HAE - Intellia Therapeutics: The Future Is Here

2023-07-26 23:18:28 ET

Summary

- Intellia is a pipeline-stage firm, leveraging gene-editing technology to develop therapies for rare diseases. NTLA is on track toward key data and regulatory catalysts.

- Early clinical data in HAE and ATTR have provided solid validation for Intellia's pipeline, and I believe its platform potential is highly attractive and overlooked by investors.

- Intellia has strong partnerships and is well capitalized, with many data-rich catalysts in the near term to keep investors engaged.

- Overall, I believe NTLA is undervalued based on the pipeline and technology engine and has attractive upside potential. My 12-month price tag is $89 based on a 10-year DCF analysis.

As you might know, Intellia Therapeutics (NTLA) is a biotech company that uses gene-editing technology to craft therapies for rare diseases and cancer. I've been a fan of Intellia for a good while, and here's my simple reason for investing: (1) Early tests have given the thumbs up for Intellia’s future work; (2) The company's potential is vast and varied with many exciting developments on the horizon; (3) They've got some strong allies in the field; and (4) Overall, Intellia is an interesting player in the industry with a fantastic team steering the ship and promising prospects for growth.

Investing in a biotech firm like Intellia isn't your usual value or growth stock game. Instead, you're betting on their ability to tackle diseases that have, till now, stood undefeated.

While I'm eager to endorse NTLA as a 'buy', factors like impending share dilutions, a projected revenue drought, and notable investment risks prevent me from pushing for a 'strong buy'. So, I kick-off my coverage of this gene-editing biotech with an $89 price tag based on my DCF analysis and recommend investors consider a long-term buy-and-hold strategy.

Introducing Intellia

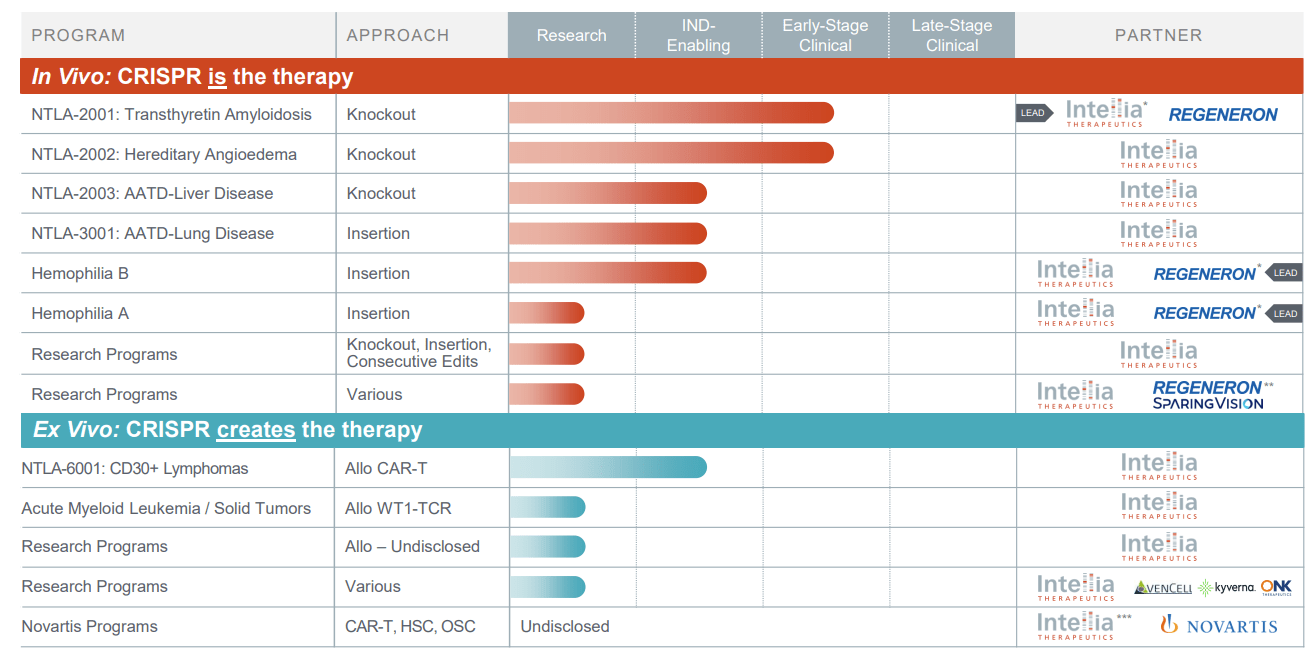

I encourage all investors to take a stroll through Intellia’s website – it's pretty much a one-stop shop. They break down how their tech works , what their approach is, the diseases they're trying to beat, and who these diseases affect. See below for NTLA's pipeline:

{kind=link}

Corporate Presentation June 2023

You may be familiar with the pipeline above if you've taken the time to explore Intellia's website or you've already dipped your toes into the gene-editing world. This pipeline is Intellia's lifeblood – It's their past, present, and future. In short, when you invest in a company at this stage, like Intellia, you're investing in this pipeline. It's pretty refreshing to see such a diverse range of projects – It takes off the pressure of reliance on just a couple of programs and keeps us, the investors, on our toes with so much happening.

