INSW - International Seaways: Best Risk/Reward Tanker Company With Significant Upside Potential

2023-12-18 08:27:44 ET

Summary

- Best tanker market in the last decade, with the potential for rates to reach new highs.

- This optimism is fueled by a combination of factors, including a low order book, an aging fleet, new regulations, and robust medium-term demand with Atlantic oil production growth.

- International Seaways is positioned as the safest choice among tanker stocks with its low valuation, good management, and generous dividend yield.

- The company's outstanding operational performance and improved shareholder returns should help close the valuation gap, 40%+ upside.

Investment Thesis

Despite an impressive tanker market and improved shareholder returns, International Seaways ( INSW ) continues to trade at a substantial discount to Net Asset Value ((NAV)). With outstanding operational performance, successful fleet expansion, and a potential 40-50% upside based on estimated NAV or dividend yield, INSW's improved shareholder returns should help to close the valuation gap. Simultaneously, the combination of its low valuation, good management, and generous dividend yield positions INSW as the safest choice among tanker stocks.

Business Overview

International Seaways is one of the largest tanker companies worldwide providing energy transportation services for both crude oil and petroleum products. This strategic positioning allows the company to leverage opportunities in both markets. INSW was a result of the strategic spin-off by Overseas Shipholding Group ( OSG ) to separate its international and domestic businesses. The resulting entity had a fleet of 55 vessels, spanning from Very Large Crude Carriers (VLCC) to Medium Range ((MR)) vessels, thereby covering a diverse spectrum of the maritime industry.

At the helm of International Seaways is Lois K. Zabrocky, who assumed the role of President and Chief Executive Officer following the spin-off. Prior to her leadership role at INSW, Lois led OSG's International Flag business unit as Senior Vice President, with responsibility for commercial management and oversight of fleet operations.

A pivotal milestone occurred with the 2021 merger with Diamond S Shipping, where International Seaways acquired an extensive clean tanker fleet at highly attractive valuations. The merged fleet initially comprised 102 ships and has since displayed notable activity in the Sale and Purchase (S&P) market, leading to a fleet size of 74 ships.

Fleet Capacity (INSW November presentation)

As of now, International Seaways owns and operates an on-the-water fleet of 74 vessels , comprising 13 VLCCs, 13 Suezmaxes, five Aframaxes/LR2s, seven LR1s, and 36 MR tankers.

Fleet Composition (INSW November presentation)

{kind=link}

The difference in number is due to the LR1, INSW includes two of their four newbuilds. These vessels are scrubber-fitted, dual-fuel LNG ready, and are expected to enter the Panamax International Pool.

One of the main characteristics of INSW is their hybrid operating model to enable flexibility to scale the fleet across the cycle. The majority of their fleet is employed in leading commercial pools, providing economies of scale through volume discounts on bunkers, agency fees, and administrative costs. INSW holds ownership stakes in three of these pools, effectively reducing daily operational expenses and facilitating involvement in specialized operations such as their lightering business. Among these, the Panamax International Pool stands out as their top-performing pool, where their seven LR1 vessels are actively trading. Notably, historical data attests to the pool's exceptional performance, surpassing the LR1 market. For instance, in Q3, it achieved an impressive $56,300 per day, outperforming competitors such as TORM PLC at $32,641 per day and Hafnia at $30,198 per day.

{kind=link}

Another noteworthy characteristic is INSW's ability to time the market with their growth. Historically, they have successfully expanded their fleet during the low points of market cycles, thereby creating significant shareholder value. This approach not only enables the company to pursue expansion initiatives but also facilitates the continuous rejuvenation of their fleet:

INSW Fleet Expansion (INSW November presentation)

