SCHQ - Interest Rates Hiked Yet Again: The Danger Of Further Hikes

2023-03-23 07:15:00 ET

Summary

- The Federal Reserve went forward with a 0.25% interest rate hike on March 22nd, despite weakness in the banking sector.

- The good news is that the Federal Reserve is forecasting only one additional hike for this year, but their language has been somewhat ambiguous.

- Further increases should be met with caution since the financial system seems to be more fragile than the Federal Reserve would like you to believe.

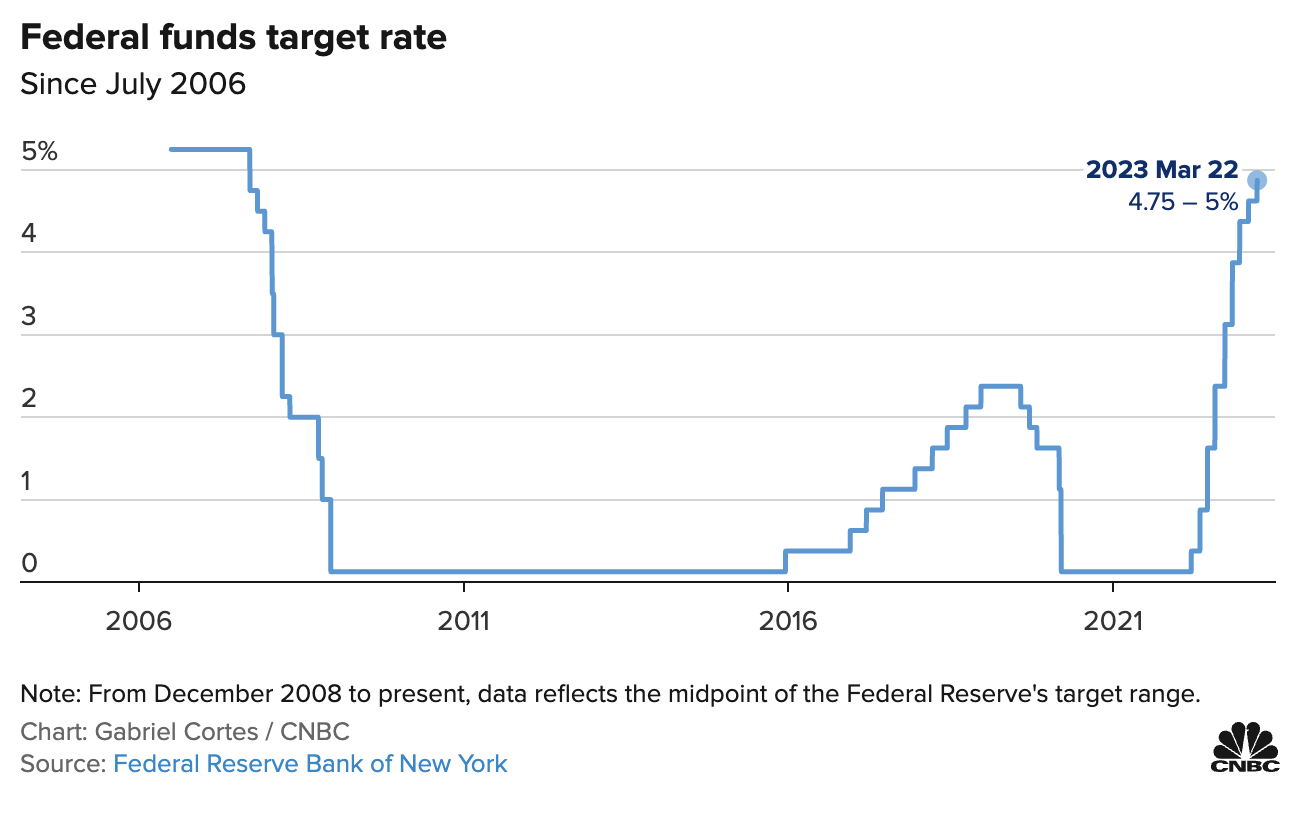

On March 22nd, the Federal Reserve announced that it was raising interest rates yet again. This time, the rate increase was a modest 0.25%, matching the rate increase seen on February 1st of this year and coming in far lower than the rate increases experienced in the second half of 2022. Initially, markets responded with optimism. But this optimism quickly faded when it became clear that further action by the Federal Reserve might be needed before interest rates reached their peak. All things considered, I believe that there is some ambiguity that is likely confusing market participants. But on the whole, I see recent developments as a net positive. This is not to say that everything is great. It is clear that certain aspects of our banking system are susceptible at this time. And when you really dig into the data, it becomes clear that this is an area investors should continue to watch out for.