And here's the thing – when compared to its peers like XNCR, ZYME, ADCT, and more, Intellia's pipeline stands out as more promising. That means plenty of potential triggers for us to watch out for:

{kind=link}

Corporate Presentation June 2023

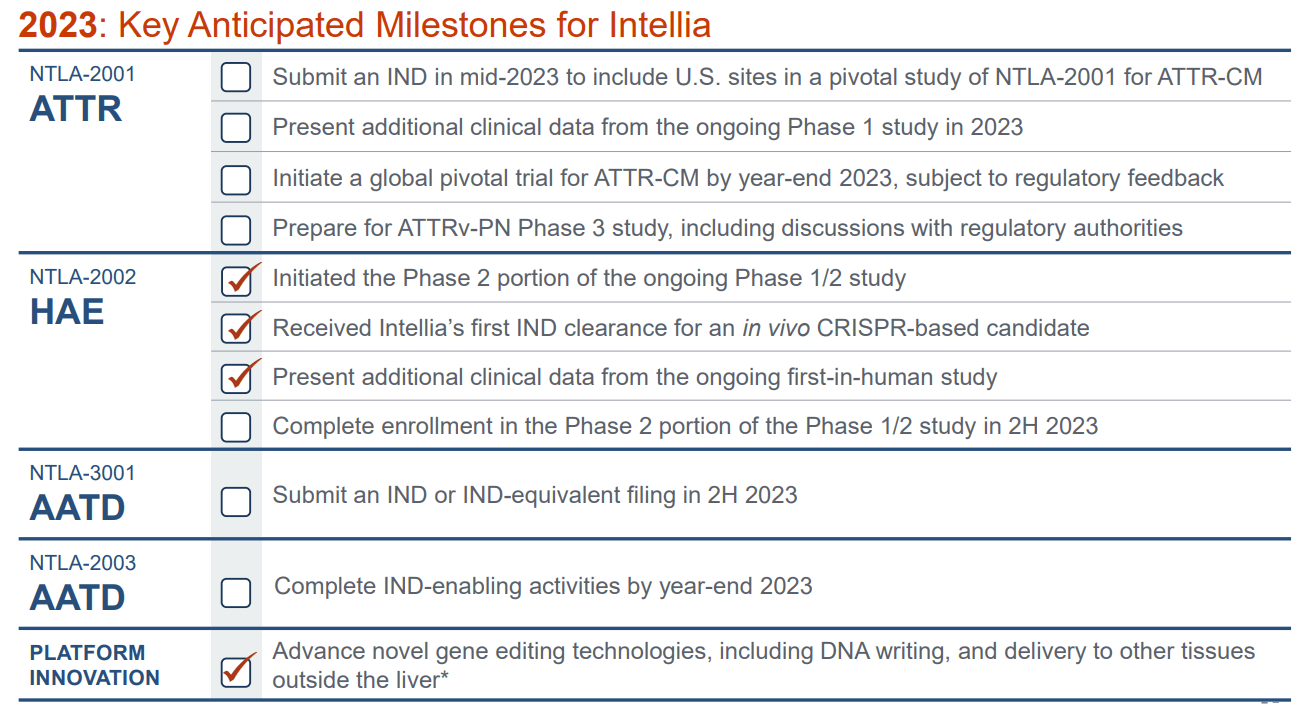

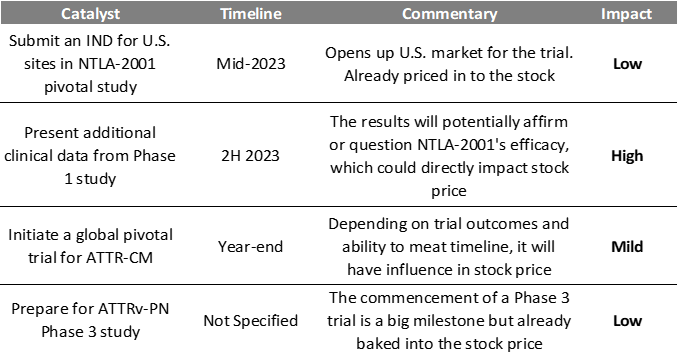

Take a look at this gem from NTLA’s Corporate Deck from June 2023. Juxtapose this with the pipeline we discussed, and you can see exactly what we should be monitoring. For instance, Intellia’s front-runner program, NTLA-2001 (still early stages), has 4 notable events on the horizon for the second half of 2023. Below I will be giving my thoughts on data we already have on these programs and why I am bullish on these upcoming catalysts.

Why Intellia’s Pipeline Is Worth Buying

NTLA-2001: Intellia’s Lead Asset

Transthyretin (ATTR) Amyloidosis – The Target

ATTR Amyloidosis is a disease caused by the buildup of wrongly folded transthyretin (TTR) proteins, mostly affecting the heart and nerves. Imagine your body constantly produces defective parts for a machine. This is the target disease that NTLA-2001 is getting in the ring with.

