SGOV - Interest Rates Aren't Sustainable At Current Levels

2023-03-14 09:35:09 ET

Summary

- The rapid rise in interest rates has been cheered on with little thought given to the consequences.

- The stress on a number of smaller US banks at the moment is the outcome of 13 years of loose monetary policy, followed by an extremely rapid tightening.

- Without a significant decline in interest rates, asset prices, lending and economic activity are likely to contract.

The rapid rise in interest rates over the last 12 months has been viewed by many as a necessary and insufficient measure to control rampant inflation. Whether this is the case is questionable, but the way that monetary policy has been implemented with little consideration of downstream effects is now becoming apparent. The collapse of Silicon Valley Bank ( SIVB ) highlights the predicament banks and the broader economy now finds itself, unless interest rates decline significantly in coming months.

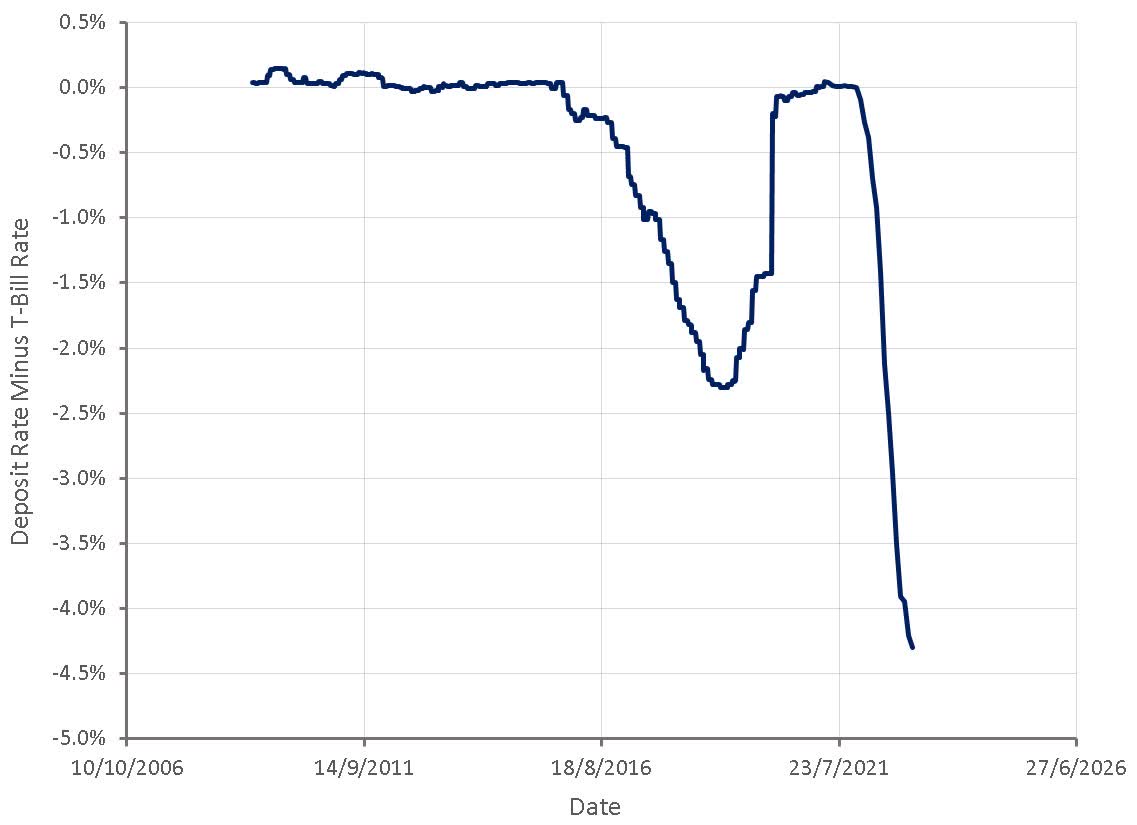

Short-term interest rates have risen by close to 5% over the past 12 months as the result of aggressive monetary policy. For bank deposits to be an attractive destination for savers, interest rates offered by banks should be similar to the yield on risk-free short-term securities. In general, banks have so far not had to offer significantly higher yields to retain deposits though, likely due to the complacency of savers. This has insulated banks somewhat from the current interest rate environment.

