ICPT - Intercept: Huge Potential Upsides With Binary Catalyst Unlocking

Summary

- Due to what is seemingly a successful comeback, you can expect Intercept Pharmaceuticals to potentially deliver several-fold returns.

- Ocaliva's revenue for PBC alone is nearly enough to bank a net profit.

- The FDA recently accepted the New Drug Application of Ocaliva for non-alcoholic steatohepatitis (NASH).

Intercept

I have already made up my mind, don't confuse me with facts. - Philip Fisher

Author's Note : This is an abbreviated version of an article originally published in advance on January 21, inside Integrated BioSci Investing for our members.

Usually, most investors do not want to touch a "turnaround stock." As you can see, a turnaround stock has rightly been beaten up to oblivion. For biotech, these are usually companies that previously received a Complete Response Letter (i.e. CRL) for its lead medicine. As the company successfully makes adjustments for a subsequent FDA trip, approval here can substantially elevate the fundamentals of the stock. As such, the shares would rally aggressively to give you multiple-fold returns.

On that note, Intercept Pharmaceuticals ( ICPT ) shares crashed in the previous year due to a CRL. In making a successful turnaround, Intercept recently sent its lead drug (Ocaliva) to the FDA for accelerated approval for NASH. As you can see, the NASH market is untapped with mega blockbuster potential for early drugs entering this niche. In this research, I'll feature a fundamental analysis of Intercept while focusing on its upcoming regulatory binary event.