NTLA-2001

{kind=link}

Corporate Presentation June 2023

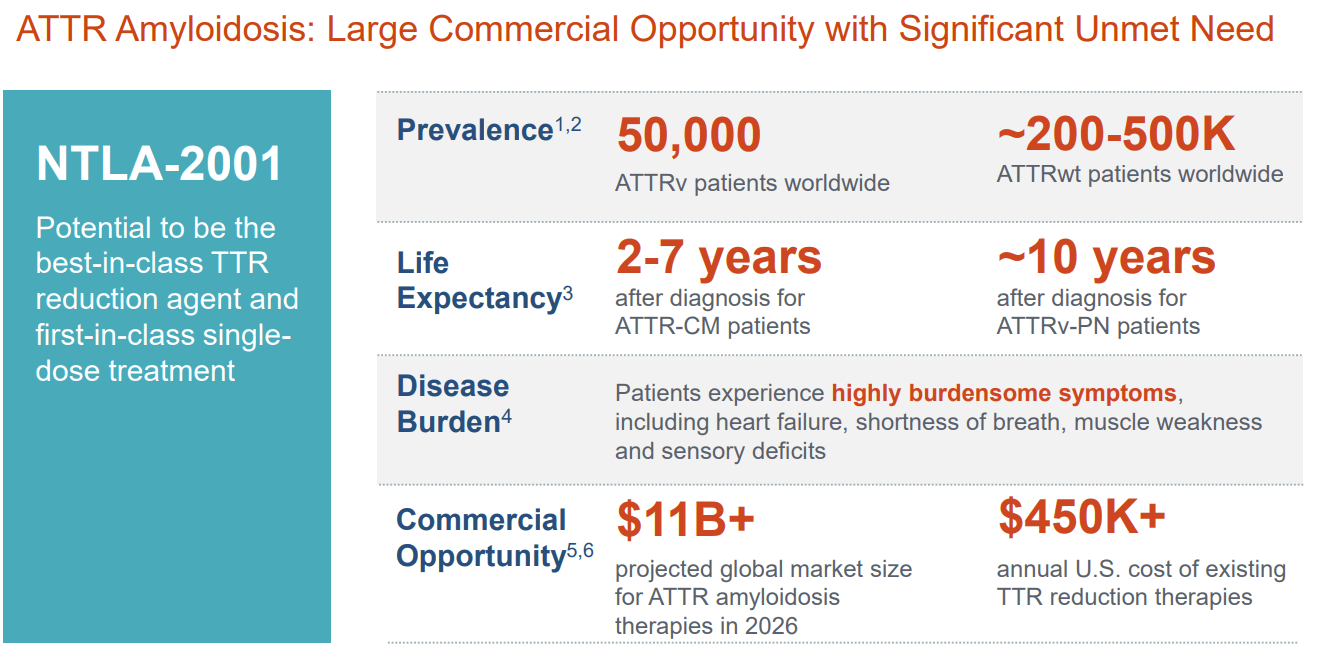

- Objective : NTLA-2001 proposes to halt and reverse disease progression through consistent TTR reduction. It's a single-dose treatment leading to a lifelong reduction of TTR levels.

- Market Potential : This disease represents a sizable opportunity with an estimated global population of 50,000 variant (ATTRv) patients, and potentially 200,000 to 500,000 wild-type ATTR (ATTRwt) patients. With current therapies' costs, NTLA-2001 could tap into a potentially substantial economic opportunity in an expected $11B+ global market for ATTR amyloidosis treatments by 2026.

NTLA-2001 Clinical Trials

{kind=link}

Corporate Presentation June 2023

- Method : NTLA-2001 works through a single-dose (like taking a shot for an instant fix) intravenous infusion. The trials focus on assessing safety, tolerability, and the effect of the drug on the body, primarily measuring serum TTR levels.

- Secondary Objectives : The trial also looks at its impact on patients' neurologic function and cardiac health.