Figure 1: Interest Rate on Deposits Minus 3 Mo. Treasury Bill Yield (source: Created by author using data from The Federal Reserve)

{kind=link}

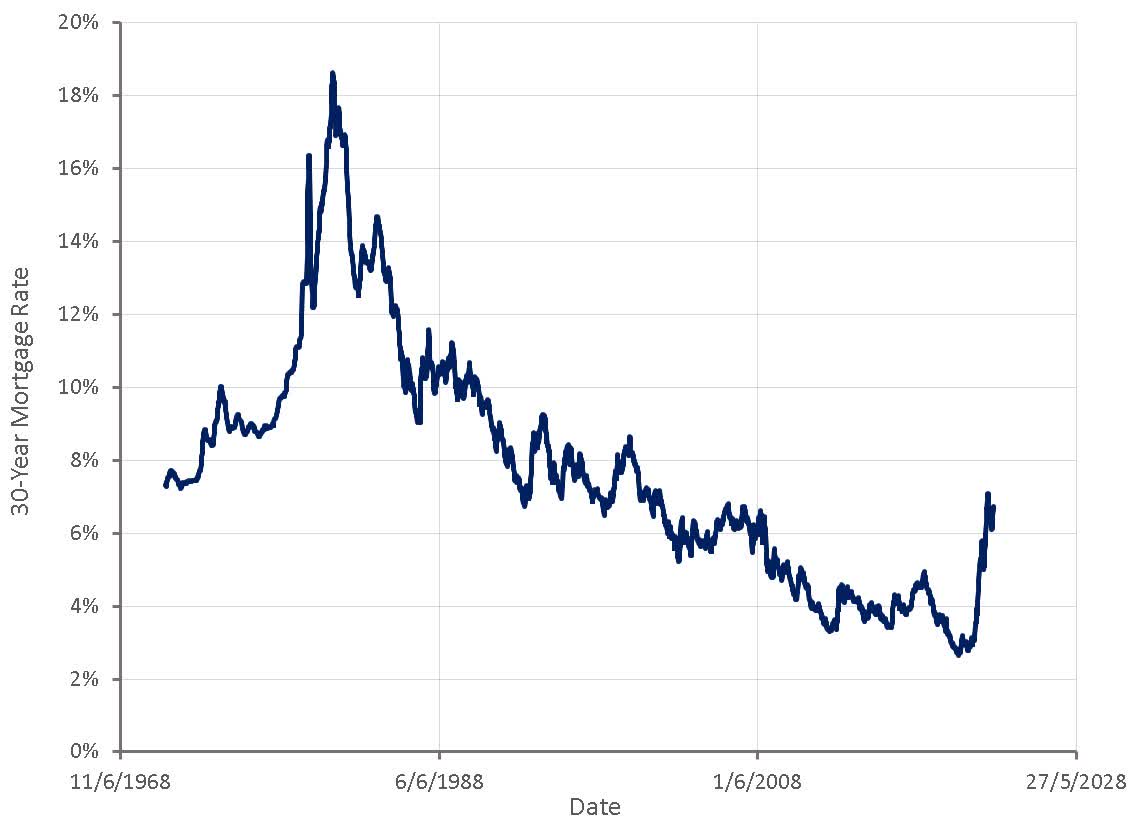

Banks in the US have averaged a net interest margin of 3.5% over the past 20 years , and with short-term interest rates near 5%, a 30-year mortgage rate of closer to 9% would likely be necessary for savers to earn a reasonable return and banks to earn a reasonable profit. This is problematic though, as lending has already collapsed with far lower rates. If depositors do begin to demand better returns, banks may be forced to bare lower net interest margins or face a complete collapse in lending volumes.

This is a concept that applies across all sources of financing for banks (wholesale deposits, retail deposits, debt and equity). If the cost of capital adjusts to current interest rates, asset prices and lending will collapse.

