IDCC - InterDigital's Mixed Q3: Strong Deals Organic Growth Concerns

2023-12-01 11:35:18 ET

Summary

- InterDigital, Inc. delivered mixed Q3 2023 results, with strong license agreements boosting revenue and free cash flow.

- Concerns persist about the company's underlying organic growth and negative year-over-year revenue growth in Q4.

- InterDigital remains attractively priced and committed to returning capital to shareholders.

Investment Thesis

InterDigital, Inc. ( IDCC ) delivered Q3 2023 results which were mixed. On the one hand, there's enough in this set of results to put a solid BUY rating on this stock. Not only was the sale of two license agreements very welcome on the top line, but it also allowed IDCC's free cash flow line to swell.

But on the other hand, the issue I have with IDCC is that its underlying organic growth isn't particularly strong.

So I remain neutral on this stock.

Rapid Recap

In my previous analysis back at the start of October, I said:

As we surmise this analysis, what stands before us is a less than straightforward thesis, with enough bullish and bearish arguments for both sides of the trade.

On the one hand, InterDigital has recently raised its dividend payout by 14% y/y, on top of repurchasing around 12% of its stock so far in 2023.

On the other hand, InterDigital's growth rates leave a lot to be desired and I'm not sure that paying around 18x forward free cash flows is such a cheap valuation. But is that enough to warrant shorting the stock? I'm not sure. And yet, the stock is around 11% shorted already.

Since then, in hindsight, this stock has been on a tear.

Michael Wiggins De Oliveira on IDCC

Evidently, I made a bad call here by staying neutral. And what's particularly interesting, is that since I made that bad call, the short interest has actually increased to just over 13%. And yet, the stock price is sizzling.

However, I remain neutral on this name. Here's why.

InterDigital's Near-Term Prospects

InterDigital is a company focused on research and development in wireless communication, video, and AI technologies.

They monetize their innovations through licensing agreements with companies across various industries, including major players like Apple, Samsung, and Google. The company's core mission is to pioneer advancements that enhance connected experiences in communication services.

InterDigital possesses a substantial patent portfolio of nearly 30,000 patents and patent applications, serving as a primary revenue source (more on this soon). Their licenses are applied in wireless communications, consumer electronics, personal computing, and automotive sectors, contributing to global technology standards.