{kind=link}

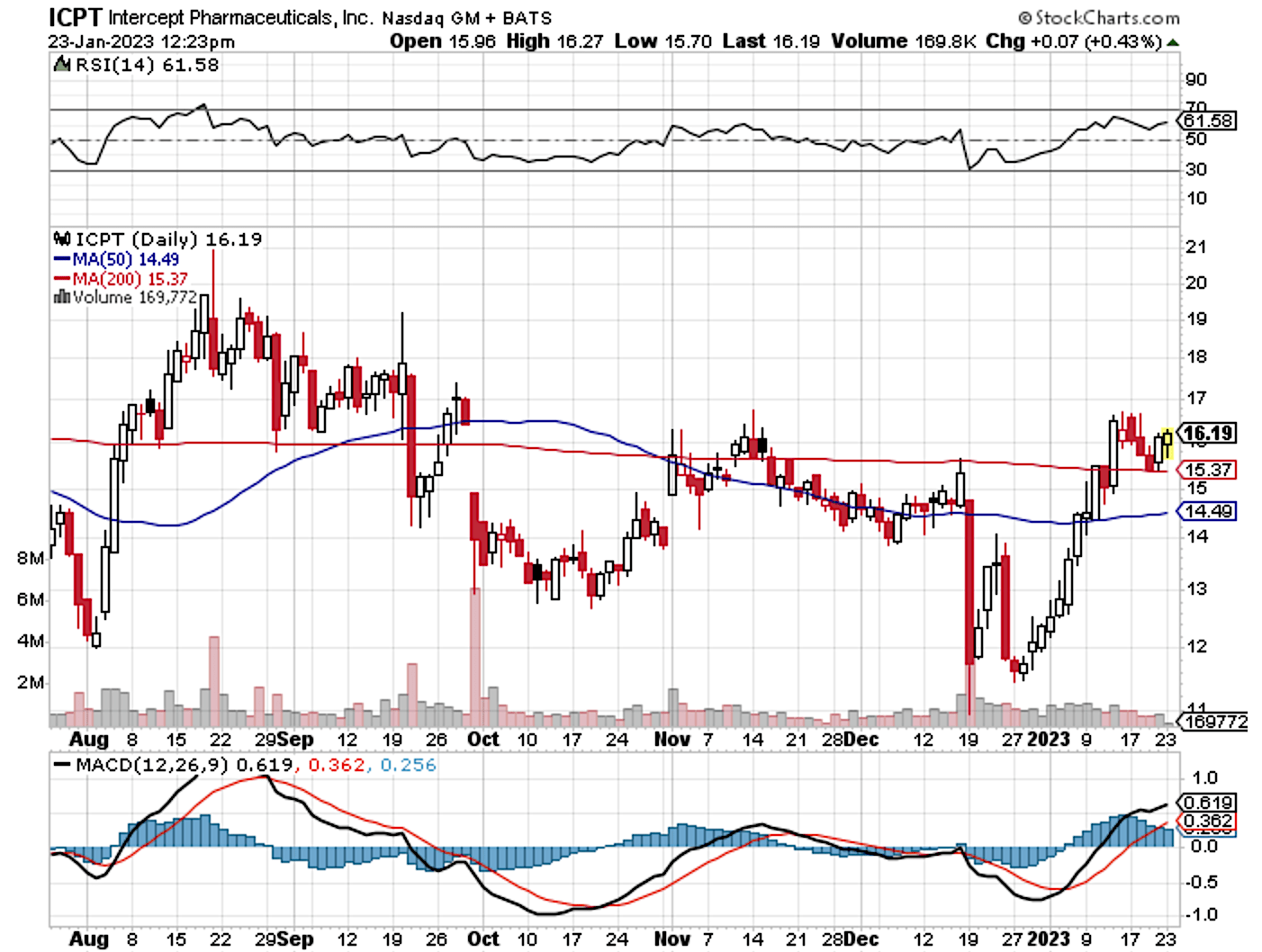

Figure 1: Intercept chart

About The Company

As usual, I'll deliver a brief corporate overview for new investors. If you're familiar with the firm, I suggest that you skip to the subsequent section. I noted in the prior article ,