Figure 2: 30 Year Mortgage Rate (source: Created by author using data from The Federal Reserve)

{kind=link}

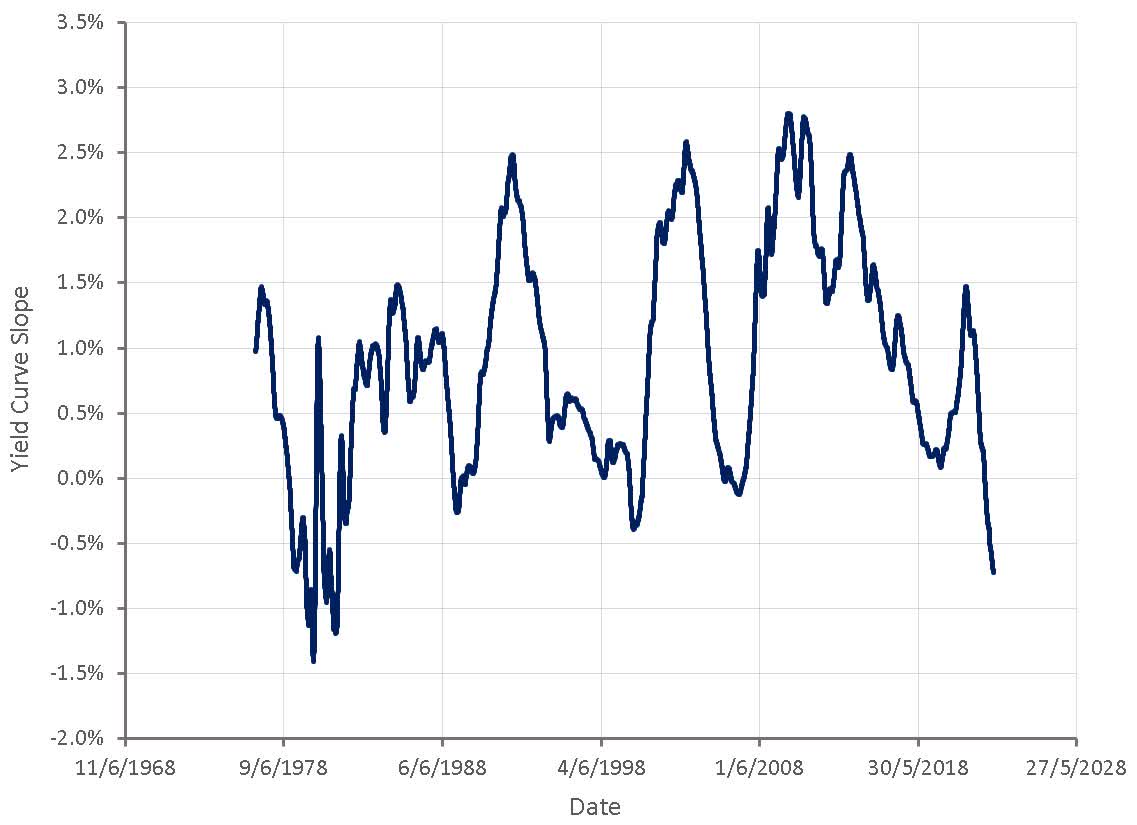

This is part of the problem of having a severely inverted yield curve for an extended period of time. Banks often have long-duration assets and short-duration liabilities, meaning a rise in interest rates will cause the banks equity to decline.

Unrealized losses at banks are largely the result of a large number of people locking in low-rate and long-term mortgages. This has hampered the ability of the Fed to implement monetary policy, as higher rates create an elevated risk of a banking crisis, and they are less effective as most mortgage holders are insulated. The flip side of this is that a decline in interest rates may not provide much stimulus, as little debt has been taken out at current interest rate levels.

It is also difficult for a bank to operate profitably when their cost of financing rises at the same time as their source of income is flat or declining.

Figure 3: Yield Curve Slope (source: Created by author using data from The Federal Reserve)