{kind=link}

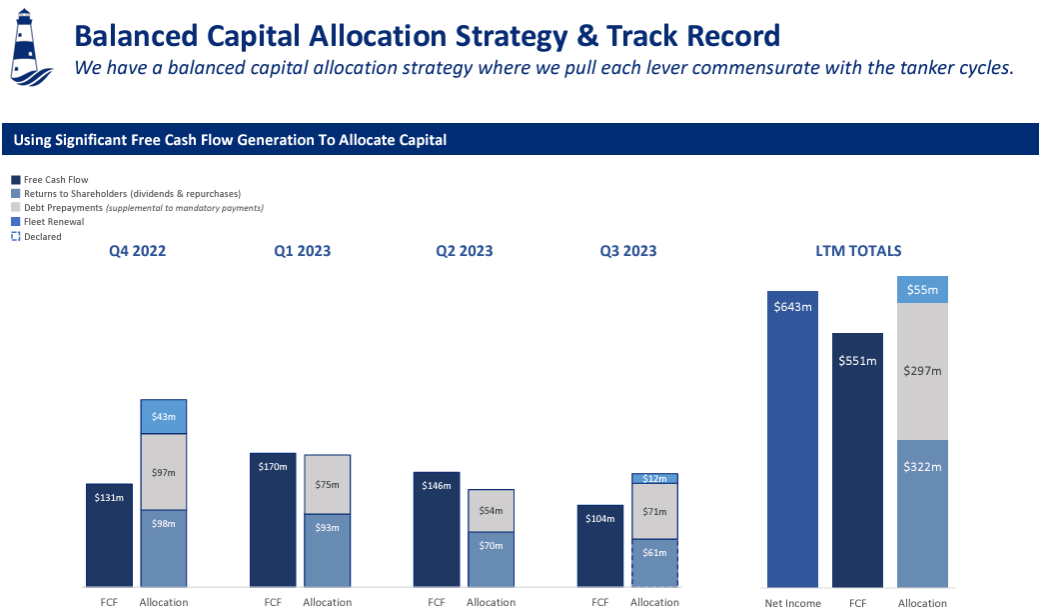

Finally, INSW's track record in capital allocation has been consistently robust since its inception, boasting an impressive Total Shareholder Return of nearly 375%. Although the company lacks a formal shareholder return policy, since the beginning of 2020, INSW has returned over $500 million to shareholders through a combination of share repurchases and dividends. In the last four quarters, the capital allocation can be broken down as follows:

Capital Allocation (INSW November presentation)

{kind=link}

Over the past four quarters, INSW allocated $322 million for returning capital to shareholders, equivalent to approximately 15% of their market capitalization. This allocation was primarily directed towards dividends, accounting for $308 million, with an additional $14 million attributed to share buybacks. Simultaneously, nearly half of their Net Income was allocated to debt prepayments. Now with a 19% Net Loan to Value, the lowest in INSW's history, the company plans to decelerate debt prepayments. This reduction in debt repayment is expected to result in an increase in shareholder returns, as highlighted in the last conference call . Omar Nokta inquired whether the increased Q3 payout (63%) represented a new threshold, to which Jeff Pribor, the CFO, responded in the affirmative.

Q3 Conference Call Transcript (Seeking Alpha)

{kind=link}

One noteworthy negative is the absence of a formal dividend policy. It's quite possible that many investors may not have been aware of the Q3 payout increase and that going forward, it is expected to continue higher.

Main Shareholders

International Seaways stands out as one of the few shipping companies without a controlling shareholder. This unique characteristic, coupled with a substantial discount to NAV, piqued the interest of Fredriksen, who acquired a 16.6% stake in April 2022. However, the management didn't like the move and implemented a poison pill to prevent Fredriksen from acquiring more than a 17.5% stake.

In response, Fredriksen released an open letter criticizing the "bloated" board, lack of value creation and urging shareholders to vote against them and the extension of the poison pill in the annual meeting. Despite his appeal, the management was reelected, albeit by a slim margin of about 3 million votes. Since then, Fredriksen has remained silent.

Several months later, in October 2022, Idan Ofer and Navig8 each acquired a 5% stake. If they align with Fredriksen in the upcoming annual meeting, they may likely secure a majority and could have some seats in the board.

Main Shareholders (Marketscreener)

{kind=link}

Another plausible scenario involves Frontline, post the completion of the Euronav acquisition, considering the acquisition of INSW in the second half of 2024. If INSW persists in trading at a substantial discount to NAV, there is a strong possibility that Frontline could acquire INSW at NAV or with a slight discount. I have no doubt that shareholders, given the persistent trading below NAV, would accept a premium of 30% or more without hesitation. The financing for this acquisition could be seamlessly achieved through issuing shares above NAV and Fredriksen support, thereby positioning Frontline as the dominant tanker stock without any direct competition. Such a move could also yield synergies by eliminating the need for INSW's management, known for their high compensation.