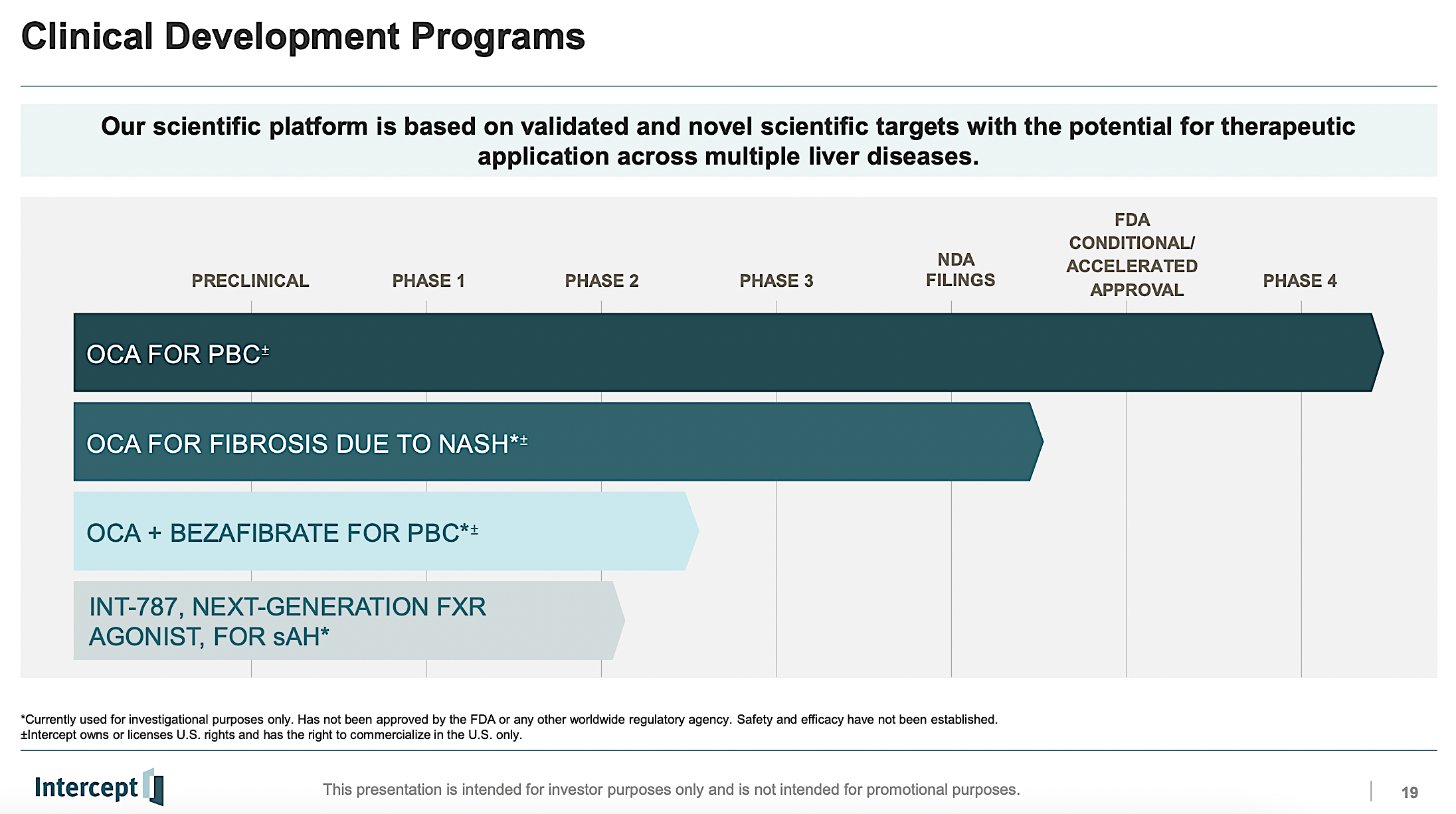

Headquartered in New York City, Intercept is focused on the innovation and commercialization of bile acid medicine. As a semisynthetic bile acid, OCA is designed to manage deadly liver conditions. Marketed under the brand (Ocaliva), OCA is used to treat primary biliary cholangitis (i.e., PBC) in U.S. and Europe. As a second-line drug, Ocaliva is already generating revenue reaching over 1/3 of a blockbuster. That aside, the company is expanding OCA's label for NASH.

