IPCFF - International Petroleum: A Strong Quarter Against A Challenging Macro Background

2023-05-08 08:57:26 ET

Summary

- International Petroleum just reported record quarterly production of 52.8k boepd. Full-year production is expected to be at the top end of the guidance range of 48-50k boepd.

- The company has just completed the acquisition of Cor4, adding a fresh 4k boepd, and started development of its Blackrod project, which is targeting 30k boepd by 2026.

- This aggressive growth strategy is consistent with my belief that oil is in a secular bull market, despite some recent weakness.

- I continue to see International Petroleum as a long-term hold in my portfolio and any dip below 90 SEK as an opportunity to accumulate.

Introduction

International Petroleum Corporation ( IPCO:CA , OTCPK:IPCFF ), an intermediate Canadian E&P company with assets in Canada, Malaysia and France, just released its Q1 2023 results. The company is continuing to deliver solid results from an operational standpoint, but the stock plunged more than 10% over the course of the week, getting smashed in the general oil sell-off. At the moment, this is therefore a story of two tales: strong performance, against a challenging macro background.

Company's strategy

Many O&G companies are keeping production roughly stable and generously returning capital to shareholders, mostly via dividends. IPCO is pursuing a different strategy. The company is in the process of significantly increasing its production, via both acquisitions and the development of Phase 1 of its greenfield Blackrod project.

Cor4 acquisition and short-term strategy

In the short term, IPCO is aiming to add new barrels as fast as possible, in order to take advantage of the current pricing environment. In fact, the company recently completed the acquisition of Cor4, a small Canadian company, for asset consideration of $62 million. The acquisition has brought 15.9 million boe (barrels of oil equivalent) in 2P reserves and forecasted net average production of 4,000 boe per day for 2023, a roughly 8% increase compared to last year's figures. The new asset is already online and has been performing ahead of expectations in the last two months. IPCO is also investing in some marginal growth at its Canadian and French assets, as well as some cost optimization projects.

Blackrod Project

In the medium term, IPCO will be focused on Phase 1 of its oil sands Blackrod project in Alberta, Canada. The project was sanctioned last February and has just gotten underway. Phase 1 is expected to add around 30 thousand boepd, a roughly 60% increase from current levels. Blackrod came into the company's portfolio via the BlackPearl acquisition of December 2018 and is estimated to hold reserves of 1.2 billion barrels, of which only 218 million are being targeted by Phase 1 (for comparison, the rest of IPCO's portfolio holds 270 million boe as of December 2022).

There are reasons for caution regarding Blackrod. First oil is expected only in 2026, with production ramping up and reaching its target capacity in 2028. Total capital expenditures are projected to be around $850 million, a significant commitment for a company that is roughly valued at $1.18 billion. Finally, Blackrod has a relatively high breakeven, at approximately WTI $60 per barrel, meaning that the margin of safety is not huge should oil prices decline going forward.

For these reasons, I believe many investors sold out in disappointment when the decision to sanction Blackrod was made public. The market reacted negatively to the increase in development costs from $500 to $850 million, together with the fact that, based on the company's guidance, IPCO is going to burn most of its free cash flow in 2023 to finance Blackrod. This comes at a time when most oil majors are returning capital to shareholders with both hands and the oil price appears weak. Some skepticism is therefore warranted. On the other hand, the cost increase is mostly due to the fact that Phase 1 was originally planned to target only 20 thousand boepd (versus the current 30 thousand) and, despite Blackrod, the company will continue to generate significant free cash flow at current oil and gas prices.

Capital returns

According to the company's forecasts, during the period 2023-2027, IPCO will generate cumulative free cash flow between $700 million and $1.4 billion (with Brent trading in the range of $75 to $95 per barrel). If the company were to use all the excess free cash flow to buy back shares, it could buy back between 60% and 118% of its current market capitalization of around $1.18 billion, which would be equivalent to an annual yield between 12% and 24%.

