BABWF - International Consolidated Airlines: Incredibly Cheap Airline With A Good Business Model

2023-12-02 07:42:00 ET

Summary

- IAG’s revenue has grown well during the last decade despite fierce competition, with a CAGR of +4%. EBITDA-M has materially exceeded this, at a CAGR of +10%.

- IAG operates a strong business model, owing to a highly competitive portfolio of brands, as well as key airport relationships that allow for lucrative routes.

- IAG has seen its competitive position decline, principally due to the rise of low-cost airlines such as Ryanair. The loss of market share has softened but pressures remain.

- IAG performs well relative to its peers but its lack of growth is evident. We do not see scope for improvement but nevertheless expect returns to be comparable due to high margins and a solid balance sheet.

- IAG is incredibly cheap at an NTM EBITDA multiple of 3x. Investor sentiment is low due to growth concerns and the macroeconomic environment, but we believe this is all sufficiently priced in.

Investment thesis

Our current investment thesis is:

- IAG is currently incredibly cheap, as are many other airlines, as investors fear the lasting damage from the pandemic, as well as the wider macroeconomic impact. We believe these factors are priced in, with IAG trading at 3x NTM EBITDA.

- The company is inherently attractive within the industry, owing to its strong business model that allows for outsized margins. We do think competition will restrict growth but IAG has shown an ability to achieve ~5% in spite of this historically.

Company description

International Consolidated Airlines Group S.A. ( ICAGY ), traded on the London Stock Exchange (LSE: IAG) and the Madrid Stock Exchange (BMAD: IAG), is a multinational airline holding company. Formed in 2011, IAG is the result of a merger between British Airways and Iberia. The company also owns other airlines, including Aer Lingus, Vueling, and Level. IAG operates flights to destinations worldwide.

Share price

IAG’s share price has disappointed during the last decade, principally due to the impact of Covid-19, with travel restrictions and subsequent disruptions contributing to equity raises, an elimination of revenue, and a change in the competitive landscape.