{kind=link}

Figure 2: Therapeutics pipeline

Latest Operating Results

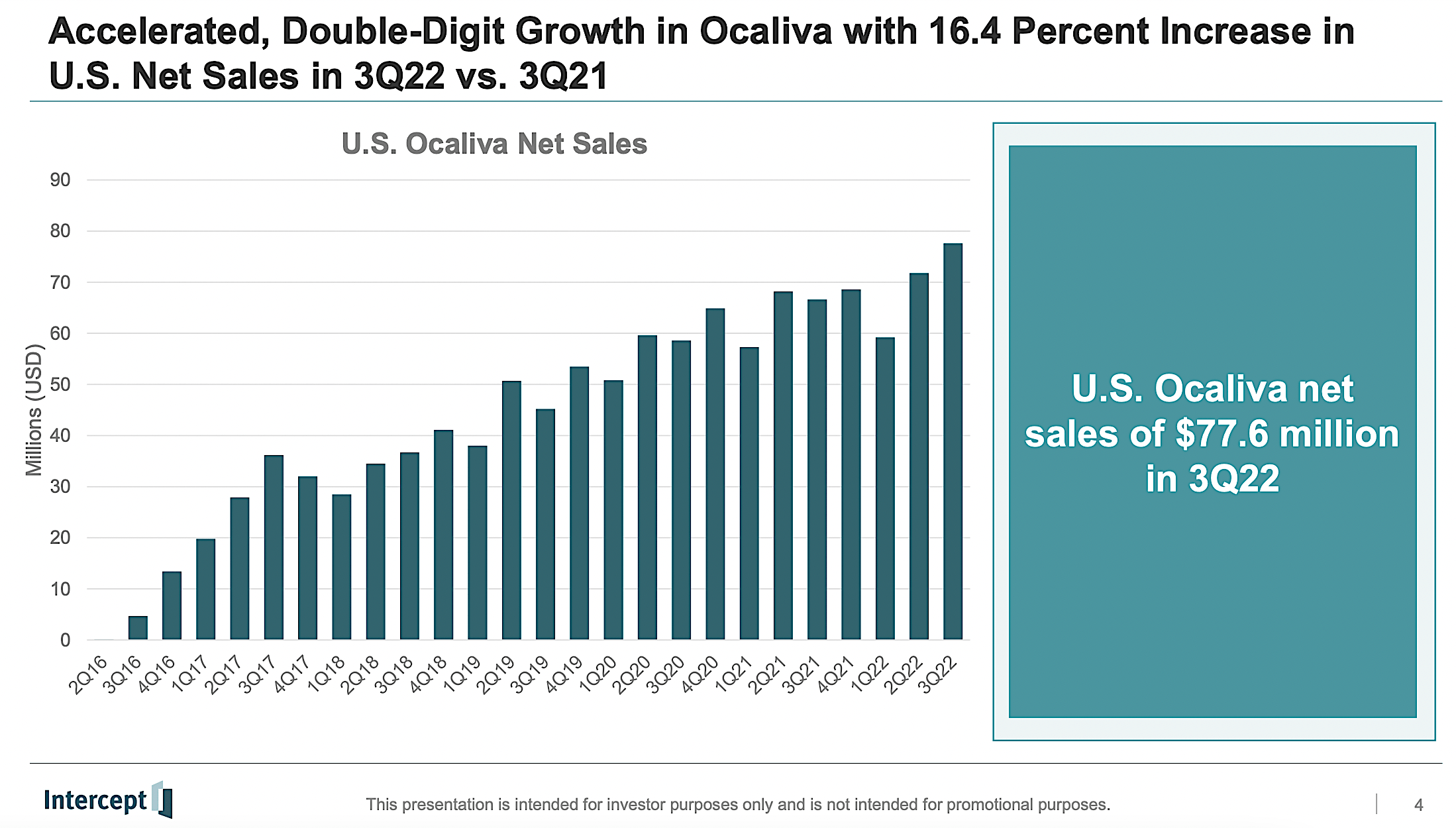

In the latest quarter, Ocaliva enjoyed a 16.4% year-over-year ((YOY)) growth rate. That is to say, revenues grew from $66.6M in 3Q2021 to $77.5M in 3Q2022. Interestingly, IQVIA also showed that prescription volume for Ocaliva was up 37% from last year. Hence, this quarter represents the highest prescription volume since the start of the pandemic.

Riding extremely robust performance, Intercept revised its Fiscal 2022 revenue estimate from $340M to $350. Commenting on the latest operating results, the President and CEO (Jerry Durso) remarked,

We drove accelerated, double-digit growth in Ocaliva this quarter, resulting in an increase to our sales guidance for this year. This quarter’s performance reinforces the underlying strength and value of our PBC business, and there is significant opportunity to grow this franchise given the number of patients who remain eligible for second-line therapy. Importantly, the long-term outcomes data we are generating reinforce the role Ocaliva can play in the future of PBC treatment.

{kind=link}

Figure 3: Latest Ocaliva sales growth

More Turnaround Progress

Asides from the robust revenue, Intercept is executing a prudent strategy to shore up cash. Specifically, the company out-licensed Ocaliva's ex-US rights to Advanz Pharma for $404M. Additionally, Intercept would receive another $45M from Advanz which is contingent on the continuing orphan drug exclusivity from the EMA/MHRA. Should Ocaliva gains approval for NASH, the firm would also receive royalty payments ex-USA.

Now, Intercept also significantly strengthened its balance sheet. That is to say, the company repurchased $388.9M of the 2026 Convertible Secured Notes for $258.2M in cash and $219.4M in equity for a total consideration of $477.6M. The result is a reduction of the principal debt to $111.M. Consequently, the annual interest payment is lowered from $13.6M to $9.8M.

Upcoming Catalysts

On January 19, Intercept disclosed that the FDA accepted its New Drug Application (i.e., NDA) for Ocaliva which is seeking accelerated approval for patients afflicted by pre-cirrhotic NASH. As such, the Agency set the tentative Prescription Drug User Fee Act (i.e., PDUFA) date for as early as June 22 this year.