Tanker Overview

As discussed in my previous articles on d'Amico and Frontline and Euronav Deal , the outlook for both crude and product tankers remains highly favorable. Despite I expect some softening in demand for Q2 and Q3 2024, the current market conditions are the most robust in the past decade, supported by strong fundamentals pointing towards sustained strength.

Since the publication of those articles, two significant developments have occurred. Firstly, the United States has started to apply sanctions over Russian oil price cap violations . This move is expected to increase fleet inefficiencies and potentially boost asset values. Secondly, Houthi forces have begun daily attacks on ships in the Red Sea, posing a major threat to shipping. As a response, vessels may opt for the longer route around the Cape of Good Hope instead of using the Suez Canal. This diversion could add between 7 and 10 days to the voyage or result in slower sailing, accompanied by heightened military presence.

Houthi attacks (@detresfa_ Twitter)

Upon reviewing tanker demand and supply, the EIA predicts that global oil demand will surpass supply in 2024. While these projections may shift in response to a potential softening in growth, a critical factor for tankers is the geographical mismatch between oil supply growth, primarily driven by America, and demand centered in Asia. This dynamic significantly amplifies the demand for ton miles

Tanker Demand (INSW November presentation)

{kind=link}

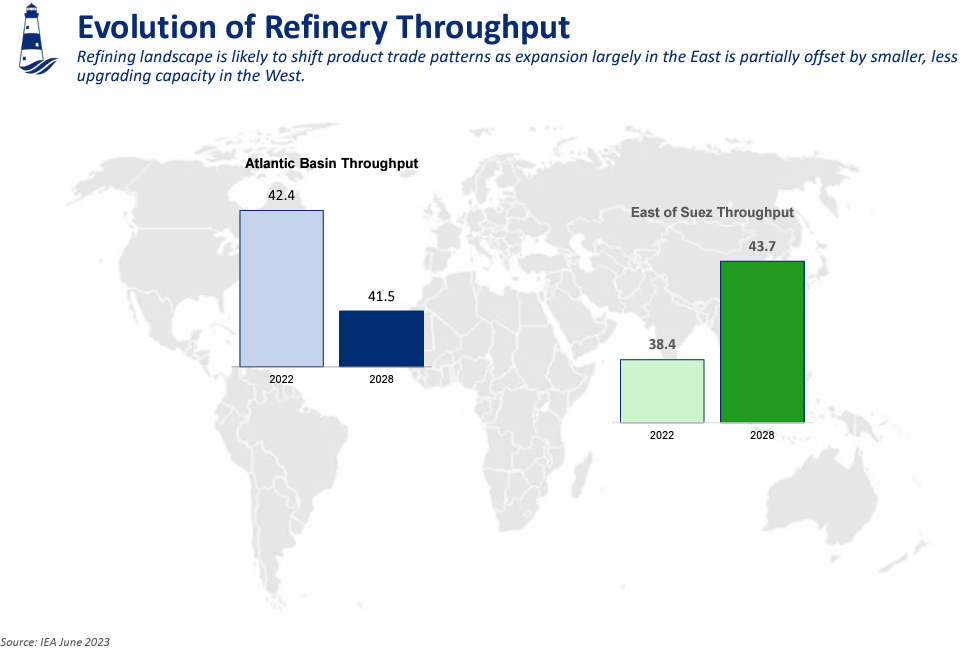

This disparity doesn't just impact crude tankers; product tankers are also affected. The IEA foresees an increase in refinery throughput in the East, resulting in a surplus of products that should be exported, while a reduction is anticipated in the West.

