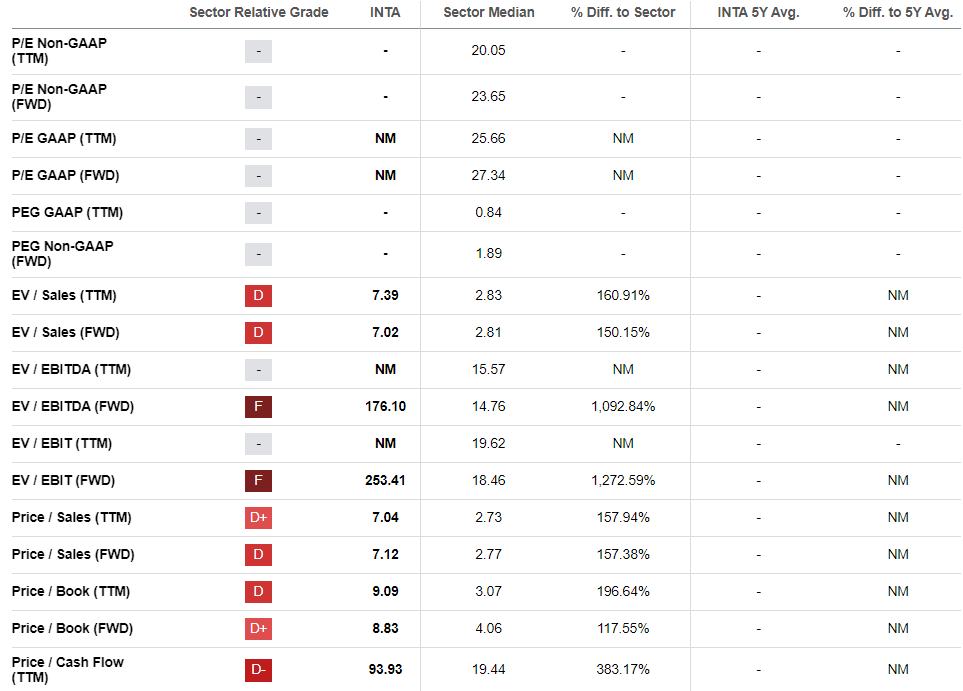

The stock rallied 48% year-to-date, significantly outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a low "D" valuation grade because of substantially higher multiples than the sector median.

{kind=link}

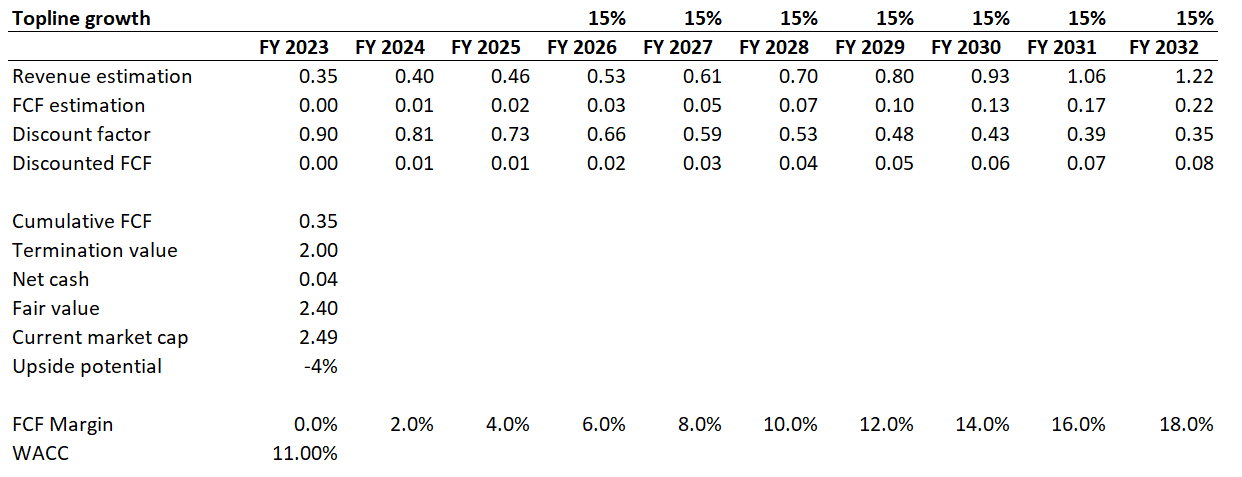

I want to continue my valuation analysis with the discounted cash flow [DCF] simulation to get more evidence. I use an 11% WACC for discounting. Consensus revenue estimates are available up to FY 2025. For the years beyond, I have implemented a 15% revenue CAGR. I expect a zero FCF margin for the base year with a two percentage points yearly expansion.

{kind=link}

Based on the above assumptions, the stock looks approximately fairly valued with a slight premium. That said, despite relatively high valuation multiples, I consider the stock fairly valued at the current stock price level.

Risks to consider

We have a concise earnings history of Intapp. Of course, past success does not guarantee future success, but the longer the historical trend horizon I see, the more conviction about the future it gives me. In our constantly and rapidly evolving world, it is important for the business to adapt and innovate. Businesses with a long history of success have a proven track record of the management's ability to adapt and face different types of crises. That said, Intapp's short publicly available track record increases the level of uncertainty about the company's execution in future.

As a growth company, Intapp is under big pressure to meet ambitious revenue growth and profitability expansion plans. Earnings consensus estimates misses or guidance downgrades might lead to investors' disappointment and a subsequent massive stock sell-off. Even if headwinds would be temporary for the company, the market sentiment regarding the stock might be substantially undermined over multiple quarters. That said, potential investors should be ready to tolerate near-term volatility and hold the stock over the long term.

As a software company serving to digitalize clients' processes related to their clients, the company stores and is responsible for the safety of sensitive information. That said, the company faces substantial cybersecurity risks, especially in case of sensitive information leaks. This will significantly undermine the company's reputation and might lead to customer relationships loss. In turn, this will adversely affect the company's market share and its earnings.

Bottom line

To conclude, Intapp is a "Buy" for investors looking for a long-term potential moonshot. The company demonstrates a solid balance between investing in innovation, achieving massive growth, and profitability metrics improvement. The market that Intapp targets is massive, and the digital transformation for financial services industries is a big tailwind. While the business's fair value and the market cap are close, I believe that such a rapidly growing business, which is ready to turn profitable, should trade with a substantial premium.

For further details see:

Intapp: A Solid Balance Between Innovation, Growth, And Profitability