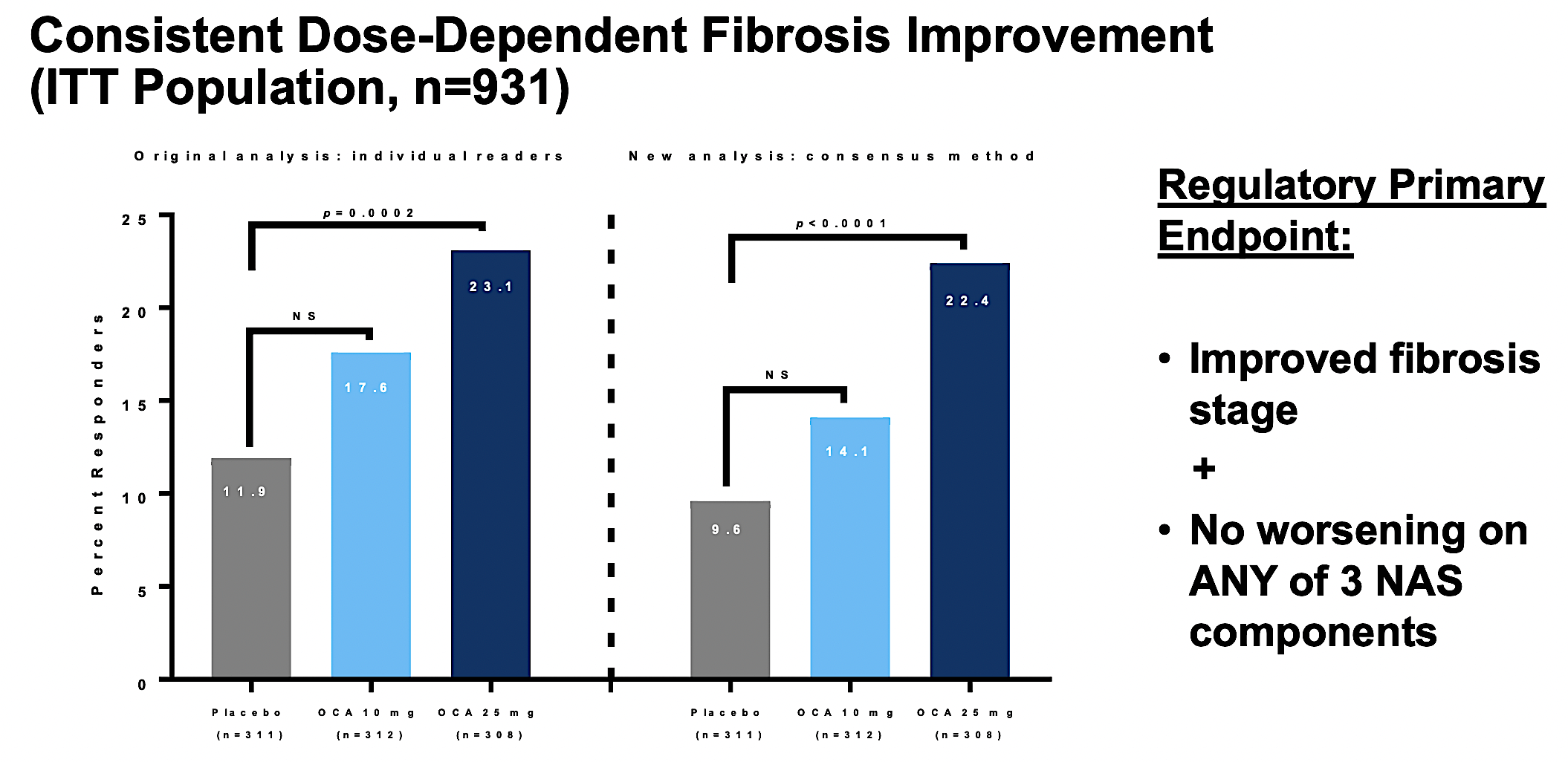

Notably, the application is supported by the two positive Phase 3 (REGENERATE) studies of patients afflicted by pre-cirrhotic liver fibrosis due to NASH. Precisely speaking, patients who took Ocaliva enjoyed double the response rate compared to patients on the sugar pill (i.e., placebo). Except for pruritus (itching), Ocaliva was well tolerated. According to Mr. Durso,

This regulatory milestone brings us one step closer to reaching our goal of delivering the first available therapy for patients living with pre-cirrhotic fibrosis due to NASH – the most rapidly growing cause of liver transplantation in the U.S. We believe OCA has the potential to become an important therapy given its strong and direct antifibrotic effect, and we look forward to continuing our work with FDA over the coming months as they review our NDA.

