ICPT - Intercept Pharmaceuticals: Do Not Expect PBC Sales To Save The Company

2023-05-22 13:17:02 ET

Summary

- After last Friday’s unfavorable AdCom meeting, Intercept’s NASH candidate now appears dead on arrival.

- Some analysts have suggested that Intercept's valuation will be buttressed by their PBC franchise - which may be extended if their OCA-Bezafibrate combination trials are successful.

- With the potential approval of elafibranor and seladelpar looming, I would avoid betting on Intercept’s PBC franchise.

- Operating expenses remain stubbornly high - and there's still a sizable debt chunk - posing an existential risk for Intercept moving forward.

Introduction

When I last assigned my sell rating to Intercept ( ICPT ) nearly a year ago, the equity was trading at $17.45 a share. As of the time of writing, the stock is down by ~27% (trading under $10 a share.) Since then, much has changed.

Some aspects remain the same: Operating expenses remain stubbornly high, there's still a palpable debt burden, and Intercept remains unprofitable. What has changed is that a formal advisory committee commissioned by the FDA has evaluated obeticholic acid ((OCA)) as a NASH treatment, with most members voting against the notion that the treatment profile is favorable (12/16 voting in the negative) or that it merits accelerated approval (15-1 voting against.) The FDA - in the vast majority of cases - aligns their final ruling with the findings of the advisory committee, which would lead to the FDA rejecting OCA and ending Intercept's NASH dreams.

More importantly, there's now information from the FDA directly regarding their perspective on OCA's candidacy as a NASH treatment is public. Slides and documents prepared by and released by the FDA during their advisory committee emphasize an unfavorable safety profile - giving insight into how the FDA internally views OCA's candidacy as a NASH treatment. (The FDA has scheduled a PDUFA date of June 22 for their NDA response.)

In my view, it's a moot point now that the FDA will not grant approval. However, the future of Intercept remains in debate. Analysts from Seedhouse and Raymond James both pointed to its PBC franchise as reason for optimism, but I think this perspective is incongruent with a treatment landscape that is ripe for potential change.

In this article, I will briefly unpack some important conclusions to draw from the AdCom discussions, as well as highlight important. Thereafter, I will highlight the emerging disruption to Intercept's PBC franchise that the market is overlooking at the moment. To conclude, I will briefly review my concerns with their capital position.

All in all, I would assign Intercept a strong sell rating. The pipeline simply isn't there, and the path to profitability appears non-existent with their current level of operating expenses.

The May 19 Challenging Outcome

The independent panel of experts convened by the FDA to assess OCA evaluated had two questions to grapple with: Do the benefits of 25 milligrams of OCA outweigh the risks in treating stage two and stage three NASH patients, and does the existing evidence support accelerated approval? And they apparently answered with a resounding no to both of those questions .