Early Results and Patient Response

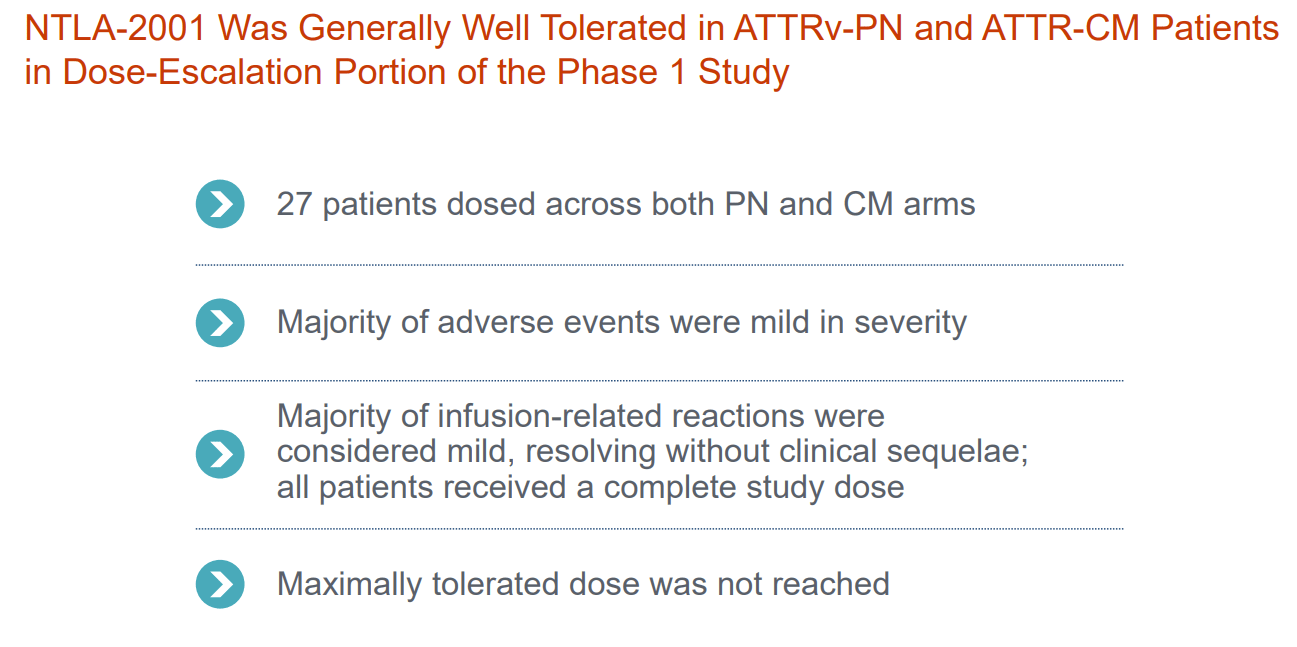

- Tolerance : So far, NTLA-2001 appears well-tolerated. Infusion-related reactions have been mild, similar to standard vaccine shots.

- Efficacy : Initial data implies a dose-responsive, rapid, and significant reduction in serum TTR levels over 6-12 months in ATTRv-PN patients, and 4-6 months in ATTR-CM patients.

NTLA-2001: A Glimpse into the Future

It's still in the early days, but the signs are positive. NTLA-2001 would signify an advancement in understanding and treating ATTR Amyloidosis for the first time. Keep an eye out for upcoming developments in 2023:

{kind=link}

NTLA-2001 Near-term catalysts (Company Reports)

NTLA-2002: A Potential Answer

Hereditary Angioedema ((HAE)) – The Target

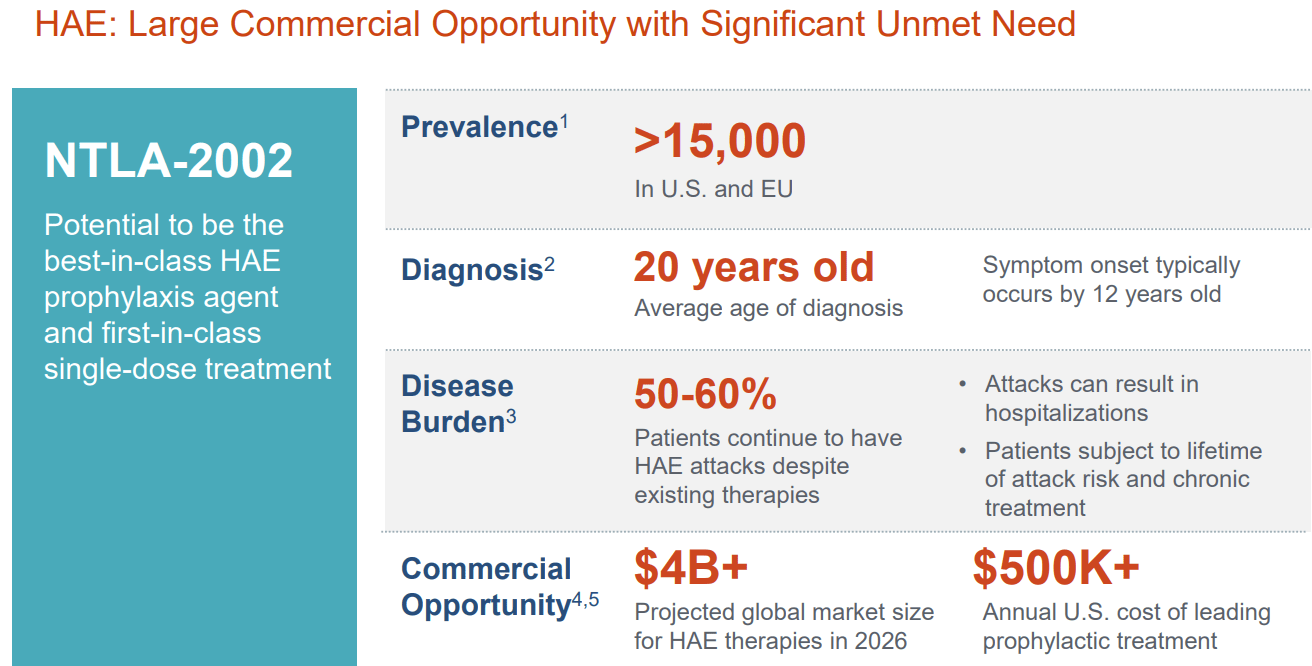

Hereditary Angioedema ((HAE)) is a chronic disease that interrupts your life much like a constant alarm clock that you have to keep snoozing over and over. NTLA-2002 is aiming to be the hammer to this constant alarm clock.

NTLA-2002 at A Glance:

{kind=link}

Corporate Presentation June 2023

- Objective : NTLA-2002 is a phase 1/2 study aimed at reducing kallikrein, a key trigger for HAE's swelling episodes. The goal is to create a consistent dosing regimen that could significantly reduce HAE attacks.