Another rate hike from Fed

The 0.25% interest rate hike announced by the Federal Reserve on March 22nd may have caught some market participants by surprise. The general sentiment leading up to this prior to the collapse of certain financial institutions like SVB Financial Group's ( SIVB ) Silicon Valley Bank and Signature Bank ( SBNY ) was that additional interest rate hikes that were of a meaningful magnitude might be in store. But once the financial system started showing significant weakness, the prospect of a smaller hike, or even no hike at all, became very real. Even so, viewing the broader banking system as ‘sound and resilient’, the Federal Reserve went forward with a 0.25% rate hike, taking the target range for rates to between 4.75% and 5%.

{kind=link}

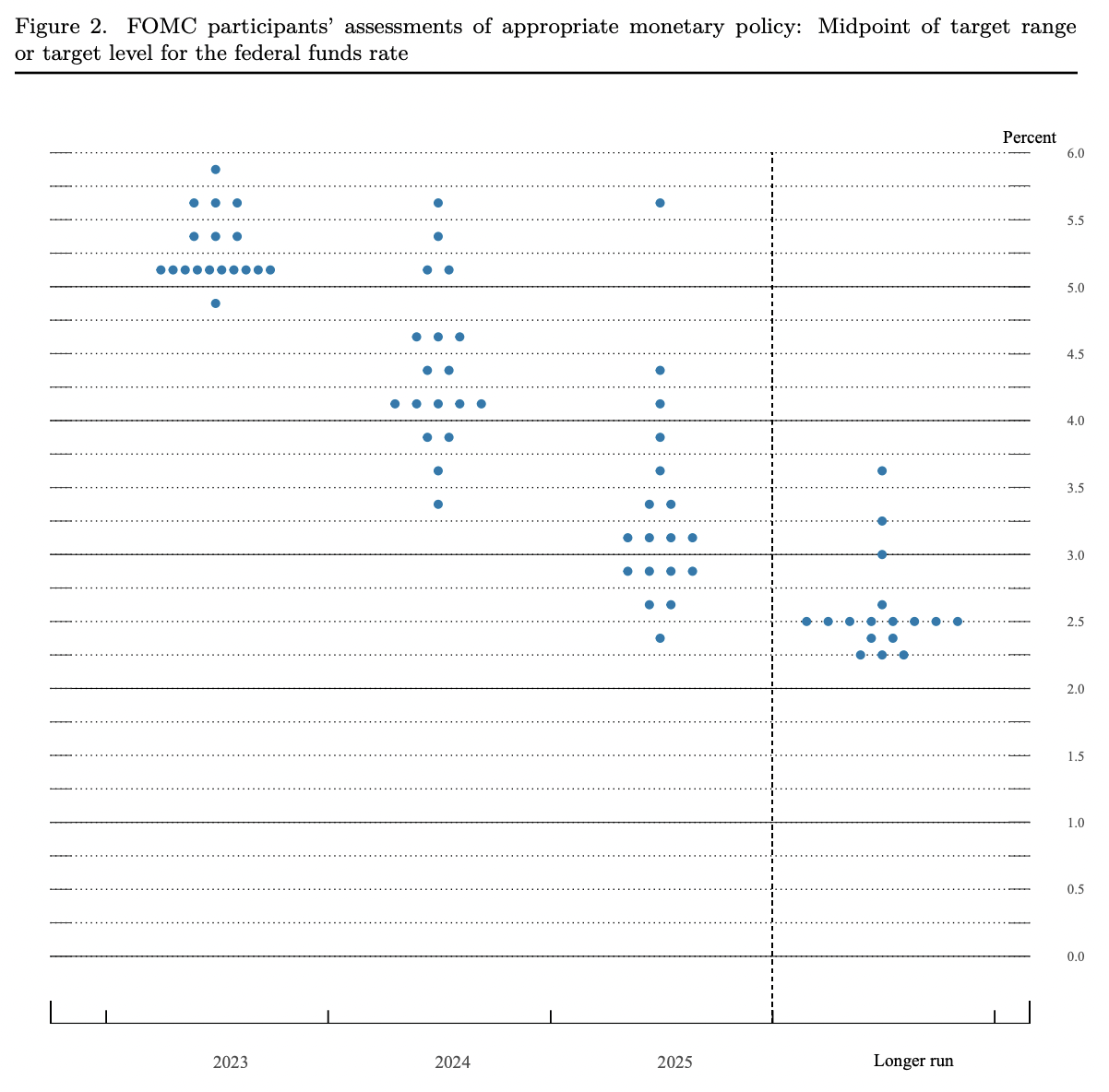

In a sense, seeing these rate increases continue is painful for investors. Even though inflation does need to be dealt with, rate hikes weaken consumer spending and reduce the willingness of companies to make investments. The good news from the meeting that the Federal Reserve had is that we may very well be near the end of rate hikes. The dot plot provided by the bank showed a general consensus for hikes eventually reaching between 5% and 5.25% sometime this year. From there, the expectation is for a decline in the rate to somewhere around 4% to 4.25% by the end of 2024 before dropping further to around 3% to 3.25% in 2025. The ultimate goal of the Federal Reserve is to have interest rates somewhere around 2.5% per annum.

{kind=link}