{kind=link}

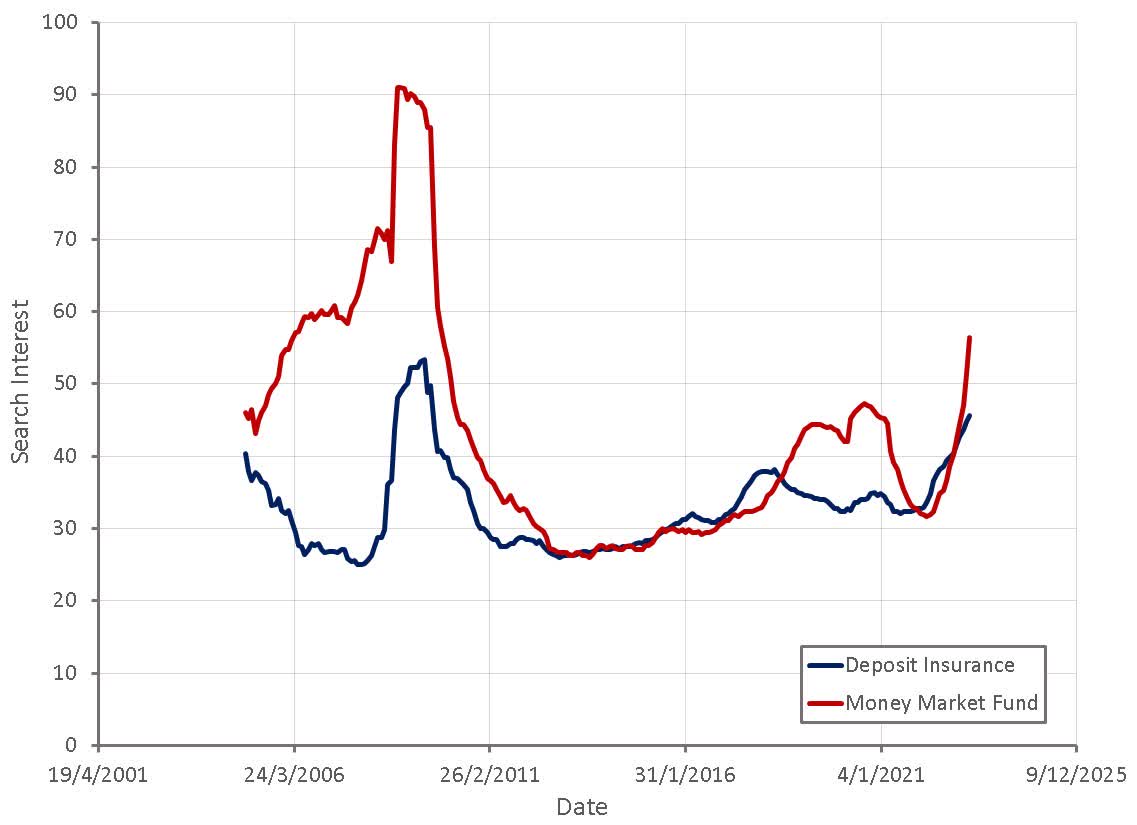

The unknown is when and to what extent savers will demand better returns, causing financing costs for banks to rise. Savers have been complacent, but awareness of the fact that deposits are not risk-free and that far better returns are available elsewhere appears to be rising. This could be sufficient for banks to tighten lending standards further, accelerating the timeline for a recession.

Figure 4: "Deposit Insurance" and "Money Market Fund" Search Interest (source: Created by author using data from The Federal Reserve)

