INPAP - International Paper: Solid Quarter And Better-Than-Expected Cost Evolution

2023-10-28 08:39:41 ET

Summary

- Two key announcements: Closure of Orange containerboard mill and proceeds from Ilim joint venture.

- The company's EBITDA increased slightly, with a better EBITDA margin. This was mainly driven by cost discipline.

- We are more cautious about the 2024 volume recovery, but we incorporated a better margin given the solid results achieved with the 'Building a Better IP' strategy.

International Paper (IP) just released its Q3 financial figures. As our readers know, we have a good grip on paper companies, and recently, we commented on the merger between Smurfit Kappa and WestRock . Regarding IP, we were forecasting " Challenges Ahead " with a solid view for 2023. An earnings recovery story backed our buy rating supported by 1) a juicy dividend per share (it currently yields 5.5%), 2) a strong balance sheet (no significant maturities until 2028), and 3) higher market share penetration with clients switching from plastic packaging to paper solutions.

Before going to the Q3 financial details, we should report two vital events. In the last month, the company announced a strategic action to permanently close the Orange containerboard mill ubicated in Texas and cease production capacity on two pulp machines located in Pensacola. Here at the Lab, we positively view this action for two reasons: 1) compared to peers, IP lacks profitability, and we believe the company strategically shut down Orange Mill to increase margins, and 2) combining the two closures, the market has 1.3 million fewer tons of annual production capability in containerboard, and this will likely help to re-balance the paper supply/demand. To recap, including this latest development, International Paper has containerboard production capacity in 17 mills with an annual capability of 13 million tons. Following our analysis called ' Looking At The Russian Exposure ,' the company communicated Ilim sale disposal. With this deal, the company fully divested its Russian activities and will receive approximately $472 million in cash (net of transaction costs). This limited downside risk on cash repatriation and limited potential litigation risks.