{kind=link}

Figure 4: Positive REGENERATE data

Estimated NASH Market

To better appreciate the aforesaid development, you should size up the NASH market. As follows, BioSpace valued the global NASH niche at $180B . Other sources like Verified Market Research ascribed $542B in 2020. I noted in the prior article ,

Growing at 29.6% CAGR, this market is expected to reach $4,287B . While the figure seems to be astronomical, you can imagine that NASH is as big as the obesity/diabetes market. After all, those conditions tend to occur together.

{kind=link}

Figure 5: NASH market

Keep in mind, Ocaliva had NOT been able to clear its primary endpoint in Phase 3 (REVERSE) study. If approved, its label would still exclude patients afflicted by compensated cirrhosis. Coupled with the pruritus (i.e. itching) side effect, its prescription might not deliver a mega-blockbuster. Notwithstanding, you can still anticipate Ocaliva to be an excellent drug for earlier-stage NASH. Given that this market is gargantuan, it should allow Ocaliva to garner at least $1B.

Financial Assessment

Just as you would get an annual physical for your well-being, it's important to check the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll assess the 3Q2022 earnings report for the period that ended on September 30.

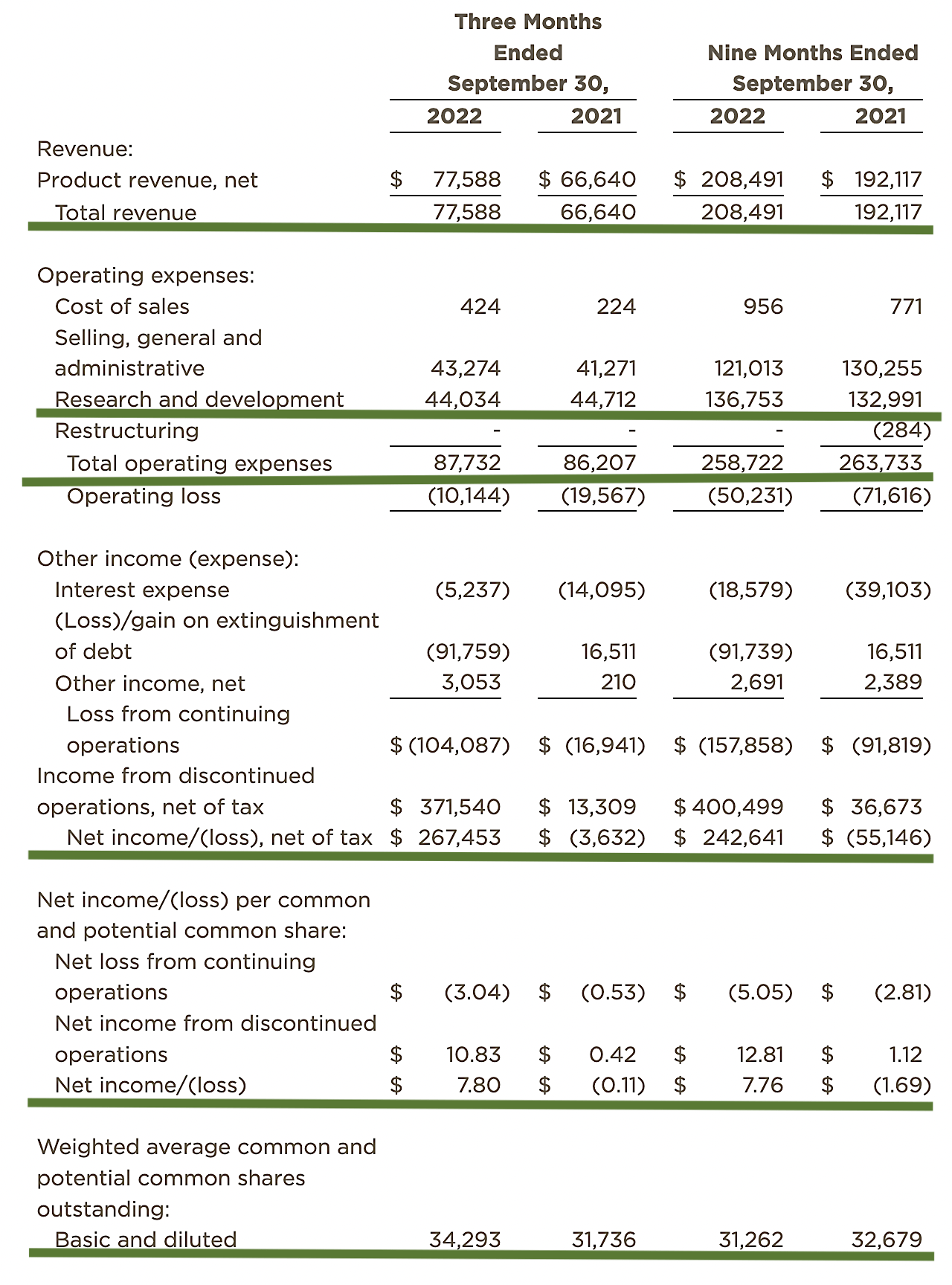

As follows, Intercept procured $77.5M in revenues compared to $66.6M for the same period a year prior for a 16.4% YOY increase. Despite having sold its ex-US rights of OCA, this is a great development because the company still enjoys robust sales growth.

That aside, the research and development (R&D) for the respective periods registered at $44.0M and $44.7M. Essentially, R&D remains flat. I generally view an increasing R&D trend positively because the money invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $267.4M ($7.80 per share) net incomes compared to $3.6M ($0.11 per share) net declines for the same comparison. As you know, the robust bottom line improvement is due to the disposition of Ex-US rights to OCA. Even without that transaction, the revenue is still growing robustly while the OpEx is reducing. At this pace, that should help Intercept to bank a net profit soon.