- Market Potential : Even though HAE is a rare disease, affecting about 1 in 10,000 to 1 in 50,000 people globally, the unmet need is significant.

NTLA-2002 Clinical Trials

{kind=link}

NTLA-2002 Interim Clinical Data Update from Ongoing First-in-Human Study

- Method : The trial primarily focuses on the safety, tolerability, and efficacy of NTLA-2002.

- Secondary Objectives : The trial also evaluates how effectively the drug can reduce HAE attack frequency.

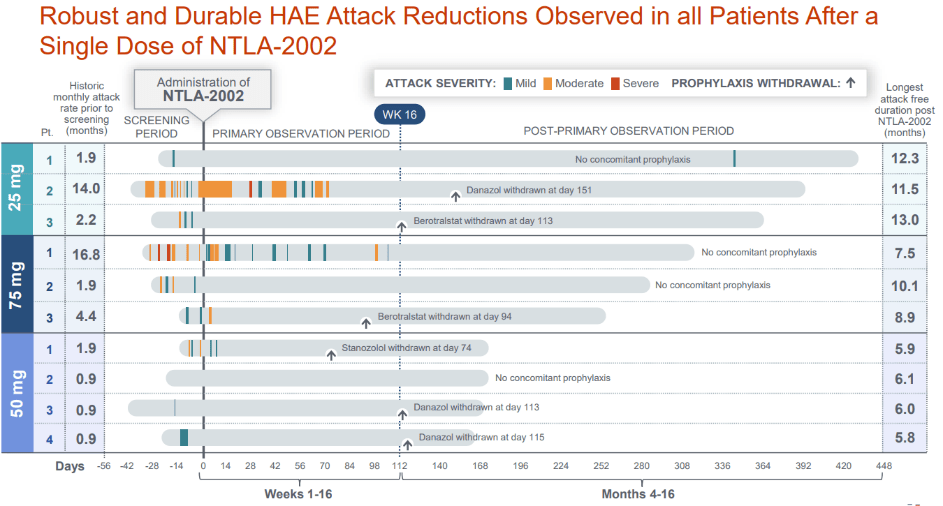

Patient Response and Early Results

- Tolerance : So far, patients seem to respond well to NTLA-2002, with no significant safety concerns raised.

- Efficacy : Even patients with a high history of attacks have remained attack-free during the trial period.

NTLA-2002: Looking Forward

The early results for NTLA-2002 are promising, and it has the potential to make HAE treatment much more manageable. I will be keeping an eye on the phase 2 trial, which is expected to finish enrollment later this year. If the data holds up, this would be a critical advancement in treating HAE and a substantial win for the gene-editing platform.