According to management's comments during the conference call, IPCO remains committed to returning capital to shareholders, in particular via buybacks, despite Blackrod's ongoing development. It should be noted that, under the current Normal-Course Issuer Bid (NCIB) program, IPCO is limited to buying back approximately 7% of the current float. Management mentioned that they expect to max out the NCIB for this year, as they have already completed 60% of it and repurchased 5.5 million shares since the start of the year, at an average price of 102 SEK per share. Going forward, the company is not excluding the possibility of supplementing its NCIB program via a Substantial Issuer Bid (SIB), as was in fact done in 2022. At the same time, capital returns remain contingent on oil prices; in the event of a further weakening, all forms of capital returns will need to be suspended.

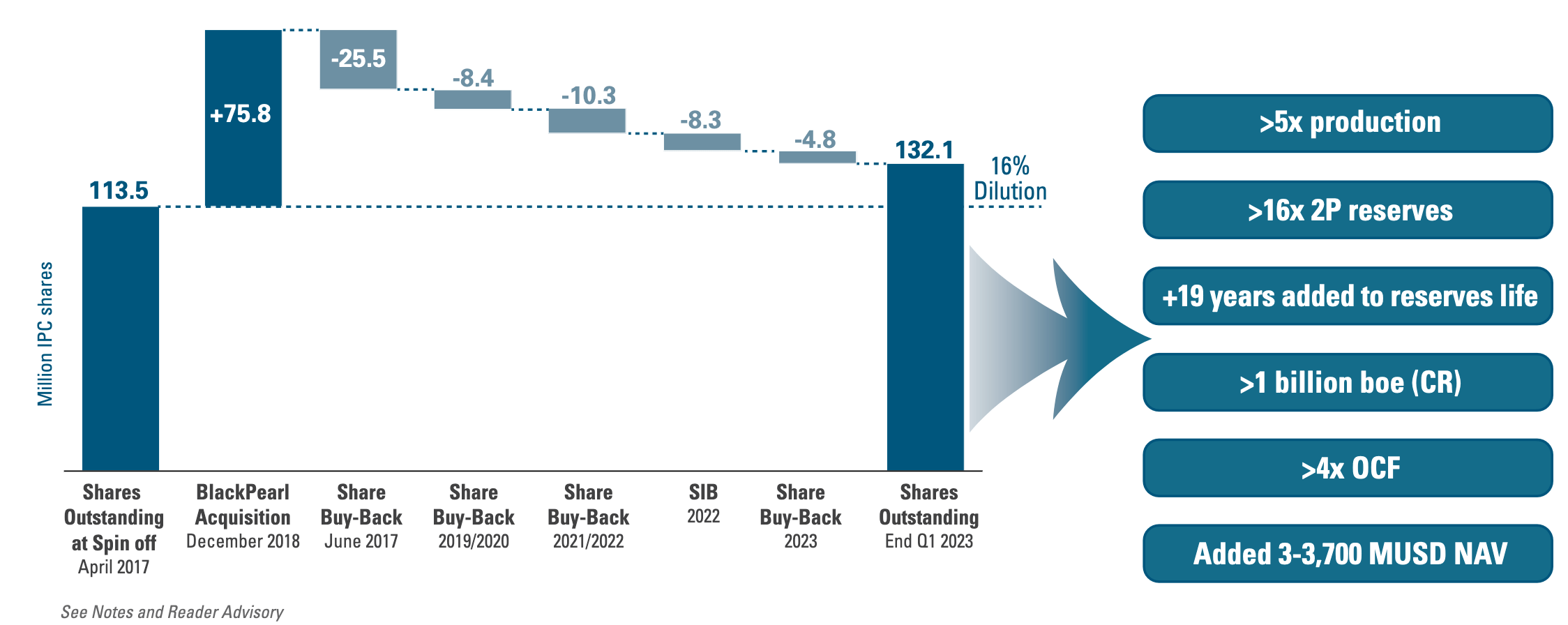

At the current valuation, I believe buybacks are more value accretive than dividends. The company has historically traded at a large discount to fair value, so management has been consistently buying back shares since 2017. As shown in the following visualization (taken from the company's Q1 2023 presentation), total dilution since IPO has been only 16% and in the meantime the company has managed to increase 5 times its production and 16 times its 2P reserves, while maintaining a strong balance sheet (the company is in a net cash position). IPCO has repurchased a total of 57.2 million shares at an average price of SEK 61 (shares are currently trading at around SEK 90 per share), thus creating more than $150 million in value for its shareholders.

{kind=link}

International Petroleum share repurchases (Company's Q1 2023 presentation, slide 9)

Valuation and share price

It is my opinion that small and intermediate producers are the place to be in oil. Not only are there many undervalued names, but they are also going to be the main beneficiaries compared with majors in a secular oil bull market. I am therefore very bullish on IPCO in the long-term.

