IPAR - Inter Parfums: Fragrant But Fragile Prospects

2023-07-13 13:39:44 ET

Summary

- Inter Parfums reported strong Q1 2023 results, driven by growth in North America, its largest market.

- Near term prospects are cautiously optimistic thanks to tailwinds from China's reopening.

- U.S. fragrance boom however is at risk of fizzling out and any material decline may not be sufficiently offset by strength in Asia.

Fragrance company Inter Parfums ( IPAR ) delivered a strong start to Q1 2023 and prospects are cautiously positive.

Tailwinds from China opening

Inter Parfums reported a 24% YoY increase in revenues for the March 2023 quarter, the highest quarterly growth in the company’s history , driven by a booming perfume market in major markets like the U.S.; Q1 2023 growth was driven by North America, Inter Parfums’ biggest market, which reported quarterly revenue growth of 36% YoY. Western Europe

Inter Parfums 10-Q, Q1 2023

Near term, prospects are cautiously optimistic. Inter Parfums launched a slew of new scents this year which may support consumer interest and demand for fragrances. However, although inflation is cooling in the U.S., it still remains above the Fed’s 2% target so consumer spending power is likely to remain constrained near term and cracks are already beginning to surface. Prestige fragrance demand growth in the U.S has largely been driven by the country’s Gen Z and millennials, the former of which is increasingly racking up credit card debt faster than any other generation and falling behind on debt payments faster than any other generation according to a report from personal finance company Credit Karma.

Moreover, more than 60% of Inter Parfums’ revenues are generated from “affordable luxury” brands, namely Montblanc (20% of revenues), Jimmy Choo (20%), Coach (15% of revenues), and GUESS (9%) of revenues. Unlike ultra luxury brands, consumers of affordable luxury brands are more vulnerable to economic slowdowns which could materially impact revenues in Inter Parfums’ biggest market. Americans with a $100,000 income (which fall under Coach owner Tapestry’s target market ), are already under pressure with 51% of them reportedly living paycheck to paycheck, a 9% increase compared to one year earlier according to a survey by LendingClub and Pymnts.com .

Inter Parfums 10-Q, Q1 2023

Considering the above factors, Inter Parfums 35% YoY quarterly growth rate for North American sales is not likely to be sustainable and could slow materially (or even decline assuming a severe recession in the worst case scenario) near term.

China’s ongoing post-pandemic economic reopening as well as continued relaxing of covid restrictions in Japan (restrictions were lifted early this year but residents continue to wear masks and remain generally cautious) may help partially offset weakness, if any, in the U.S (barring a sharper than expected decline in U.S. sales for reasons like a severe recession).

Increasing social mobility in China and Japan, Asia’s top two fragrance markets, could drive fragrance demand, and unlike the U.S., Chinese and Japanese consumers are not weighed down by inflationary pressures (Japan’s core inflation was around 3% in April 2023, and China’s CPI rose just 1% for the first four months of 2023, well below the 5.6% average in the U.S. and 7.7% in the euro area). Currency headwinds from an appreciating dollar however may limit growth on a reported basis.

At $46 million for the March 2023 quarter, sales in Asia increased 10% YoY, its second-slowest growing region. Asia sales growth has lagged other regions, rising just 40% between Q1 2019 and Q1 2023. By contrast, North America sales have more than doubled over the period and as of 2023, North America sales are more than double that of Asia, compared with the same quarter in 2019 when North America was just 1.4 times bigger.

Inter Parfums 10-Q, Q1 2023 and Q1 2019

It may seem as if Asia has considerable runway for recovery but not necessarily so; an appreciating dollar may be partially responsible for Asia’s subdued sales growth (the dollar has roughly appreciated more than 25% against the Japanese yen compared to 2019) and in addition, the West’s fragrance obsession could be a localized trend. Industry reports expect a mid-single-digit growth rate for China’s fragrance market over the coming years. Conservatively assuming Inter Parfums’ Asia sales grow at mid-single digit rates sequentially for each of the coming quarters on the back of a strong recovery in the region, it could meaningfully contribute to top line growth and help offset any slowdown (but not decline) in the U.S.