Refinery Throughput (INSW November presentation)

{kind=link}

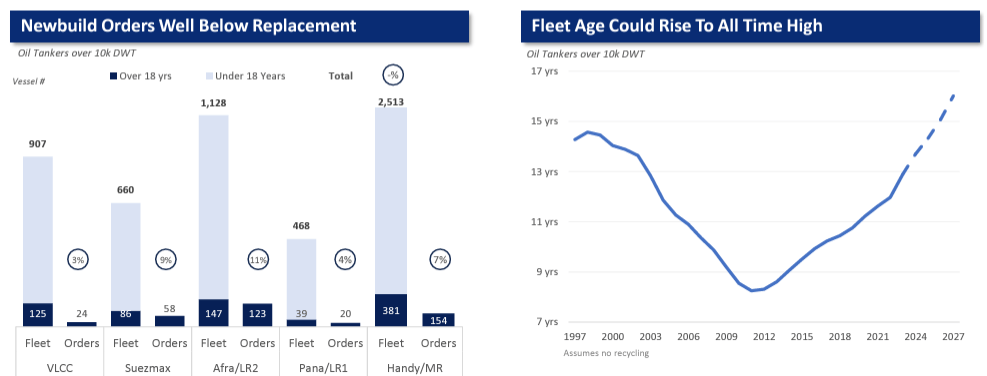

Considering that shipyards are already booked until 2026 and new orders are extending into 2027, anticipated supply growth remains minimal, supporting rates in the coming years. With the current order book accounting for less than 6% by deadweight tonnage, there is insufficient capacity to meet the anticipated growth. This percentage is notably low across all segments, particularly for VLCCs, which stand at just 3%. Adding to this, the average age of the fleet has increased to 12.8 years and is projected to continue rising in the coming years, leading to higher inefficiency and an increased number of scrapping candidates. It's important to remember that when a tanker reaches 15 years old, survey intervals are required every 2.5 years instead of the standard 5, emphasizing the challenges posed by aging vessels in maintaining operational efficiency.

Tanker Supply (INSW November presentation)

{kind=link}

Financial Position & Stock Valuation

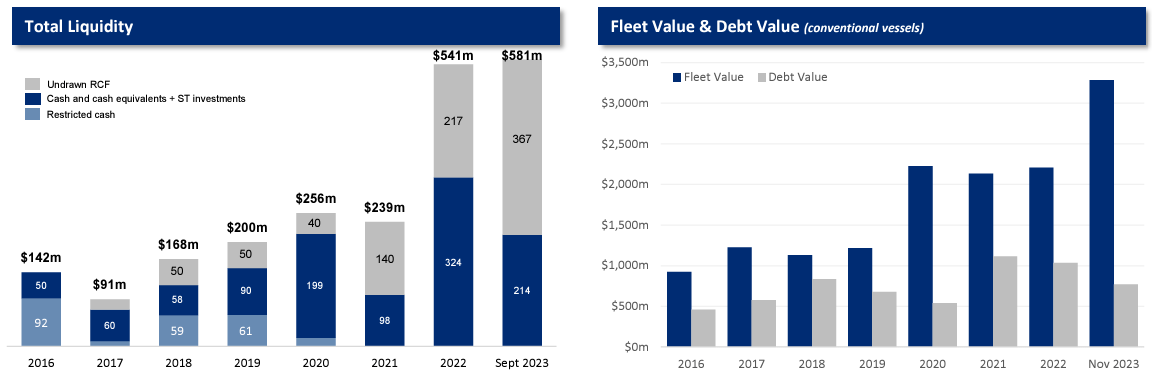

INSW Liquidity (INSW November presentation)

{kind=link}

International Seaways has been conservatively managed, that has allowed them to be in a comfortable financial position enabling the payment of substantial dividends while concurrently reducing leverage. As of September 2023, the company holds $214 million in cash and cash equivalents, boasting a total liquidity of $581 million, while its debt stands at $855 million, with 40% of the fleet unencumbered. This financial setup provides ample flexibility.

Regarding the debt, INSW executed various liquidity-enhancing initiatives during 2021 and 2022. These initiatives significantly diversified their financing sources, extended debt maturities between 2026 and 2031, and effectively reduced their weighted average interest rate to 6.05%, with 85% of interest fixed or hedged. The amortization, standing at $32.2 million per quarter, is notably $6 million less than the previous quarter, demonstrating a highly manageable debt structure.

INSW Debt Profile (INSW November presentation)

International Seaways usually discloses their fleet value using VesselsValue figures. As of October 31, their fleet value stood at $3,285M . With this information and balance sheet data calculating INSW's NAV becomes a straightforward process:

NAV Calculation (Author & INSW November presentation)

{kind=link}

At the current stock price, INSW trades at a 25% discount to its NAV. Considering the guidance provided by the company and factoring in the subsequent improvement in rates since the last update, it becomes feasible to estimate the year-end NAV.

