QRTEA - Intelligently Speculating On Qurate Retail

2023-05-01 00:07:44 ET

Summary

- If Qurate Retail can return to earning a fraction of normalized EBITDA, the upside to equity holders could be significant.

- As preferred shares and much of QRTEA's termed-out debt are trading for pennies on the dollar, significant positive changes in capital structure are possible.

- As the company appears to have minimal risk of bankruptcy in the near term QRTEA seems like a good addition to a diversified portfolio of "intelligent speculation" type stocks.

- I also believe the market is completely disregarding the recent rollout of the "Sune" app and does not recognize the potential for growth in live-streaming e-commerce.

Executive Thesis

There has been a lot of speculation around Qurate Retail Inc. ( QRTEA ), and rightly so as outcomes appear to be binary for equity holders with high debt combined with industry headwinds putting bankruptcy on the table over the next few years. There has been a good amount of quantitative analysis articles from intelligent SA authors, so I will not again dive deeply into near term bankruptcy risk or levers that have already been pulled to prevent it and I will assume readers are familiar with the company. I do agree with the assessment that the company likely has ample liquidity to survive at least through 2024 given their debt maturation schedule, though additionally faces the risk of tripping covenants on its revolving credit facility if operating income cannot be restored quickly.

That being said, as there appears to be low risk of bankruptcy in the near term, the company has a strong history of free cash flow generation, and higher interest rates give the company the opportunity to make significant positive changes to its capital structure, I believe QRTEA shares offer an intriguing risk/reward payoff. I also believe that the market is completely disregarding an area of high margin potential growth with the recent rollout of the Sune smart phone application .

Why is This "Intelligent Speculation"

In Security Analysis Graham and Dodd describe a method of "intelligent speculation" involving purchasing shares in multiple highly leveraged companies with a good chance of survival during periods of economic stress. These types of stocks tend to overcorrect, both to the downside and the upside, for intuitive reasons. When times are tough, interest expenses have a more pronounced effect on earnings and therefore the stock gets bid down further compared to its conservatively leveraged peers.

This same effect, is of course reversed to the upside if and when earnings recover. Interestingly, Graham and Dodd also recommend purchasing shares in these types of companies that are selling at a lower dollar amount, such as a $4 stock instead of a $400 stock. This is because there is a psychological effect of this lower share price, and a $4 stock is theoretically more likely to double or triple than one that costs $400.

I would guess this psychological effect could be even more pronounced when we start getting into stocks like QRTEA which have fallen from grace to prices even below $1 a share. In addition to this, many institutions are barred from investing in penny stocks, and therefore selling pressure is likely amplified even more. The company has also recently fallen from a multibillion dollar market cap to around $300 million, which could also reduce interest. Any recovery will likely be amplified, as these conditions could all reverse together.

Sune Rollout Has Been Completely Ignored

The recent rollout of the company's mobile live stream video shopping app, Sune , deserves an honorable mention despite the news being largely ignored by the market. Bears have regularly criticized QRTEA for its narrow customer focus and decreasing customer base, and expanding into app format with a focus on a younger audience deserves praise. Importantly, the app clearly states for most products that orders will be fulfilled by the brand, so the Sune rollout will likely not add to inventory issues. If the app can scale, sales will likely be high margin.

My wife and I are in our late 20s and we have received gifts of multiple products that I found advertised on the platform, including Opopop popcorn and Poppy and Pout lip balm . These kinds of products are generally not things we would buy for ourselves, but are nice as gifts. I believe this type of product is a good focus for the app. When people are stumped for ideas on what gift to give, they can easily turn to Sune for entertaining sales pitches on premium products. There are also a few smaller business founders pitching their products, telling their stories and using the platform as a new way to promote their brands. Having a reputation for these types of products will add to the exciting and unique "discovery" aspect of the app.

In addition to these types of finds, video e-commerce has the benefit of the hosts trying on products or demonstrating how they work. People may find hosts that have similar styles or body shapes to them, and could more easily be able to order products with the right fit. App store comments need to be taken with a grain of salt, but one happy user of Sune described the app experience as follows:

Most of this stuff I would just scroll by on the normal e-commerce websites, but once I see demonstrations or try-ons it totally changes things for me. I can't stop purchasing!!!

