TILE - Interface Inc.: Extremely Cheap At Current Prices

Summary

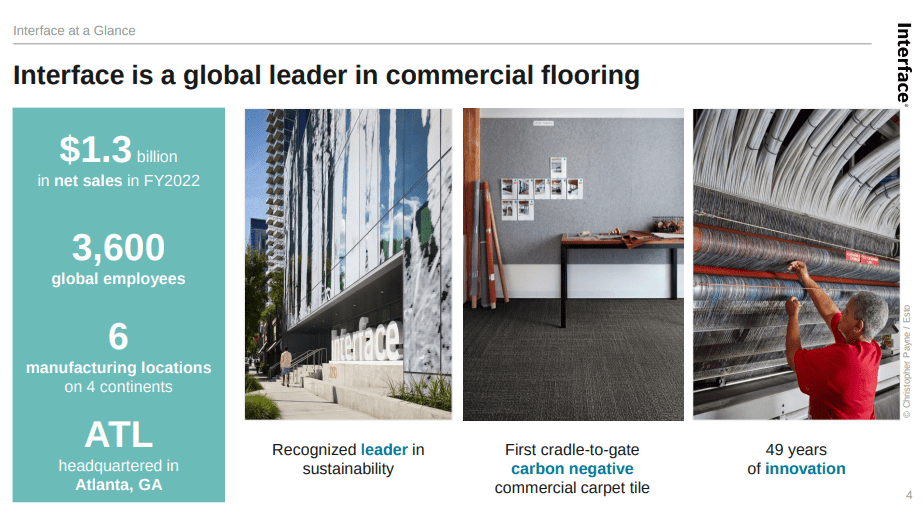

- Interface is a global leader in the commercial flooring, with a reputation for sustainability practices.

- Interface delivered decent results for FY2022 and expects some growth in FY2023.

- Shares are trading at an extremely low valuation, the EV/Revenues multiple is close to what it reached during the worst of the Covid crisis.

Interface Inc ( TILE ) is a leading manufacturer of modular carpets and flooring solutions that is known for its innovative and sustainable products. Some of its major competitors include Mohawk Industries ( MHK ), and Berkshire Hathaway's ( BRK.A )( BRK.B ) Shaw Industries. While this is a low-growth company, and its financials are not particularly attractive, we still like the company for a number of reasons. These include the fact that Interface is considered a sustainability leader with some of the most environmentally friendly flooring products.

The company is also trading with an extremely cheap valuation despite recently delivering good results for FY2022, and providing solid guidance for FY2023. In 2022 its currency neutral sales grew ~13%, and its adjusted operating income increased ~8%. These are not bad results considering the significant headwinds the company experienced during the year, including significant raw material inflation and foreign currency exchange impacts.

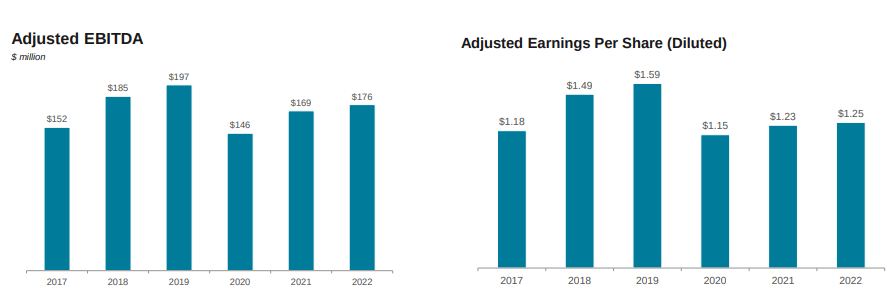

During the most recent earnings call, the CEO Laurel Hurd shared that they do not see signs of softening in the business, but that they are aware the economy could potentially weaken during 2023. In FY2022, the company delivered adjusted earnings per share of $1.25. Given that shares are currently trading at ~$8.82, that puts the trailing twelve months p/e ratio at ~7x. Even though Interface is a low-growth company, we believe this multiple to be unsustainably cheap. The company appears to think so too, as they announced a $100 million share repurchase program in May of last year. In 2022, they repurchased ~$17.2 million, which means there is a significant amount left in the share buyback authorization.

Interface Investor Presentation

{kind=link}

Q4 and FY2022 Results

Fourth quarter net sales were $335 million, a decrease of ~1.2% when compared to Q4 2021. Adjusting for currency impacts, growth was 3.6% y/y. Q4 adjusted gross profit margin was ~33.2%, a decrease of 294 bps from the previous year. This was mainly the result of higher raw material and labor costs, partially offset by higher pricing. For Q4 2022 adjusted operating income was $32 million, down ~22% compared to Q4 of 2021. For Q4 2022 adjusted EPS was $0.31 compared to $0.47 in Q4 of 2021.

For the full year 2022 consolidated net sales were $1.3 billion, up ~8%, compared to $1.2 billion in the previous year. Adjusting for currency impact, growth was ~13%.