The fact that the Federal Reserve is pointing to only one additional rate hike this year is a net positive for investors. But not everything was perceived by the market in a bullish way. Some of the language used in their official statement was a bit ambiguous. Previously, the Federal Reserve said that the committee anticipates that ‘ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time.’ However, their most recent statement removed part of that and stated instead that ‘some additional policy firming’ may be appropriate. In a separate statement, Federal Reserve Chairman Jerome Powell stated that ‘financial conditions seem to have tightened, and probably by more than the traditional indexes say.’ While this is still very open-ended in terms of interpretation, it makes me feel as though they are leaning more in the direction of not pushing rates up much further from here and potentially easing them early next year.

A cut is likely before year-end

Although this is the official stance of the Federal Reserve, I do believe that a more likely scenario is a cut to the interest rate before the year is out. In fact, I wouldn't be surprised if they forgo the next rate hike entirely and take a wait-and-see approach instead. Despite Powell’s statement that the US banking sector is strong, there are some meaningful signs of weakening that investors should be aware of. And frankly, some of these signs have been developing for several months. As I highlighted in a prior article , a lot of the troubles that we have seen in the banking sector recently were caused by banks that were most exposed to companies that were the most susceptible to funding shortfalls. These were largely startups and other early-stage companies. As interest rates rose, it became more difficult to raise capital. Even so, these financial institutions needed the cash in order to keep operating since many of them operate at losses for many years. This eventually led to a drawdown of their deposits.