Financial analysis

{kind=link}

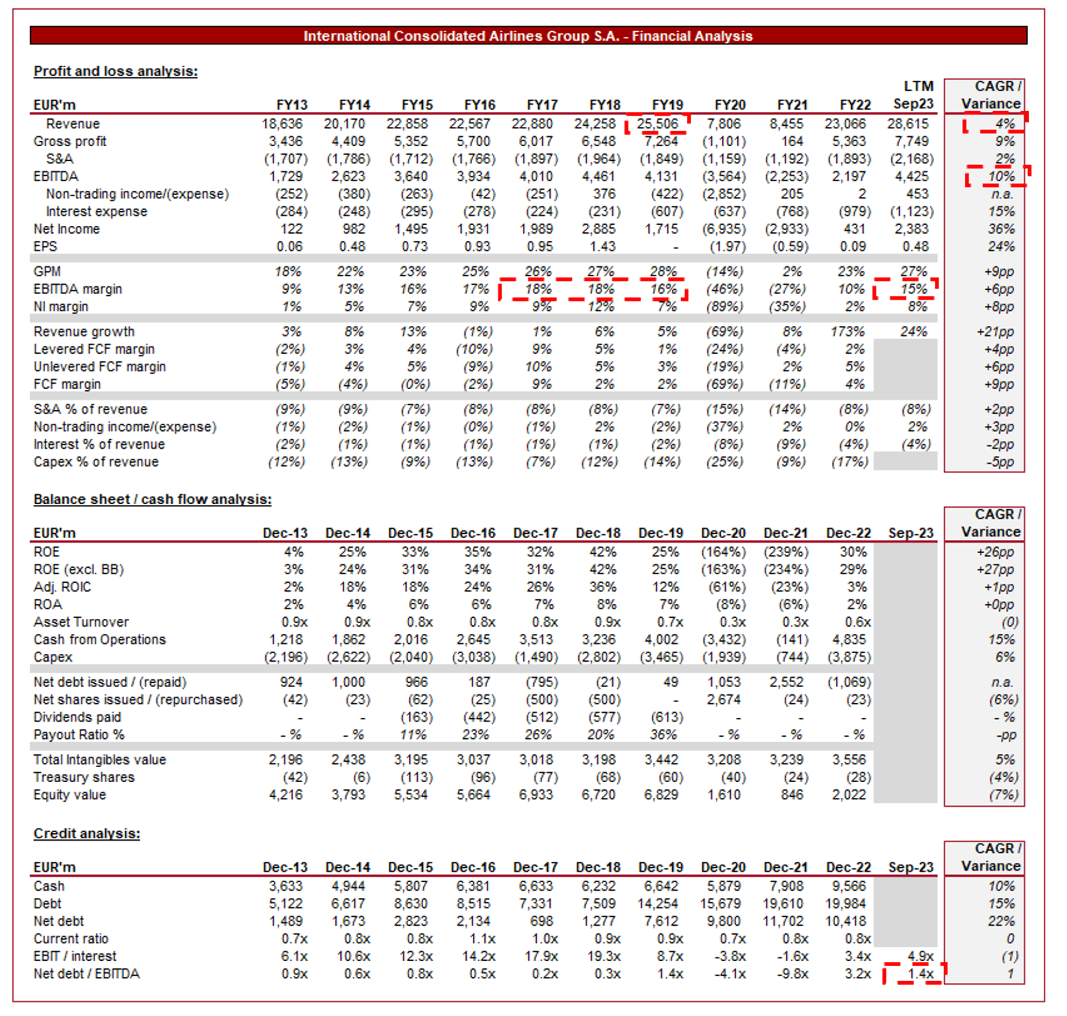

Presented above are IAG's financial results.

Revenue & Commercial Factors

IAG’s revenue has grown well, with a CAGR of +4% into the LTM period. The superior achievement is its margin growth, with EBITDA growing at a CAGR of +10%.

Business Model

IAG operates a dual business model, comprising full-service carriers (British Airways, Iberia) and low-cost carriers (Vueling, LEVEL). This allows it to cater to a broader market, targeting both business and leisure travelers. This said, there has been a noticeable shift in the quality of BA and Iberia, particularly in Europe, as consumers increasingly seek no-nonsense carriers at affordable prices ( an idea we explore in detail later ).

IAG focuses on developing a comprehensive network that connects major global destinations. This strategy is aimed at attracting a diverse range of passengers and capturing a significant share of the international travel market. Further, retaining these routes has allowed the company to develop a competitive advantage, such as BA’s route from LHR to JFK, which is one of the most traveled international routes.

The consolidation of British Airways and Iberia was designed to generate operational synergies and cost savings, particularly when partnered with its low-cost airlines. By sharing resources, including aircraft, maintenance, and support services, as well as competencies developed through market experience, IAG has improved overall efficiency.

IAG is part of the oneworld alliance, allowing it to collaborate with other major airlines like American Airlines, Qantas, and Cathay Pacific. This alliance provides benefits such as code-sharing, joint marketing, and shared airport lounges. Further, the company operates a reward system through Avios, which is incredibly popular and has an existing partnership with American Express (AXP).

Competitive Positioning

The airline industry, especially in the last decade, has faced numerous challenges, including economic uncertainties, geopolitical tensions, changing consumer behaviors, and health crises (e.g., COVID-19). The industry is notorious for being value-destructive for shareholders, with a race to the bottom on quality and prices. Theoretically, this should be a robust industry with a long runway for growth, owing to economic development globally driving greater travel.

Intense competition within the airline industry has spawned through pricing, with low-cost carriers such as Ryanair (RYAAY), gaining market share rapidly as consumer interests have trended toward affordable travel. The novelty of the airline experience has diminished, with consumers now valuing timing and price far more highly. This has impacted IAG's market share, as its brands are historically known for quality first. Its response has left the likes of BA in a middle ground, where it cannot price like Ryanair but equally does not have a market in the quality segment. This has contributed to a decline in its brand as quality has fallen, but equally has allowed it to maintain competitiveness.

The COVID-19 pandemic has severely impacted the aviation industry, with widespread travel restrictions, lockdowns, and a decline in passenger demand. This has crippled many airlines, with large amounts of debt raised and cost-cutting initiated. IAG is broadly in good shape ( discussed in detail later ), which positions it well to expand and potentially gain market share.

IAG faces competition from:

- Ryanair ((RYAAY)): The leading low-cost carrier providing competition in short-haul routes.

- Lufthansa Group ( DLAKF ): A major European airline group with a broad network of subsidiaries.

- Air France-KLM ( AFRAF ): The result of a merger between two prominent European carriers, operating in similar markets.