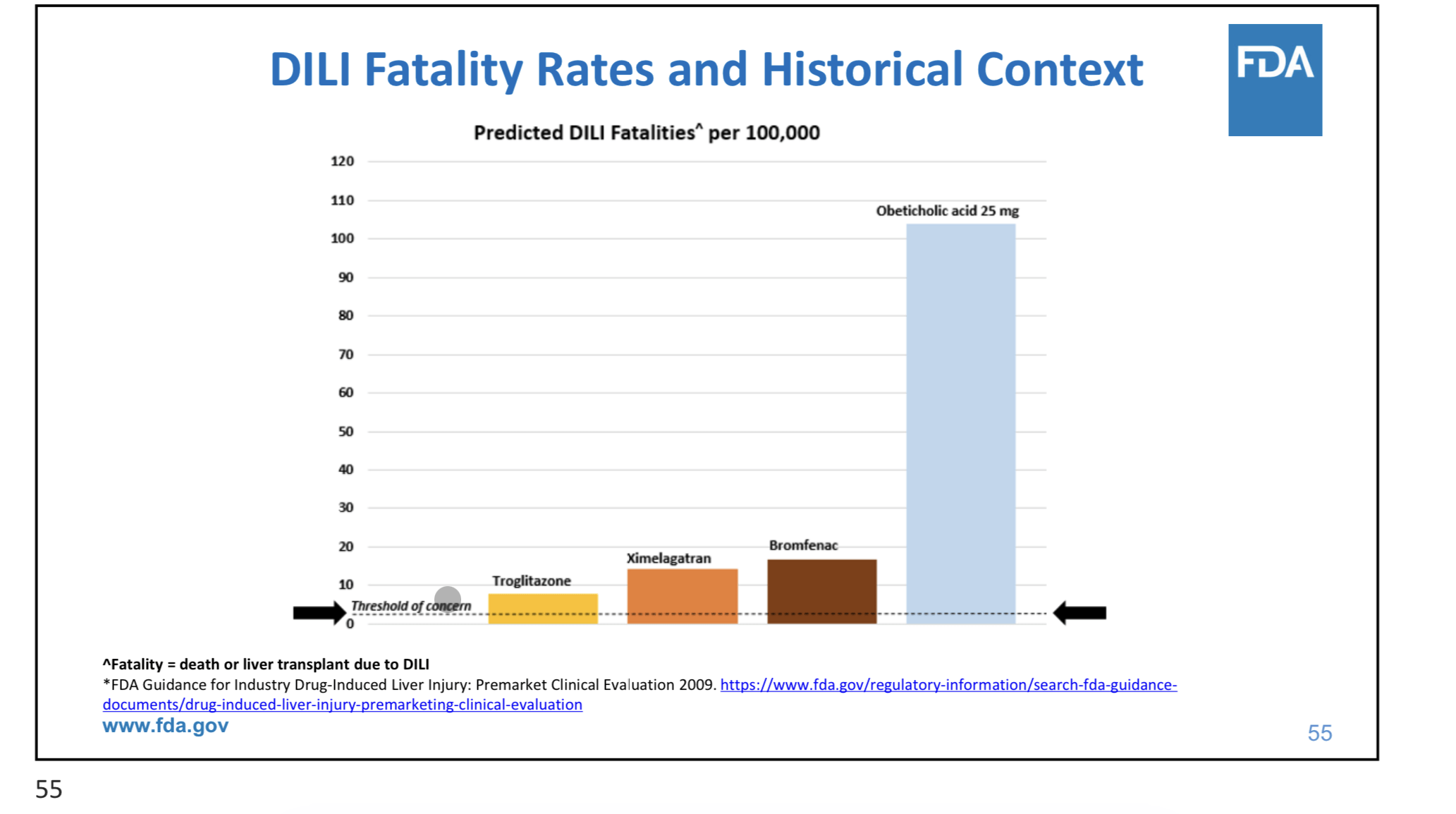

The main concern discussed in the AdCom revolved around different safety signals. And the panel took notice of several key elements. The FDA themselves emphasize that the 25 milligram dose (the dosage that hit one of the two primary endpoints in REGENERATE) "exacerbates co-morbidities or creates new ones for a patient population at risk for metabolic syndrome and its manifestations." Six co-morbidities were cited in total: Hepatotoxicity, excess risk of cholecystitis and bile duct stones/sludge, excess risk of onset diabetes, substantial excess risk of dyslipidemia, substantial excess risk of severe pruritus and excess risk of acute kidney injury. It's worth noting that the document explicitly mentions how the death or transplant rate of the 827 subjects exposed to OCA is 18 times greater than the rate that typically raises agency concerns for drug approvability.

Adcom Presentation for OCA - Slide 55 (FDA)

{kind=link}

The slide depicted above from the FDA presentation during the AdCom exemplifies the magnitude of the risk factor. It shows the predicted drug induced liver injury fatality (DILI) rates of OCA in comparison with three other drugs. (It should be noted that all three of those drugs were pulled by the FDA because of their excessively high DILI rates.)

Consider the following paragraph from the conclusion segment of the briefing document:

While FDA recognizes presently there is an unmet need, the Agency's current benefit-risk assessment includes selecting patients for long-term OCA treatment that will require baseline liver biopsy. Further liver biopsies may be required during treatment given the uncertainty of predicting DILI when one considers transaminase fluctuations in NASH, and along with a higher risk than the general population for cholelithiasis and its complications. Therefore, despite the modest treatment effect over placebo, FDA cannot justify OCA use in NASH subjects with Stage 2 or 3 fibrosis.

Source: Page 53 of FDA Briefing Document, NDA # 212833

The last sentence speaks for itself, and it would - in my view - take a miracle for the FDA to approve NASH. Moreover, mandating liver biopsy prior to long-term OCA treatment would greatly dampen sales even if OCA were miraculously approved. NASH is often asymptomatic until the later stages, and even many participants who undergo biopsies in hopes of enrolling in a NASH trial often do not show the level of fibrosis needed for inclusion. Taken together, these statements from the briefing document and other FDA provided materials suggest that there is a small chance that the FDA sees any reason to go against the vote of the advisory committee.