Q3 results

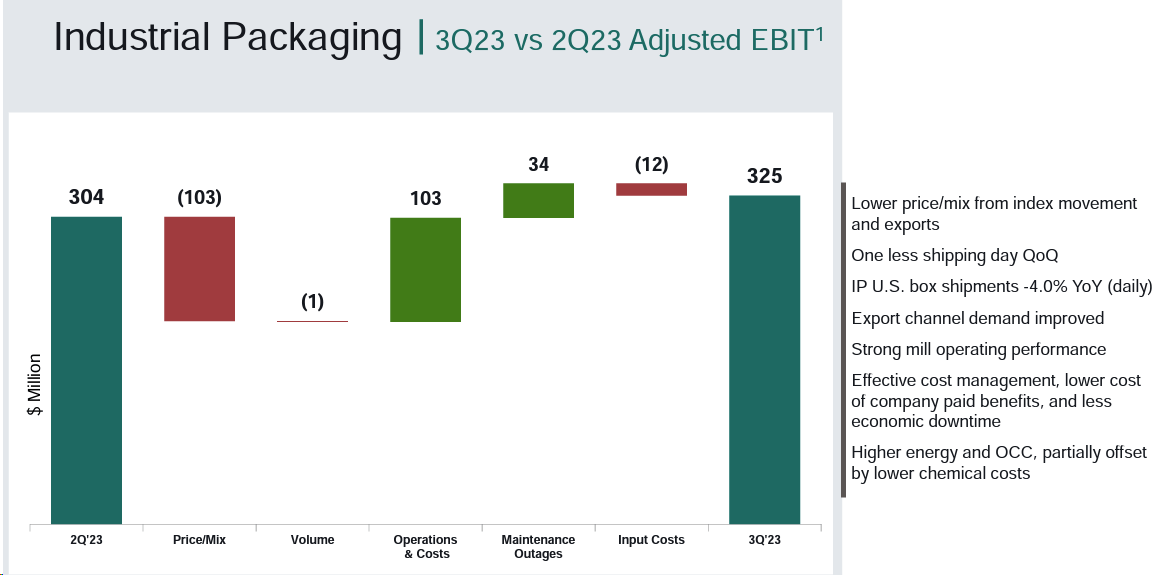

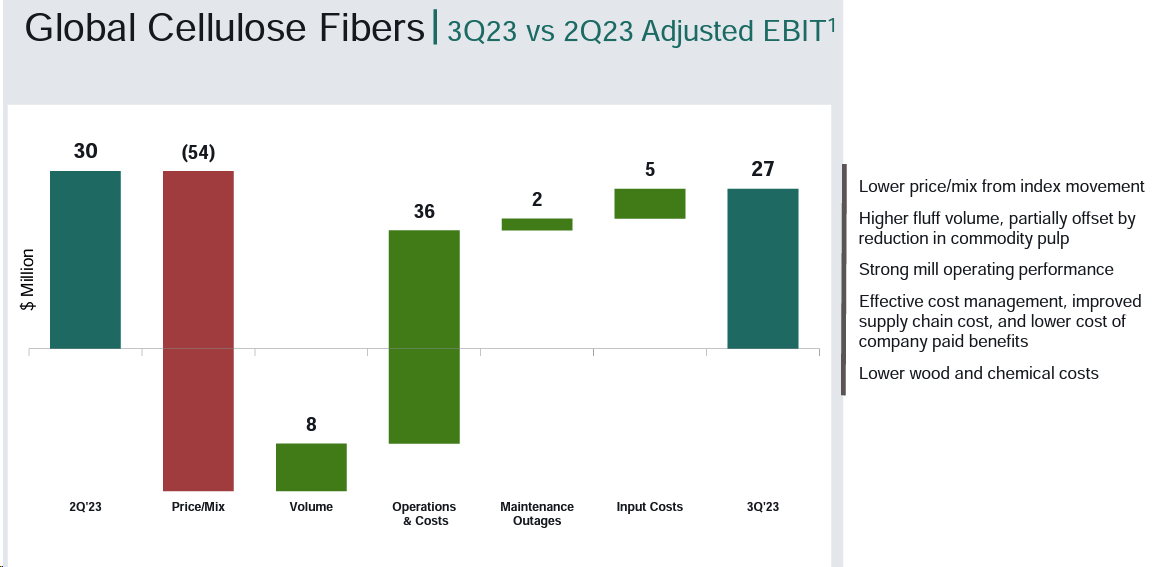

Here at the Lab, we forecasted clients' destocking activities and volume stabilization in Q3. Therefore, we are not surprised that top-line sales were broadly stable from Q2 and significantly decreased compared to last year's results. In numbers, IP reached a turnover of $4.6 billion vs. Q3 2022 at $5.4 billion. Despite that, the company's EBITDA was slightly up quarter on quarter and moved from $570 million to $590 million with a better EBITDA margin, which stood at 12.8%, gaining 60 basis points. Looking at IP at the divisional level, Industrial Packaging's operating profits increased in Q3 to $325 million (Fig 1). Despite an unfavorable geographic mix, earnings improved thanks to higher volumes and lower planned maintenance costs. COGS inflation still impacted the company primarily for logistic costs, energy, and fiber. Going to the Global Cellulose Fibers division, the segment operating profits were $27 million (Fig 2). Earnings were lower than anticipated due to lower prices; however, the company benefits from lower operating costs positively.

Industrial Packaging Q3 Financials in a Snap

{kind=link}

Fig 1

Global Cellulose Fibers Q3 Financials in a Snap

{kind=link}

Fig 2

Why are we still positive?

- Even if the company sales were down 14% on a yearly revenue, the company missed expectations by only $210 million and beat EPS estimates by $0.06. Therefore, Wall Street analysts are not correctly pricing IP's margin recovery story;

- There were many questions related to the mill closure. However, there is an evident change in the management approach, considering the more competitive landscape in the paper market, and International Paper will show cost discipline in the future. In a nutshell, the company is optimizing its entire mill system, reducing the fixed cost while improving marginal cost;

- Having participated in the Q3 Q&A call, it is essential to report the following statement: " stabilization in Q3, and improvement in Q4; "