NTLA-3001 & ‘2003: Intellia’s Hidden Gems

{kind=link}

Corporate Presentation June 2023

Alpha-1 Antitrypsin Deficiency (AATD) – The Disease

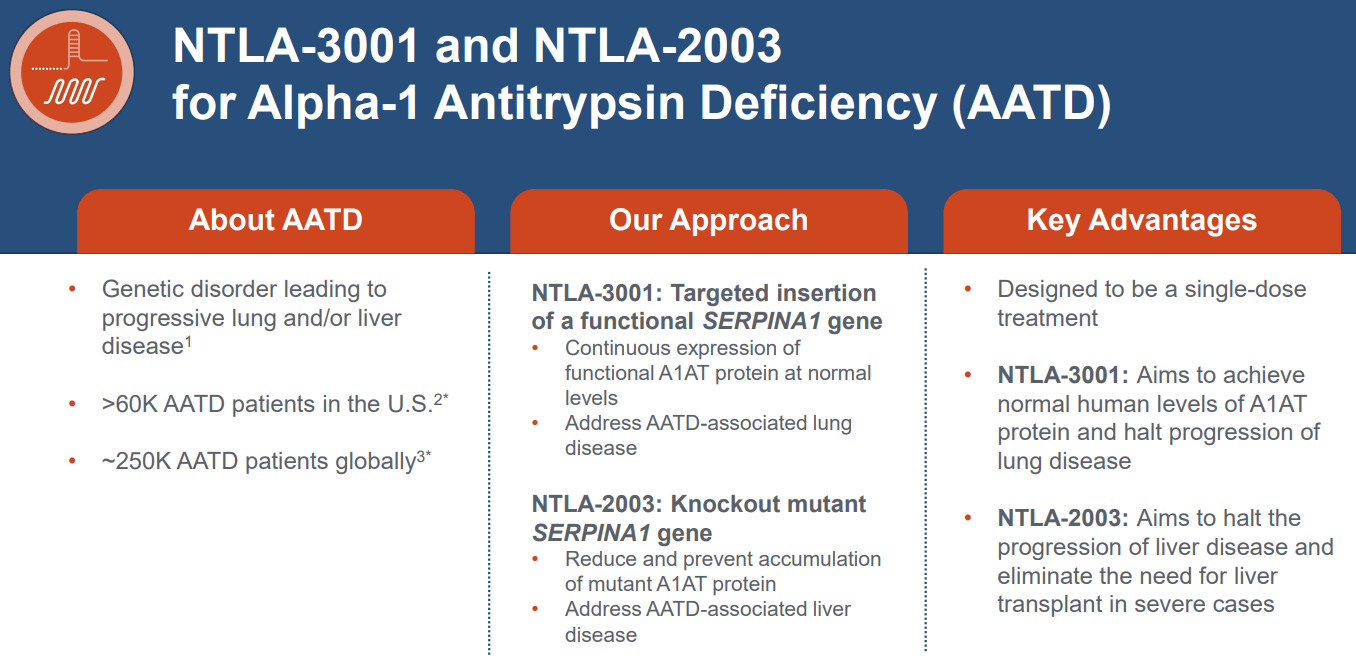

AATD is a genetic disorder. It's like having a misprinted recipe for a vital body protein, leading to progressive lung and/or liver diseases. Both ‘3001 and ‘2003 are getting in the ring with this disease.

The Treatments: NTLA-3001 and NTLA-2003

- NTLA-3001 : This is like getting a corrected version of the recipe, enabling the body to make the right protein. It aims to insert a functional SERPINA1 gene, leading to the continuous production of functional A1AT protein at normal levels. It addresses AATD-associated lung disease.

- NTLA-2003 : This is like erasing the misprinted part of the recipe so it no longer causes problems. It aims to knock out the mutant SERPINA1 gene, reducing and preventing the accumulation of abnormal A1AT protein. It addresses AATD-associated liver disease.

The Impact

Over 60K AATD patients in the U.S. and 250K globally would benefit. Both are designed to be single-dose treatments, offering a potentially transformative, one-time solution.

The Trials

- NTLA-3001 First In-Human Trial : The goal is to see AAT levels similar to heterozygous patients, who preserve most lung function over their lifespan. The trial will closely monitor lung density and pulmonary functions and will avoid patients who also have liver disease.

- Key Data : Achieving plasma AAT levels above the "protective threshold" of 11?M would be clinically significant.

- Treatment Method : Both LNP (lipid nanoparticle) and AAV (Adeno-Associated Virus) components will be administered separately via an intravenous route.

Why NTLA-3001 and NTLA-2003 Matter

- High Unmet Needs : AATD currently has no effective treatment addressing the root cause of the disease. Both these programs could halt or even reverse disease progression.

- Clear Path to Success : AAT augmentation data suggest slowing disease progression, indicating a clear bar for early clinical trial success.

- Single Dose Advantage : The possibility of a one-time treatment would be crucial for patients, freeing them from the chronic, frequent dosing currently required.

Remaining Bonuses for Investing In NTLA

Gene-editing toolbox – NTLA has proprietary editing tools, such as CRISPR/Cas9, base editors, and DNA writers, for both in vivo (in the body) and ex vivo (external) applications. This platform allows for either knockouts, insertions, corrections, or deletions (4 approaches to editing genes in one platform).

Persistence of In Vivo Edits – the co. has shown that edits in the genes can persist through regular cell turnover for up to a year, even in the context of tissue regeneration following partial hepatectomy (a model used to accelerate the process of dividing cells)

In vivo editing of HSCs (hematopoietic stem cells) – the co. aims to improve the limitations of ex vivo SCD (sickle cell disease) by developing an in vivo approach. Even though other firms are already way ahead in SCD, such as CRSP and BLUE, Intellia’s approach is differentiated through multi-dosing and preserves the regenerative potential of edited cells.

LNP-Based Editing of T Cells – Intellia has made a gene editing method that uses LNPs to deliver the editing machinery to T cells. This method has pros over traditional methods, including better cell health and function, reduced DNA damage, and the possibility of sequential editing. The cons are that it costs more and it's extremely difficult.

Allogenic Solution – this is NTLA’s method of modifying T cells to make them less likely to be rejected by the host immune system when transplanted. This includes knocking out certain genes that have to do with immune recognition and inserting genes that inhibit natural killer cell activity.

Track Record – as shown from previous clinical trials for ‘2001, ‘2002, ‘2003, and ‘3001, Intellia has provided validation that their approach to curing these deadly diseases is possible through their gene-editing platform. This is crucial for any new programs they add to their pipeline as it adds investor confidence and enriches its valuation.

Collaborations – Intellia is partnered with many exceptional corporations. For In Vivo Partnerships, NTLA is collaborating with Regeneron ( REGN ) for genetic diseases and with Sparing Vision for Ophthalmology. For Ex Vivo, NTLA collaborates with AvenCell for IO (immune-oncology), with ONK Therapeutics for NK Cells, with Kyverna for CD19 (Autoimmune Disease), and with the most notable one: Novartis ( NVS ) for HSC and Car-T. All of these partnerships differentiate NTLA from its competition, and they do enhance shareholder value since it gives NTLA access to external expertise, accelerate development, and expand the pipeline with fewer investments in R&D than just Intellia.

