WINN - Interest Rates Currency Risks Whipsaw WINN Softer Performance Likely

2023-09-22 02:19:56 ET

Summary

- WINN, an actively managed growth-centered fund, may experience more softness going forward as the higher-for-longer narrative is clearly entrenching in the market.

- Harbor Long-Term Growers ETF has an outstanding growth profile, with an over 21% weighted-average forward EPS growth rate, which is why it is so vulnerable now.

- A few indicators reveal an acute valuation problem, which exposes it to the growth premia issue amid the market factoring in a higher cost of capital.

Harbor Long-Term Growers ETF ( WINN ), an actively managed growth-centered fund, may experience more softness going forward as the higher-for-longer narrative is clearly entrenching in the market.

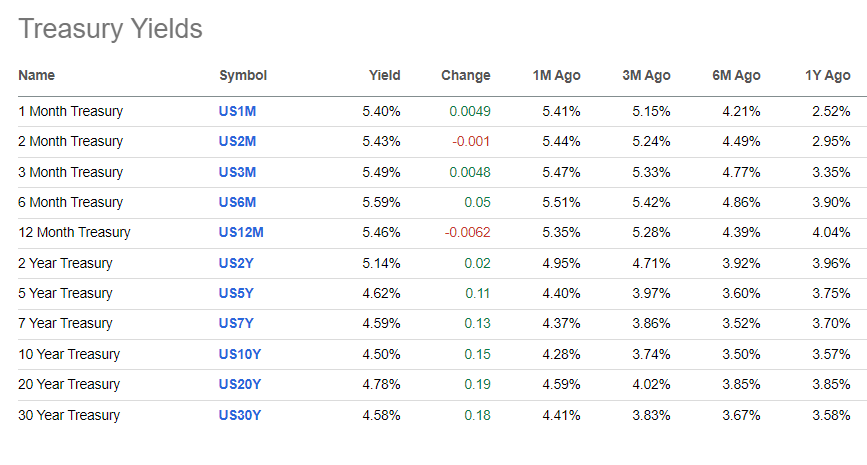

The most recent Fed interest rate decision announced on September 20 was momentous. At first glance, nothing meaningful happened as the regulator simply opted for a pause once again. However, the gist is that:

the Federal Open Market Committee members indicated rates will stay higher for longer in their summary of economic projections.

In my understanding, the markets are at a point where they need assurance that there is a clear path to the first interest rate cut in early 2024 after a record streak of increases. And they have not received one. Contrarily, the higher-for-longer scenario is now more realistic than ever. And I believe the landing can finally turn out to not be that soft.

Unsurprisingly, long-duration equities stumbled, while Treasury yields crept higher.

{kind=link}

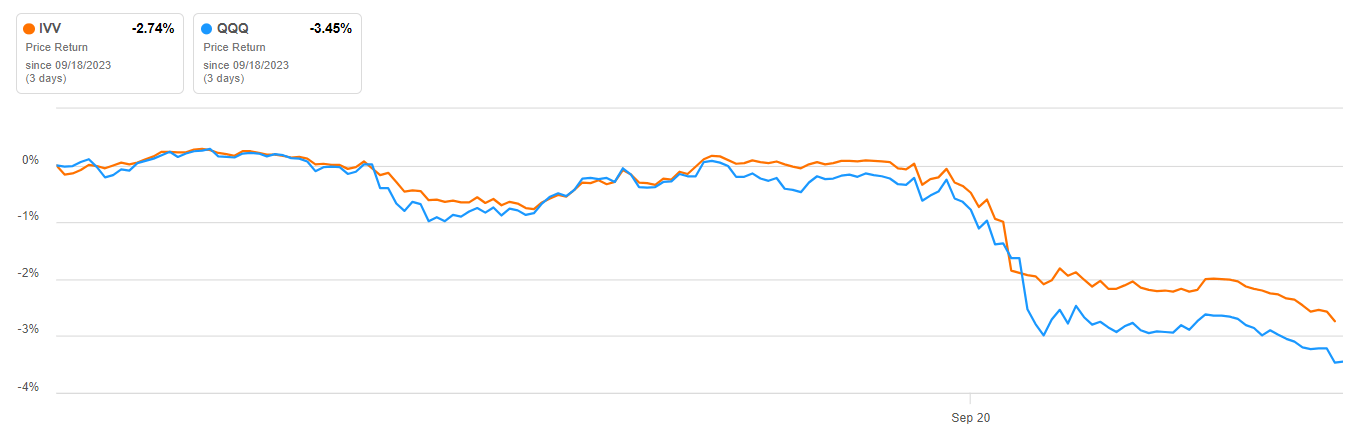

To corroborate, we saw both the Invesco QQQ ETF ( QQQ ) and iShares Core S&P 500 ETF ( IVV ) declining on September 20 and September 21 (as of writing this article).