In 2022 adjusted gross profit margin was 34.7%, a decrease of 184 bps from the previous year due to higher raw materials, freight, and labor costs, partially offset by higher pricing. Adjusted operating income for 2022 was $132 million, up ~8.3%, compared to the previous year. In 2022 adjusted earnings per share were $1.25, compared to $1.23 in 2021. During the earnings call, the company shared that it has a goal to return its gross profit margins back to pre-Covid levels of ~38%.

Financials

Interface operated in a highly competitive industry, which is reflected in relatively low operating margins. Over the past ten years, the company has averaged operating margins of approximately ~9.5%, very close to the ~10% average that Mohawk Industries has delivered. While this is clearly not the most attractive of industries, it is far from the worst. What we have with interface, in terms of financial performance, is a relatively average company trading at an extremely low valuation.

In terms of returns on capital employed, the average over the past ten years has been ~10.8%, very close to its competitor Mohawk Industries.

The company was clearly very significantly impacted by Covid, as its adjusted EBITDA and adjusted earnings per share have yet to recover to 2019 levels. The company is talking about FY2023 as a transition year, so earnings are unlikely to post new records any time soon.

Interface Investor Presentation

{kind=link}

Growth

Interface is not a high-growth company, as can be seen in the graph below, its average quarterly y/y growth rate has been only ~4.2%. Based on guidance provided by the company, this is not expected to drastically change any time soon. Still, a low-growth company can deliver good returns for investors if bought at a low enough valuation.

Competitive Advantages

Interface differentiates itself from its competitors by offering unique and sustainable products that are designed to reduce the environmental impact of commercial buildings. The company has some strong brands, including Interface, nora, and FLOR. Interface's modular carpet tiles offer several advantages over traditional flooring solutions. They are easy to install, maintain, and replace, which makes them a good option for commercial spaces where frequent renovations are required.

Interface Investor Presentation

{kind=link}

Balance Sheet

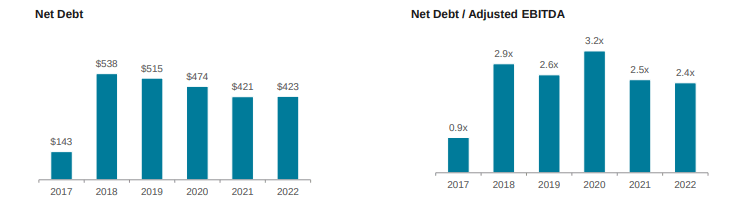

The balance sheet is in decent shape, ending the year with ~$372 million in liquidity, having ~$97 million in cash and investments and $274 million of revolver capacity. Net debt was ~$422.6 million at the end of the year, resulting in a net leverage ratio of ~2.4x. The company is targeting a net leverage ratio of ~2x.

Interface Investor Presentation

{kind=link}

Guidance

The company sounded optimistic in the earnings call about the current quarter, saying that demand has remained strong. Still, given the weakening economy and macroeconomic uncertainty, they are cautious about 2023.

For Q1 2023 they expect net sales between $290 million and $305 million, with an adjusted gross profit margin of ~34%. For 2023 they guided for y/y net sales growth of roughly 1% to 5%, with an adjusted gross profit margin of ~35%. The adjusted gross profit margin guided for 2023 is very close to what the company delivered in 2022.

Valuation

The reason why we think value investors should pay attention to Interface is that the valuation is extremely low. The company is trading with an EV/Revenues multiple of almost half its ten-year average, and very close to the levels it traded at during the worst of the Covid crisis. This multiple is also very close to that of Mohawk Industries, which is trading with an EV/Revenues of ~0.74.

While the company pays an extremely low dividend of only $0.01 per share per quarter, it has been buying back significant amounts of shares, resulting in a net common payout yield of ~2.4%. Importantly, the company still has significant amounts remaining on its stock repurchase authorization.

Looking at the forward EV/EBITDA, its shares, and those of Mohawk Industries, are trading with a very low multiple of roughly 6x. Despite the low growth and unattractive profit margins, we believe the valuation multiples to be extremely low.

We therefore agree with Seeking Alpha's valuation grade of 'A'. Note that the trailing twelve months GAAP p/e is quite high at ~26x, but this is mostly the result of the company taking some goodwill and intangible assets impairment charges.

Seeking Alpha

Risks

The main risk we see with Interface is that its sales are highly correlated with activity in the construction industry, which in turn can be significantly impacted by a recession. The company's Altman Z-Score is also below the 3.0 threshold. We therefore hope the company further strengthens its balance sheet.

Conclusion

Despite delivering solid Q4 and 2022 results, Interface shares are trading at valuation levels close to those seen during the worst of the Covid crisis. While we are not particularly impressed with the company's growth or profit margins, we still find the current valuation to be extremely low. At least, the company is taking advantage of the attractive prices to repurchase shares. While we believe there are significant risks, including a recession potentially arriving soon, we believe that at these prices shares certainly deserve some consideration.

For further details see:

Interface, Inc.: Extremely Cheap At Current Prices