- easyJet ( EJTTF ) and Wizz Air ( WZZAF ): low-cost carriers focused on short-haul routes.

Opportunities

We see the following as potential growth drivers beyond a LSD rate, which represents its current opportunity based on the level of competition:

- Transatlantic Expansion - Capitalizing on post-pandemic conditions to secure lucrative transatlantic markets by expanding routes and services.

- Sustainable Aviation Initiatives - Investing in eco-friendly technologies and practices to meet increasing environmental regulations. This will also benefit the company with positive marketing.

- Strategic Alliances - Expanding and developing alliances to strengthen market presence and share resources.

Notable threats

We consider the following to be key threats to IAG in the medium term:

- Fuel Price Volatility - Fluctuations in oil prices are a risk currently following soaring prices. The company is well-hedged to mitigate this in 2024.

- Global Economic Uncertainty - The potential for an economic downturn is heightened currently, which will materially impact a discretionary industry such as this ( we discuss this topic later in detail ).

- Changing Traveler Behavior - Shifts in consumer preferences and travel patterns post-COVID-19 could potentially be negative. The shift to lower-cost airlines has already been damaging, the loss of business travel volume could also have an impact, as an example.

Margins

{kind=link}

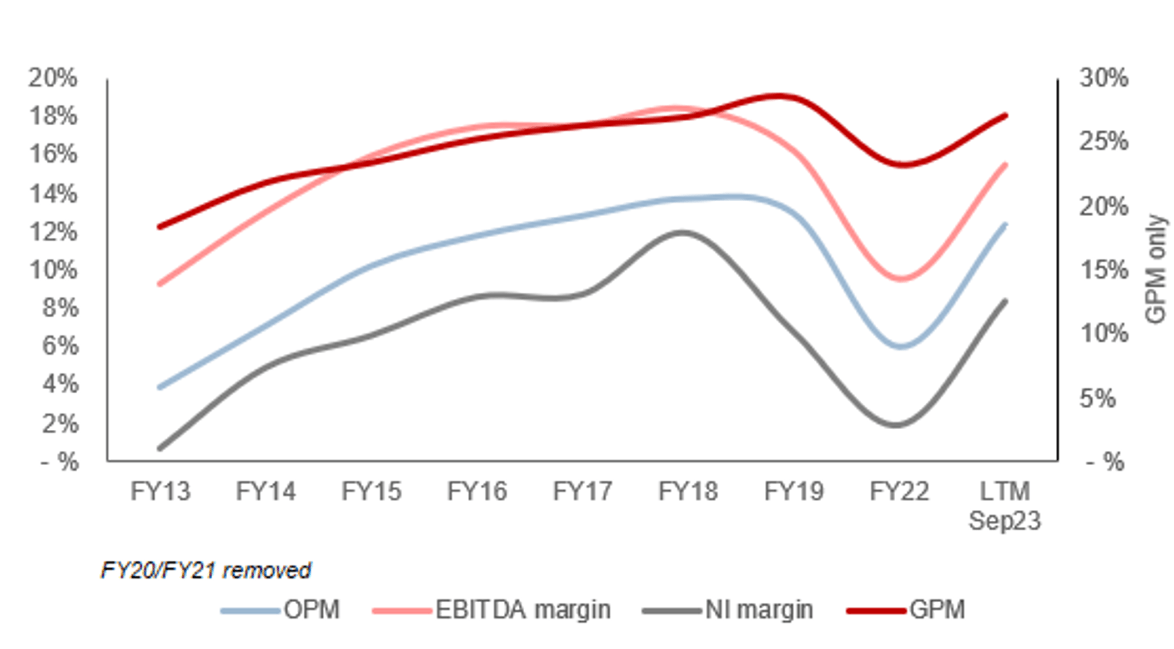

IAG’s margins have progressively improved when excluding the pandemic-impacted periods. This is a reflection of a change in approach in our view, with low-cost airlines forcing the company to cut costs to enable a decline in prices.

At a current EBITDA-M of 15%, while still ramping up following the return of travel, we believe IAG is positioned well to maintain incremental margin improvements. This should allow the company to at least reach its historical peak EBITDA-M, if not exceed it.

Quarterly results

IAG’s recent performance has been strong, with top-line revenue growth of +81%, +71%, +30%, and +18% in its last four quarters. In conjunction with this, margins have progressively improved. The broader reason for this is the ramp-up of travel returning in the post-pandemic period, with sufficient scale to achieve an impressive acceleration.