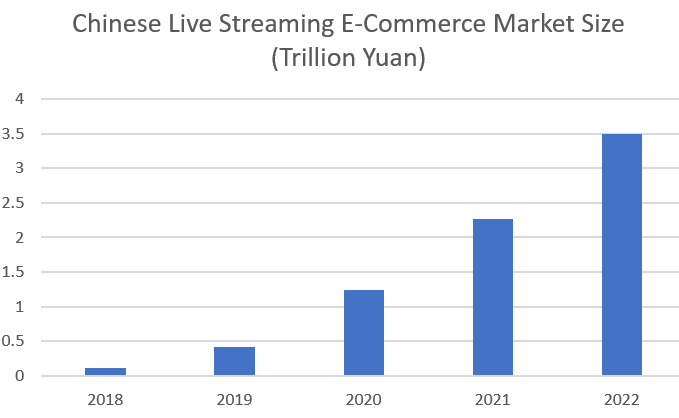

Though there is much competition in the field, the total addressable market could be immense and is likely to grow further. In China, live streaming e-commerce growth over the last few years was as follows :

{kind=link}

For reference, 3.5 trillion yuan is approximately $500 billion USD, and at least in China this market is showing no sign of slowing down. In the US, this is a relatively new field with early signs of rapid growth, and QRTEA could be a natural leader in the space with its already established video commerce abilities and techniques.

Options on Termed out Debt

Much of the company's termed out debt as well as the preferred shares are trading for pennies on the dollar, due to higher interest rates and lowering of the company's credit rating. This may give the company bargaining power with refinancing, or allow retiring of debt at a significant discount. Of course, this can only happen if the company can generate free cash flow. If the company is limited with cash generation and can only pay off debt as it matures, of course this will not provide much of a discount at all. To give you an idea, here's a list of some of the company's near term bonds and most recent selling prices:

{kind=link}

Of course managing nearer term maturities and avoiding default is paramount. But if the company does ever have excess cash, it can also scan the capital structure and try to figure out what would give them the highest rate of return. Interestingly, one of the highest returns right now would be retiring preferred shares, QRTEP, as they have an 8% coupon and are trading for 30 cents on the dollar. An odd choice I know, as missing preferred coupon payments do not generally result in bankruptcy. At these prices, one dollar spent on QRTEP would equal over 25 cents of coupon payment savings per year, not to mention the reductions in future maturation liabilities in 2031.

Just to illustrate what a good deal this is for the company (I know it's likely not possible), if QRTEA could theoretically buyback all the preferred now at 30 cents on the dollar, this would cost $380 million, save the company around $100 million a year in coupon payments, and prevent a $1.26 billion payment in 2031. Quite a nice return on investment.

Risks

Recent Increase in Short Interest

Many bulls have pointed to QRTEA having relatively low short interest, though I've noticed there has been a recent increase, with 9% of the float shorted compared to 6% a month ago. Something to watch could be the end of April short interest report, which is scheduled to be released on May 2nd. Of note, this is prior to upcoming earnings on May 5th.

Macroeconomic Factors

I have covered a few other discretionary retailers including Big Lots ( BIG ), and the story has been pretty much the same. 2022 was a terrible year with consumers weakened, and the companies are hopeful things will be looking up soon. It is uncertain if discretionary spending will recover in the near future, and it's likely that with rampant inflation, staples are taking up a larger proportion of consumer's incomes. This leaves less money to spend on premium products from QRTEA of course, and if this is a longer term issue bankruptcy likelihood becomes much higher.

Competition

Streaming e-commerce has many competitors including most of the big tech companies. These companies have deep pockets and often don't mind expanding horizontally, even if that means operating at a loss. This will likely put pressure on margins, though this could be offset if the market grows rapidly.

Debt Maturity Schedule

As I mentioned, if free cash flow generation is limited the company will not be able to realize cost savings on their debt, as the closer to maturity the bonds are the closer to par value they will likely trade at. There is of course a chance of bankruptcy in the next few years if capital is not managed well or if headwinds persist.

Conclusion

Ultimately, I consider QRTEA to be a good candidate for a position in a diversified portfolio of Graham and Dodd's "intelligent speculation" type stocks. The market is extremely pessimistic on the company now, and maybe rightly so as the high debt combined with lack of profitability is alarming. That being said, there appears to be ample liquidity to survive headwinds for the next 1-2 years. If free cash flow generation can return when economic conditions improve, QRTEA will likely have options to retire debt, or buyback preferred shares at a significant discount if interest rates remain elevated.

I also believe the market has completely disregarded the potential growth in live-streaming e-commerce markets, and with the rollout of Sune , QRTEA could be a leader in this field and expand to a younger customer base. If QRTEA can return to earning $1.5 billion in EBITDA which is less than 75% of normal operational years, a conservative EV/EBITDA multiple of 6 would indicate an EV of $9 billion with over $1 billion of upside attributable to equity holders at current market prices. Investors may want to wait until earnings are released later this week before deciding on taking a position, though I do already own shares.

For further details see:

Intelligently Speculating On Qurate Retail