Intellia – Financial Outlook

Cash Runway Model

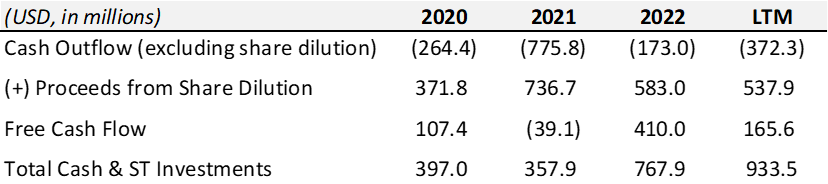

Intellia is an early-stage pipeline company, which means they are unprofitable until they can sell the drugs they are developing. I use the consensus estimates to see when analysts expect this change to occur for NTLA. Now, I do want to mention that even though NTLA has a strong cash balance of $933.5M as of Q1 2023, this isn’t from raising capital or making money from their operations; this cash balance has been solely accumulated from diluting shareholders. For context, this has been NTLA’s cash flow statement in the past 3 years:

{kind=link}

Author's Data

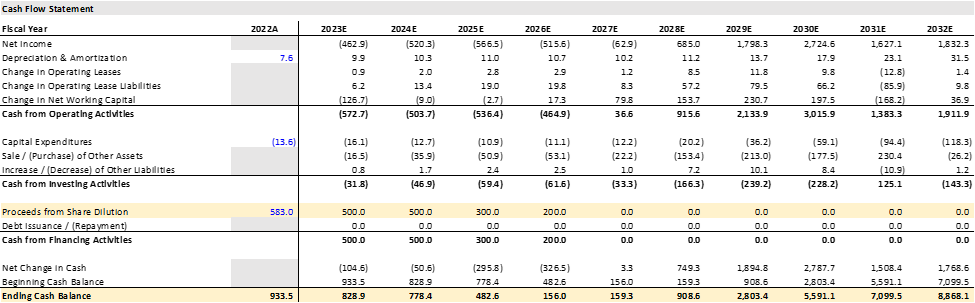

The only reason the company has a positive and sizeable cash balance is from diluting shareholders. This is normal for early-stage pipeline companies like NTLA, but this is a radical amount we are talking about here: from 2020-2022 (3 years), the firm has diluted shareholders by $1.69 billion (~46% of its market value as of writing). Now, I point that out because going forward, I want to understand how many more share dilutions should come. So, I forecast NTLA’s cash flow statement using the consensus estimates over 10 years. However, I want to mention that I only know consensus estimates for net income, capex, and D&A – everything else I forecast through the balance sheet as a % of the consensus estimates for SG&A, and then I add on proceeds from share dilution to see how much NTLA would need to sustain their cash balance. See below:

{kind=link}

Cash Flow Statement (Author's Data)

From my projections, NTLA will need ~$1.5 billion more in share dilutions to keep investing in R&D and G&A. If I take out the $500M in share dilutions from 2023 and from 2024, NTLA would have a negative cash balance of over $200M by mid-2024.

Bottom line, NTLA has an attractive cash balance, but at the rate they are spending, this won’t last them long, and even though they have already diluted shares by almost $1.7B in just the past 3 years, they will need to dilute more shares over the coming years by my estimate of $1.5B by FY26 – over 40% of what their equity value is worth today. But again, this is normal for a company like NTLA, and as long as the firm can meet its budget spending goals, it should not be a big concern for investors. For context, even though Intellia has diluted many shares since 2020, the firm is also up nearly 3x the value of what it was at the start of 2020.

Discounted Cash Flows

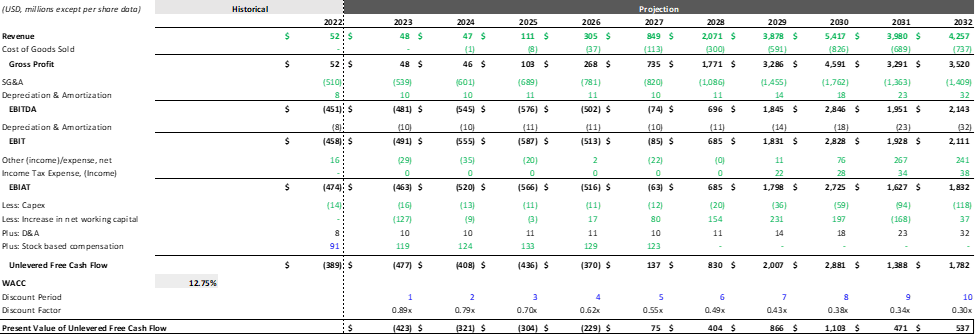

In the following DCF, I arrive at my 12-month, $88.8 price tag for NTLA. In this segment, I will explain how I arrived at this price tag and why I believe it is rather conservative.

Like the cash flow statement, I use the consensus estimates to project out the necessary items for the discounted cash flow analysis. The numbers in green are numbers from a different Excel sheet, and the numbers in black are calculated. With that in mind, I calculated a hefty 12.8% WACC to discount the future cash flows seen below:

{kind=link}

NTLA DCF Analysis (Author's Data)