Further, inflationary price increases have also supported the business materially. With oil prices soaring, Airlines have responded aggressively. It is estimated that European airfares have increased +36% in 2023 compared to 2022 . Consumers have accepted this thus far, allowing for the accelerating force on passenger number growth driving revenue.

Looking ahead, we expect this ramp-up to slow in Q4’23/Q1’24, as the business begins to reach a normalized level. Compounding this is the current macroeconomic environment, which is contributing to a slowdown in discretionary spending as consumers’ finances are squeezed. Beyond early FY24, this will likely lead to growth pressures in the year, although the expectation is for inflation to be lower by this point, potentially allowing IAG to avoid a material decline.

Balance sheet & Cash Flows

At the cost of existing investors, IAG raised a substantial amount of cash through equity, which has ensured the protection of its balance sheet despite the impact of the pandemic. With an ND/EBITDA ratio of 1.4x, IAG is positioned well to reinvest in growth without committing a significant portion of cash to interest.

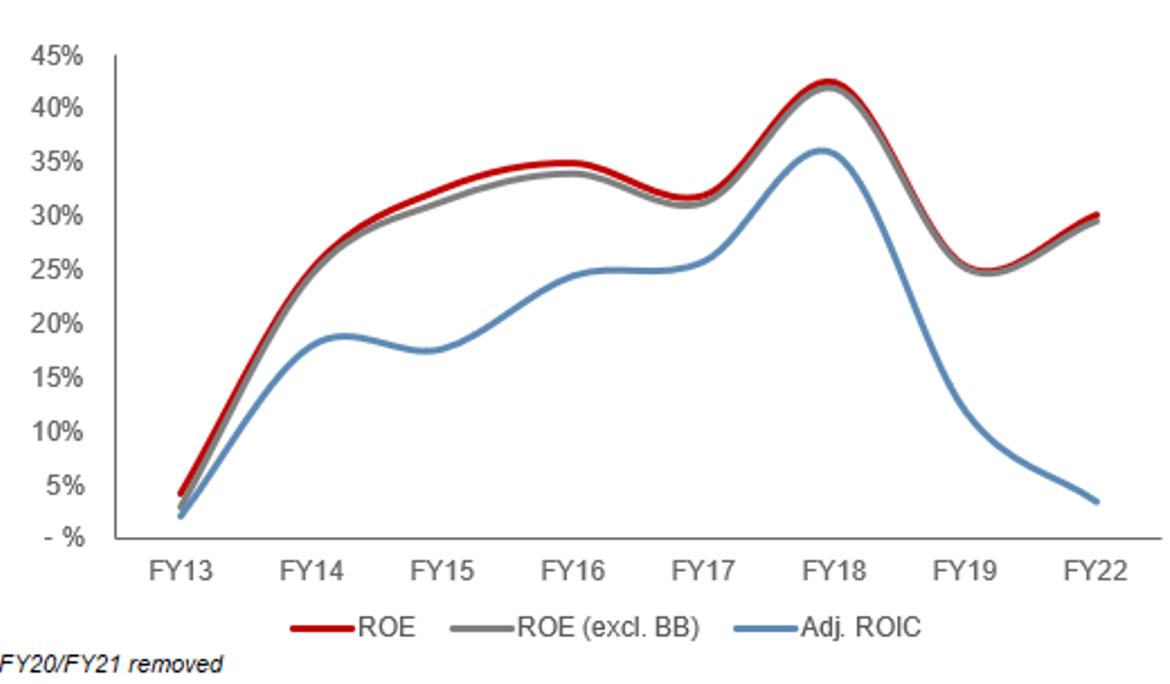

IAG has historically boasted an impressive ROE, owing to limited debt usage, historically important brands, and quality global routes / relationships with airports. A return to its historical peak levels is possible following a period of deleveraging.