{kind=link}

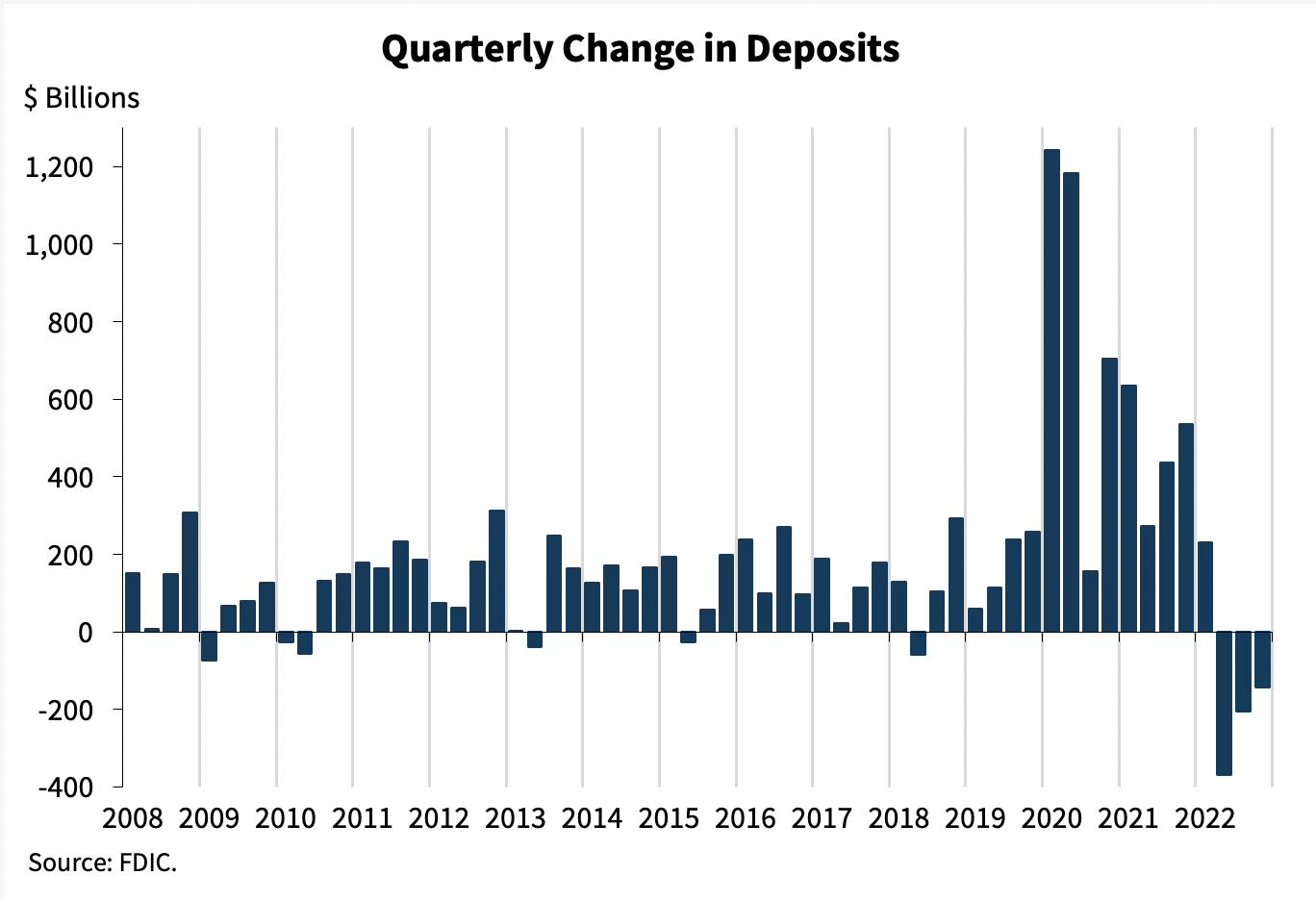

The common thought process here is that the bank runs that were ultimately experienced occurred in a relatively short period of time. But I would make the case, after reviewing the evidence further that, they were months in the making. Instead of a sudden panic that created a mass exodus of capital from accounts, we actually saw deposits in the banking sector decline over the course of three quarters last year. As you can see in the chart above, the decreases seen in the second, third, and fourth quarters of 2022 were far larger than any other dating back to at least 2008. To be clear, not all of this weakness was driven by the tech industry. A large portion of it was almost certainly driven by the average depositor looking for attractive returns elsewhere.

{kind=link}

You see, as interest rates rose, the search for yield began. Those who have deposits began drawing them down, taking that capital and instead allocating it to treasury bills and other investment opportunities. This outflow caused banks, particularly the community banks that are both more susceptible to recent pain and less stable than their larger national counterparts to begin offering more attractive returns on those willing to keep their money in the bank. This is why, even as deposits shrank by $278 billion in 2022, representing the first annual decline in deposits since 1948, there was a surge in bank products such as CDs. CDs specifically saw total contributions climb from $1.49 trillion to $1.7 trillion over the course of one year. Where it was once nearly impossible to find opportunities in the banking sector yielding 4% or 5%, you can now find many such prospects.