Intercept's Poor Transparency

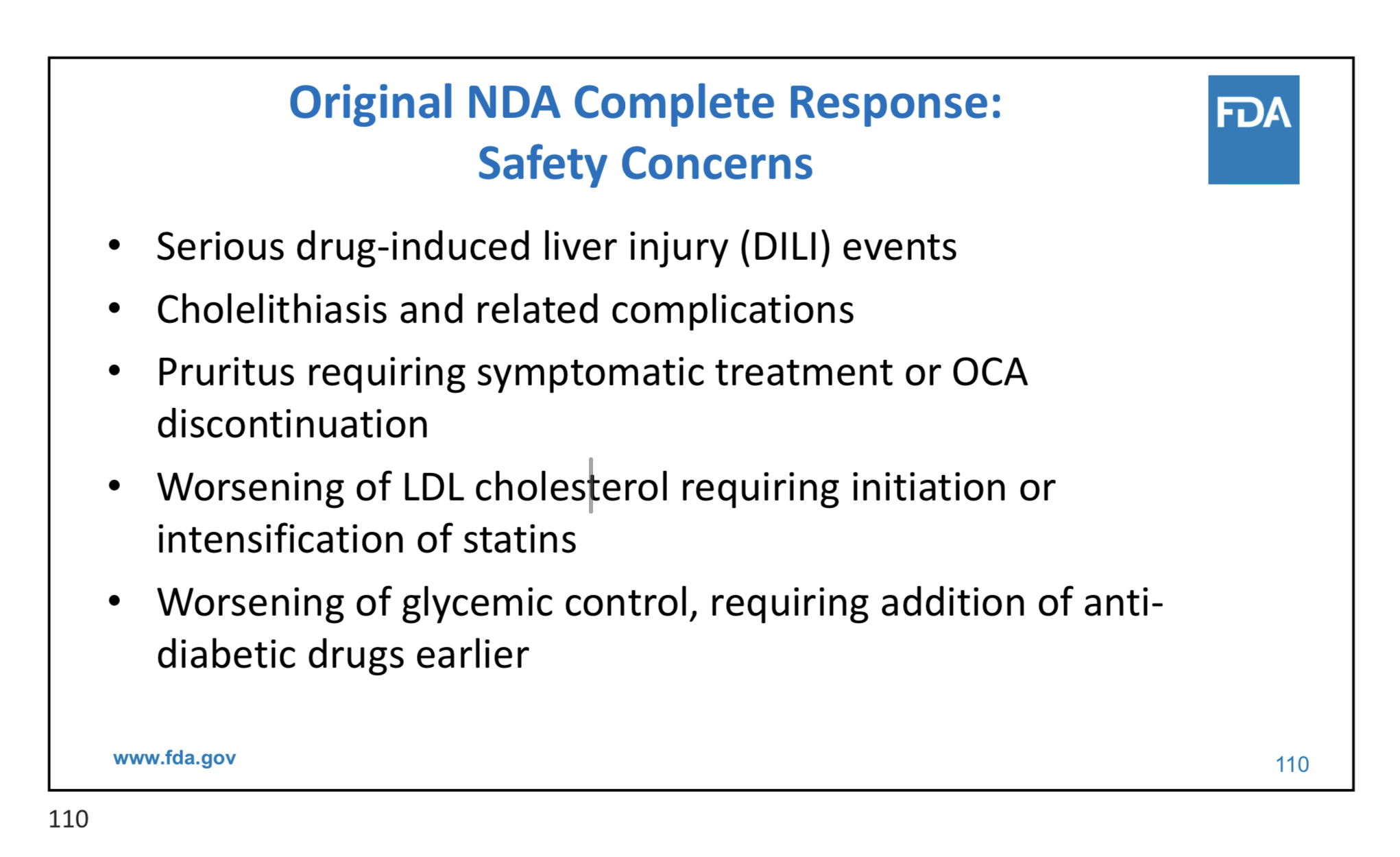

If the FDA refuses to grant approval in June, it would not be Intercept's first rejection. They received a CRL for their original NDA of OCA from the FDA in 2020, and instead of running another trial, they decided to reanalyze the existing data. When I last wrote about Intercept, I noted how there was no way to know if this is actually what the FDA requested or not. I argued that Intercept should release a copy of the CRL to the public for full clarity. In retrospect, this suspicion was warranted.