{kind=link}

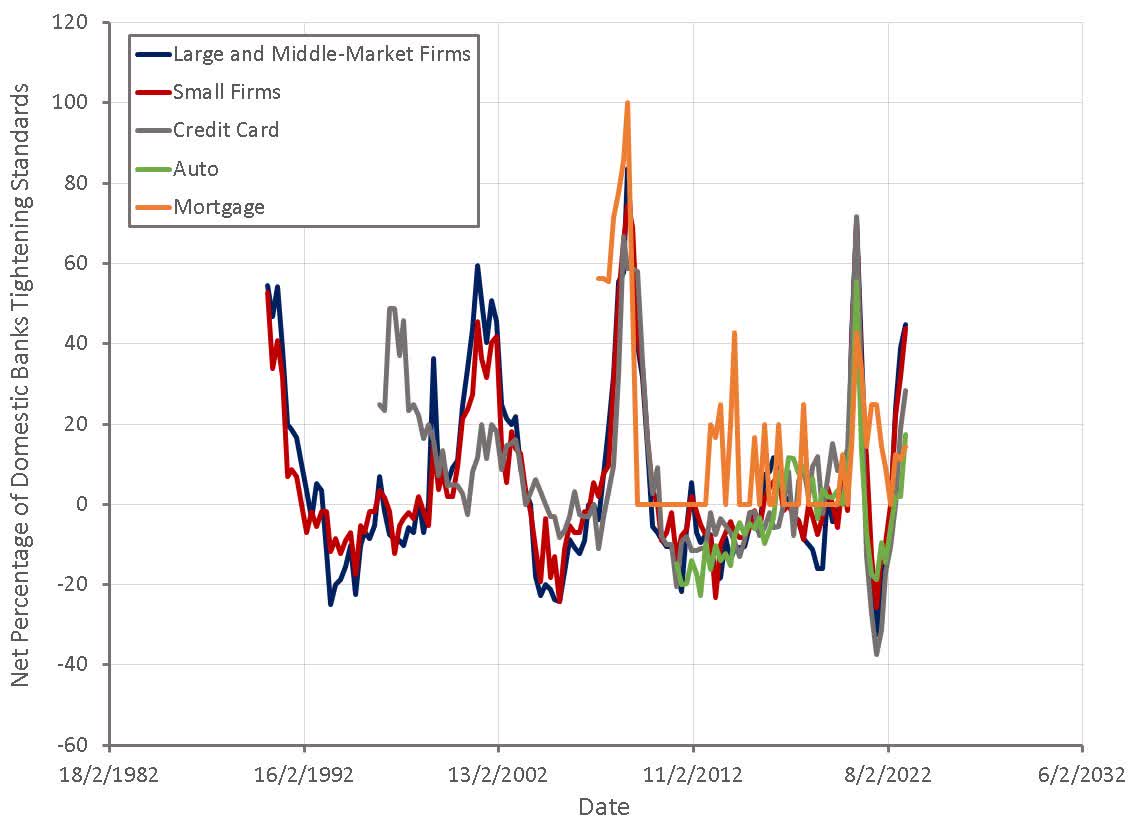

While indices of financial conditions generally show that financial conditions are still loose and have loosened in recent months, they are not really measuring anything relevant for the current situation. Banks are tightening lending standards to an extent that is generally only observed during recessions. Many parts of the economy, like real estate, do not function without access to financing.

Figure 5: Net Percentage of Banks Tightening Lending Standards for Different End Markets (source: Created by author using data from The Federal Reserve)

{kind=link}

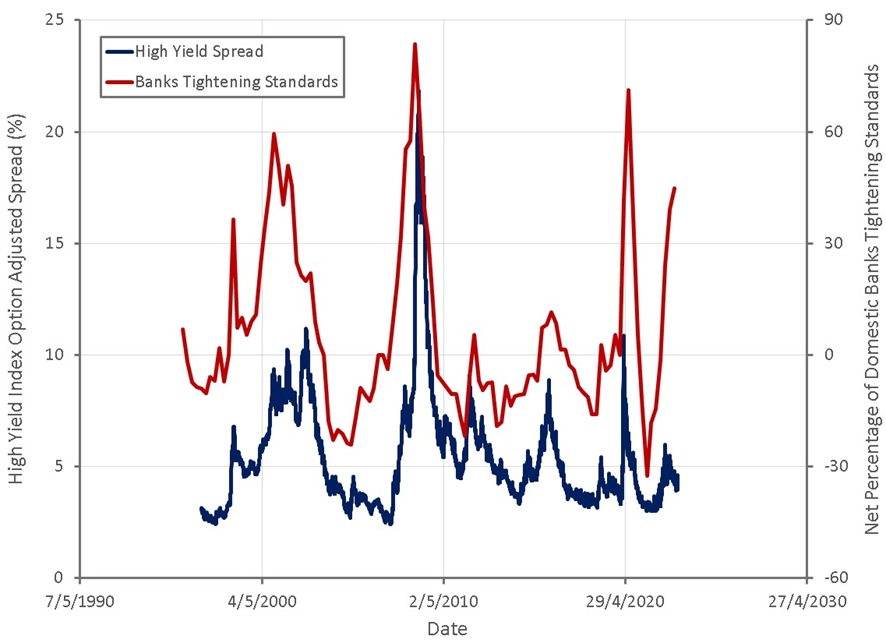

A rapid tightening in lending standards is generally followed by a rise in credit risk, albeit with a sizeable time lag. With banks set to continue tightening standards, it seems likely that defaults and rising credit spreads will follow.

Figure 6: Tightening Lending Standards and Credit Risk (source: Created by author using data from The Federal Reserve)

{kind=link}

The rapid rise in interest rates over the past 12 months is beginning to cause parts of the economy to seize. For example, the housing market likely needs a combination of significantly lower home prices and significantly lower interest rates before activity returns to healthy levels. The pension fund issue in the UK in 2022 and problems with a number of small banks in the US are both the result of an unexpected and rapid rise in interest rates. These types of issues are likely to be ongoing and potentially more severe as the impact of higher rates works its way through the economy.

For further details see:

Interest Rates Aren't Sustainable At Current Levels