At the same time, I don't see any catalyst that can lift the undervaluation in the near term. The undervaluation is certainly significant: as per the company's Q1 presentation, the NAV 10% is estimated at 270 SEK / share, a roughly 65% discount compared with today's closing price. However, the fact remains that IPCO will not be making any money this year after Blackrod's expenses. Production is projected to remain roughly flat at 50 thousand barrels for the next three years. Even if IPCO keeps maxing out its NCIB program, capital returns are unlikely to increase relative to current levels.

Therefore, I can understand the rationale of investors selling after Blackrod's announcement and planning to rebuy in a few years. Personally, however, I am wary of selling at the current valuation, especially after the recent sell-off. Sentiment is extremely negative in oil at the moment, but it can turn quickly, especially with the oil market projected to move into a deficit from the second half of the year. Crucially, I remain convinced in the long-term bull thesis that oil prices are going to rise significantly because of years of underinvestment and ESG policies. IPCO has a strategy consistent with this long-term view: investing now in meaningful production growth to reap the benefits in 3-5 years.

Oil market

In the short term, the main driver of price fluctuations will be movements in the oil price. Just slightly over half of IPCO's production is from Canadian oil, one third from Canadian natural gas, and 15% Brent. The company is therefore exposed to global oil prices, in particular to the WTI-WCS differential and Canadian natural gas prices.

Natural gas prices have declined below 2 CAD/m cf during 2023; however, IPCO has managed to hedge a significant portion of its production at 4.10 CAD/mcf until October 2023. As a result, the average realized price during Q1 was higher, at around 3.60 CAD/mcf.

Oil prices have also declined. The WTI/WCS differential has decreased (from around 30 USD/bbl at the end of 2022 to 15 USD/bbl); the company had hedged this spread at 10 USD/bbl for 12 thousand boepd, which resulted in a small loss. In particular, over the last week WTI prices have declined more than 10%, before a small recovery on Friday. Shares in Stockholm have also plunged around 10%. I believe IPCO will continue to trade weakly in the short-term, as long as the outlook for oil remains challenged.

