ICPT - Intercept Pharmaceuticals: Will OCA Win Approval For NASH In June?

2023-04-12 12:54:05 ET

Summary

- Intercept Pharmaceuticals markets and sells Ocaliva to patients with primary biliary cholangitis.

- Sales grew >10% in 2022 and are forecast to grow ~14% in 2023, to ~$325m, but the much larger market opportunity is in non-alcoholic steatohepatitis ("NASH").

- OCA has been rejected once in NASH by the FDA, but Intercept recently resubmitted its NDA and a PDUFA date is set for June 22.

- Before that, an FDA Advisory Committee will convene on May 19 to discuss the case for approval.

- The riches to be gained from a NASH approval are enough to at least double Intercept's valuation but a more likely scenario may be that OCA is rejected again. I break down the arguments for and against buying stock at an >85% discount to former highs.

Investment Overview

Over the past 12 months the share prices of several biotech companies developing drugs targeting non-alcoholic steatohepatitis ("NASH") - a liver disease with a prevalence of nearly 50m in the US and Europe, ~19m of which have NASH with significant fibrosis (which can lead to liver cirrhosis, liver failure and liver cancer) - have been skyrocketing.

The share price of Madrigal Pharmaceuticals (MGDL) has risen >165% across the past 12 months, based on Phase 3 data that met both primary endpoints of NASH resolution with a 2-point reduction in Non-Alcoholic Fatty Liver Disease Activity Score ("NAS") and no worsening of fibrosis, and a >1 stage improvement in fibrosis with no worsening of NAS.

Madrigal expects to file its New Drug Application for its candidate Resmetirom in the first half of this year and the data appears to support the company's push for an accelerated approval.

Meanwhile the share price of Viking Therapeutics ( VKTX ) - whose NASH candidate VK2809 has a similar mechanism of action ("MoA") to Resmetirom, being a selective thyroid hormone receptor beta (TR?) agonist, is up >500% as investors await updates from a Phase 2b VOYAGE study. Admittedly, Viking stock also has been gaining on positive Phase 1 data relating to its weight loss candidate, VK2735, but the progress made by Madrigal has upped expectations for VK2809.

Two other companies - 89bio ( ETNB ) and Akero Therapeutics ( AKRO ) - have seen their stock prices rise by >330% and >170% across the past 12 months, based on clinical progress of their NASH candidates Pegozafermin and Efruxifermin - both drugs are engineered to mimic the biological activity profile of native FGF21, an "endogenous metabolic hormone that regulates energy homeostasis, glucose-lipid-protein metabolism and insulin sensitivity."

In other words, the so-called "NASH dash" - the race to have a first drug approved to treat NASH, opening up a double-digit billion dollar market opportunity - has been heating up, although surprisingly, the share price of the company that remains a warm favorite to win the race - Intercept Pharmaceuticals ( ICPT ), the subject of this post - has sunk in value by 7% over the past year.

Intercept Overview - Cash Rich, Commercial Stage Pharma Currently Leading The "Nash Dash"

Morristown, New Jersey,-based Intercept has ~350 employees, and unlike its closest current rivals in the "NASH Dash," it already secured approval for its lead drug Ocaliva, a formulation of obeticholic acid ("OCA"), which is a farnesoid X receptor ("FXR") agonist. Activating FXR helps to increase the flow of bile acids out of the liver and reduces exposure to toxic bile acids, according to Ocaliva.com .

Since May 2016, Ocaliva has been - according to Intercept's 2022 10K submission:

approved in the United States, the United Kingdom, the European Union and several other jurisdictions for the treatment of primary biliary cholangitis (“PBC”) in combination with ursodeoxycholic acid (“UDCA”) in adults with an inadequate response to UDCA or as monotherapy in adults unable to tolerate UDCA

The PBC market is much smaller - <$2bn per annum - than a NASH market is projected to become - perhaps >$40bn per annum. Ocaliva's net sales in 2022 were $285.7m, which represents double-digit year-on-year growth, and management is guiding for $310 - $340m of net sales in 2023, up ~14% year-on-year at the midpoint of guidance. Sales of Ocaliva have not yet made Intercept profitable however - earnings from continuing operations across the past 4 years have been $(345m), $(273m), $(136m) and $(175m).