Adcom Presentation for OCA - Slide 55 (FDA)

{kind=link}

Also, from the AdCom presentation, the slide above highlights the reasons why the FDA responded with a complete response letter to their original NDA. Intercept did not disclose any of these details in neither their original press release upon first receiving the CRL , nor in any other follow-up communications. It's difficult to understand why Intercept did not reveal these specific safety concerns to the public.

What About PBC?

One aspect where I was incorrect in my earlier analysis was assuming that OCA's PBC related sales would stagnate. They have instead grown modestly, exceeding analyst expectations in some quarters . However, the revenue stream is still not large enough to translate into profitability. (They missed bottom and top-line expectations in their latest quarter, too.)

The method of use and finished drug patents for OCA are set to expire in 2036, so Intercept still has over a decade of sales to accumulate from their franchise. If they're able to successfully get their combination therapy - OCA in conjunction with bezafibrate - across the regulatory finish line, then it would extend the lifespan of that commercial stream by many years. It is a big if, but it's possible.

However, this occurring is certainly not something that I would bet on. Data from two phase two trials evaluating the combination are due to be presented in June . There simply isn't enough existing data to draw any strong conclusions about efficacy or safety improvements from the dual therapy.

However, there's existing data supporting the approval of two rivaling therapies from CymaBay ( CBAY ) and Genfit ( GNFT ) respectively: Seladelpar and elafibranor. Both assets are being evaluated in phase three trials, with elafibranor ahead and due to post data soon ( end of Q2'23 ); seladelpar finished enrolling their phase three trial earlier this year in August.

Both have their own merits, and both have reported strong efficacy in earlier phase two trials. Although it's difficult to compare data directly (heterogenous patient pool, differing endpoints in some trials etc.) it should be noted that PBC is a small market. OCA has a black-box warning for safety, and the severe pruritus associated with the treatment is a major issue for many who have to take it. ( Elafibranor and seladelpar actually both resulted in reductions of pruritus in their respective trials.) These therapies may come onto the market as soon as the end of 2024 or 2025, competing head-to-head with OCA - threatening the only revenue stream that Intercept has.

Conclusions - Debt Is Still A Problem

When I last wrote about Intercept, they had ~$710 million in debt on their balance sheet. Since then, they have taken action to shrink that burden, resulting in their debt today totaling ~$220 million. It's a major improvement, but it's still a problem because operating expenses remain stubbornly high.

Total operating expenses for this past quarter were the highest they have ever been compared to any of the past eight quarters prior. Despite reporting Ocaliva sales that exceeded expectations, operating income still fell further into the red because of how sharply expenses rose.

This should be a time for austerity, because their ~$430 million cash pile will not last forever. Until expenses are sharply reduced, the looming threat posed by the debt pile and the risk of secondary equity raises will grow. (Remember, Intercept still has more trial expenses to contend with down the line, too.)

At the moment, Intercept faces too many challenges to merit a prospective investment. Every day, the company is losing cash as competing therapies inch closer to reaching the market - and their NASH candidacy (in my opinion) faces long odds for approval. I would assign Intercept a strong sell rating because of this difficult context.

Risks To Thesis

Although I believe Intercept is a strong sell going forward, there are palpable risks to my thesis. Notably, the market could react positively if Intercept were to decide that they're axing their NASH program in order to focus on profitability. In their last quarterly conference call, they suggested that they would follow this path if OCA were not granted approval for NASH.

In summary, we believe that our balance sheet cash position and foundational PBC business provide us with the financial strength to grow our existing business and meet our strategic objectives, including preparation for a commercial launch in NASH should we gain approval by the FDA or a pivot to profitability if we are unable to achieve an approval in NASH. - Andrew Saik, CFO.

If they were to "pivot to profitability" with their PBC franchise, it could positively impact the market sentiment surrounding their future - resulting in multiple expansion.

Another risk to this thesis lies in their PBC franchise being stronger than I anticipate. Seladelpar and Elafibranor could fail their phase three trials or perform poorly in comparison to OCA, allowing it to in turn retain a dominant market position. Or, OCA in conjunction with bezafibrate could prove to be much more efficacious and safe than OCA alone, thus accelerating sales and retaining market share in the PBC space for Intercept.

For further details see:

Intercept Pharmaceuticals: Do Not Expect PBC Sales To Save The Company