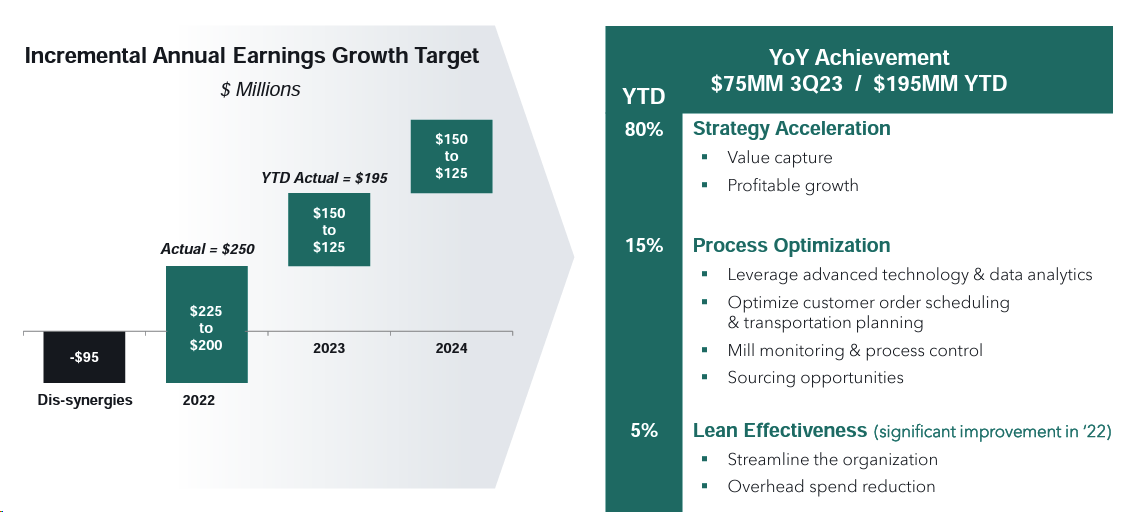

- On a positive note, with its strategy called ' Building a Better IP ,' the company exceeded its full-year saving guidance with a YTD total achievement of $195 million. These lower costs basis almost entirely offset the Ilim dividend previously estimated at $200 million per year (Fig 3);

- Post Q3 results, we adjusted our internal estimates, and in line with the company's Q4 estimates (EBITDA of $400 million), we arrived at a 2023 adj. EBITDA of $2.1 billion. This is due to lower earnings in Global Cellulose Fibers. At the same time, we left our CAPEX level unchanged at $1 billion.

{kind=link}

Fig 3

Conclusion and valuation

IP has no significant debt maturities in the short-term horizon, and looking at the FCF evolution, the company has sufficient funds to pay the current dividend ($160 million per quarter). IP quarterly cash dividend will be paid on the 15th of December and goes ex-div on the 14th of November. These FCF evolutions show that in the downcycle cycle, IP entirely covered the dividend expense.

{kind=link}

Looking ahead, consumer demand and persistent inflation will likely hurt packaging product volume. Here at the Lab, we are more concerned about Q1 2024 than Q4 (this is mainly due to e-commerce seasonal growth thanks to the Christmas period sales pick-up). At the same time, logistic disruptions have eased, and there is minor pressure from higher input costs. Compared to our last publication, we are more worried for the foreseeable period. For this reason, we are lowering our 2024 EBITDA from $2.5 billion to $2.2 billion and leaving unchanged our EBITDA multiple at 8x; we derive a target price of $36 per share versus our previous estimates of $42 per share . This implies a 10% upside on the current market value, maintaining an overweight view. Downside risks for paper companies include 1) a containerboard demand slowdown, 2) logistics constraints, 3) higher energy costs, and 4) new capacity coming online with an imbalance between supply & demand. Looking at IP, we also reported a new risk in the CEO succession plan change . In early September, the current CEO, Mark Sutton, requested the board to move forward with a replacement. Sutton has been IP's CEO since November 1014 and joined the company in 1984. He said the board would find " the right leader grounded in the company's core values and focused on creating value for our stakeholders ." However, succession plans are riskier for at least three reasons: 1) the company might lose a strong internal candidate, 2) there is usually insufficient time for a suitable replacement, and 3) an external CEO might take time to understand the company fully (IP has 39k employees globally). In addition, a succession plan might create internal fights that likely lead to value disruption, in our opinion.

For further details see:

International Paper: Solid Quarter And Better-Than-Expected Cost Evolution