{kind=link}

Outlook

{kind=link}

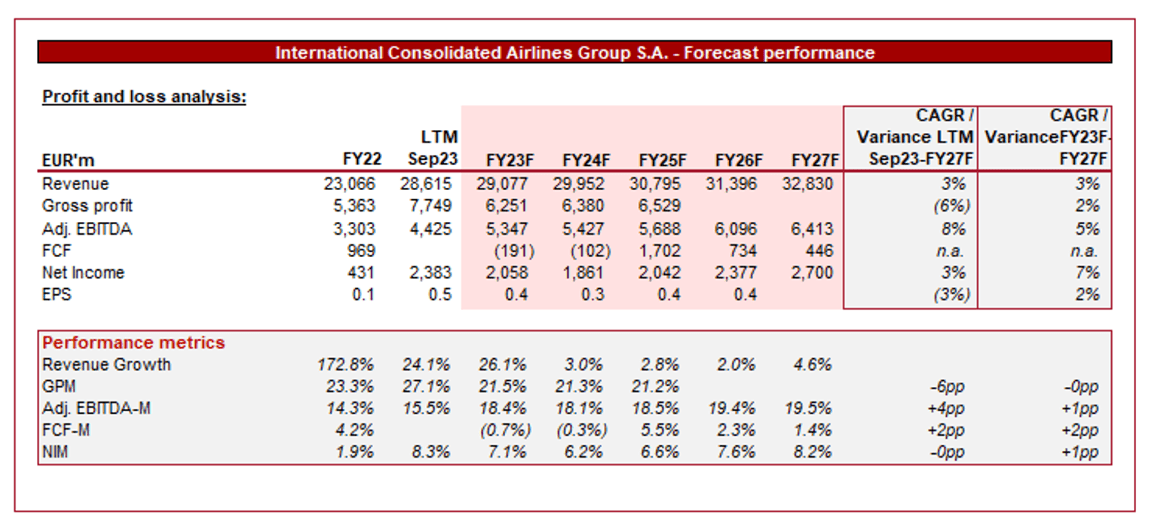

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting mild growth in the coming years, with a CAGR of +3% into FY27F. In conjunction with this, EBITDA-M is expected to sequentially improve into FY26F.

We broadly concur with these forecasts. The company’s growth has historically been mild due to heavy competition, as has the industry’s as air travel matures, suggesting a 3% rate is reasonable. This said, its average growth rate between FY13 and FY19 was 5.4%, while further inflationary price increases are also possible. Therefore, we suggest this leans toward conservatism.

Further, as we have discussed, the company is still ramping up and has shown a track record of achieving margin improvement, suggesting it can deliver the EBITDA-M improvements.

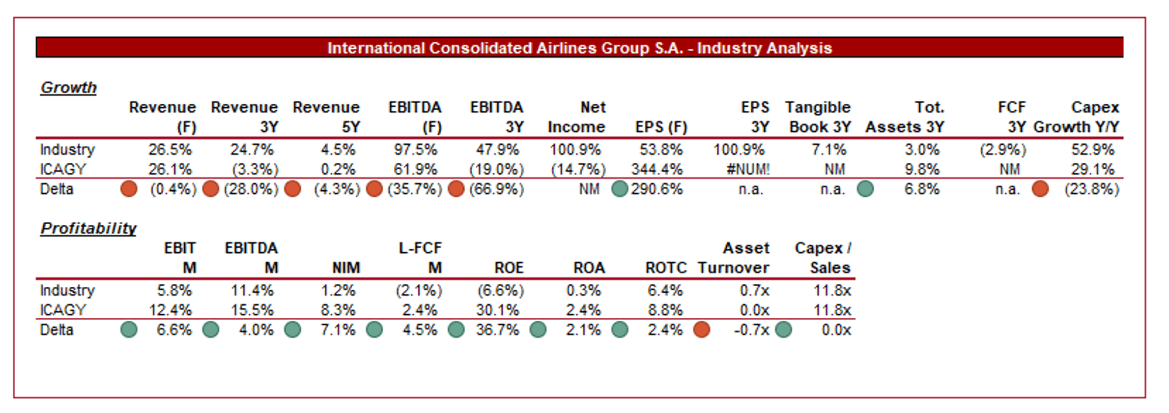

Industry analysis

Airlines Stocks (Seeking alpha)

{kind=link}

Presented above is a comparison of IAG's growth and profitability to the average of its industry, as defined by Seeking Alpha (20 companies).

IAG performs well relative to its peers, although certainty has weaknesses. The company’s growth has materially lagged behind its peers, in part due to a delayed recovery (3Y metric). This said, although the figures are heavily distorted by the impact of the pandemic, the directional trend is correct. IAG has struggled with competition from low-cost providers, while also alienating some of its loyal customers (and degrading its brand) but cutting costs to respond.