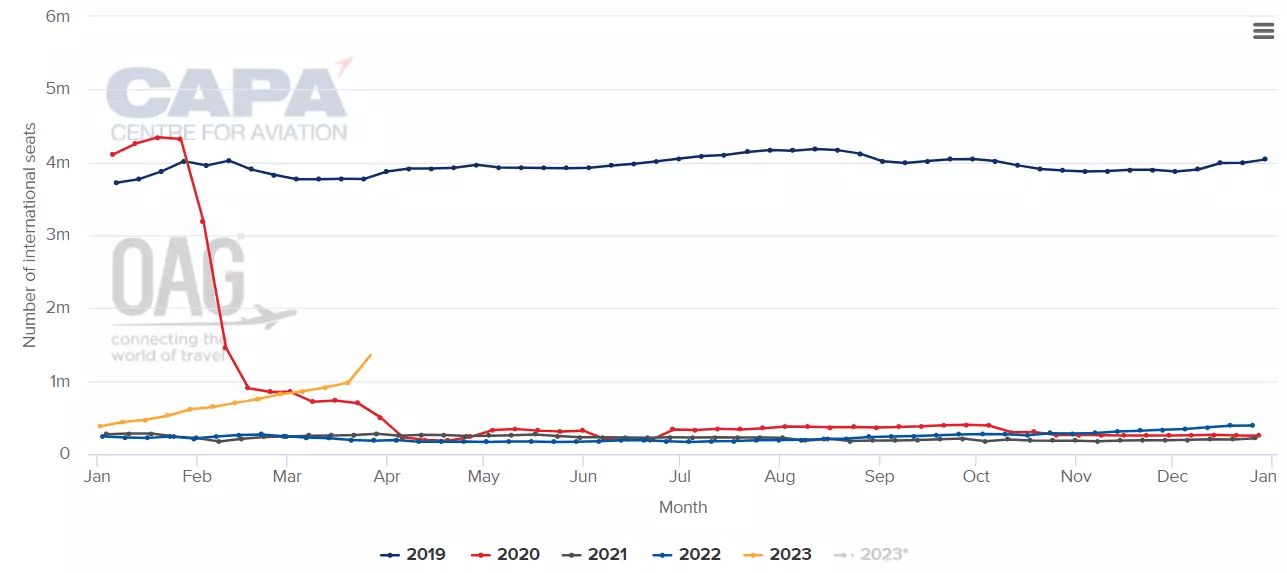

China’s re-opening could boost travel retail sales; China was the most important source market of tourists and tourist spending pre-pandemic and as international travel recovers, sales from this segment could further support near term financial performance. As of May, China’s visa applications are just around 35% of pre-pandemic levels, and international air capacity remains way below pre-pandemic levels. However, at just around 5% of Inter Parfums’ top-line, travel retail comprises a very small proportion of the company’s business so this segment alone may not meaningfully move the needle.

{kind=link}

Longer term, prospects are also cautiously optimistic; it remains to be seen if America’s fragrance boom would last but the prestige perfumes market has significant growth potential elsewhere particularly in emerging markets like China where fragrance usage remains comparatively low. Per capita fragrance spend in China for instance is around $1.5 , versus $4 for Japan, and $12 for South Korea. Additionally, the company is looking at opportunities in the travel retail segment worldwide with ambitions to increase travel retail’s share of sales to 7%-8%.

Improving margins an earnings positive, profitability better than rivals

Alongside moderating inflation, Inter Parfums’ gross margins have continued to trend upwards rising from 55.33% in the May 2021 quarter to 57% in the latest quarter. There is still further room for margin expansion (Q1 2023 gross margin of 57% is 400 basis points lower than the 61% margin recorded in Q1 2019). Given the company’s brands’ pricing power, and continued supply chain adjustments, pricing actions may catch up to costs, and therefore margin and earnings prospects are generally positive assuming inflation remains under control.

Inter Parfums has considerably better financials than rivals.

| FY ended December 2022 |

| Symrise (SYIEF) |

| Gross margin % |

| 55.9% |

| 38.8% |

| 33.4% |

| 36.8% |

| Return on assets % |

| 11.4% |

| 6% |

| 1.5% |

| 5.4% |

| Debt to equity |

| 26 |

| 118 |

| 66.9 |

| 70.56 |

Risks

Competitive risks may hinder performance particularly in attractive markets like China . Not only could increased competition potentially result in market share losses in what is already a highly fragmented industry with low barriers to entry, it could potentially cut into profitability if it results in lower marketing ROI. Unlike rivals like Givaudan which has an industrial fragrance business, Inter Parfums focuses exclusively on the consumer side of the fragrance market (in fact Inter Parfums is a customer of Givaudan (GVDBF) and IFF (IFF)) and so may be more vulnerable to the entry of new players. In addition, Inter Parfums focuses exclusively on prestige fragrances, and that too focused on ‘evergreen’ brands’, and so the entry of new brands outside their focus (like celebrity fragrance brands for instance) may further impact Inter Parfums’ market share and performance.

A further risk is that of brands taking their business in-house, to capture more of the businesses' economics. Beauty powerhouses like LVMH and L’Oreal already manage a broad portfolio of their own and third party fragrance brands, and more fragrance brand owners may opt to follow a similar strategy impacting demand for services from third-party contractors like Inter Parfums. Estee Lauder’s purchase of Tom Ford for instance appears to be largely driven by the latter’s fragrance business (fragrance makes up about 50% of Tom Ford’s beauty sales and Estee Lauder has been a long time licensee to Tom Ford’s beauty and fragrance products).

Finally, Inter Parfums is relatively not as diversified as rivals Givaudan which has a flavors business so any slowdown in the fragrance industry could have a disproportionately large impact on Inter Parfums. Whether the current fragrance boom in the U.S. can last is a major question mark and if growth begins to stagnate or even decline over the coming years due to a fizzling out of the fragrance trend, Inter Parfums could be affected.

Conclusion

Inter Parfums has an analyst consensus rating of moderate buy.

WSJ

With a forward P/E of 30, Inter Parfums is trading at a discount to their five year average of 39 which may seem cheap. However, although prospects are generally optimistic at the moment (as China's reopening could partially offset mild weakness in the U.S.), it is fragile because any material decline in the U.S. may not be sufficiently offset by strength in Asia; a buildup of credit card debt and unpaid dues from prestige fragrance's key demographic does not bode well for U.S. prospects. The risk-reward isn't compelling at this point and the stock could be considered a hold.

For further details see:

Inter Parfums: Fragrant But Fragile Prospects