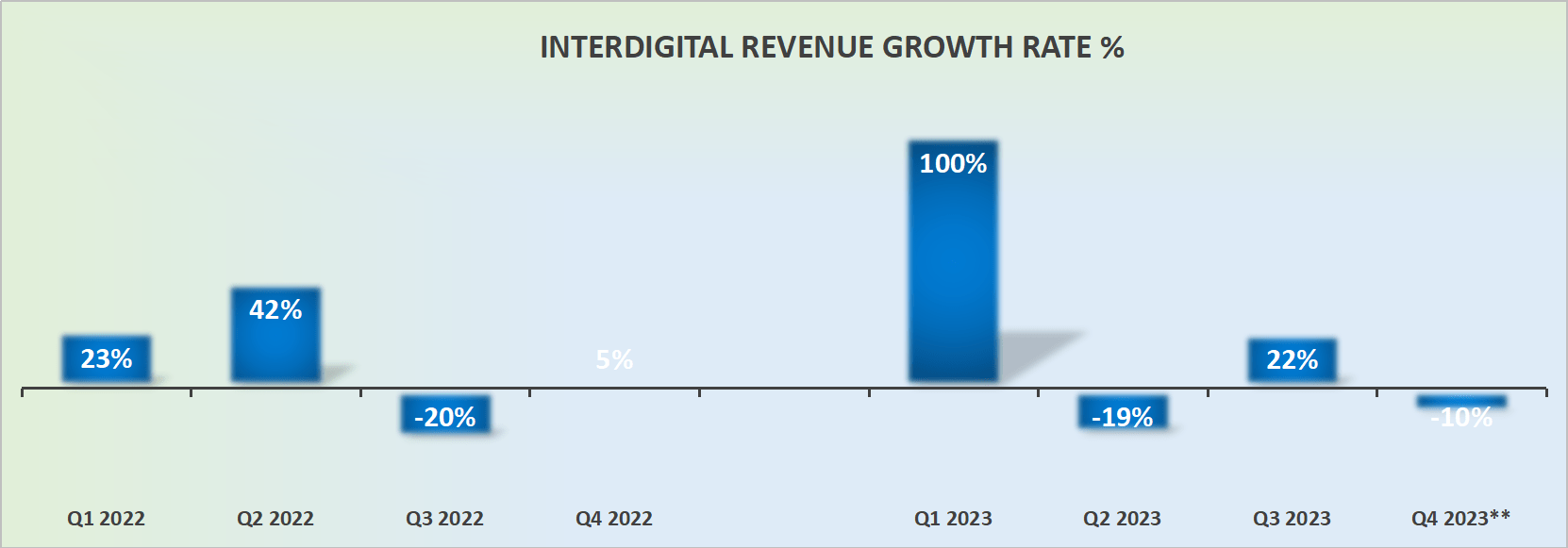

During the earnings call , Liren Chen, the President and CEO, highlighted the company's robust financial performance, boasting a 22% year-over-year increase in revenue, a 19% surge in smartphone licensing revenue, and a 30% rise in CE and IoT licensing revenue.

The multi-year royalty-bearing license with Lenovo, covering HEVC video compression technology, underscores the company's ability to secure valuable agreements with industry leaders.

Furthermore, InterDigital's active involvement in the Avanci 5G automobile patent licensing platform, licensing both Mercedes-Benz and BMW for 5G, demonstrates a strategic positioning in the lucrative connected car market. The continuous innovation, exemplified by the company's 30,000 granted patents and pending applications, solidifies its status as a key player in wireless and video technologies. As Liren Chen stated, "The strength of our portfolio was recently confirmed by a new analysis from LexisNexis, recognizing InterDigital as having one of the top five 5G patent portfolios in the world."

However, amid InterDigital's promising trajectory, the company faces certain challenges that warrant careful consideration. One notable challenge is the ongoing arbitration with Samsung regarding the smartphone licensing program. While Samsung has agreed to take a license to InterDigital's portfolio starting January 1, 2023, the final terms are subject to determination through arbitration, with the hearing scheduled for the summer of the following year and the final decision expected by the end of 2024.

The resolution of licensing disputes, particularly with major industry players like Samsung, remains a crucial challenge for InterDigital in maintaining its revenue momentum.

This leads to the crux of the bear thesis.

Revenue Growth Rates Looks Solid, With a But

{kind=link}

Some context is needed. InterDigital's Q1 2023 saw its revenues increase triple digits. However, the strong increase in revenues was due to the positive settlement of the Lenovo trial.

Secondly, during Q3 2023, there were two new patent license agreements. These agreements are very lucrative for InterDigital. On the top line, but particularly on the bottom line.

But the issue I have is that these deals are non-recurring. And by extension, we can see that InterDigital's guidance for Q4 points toward negative y/y revenue growth rates.

This is not such a big issue in and of itself, rather it's more the case that given its unpredictable growth rates, it's difficult to ascertain a reasonable multiple on its valuation.

Because when it comes down to the recurring revenue stream, it was only up 3% y/y. Put another way, the recurring revenue stream is delivering about $450 million of annualized revenues, and it's not growing all that fast.

IDCC Stock Valuation -- Attractively Priced

Here's where the bull case is found. Because up until this moment, I've simply highlighted the challenging matter of getting to grips with its growth rates. However, the stock is cheaply valued on a free cash flow basis.

Here I'll refer only to EBITDA and not free cash flow. The reason being that during the earnings call , management explicitly noted its very strong free cash flow in the quarter, alluding to the fact that investors should not expect this sort of cash flow to be a recurring feature.

Nonetheless, IDCC is now on a path towards approximately $350 million of annualized EBITDA. A figure that is up 37% y/y from 2022.

What's more, IDCC is eager to capitalize on its strong cash flows and return capital to shareholders. While its dividend isn't particularly noteworthy, at less than 2%, what is attractive is its share repurchase program.

During Q3 IDCC repurchased 700K worth of shares at approximately $81.30. With the share price at very close to $100 per share right now, those were clearly terrific buybacks.

And on top of all that, IDCC still holds approximately $400 million of net cash.

The Bottom Line

In summary, InterDigital's Q3 2023 results showcase a mixed performance, with strong license agreements boosting revenue and free cash flow, but concerns persist about the company's underlying organic growth.

Despite recent stock surges, the non-recurring nature of lucrative deals and a cautious Q4 guidance hinting at negative year-over-year revenue growth raise questions about sustainability.

The challenges in predicting growth rates and the ongoing arbitration with Samsung add complexity. While InterDigital, Inc. remains attractively priced and demonstrates a commitment to returning capital to shareholders, the uncertainties surrounding sustained growth prompt me to maintain a neutral stance on the stock.

For further details see:

InterDigital's Mixed Q3: Strong Deals, Organic Growth Concerns