{kind=link}

Figure 6: Key financial metrics

About the balance sheet, there were $497.8M in cash, equivalents, and investments. On top of the $77.5M quarterly revenue and against the $87.7M quarterly OpEx, you should not be concerned about the cash flow issue. Simply put, the cash position is extremely robust relative to the burn rate.

While on the balance sheet, you should check to see if Intercept is a "serial diluter." After all, a company that is serially diluted will render your investment essentially worthless. Given that the shares outstanding increased from 31.7M to 41.7M, my math reveals a 31.5% annual dilution. At this rate, Intercept "more or less" cleared my 30% cut-off for a profitable investment.

Notably, the 10-Q filing showed a discrepancy in the total common shares. That is to say, the shares outstanding are actually 41.7M rather than 34.2M as shown above. I believe that the higher shares count is due to the equity raised to reduce the Convertible Note debts.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with an investment regardless of its strength. At this point in its growth cycle, the biggest risk for Intercept is whether Ocaliva would gain FDA approval for pre-cirrhotic NASH by July.

Even if approved, sales growth would be modest due to what is likely a narrow label. Launching the drug in-house would also limit the ability to reach many patients. The other concern is that Intercept might not be able to continue to ramp up Ocaliva sales growth for PBC.

Conclusion

In all, Intercept has been adamantly fighting to make a surprising comeback . Specifically, the recent NDA filing is already accepted by the FDA. Though its application for advanced NASH failed, the approval chances for the earlier stages of NASH should be higher. Even without approval, you can bet that Ocaliva's revenue for PBC is increasing significantly enough to allow the company to generate net earnings in the next year or two. Interestingly, Intercept is still trading near its cash position which makes it an extremely enticing bet.

For further details see:

Intercept: Huge Potential Upsides With Binary Catalyst Unlocking