{kind=link}

Increasing skepticism towards long-duration equities is even more noticeable when it comes to the ARK Innovation ETF ( ARKK ), which favors speculative growth names; ARKK declined by more than 3% on September 21, delivering a negative 5-day price return of 6.7%.

Brent price is also negatively reacting to the decision and the outlook, with traders reassessing the supply-demand balance, yet it is questionable whether petroleum benchmarks will embark on a sustainable downward trend, going low enough to remove the oil price-related inflation risks, especially assuming supply remains tight .

Furthermore, when it comes to growth-heavy WINN, almost all its basket was in the red on September 21, with the most afflicted stock being Snowflake ( SNOW ), which declined by more than 6%. Just three names eked out gains (more on that shortly).

In addition, growth portfolios that not only seek opportunities in the U.S. but also venture overseas are even more vulnerable now, as the hawkish outlook is a factor of paramount importance for FX markets since U.S. dollar appreciation is in the cards. As a refresher, as mentioned in the summary prospectus , WINN:

may invest up to 20% of its total assets in the securities of foreign issuers, including issuers located or doing business in emerging markets.

Among the most notable non-U.S. companies in its portfolio is LVMH Moët Hennessy - Louis Vuitton ( LVMUY ), represented by the unsponsored ADR with a 1.2% weight.

A Quick Strategy Recap

In the strategy profile document says, WINN is described as:

an actively-managed Fund that offers exposure to Jennison's flagship large cap growth strategies, as well as an expanded investment opportunity set sourced across Jennison's other growth strategies. The Fund employs a proprietary combination of bottom-up, fundamental research and systematic portfolio construction.

Regarding the objective, the document says that the ETF:

seeks long-term growth of capital by investing in large- and mid- capitalization companies, primarily in the US, that have compelling prospects for long-term growth.

According to its website , it is benchmarked against the Russell 1000 Growth Index.

How The Portfolio Has Changed

The first time I reviewed the ETF was in May, when I arrived at the conclusion that:

as most of its holdings are priced at a sizeable premium to their respective sectors, with the ETF's earnings yield at just 2.3% and debt-adjusted yield (EBITDA/EV) at 2.9%, I believe WINN is only a Hold.

In fact, little has changed since then, especially amid the more hawkish interest rate outlook. Let us look at the data.

As of September 20, WINN had a portfolio of 67 holdings, compared to 75 as of May 30. Among the additions, I have spotted Becton, Dickinson and Company ( BDX ), MongoDB ( MDB ), ServiceNow ( NOW ), HubSpot ( HUBS ), and Bristol-Myers Squibb Company ( BMY ).

| Stock |

| Weight |

| BDX |

| 0.9% |

| MDB |

| 0.7% |

| NOW |

| 0.3% |

| HUBS |

| 0.2% |

| BMY |

| 0.9% |

Created using data from WINN

There were more stocks removed than added as the ticker comparison revealed, 13 in total, with the most notable being Schlumberger ( SLB ), an energy sector bellwether, which had about 1.27% weight in May and was one of the top contributors to the fund's weighted-average earnings yield as it sported an EY of 6.1%, as per my calculations back then.

Nevertheless, perhaps the most remarkable fact here is that BMY is the only adequately valued stock in the entire WINN portfolio, with a C+ Quant Valuation grade. Hardly surprising, the stock was one of the three names that eked out a gain on September 21 (as of writing this article), rising by 51 bps; the other two were UnitedHealth Group ( UNH ) and Vertex Pharmaceuticals ( VRTX ). As I said above, the rest was in the red, with a median decline of 2.48%. In my view, this once again brilliantly illustrates that investors should take valuations seriously in this environment.