Last year, after selling the rights to market and sell Ocaliva, and develop the drug for NASH outside of the US, for $450m to Advanz Pharma, Intercept was able to report net income of $222m. Intercept also boasts ~$485m of cash, versus current liabilities of $230m, and long term debt of $223m, reduced from $540m during the course of last year.

Winding Path To Second NASH Approval Shot

Although Intercept refers to its PBC business as "sustainable and growing," an approval for Ocaliva in NASH must surely remain the key goal.

The company does have other pipeline assets - it's developing a fixed-dose combination of OCA and bezafibrate for patients with PBC who have not achieved an adequate biochemical response to UDCA, and a next-generation FXR agonist, INT-787, which has secured its Investigational New Drug ("IND") approval from the FDA and entered a Phase 2a clinical study in patients with severe alcohol-associated hepatitis ("SAH").

Nevertheless the NASH market opportunity dwarfs that in PBC, or likely SAH, and Intercept has a Prescription Drug User Fee Act ("PDUFA") date upcoming on June 22, when the FDA will rule on whether to approve Intercept's New Drug Application ("NDA") for treatment of pre-cirrhotic liver fibrosis due to NASH.

This is the second NDA Intercept has submitted for Ocaliva as a therapy for NASH. The first was submitted in 2019, shortly after Intercept released results from its Phase 3 study REGENERATE and was backed up "data from 35 clinical trials and more than 1,700 NASH patients treated," and it was rejected by the FDA. According to a press release , the FDA's Complete Response Letter ("CRL"), outlining reasons for rejection stated that:

based on the data the FDA has reviewed to date, the Agency has determined that the predicted benefit of OCA based on a surrogate histopathologic endpoint remains uncertain and does not sufficiently outweigh the potential risks to support accelerated approval for the treatment of patients with liver fibrosis due to NASH.

Prior to the rejection, Intercept's share price had reached a peak value of ~$120, but the news caused the stock price to fall <$50 and it has failed to recover, sinking to its current value of $16 per share.

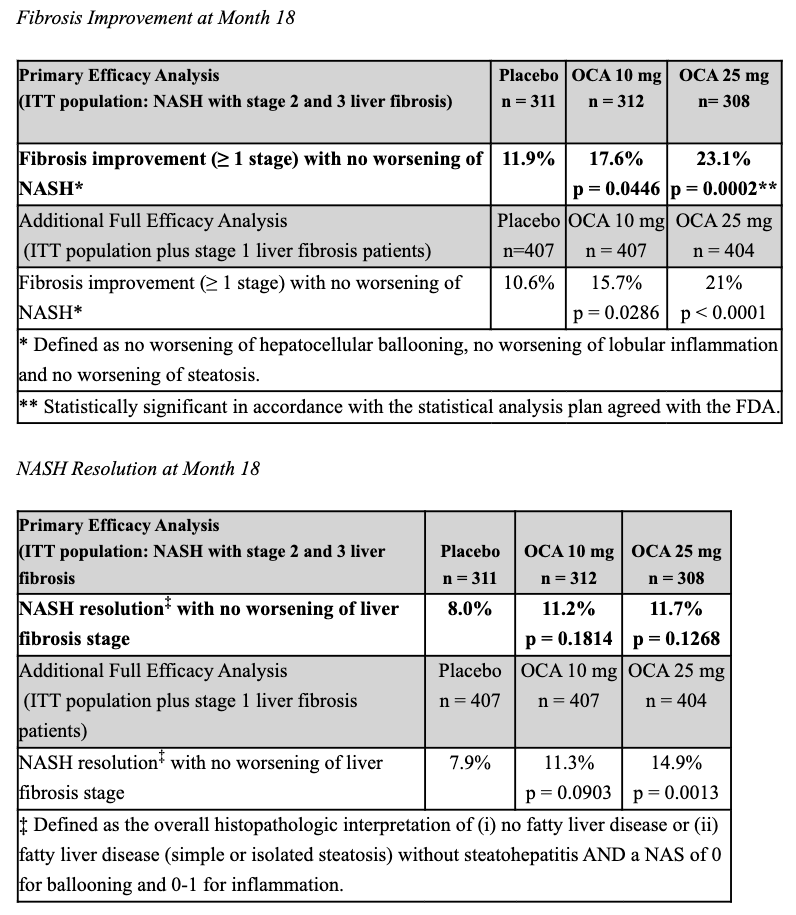

According to Intercept's 2022 10K submission the 2019 REGENERATE results showed that OCA 25mg:

... met, with statistical significance, the primary endpoint agreed with the FDA of fibrosis improvement by at least one stage with no worsening of NASH (defined as no worsening of hepatocellular ballooning, no worsening of lobular inflammation and no worsening of steatosis) at the planned 18-month analysis.

Adverse events were "generally mild to moderate in severity and the most common were consistent with the known profile of OCA." The REGENERATE study had 2 primary endpoints however and the 10K states that:

Although a numerically greater proportion of patients in both OCA treatment arms compared to placebo achieved the primary endpoint of NASH resolution with no worsening of liver fibrosis in the primary efficacy analysis, this result did not reach statistical significance.

NASH resolution is defined as the overall histopathologic interpretation of (i) no fatty liver disease or (ii) fatty liver disease (simple or isolated steatosis) without steatohepatitis AND a non-alcoholic fatty liver disease (“NAFLD”) activity score (“NAS”) of 0 for ballooning and 0-1 for inflammation.

{kind=link}

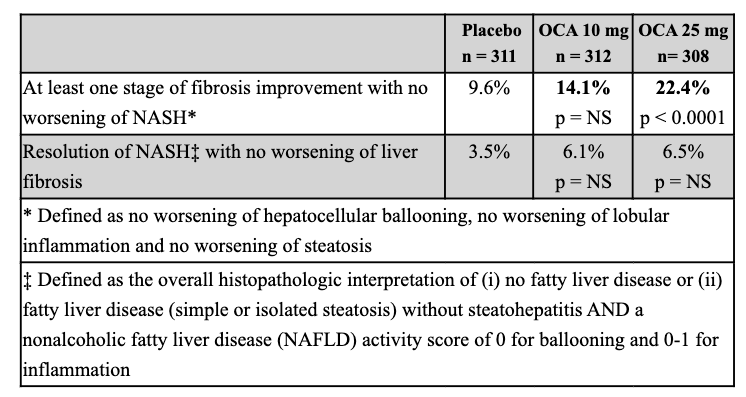

Clearly, the missed endpoint may have influenced the FDA's decision not to approve OCA for NASH, and unfortunately for Intercept, when the company announced data from a new interim analysis last year, the NASH resolution endpoint had still not been met with statistical significance.

New interim analysis of REGENERATE STUDY (10K submission 2022)

{kind=link}

The updated data doesn't suggest the FDA is likely to change its mind about OCA in June when the PDUFA arrives for second time, although after resubmitting its NDA, Intercept's share price did begin to climb, reaching highs of >$20, before it was revealed that the FDA had arranged for an Advisory Committee to convene on May 19th, to discuss the NDA application and whether to approve OCA in NASH.

What Conclusions Will FDA AdComm Draw Regarding Approval of OCA in NASH?

As soon as Intercept circulated a press release about the AdComm date, its stock price began to fall, reaching a low of $13 at the beginning of this month, although it has begun to climb slightly since.

NASH is a notoriously tough indication to design drugs for and the FDA's stringent approval criteria, shared by the European Authorities - Intercept eventually withdrew its marketing application for the region after the failing to extend the review period to include new data - is the reason why no drugs are approved to treat NASH.

Trials of NASH drugs are expensive, since they involve patients undergoing liver biopsies, and in a commercial setting, the requirement for a liver biopsy to be conducted before a NASH drug can be prescribed could be a major stumbling block as insurers may not want to provide reimbursement for such a risky and costly procedure. Some physicians simply believe NASH is better treated with a more active lifestyle than with a drug.

NASH drug developers have nevertheless been desperately searching for alternative biomarkers that could be a surrogate for a liver biopsy, but the FDA's stance on surrogate endpoints has been inflexible to date - could the AdComm prove to be more supportive of Intercept's data and request for approval?