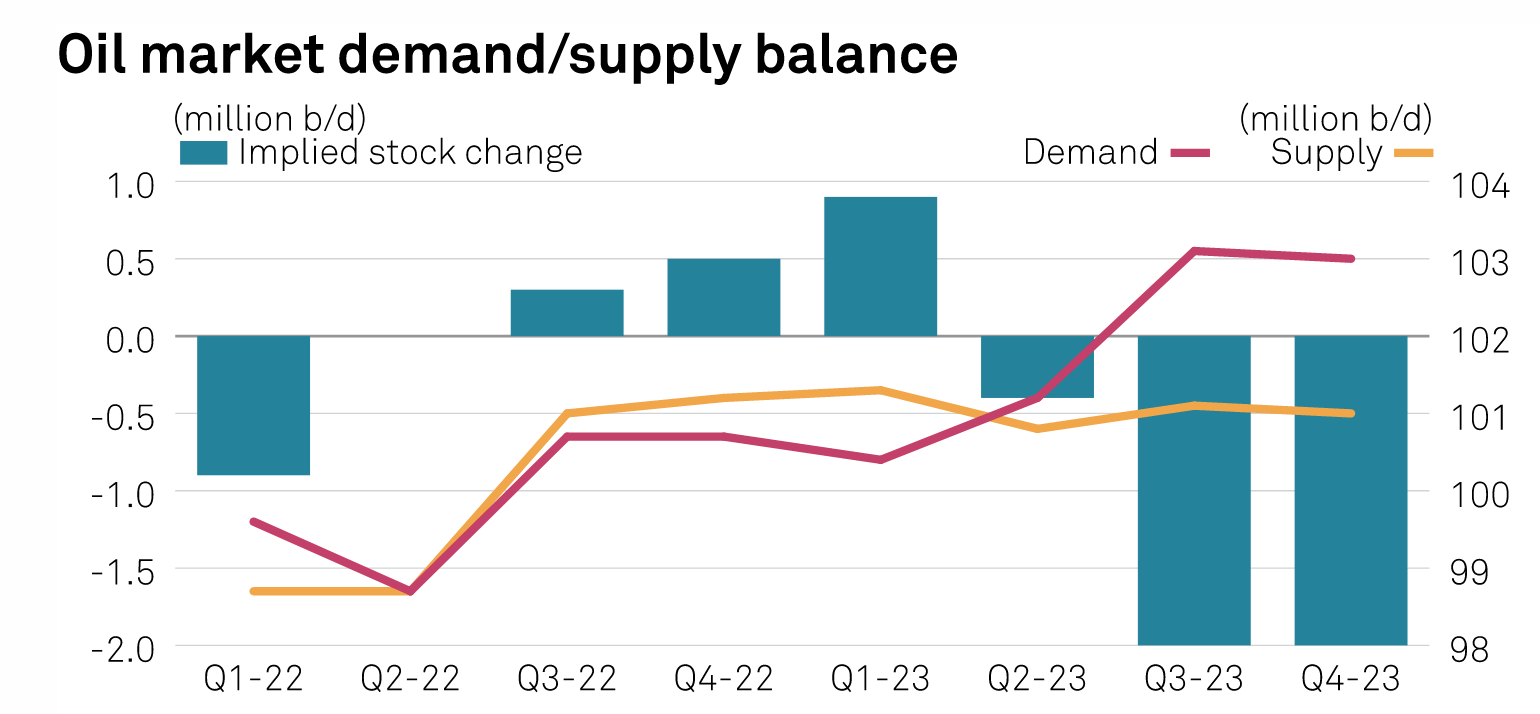

Contrary to my expectations from last year, oil is currently oversupplied. The recovery in Chinese demand has been weaker than expected and Russian oil continues to flow to the market in record quantities despite the EU ban. Recession fears also represent a headwind. Nonetheless, my belief is that the current slowdown will prove to be a mid-cycle soft patch and that oil prices will average significantly higher than current spot over the next 5-10 years. It is possible that already in the second half of the year the oil market will be in a deficit , assuming OPEC+ maintains its cuts and Iran remains under sanctions.

{kind=link}

Oil market demand/supply balance (spglobal.com)

Q1 2023 results

IPCO reported very strong operational results for Q1 2023. Total production reached a new quarterly record of 52.8k boepd, as a consequence of optimization programs and high facility uptime across all assets. Full-year production is now expected to be at the top end of the guidance range of 48-50k boepd. Operating costs came in at 17.3 USD/boe , slightly below the guidance range of 17.5–18.0 USD/boe .