{kind=link}

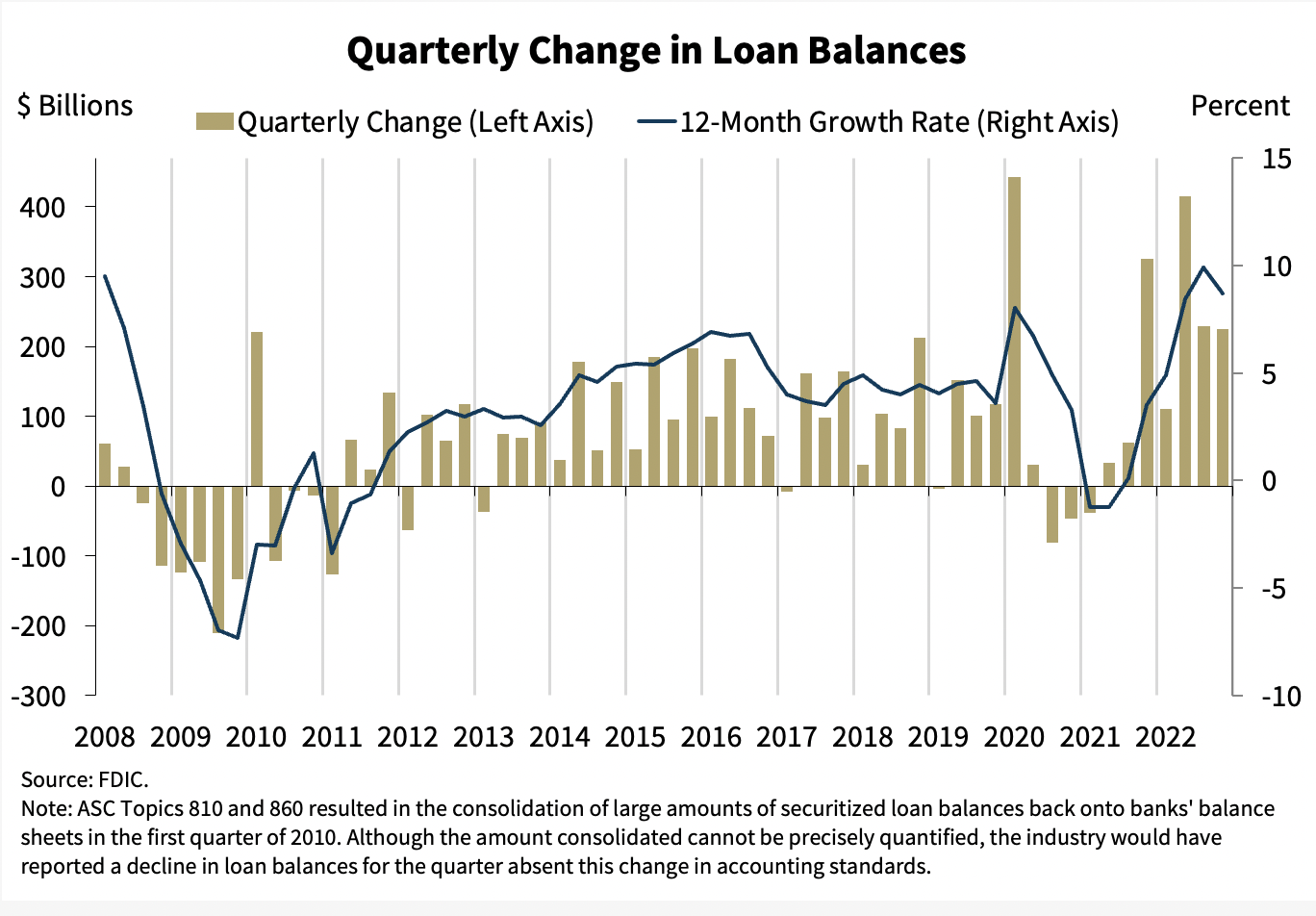

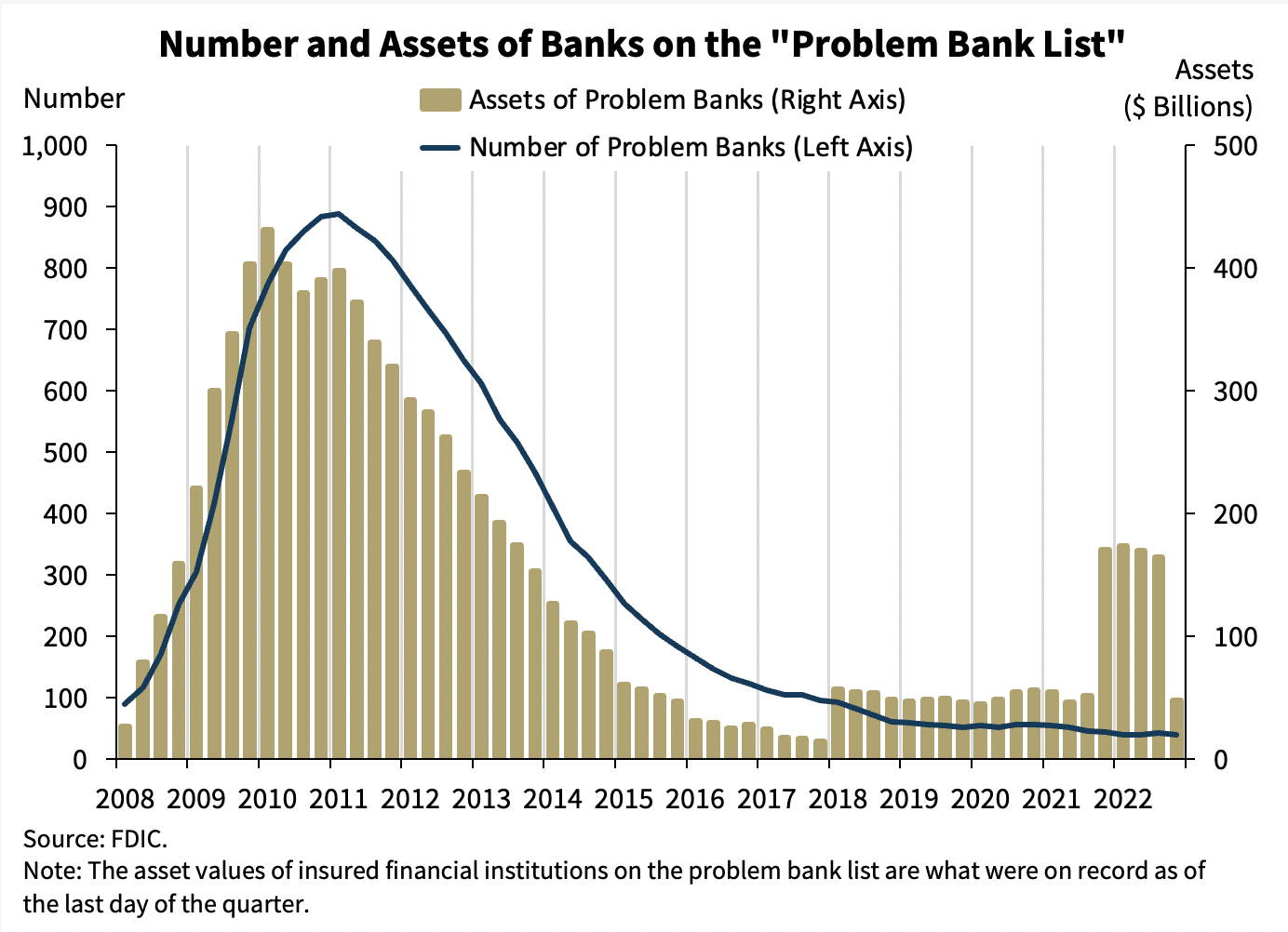

The search for stronger returns ultimately led banks to become more aggressive as well. 2022, for instance, saw significant growth in loan balances. But this has also had some negative side effects as well. For starters, we have seen loan loss provisions begin to rise and, while the number of ‘problem banks’ reported by the FDIC is still low, the value of the assets that are held at these institutions remained elevated for much of last year. Although this asset value did decline in the final quarter of last year, we now know that a collapse of the most exposed banks may have been inevitable.

{kind=link}

Takeaway

From what I can see, it's good that the Federal Reserve is thinking about not raising interest rates all that much compared to where they are today. However, I think that the data that's available on the market at the moment suggests that any further rate increases could prove painful for the financial sector. Already we have seen a rise in interest rates over the past year result in bank deposits falling, bank loans rising as banks looked for opportunities, loan loss provisions rising, and the value of assets held at problem banks increasing. A continued increase in the interest rate will only exacerbate this trend and increase the likelihood of additional pain in the banking sector. This, in turn, brings with it additional risk of a spillover into the broader economy.

For further details see:

Interest Rates Hiked Yet Again: The Danger Of Further Hikes