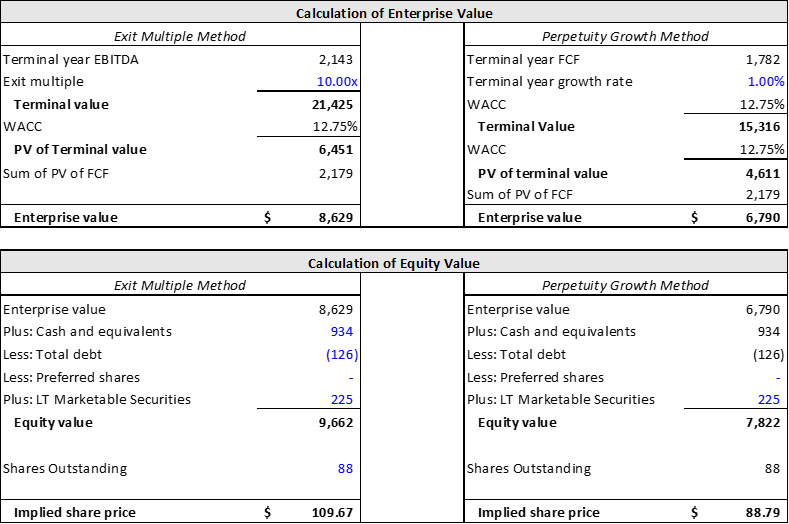

A 12.8% WACC is high (the higher the WACC, the lower the intrinsic value), and typically, when interest rates aren’t at decade highs, a WACC above 10% is unheard of. The high WACC for NTLA is also due to its 5-year BETA of 1.84. However, even with a high WACC, I only apply a 1% terminal growth rate and a 10x EBITDA multiple (conservative) to calculate Intellia’s intrinsic valuation below:

{kind=link}

Calculation of Firm Value (Author's Data)

As shown on the left-hand side of the figure above, my price target would be ~$110 (over a 130% upside) using a 10x EBITDA multiple. However, I don’t like to use the exit multiple methodologies for early-stage companies like NTLA as it is less reflective of their intrinsic value due to the dependence on last year’s EBITDA number. So, I use a 1% terminal growth rate to reflect the world’s growing population (NTLA’s drugs will be needed in perpetuity), and I calculate an implied equity value of $7.8 billion, or a $88.8 share price. In my view, this is a conservative valuation, given that I am using consensus estimates (both the bear and the bull) and using a much higher-than-average WACC. Thus, I believe NTLA is trading at over a 100% discount to its real (intrinsic) value of $88.8 a share and will make that my 12-month price tag as NTLA continues to progress on its pipeline.

Concerns to Rating and Price Target

Investing in a company like NTLA is undoubtedly one of the riskiest investments. Your investment could drop over 50% overnight due to a clinical failure. We have seen this time and time again just this year. For example, Mersana ( MRSN ) dropped over 60% pre-market this year on reporting a clinical failure, and just last week, Vir Biotechnology ( VIR ) dropped ~50% pre-market for the same reason. With that in mind, here are my 5 concerns (ranked) for Intellia going forward:

- Failure related to clinical development – for example, if NTLA-2001 undergoes a clinical trial and then reports there were bleeding events or something unsafe or with a lack of efficacy, their share price will plummet. Conversely, if it is successful, the share price will skyrocket.

- The FDA is strict – the FDA (in the US) or the EMA (in the EU) is responsible for approving any new drug. Even if a drug passes all of its clinical trials, there is no guarantee it will be approved and if the FDA or EMA needs more data, delay approval, or reject applications altogether, this will lead to a big drop in NTLA’s value. However, if the FDA approves one of NTLA’s drugs, their shares will rally.

- Executing current plans – problems could happen with manufacturing a drug, or issues with recruiting and retaining personnel, managing budget expenses, or having slower than expected progress will damage NTLA’s share price over time. Conversely, if we get better-than-expected or faster-than-expected executions, investors will be rewarded.

- Commercial risks – say the FDA approves a drug, if the company does not meet the consensus estimates for what analysts expect a certain drug to make in revenue, the share price will drop. Conversely, if the approved drug does better than expected, shares will rise.

- Financing risk – now, I have already given my two cents on NTLA diluting shares over the next few years. However, this risk applies to having greater than expected share dilution. For example, if NTLA dilutes shares by $1 billion in the next 12 months, that will negatively impact the share price. That said, NTLA diluting shares by ~$500M in the next 12 months is already priced into the stock price, and I am not concerned about this.

Final Thoughts

The intention of this piece was twofold: (1) to explain my rationale behind investing in NTLA and to provide sufficient information for potential investors to make an informed decision. With established giants like Alphabet, Coca Cola, or Apple, the risk of seeing your share price tumble by over 70% virtually overnight is minimal, while you still enjoy long-term upside potential. In contrast, NTLA does come with substantial risks, but these can potentially translate into sizable short and long term returns. The investment rationale for NTLA isn't overly complex: if you believe in their ability to use gene editing to cure diseases more than you doubt it, and are prepared to wager on this belief, then that forms your investment thesis.

From my perspective, I'm convinced that NTLA has already provided adequate proof of its capability to achieve this. They have a variety of programs and events on the horizon that promise to keep investors engaged. What makes NTLA a superior investment compared to its competitors, in my opinion, is the firm's strong partnerships and its current price, which I believe is significantly lower than its intrinsic value of $88.8 per share. Despite my enthusiasm, I can't fully endorse NTLA as a 'strong buy' due to the considerable share dilutions ahead, the roughly three-year revenue drought, and the significant investment risks. As a result, I am assigning an $89 price tag to this trailblazer in gene-editing and advise investors to consider a long-term 'buy and hold' approach with NTLA.

For further details see:

Intellia Therapeutics: The Future Is Here