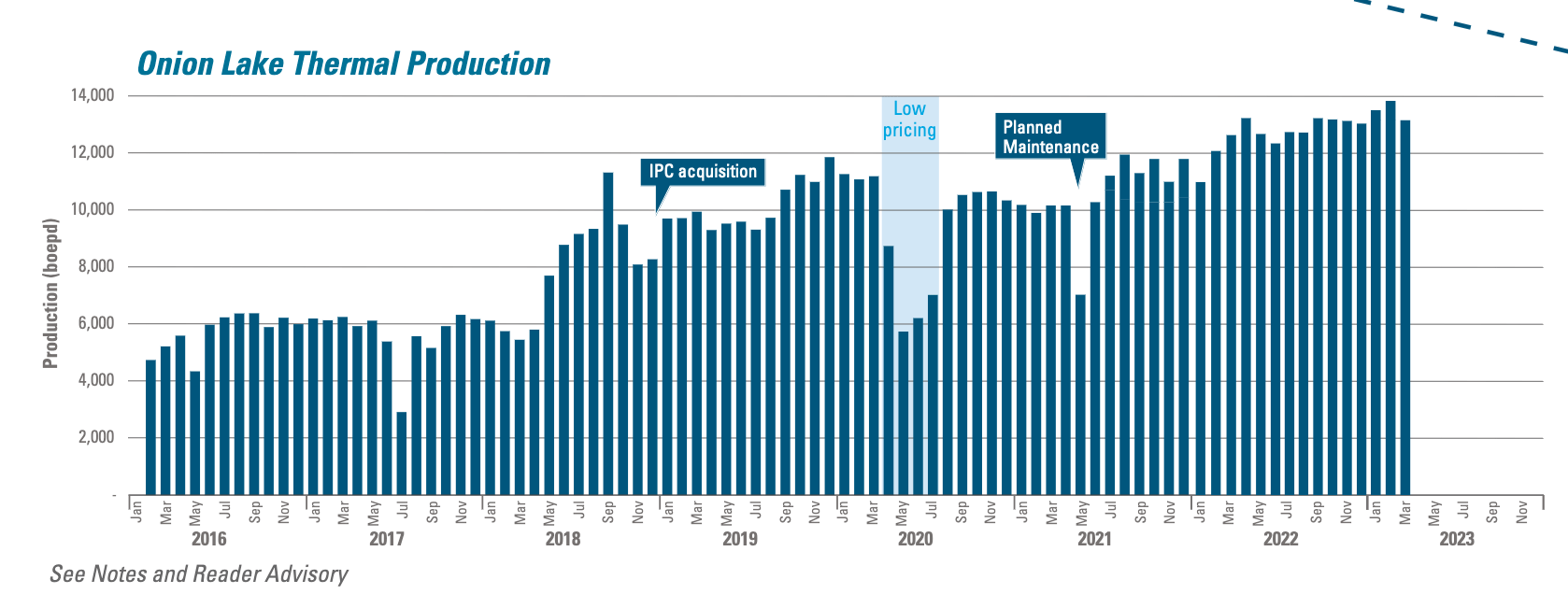

Looking in more detail at each asset individually, Onion Lake Thermal , the company's Canadian heavy oil field, delivered particularly strong results, reaching a new record production in January. Two expansion programs are ongoing, namely the development of Pad L, as well as new infill wells.

{kind=link}

Onion Lake Thermal production by month (Company's Q1 2023 presentation, slide 13)