After a review meeting in October 2020 Intercept says that the FDA:

provided us with helpful guidance regarding supplemental data we could provide to further characterise OCA’s efficacy and safety profile that could support resubmission based on our Phase 3 REGENERATE 18-month biopsy data, together with a safety update from our ongoing studies.

Ultimately, however, after Intercept went back and reanalyzed its data it still could not meet its NASH resolution endpoint. If not a great deal changed data-wise since the last approval shot, it seems logical that the FDA and its AdComm will raise the same objections as last time.

Perhaps sensing it needed to provide more evidence of efficacy or target a slightly different type of patient, Intercept has conducted a new study, REVERSE, in ~900 NASH patients with biopsy confirmed diagnosis of cirrhosis due to NASH. In September 2022, however, the company revealed that the REVERSE study:

did not meet its primary endpoint of a ? 1-stage histological improvement in fibrosis with no worsening of NASH following up to 18 months of therapy.

In fairness to Intercept, the new data supporting its second bid includes longer safety follow-up, and a link between use of OCA and improvement's in NASH patients' conditions has clearly been established, even if it has not reached statistical significance at times.

The drug has proven safe and effective to date at treating PBC, although it should be noted this accelerated approval could still be withdrawn if post-marketing studies do not support the original pivotal studies, and that Ocaliva in PBC is administered at a lower dose than the 25mg planned for NASH.

It would certainly be interesting to see what the AdComm made of OCA and its effects on treating NASH if there were no competing therapies with late stage study data under their belts, but unfortunately for Intercept, there are several.

Does The Strong Competitive Field Preclude Approval for OCA in NASH?

The problem that Intercept has is that Resmetirom will likely be up for approval soon, and unlike OCA, Resmetirom met both of its dual primary endpoints in its MAESTRO study, so the FDA could theoretically reject OCA and opt to approve Resmetirom instead. Furthermore, after Resmetirom, 89Bio and Akero could both achieve positive outcomes in their Phase 3 studies of Pegozafermin and Efruxifermin, and Viking Therapeutics' candidate may also warrant an approval next year.

Perhaps even more concerning for Intercept, and the others, is the fact that pharma giants Eli Lilly ( LLY ) and Novo Nordisk ( NVO ) have developed GLP-1 receptor agonists - Tirzepatide and Semaglutide - that already are making waves in diabetes and weight loss and which also are being tested in NASH. These two drugs are expected to drive peak revenues in excess of >$25bn per annum, and if they do secure approvals to treat NASH, the Pharmas much larger marketing budgets could sideline the smaller biotechs in a battle for market share.

There's one alternate theory that could play out in Intercept's favor however. The FDA has been known to make controversial decisions around drug approvals - for example when approving Amylyx' Amyotrophic Lateral Sclerosis ("ALS") drug Relyvrio last year - and could use the upcoming AdComm for OCA to announce new guidelines around approving NASH targeting drugs.

The FDA could decide, for example, that approving multiple different classes of drug in NASH could be the best way to serve patients, and therefore advise its AdComm to consider voting for approval - and even if the AdComm disagrees and votes against an approval, the FDA ultimately has the final say.

What's for certain is that all NASH drug developer's eyes will be on the AdComm in May, as the FDA will be forced to show its hand and rule on what constitutes grounds for an approval and what may lead to rejection, and whether anything has changed since OCA was rejected in 2020.

Conclusion - Is Intercept Pharmaceuticals a Buy, Sell, or a Hold?

To summarize the arguments for and against backing Intercept as a viable investment opportunity I would list the pros and cons as follows, beginning with the pros.

- Intercept is currently ahead in the NASH approval race with its PDUFA date set for June 22 and an AdComm convened for May 19.

- Ocaliva is approved to treat PBC and its revenues are growing - net sales are forecast to rise ~14% in 2023 to ~$325m

- The resubmitted NDA contains longer-term safety data and the drug has met a key primary endpoint indicating that it can benefit patients.

- Ocaliva is well-funded and operating losses have been narrowing in each year.