Portfolio-wise, WINN still does not deliver on the valuation front; in fact, the changes mentioned above were minor, and the basket is still dominated by Microsoft ( MSFT ), Apple ( AAPL ), and NVIDIA ( NVDA ), with the trio accounting for over 28% of the net assets (about 30.4% in May). The table below offers a bigger story, with the key factor parameters compared.

| Metric (weighted-average) |

| May |

| September |

| Market Cap, $ billion |

| 960.48 |

| 992 |

| P/S |

| 9.94 |

| 9.87 |

| EY |

| 2.321% |

| 2.324% |

| Fwd EPS Growth |

| 17.94% |

| 21.1% |

| Fwd Revenue Growth |

| 13.95% |

| 15.8% |

| ROE |

| 40.41% |

| 54.6% |

| ROA |

| 12.49% |

| 13.4% |

| EV/EBITDA |

| 34.80 |

| 37.86 |

| Fwd EBITDA Growth |

| 13.78% |

| 17.2% |

| 3Y EPS Growth |

| 11.21% |

| 28.4% |

| 3Y FCF Growth |

| 19.94% |

| 20.5% |

Calculated by the author using data from Seeking Alpha and the fund

The essential takeaway is that WINN's growth characteristics have become even stronger, with the forward revenue, EPS, and EBITDA growth rates all rising notably. There has been an improvement in the backward-looking metrics as well, like 3-year EPS and FCF growth rates. But what has not changed is its rich valuation. The EY has not moved much as the weighted-average market cap went even higher, thanks to the $1 trillion league members. Also, neither EV/EBITDA nor P/S have become attractive enough. There is no denying that WINN holds top-notch quality stories, with about 93.5% of the portfolio having A (-/+) Quant Profitability grades. But with a low-single-digit earnings yield and all the holdings except for BMY having a D+ Valuation grade or worse, it is tough to be bullish on it.

Final Thoughts

The Federal Reserve's interest rate decision and new outlook have roiled the growth stock echelon. I believe the market has received a clear signal that the risk of a hard landing is real. In this regard, growth investors should be on high alert. Cutting exposure to overpriced names and rotating out of quality & growth, value-agnostic growth, etc. to the quality & value factor combination is a reasonable step to consider.

As discussed above, WINN has an outstanding growth profile, with an over 21% forward EPS growth rate, which is why it is so vulnerable now. In other words, the portfolio has an acute valuation problem, which exposes it to the growth premia issue amid the market factoring in a higher cost of capital.

Growth premia, inflation, and interest rates are intimately intertwined. As a reminder, WINN declined by 25.9% in 2022 amid aggressive interest rate increases. Importantly, it grossly underperformed IVV, QQQ, and the iShares Russell 1000 Growth ETF ( IWF ). Over the March 2022-August 2023 period, WINN (incepted in February 2022) also trailed these ETFs, delivering the deepest maximum drawdown in the group and the lowest risk-adjusted returns.

| Portfolio |

| WINN |

| IVV |

| QQQ |

| IWF |

| Initial Balance |

| $10,000 |

| $10,000 |

| $10,000 |

| $10,000 |

| Final Balance |

| $10,324 |

| $10,561 |

| $11,011 |

| $10,669 |

| CAGR |

| 2.15% |

| 3.71% |

| 6.63% |

| 4.41% |

| Stdev |

| 26.74% |

| 20.49% |

| 26.86% |

| 23.77% |

| Best Year |

| 39.30% |

| 18.69% |

| 42.37% |

| 32.07% |

| Worst Year |

| -25.88% |

| -11.02% |

| -22.65% |

| -19.22% |

| Max. Drawdown |

| -28.85% |

| -20.28% |

| -26.10% |

| -23.88% |

| Sharpe Ratio |

| 0.08 |

| 0.11 |

| 0.24 |

| 0.15 |

| Sortino Ratio |

| 0.12 |

| 0.16 |

| 0.36 |

| 0.22 |

| Market Correlation |

| 0.91 |

| 1 |

| 0.92 |

| 0.96 |

Created using data from Portfolio Visualizer

Overall, despite the fund having exceptional growth stories under the hood, I believe it is unattractive tactically; thus, at this juncture, it is a pass.

For further details see:

Interest Rates, Currency Risks Whipsaw WINN, Softer Performance Likely