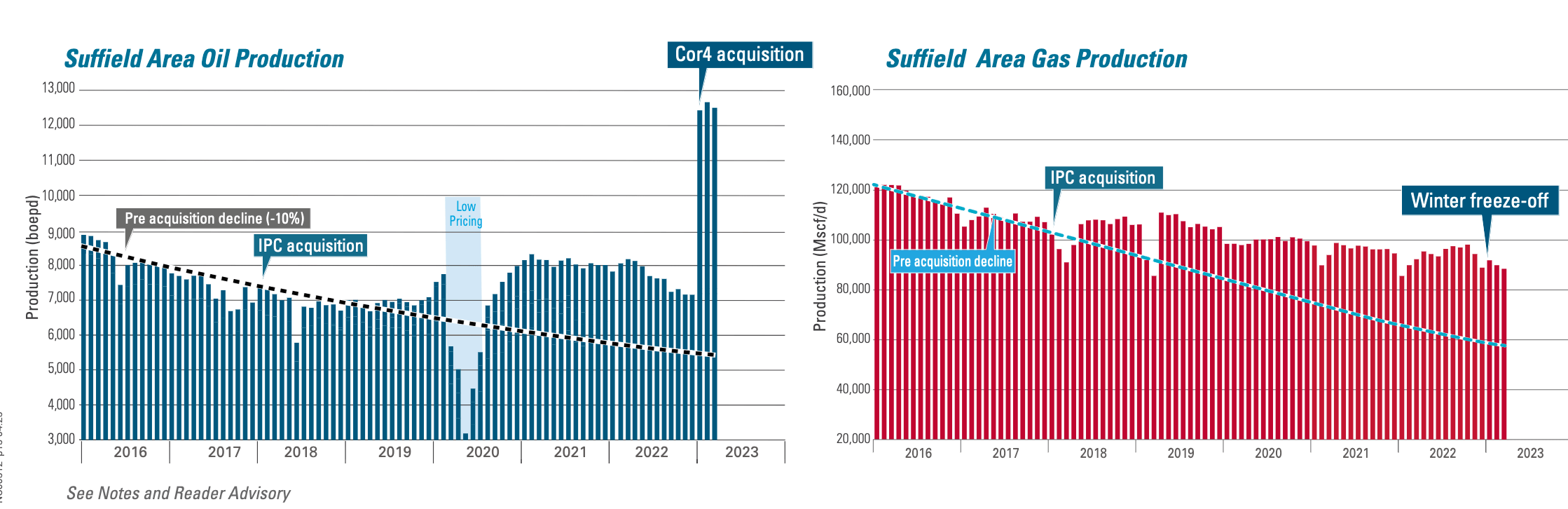

Suffield's oil and gas production was also very strong, thanks in particular to the addition of Cor4 assets, that have been performing ahead of expectations. It is also interesting to note in the graphs below how IPCO has been able to maintain and expand production over the years compared with pre-acquisition decline expectations. Six new wells are being budgeted for 2023, of which 3 have already been completed.

{kind=link}

Suffield's oil and gas production (Company's Q1 2023 presentation, slide 14)

The Bertam field in Malaysia posted roughly stable performance, and similarly for the French assets, despite a dip in March due to political protests that caused the shutdown of many refineries in the country.

Regarding financial results, IPCO achieved o perating cash flow of 76 MUSD and free cash flow of 16 MUSD (impacted by 55 MUSD of capital expenditures). With Brent at 70 USD/bbl, operating cash flow for the full year is expected to be around 250 MUSD. Since capital expenditures are weighted towards the later part of the year, with Blackrod picking up steam, full-year FCF will likely be in negative territory (around -145 MUSD with Brent at 70 USD/bbl). This however is expected, and capital expenditures for Blackrod will start decreasing from 2024 onwards.

Conclusions

IPCO has just delivered strong operational results across all its assets. Management is executing a long-term strategy of aggressively growing production, while maintaining a strong balance sheet and returning capital to shareholders. Blackrod's development has started. In the long-term, the company has significant optionality for growth, in particular by developing Blackrod beyond Phase 1. In fact, even after Phase 1, around 80% of its reserves will remain undeveloped and the company has already obtained regulatory approval for a further 50 thousand boepd. Unfortunately, oil price weakness is proving to be a short-term headwind. Nonetheless, I continue to see IPCO as an excellent play on the oil supercycle thesis over the next few years. I therefore consider IPCO a long-term hold in my portfolio and any dip below 90 SEK as an opportunity to accumulate.

For further details see:

International Petroleum: A Strong Quarter Against A Challenging Macro Background