Switching to the Cons:

- OCA has been rejected before in NASH, based on a key missed endpoint which was still not met after data was re-evaluated ahead of the latest NDA submission.

- OCA missed a key endpoint in a study in patients with compensated NASH cirrhosis, narrowing the addressable market even if the drug is approved.

- The FDA would likely have to re-evaluate its NASH approval criteria in order to approve OCA - this appears unlikely given several other candidates may be capable of meeting existing approval criteria.

- Intercept could struggle to capture market share in NASH, even if OCA were approved, given the likely presence in the market of GLP-1 receptor agonists developed by large Pharmas Lilly and Novo Nordisk.

- Intercept may experience patent issues around Ocaliva in PBC as well as NASH.

Intercept's market cap is currently $673m, which is just about 2x forecast net sales revenues in 2023. That seems low, so is there an argument that Intercept is undervalued based on its PBC opportunity alone? If we typically value a commercial stage pharma at ~5x sales, then could Intercept's true worth be more than double what it stands at today?

There are a couple of issues with that way of thinking. First of all, Intercept is not profitable, so its sales revenues are to some extent irrelevant - unless the company can develop a profitable business model, despite its large cash reserves, it will eventually run out of funding. $450m was raised by selling the ex-US rights to its lead drug, but that's a one-off deal - recent levels of losses cannot be sustained, especially with long-term debt >$200m still to pay back.

The other issue is to do with patent protection. In 2022, Intercept entered into settlement agreements with no fewer than six generic drug manufacturers - Apotex, Lupin, Amneal, Optimus, MSN and Dr Reddy's - by the terms of which the manufacturer's agreed not to commercialize a version of Ocaliva before 2031. All six had submitted Abbreviated New Drug Applications (“ANDAs”) challenging Intercept's patents, whilst Intercept has an upcoming court case (in 2024) against a 7th company, Zenara, who also hope to launch a generic form of Ocaliva (data from 10K submission).

If Zenara prevails in that court case it could spell trouble for Intercept, as it may permit a generic version of Ocaliva to be marketed, meaning Intercept would likely have to drop the price of its drug, and cede market share, which may significantly impact its top and bottom lines. Presumably, settling the other cases was a costly process, and it seems likely that by the beginning of the next decade, if not before, the peak revenue potential of Ocaliva will be falling year-by-year.

Pricing is another issue that could lead to an FDA rejection in NASH - a recent study completed by the Institute for Clinical and Economic Review ("ICER") concluded that:

The cost-effectiveness of both drugs will depend on their price though, notably, at our placeholder price, Resmetirom would appear to be cost saving. If the price of OCA is not substantially reduced from the price of the approved (lower) doses used for PBC, it will not meet typical cost-effectiveness thresholds.

The report gave Resmetirom a placeholder price of $19k, vs. Ocaliva's $85k. Although Intercept management heavily criticized ICER's model during its Q422 earnings call with analysts, the fact remains that Ocaliva's current pricing structures may have to be heavily revised owing to both generic competition, and if the company wants to expend its label into NASH.

Summarizing all of the above opportunities and threats, I still think it's tricky to make a call on Intercept stock at the present time. An optimist may believe that the market is already factoring in an FDA rejection in NASH and therefore buying shares in the hope of a surprise approval is essentially a risk free opportunity.

A pessimist on the other hand may see little prospect of a NASH approval and also note that in PBC, Ocaliva is under threat from generic competition, and that the company is not profitable, and not likely to become profitable when pricing pressure and limited patent protection are factored in.

I do think it's important for the share price long term that Intercept gets an approval in NASH, although the new version of OCA and bezafibrate the company is developing may help protect it from generics within the PBC market.

By rights, Intercept does not have the data necessary to force the FDA to approve OCA, so I will remain on the sidelines in relation to this opportunity, although those with a larger appetite for risk may be tempted to bet that the FDA surprises everyone in May when the AdComm takes place.

The gains on offer should that happen would likely be in the triple-digit percentages, while losses on a rejection would be much milder, but unfortunately, the latter scenario appears the more likely at this time. All eyes now turn to the AdComm.

For further details see:

Intercept Pharmaceuticals: Will OCA Win Approval For NASH In June?