This said, IAG’s strengths are in its margins, with a noticeable delta across all key metrics. This is a reflection of its legacy business model, with strong market share in lucrative markets such as the UK, as well as strong European brands (British Airways and Iberia) and key routes across Europe (and globally). Given its financial position, we believe IAG is well-positioned to invest in its capabilities to maintain its competitive position.

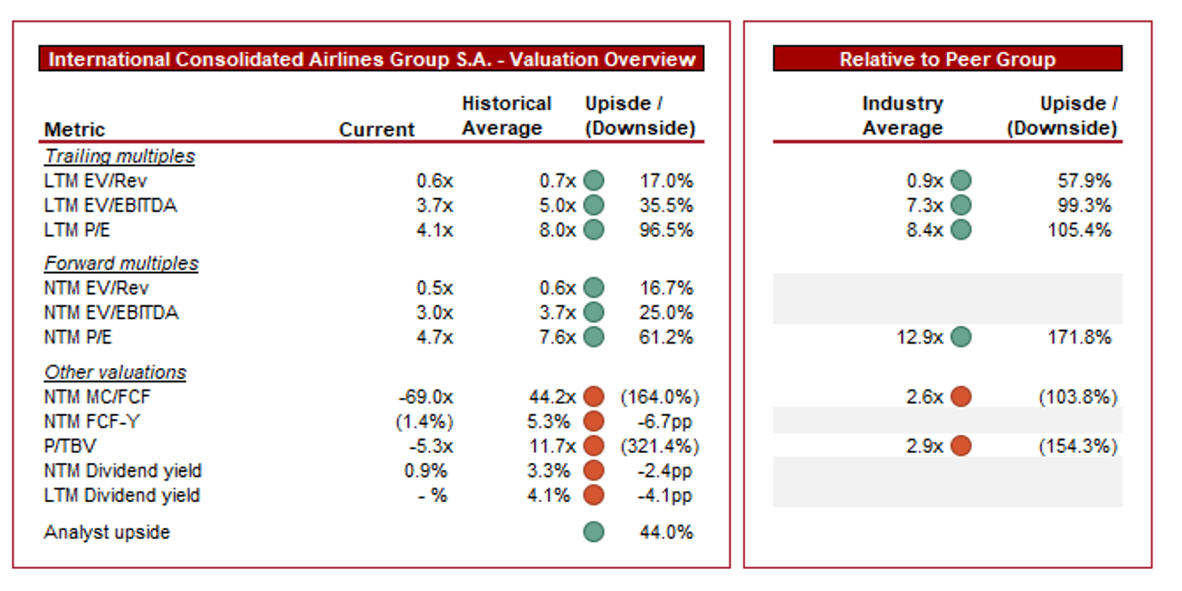

Valuation

{kind=link}

IAG is currently trading at 4x LTM EBITDA and 3x NTM EBITDA. This is a discount to its historical average. Note: we have adjusted its historical average to exclude its pandemic multiples, which materially distort how investors have seen the company over time.

A discount to its historical average is warranted in our view, owing to margin deterioration, macroeconomic risks, increased competition from low-cost airlines, and risks associated with a return to its pre-pandemic levels (primarily margins and deleveraging). This said, many of these factors are either already priced in (such as competition) or are now at a lower risk given visibility (margin improvement). For this reason, we believe the current discount is overdone.

Further, IAG is currently trading at a discount to its peers on an LTM EBITDA basis (~99%) and a NTM P/E basis (~171%). This is a substantial level, implying investors continue to be downbeat on IAG, primarily due to competition and limited growth levers. Although we concur with this assessment, we do not think the valuation adequately reflects this as its margins should allow for comparable returns even as growth lags behind.

Based on this, we believe IAG is undervalued, with negative growth sentiment and wider macroeconomic factors likely a reason.

Key risks with our thesis

The risks to our current thesis are:

- Lingering pandemic-related challenges.

- Further competition through pricing.

- Economic downturn in key economies.

Final thoughts

IAG is a solid company. It is potentially lacking the qualities of a long-term winner due to its inability to successfully respond to the likes of Ryanair, however, it is currently extremely undervalued and still generating strong value for shareholders through leading profit margins.

At a 3x NTM EBITDA multiple, we believe any near-term downside risk is priced in, allowing for investors to participate in the final stage of IAG’s resurgence.

For further details see:

International Consolidated Airlines: Incredibly Cheap Airline With A Good Business Model