Rates and Guidance (INSW November presentation) MR Atlantic Rates (Infinity Shipbrokers)

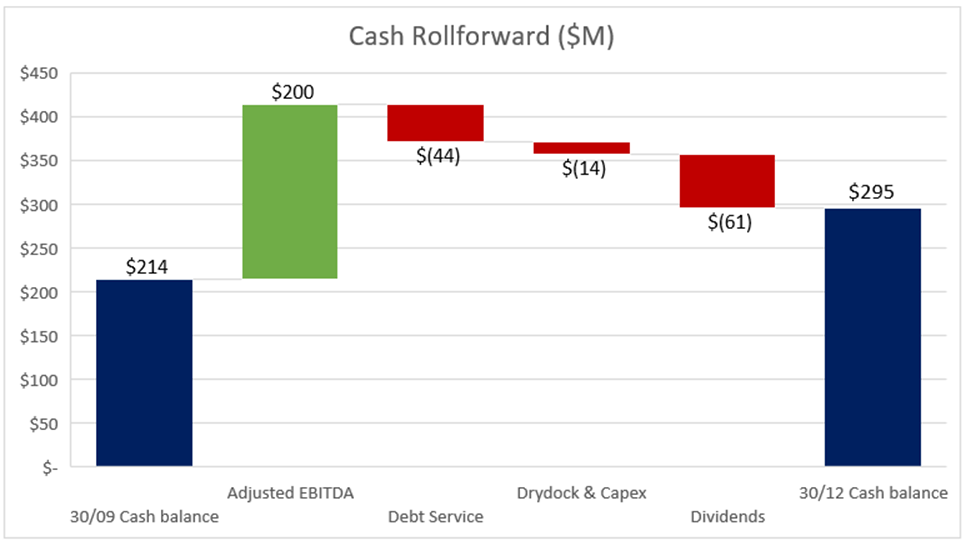

Post-Q3 reporting, there has been a significant improvement in rates, particularly in the Americas, where INSW predominantly operates its product ships. Based on this information, I anticipate INSW to achieve a net income of nearly $150 million and approximately $200 million in EBITDA. The expected cash position at the end of the period is around $300 million. Notably, debt amortization is set to decrease to $32 million, and interest to $11.6 million, in contrast to $39 million and $15 million, respectively, in Q3. Additionally, there is a modest increase of $1 million in Drydock and Capex, primarily attributed to Capex in Aframaxes. Finally, during this quarter, INSW distributed $61 million in dividends.

{kind=link}

These figures suggest an approximate $3 EPS and a minimum $1.85 dividend, resulting in a compelling 16% yield. Utilizing this data to calculate year-end NAV and assuming a 5% increase in asset values-already on an upward trajectory-implies a NAV of $64 per share, reflecting a substantial 30% discount.

NAV Calculation (Author)

This projection indicates a noteworthy 40% upside solely based on the 2023 year-end NAV, with the prospect of continued NAV growth in the following year. Notably, management has consistently showcased operational excellence, outperforming industry peers, and has displayed shareholder-friendly capital allocation, primarily through substantial dividends-though an increase in share repurchases would be particularly favorable. Furthermore, there is a demonstrated awareness of the undervaluation. Considering all these factors, in my view, INSW deserves to trade around NAV. If, however, management falls short of closing this valuation gap, I anticipate strategic moves from Fredriksen

Given this analysis, I would assign an immediate fair value of at least $60 per share to INSW, signifying a robust 40% upside. Depending on next year's rates, this valuation could easily surge to $65 per share or even surpass $70 per share, translating to a remarkable 50% or more upside potential.

INSW has a repurchase authorization that could help to close this valuation gap; however, this year it was utilized only in Q2. Management is showing a preference for rewarding shareholders through dividends, so I don't expect them to deploy it in substantial amounts. Nevertheless, to illustrate the potential impact, consider a $100 million expenditure -less than half of their cash reserve- on repurchases at a share price of $45 would result in a NAV increase of $1 per share. Simultaneously, the next dividend per share would experience a 5% uptick; for instance, a $60 million dividend would go from $1.22 per share to $1.28 per share with the repurchase.

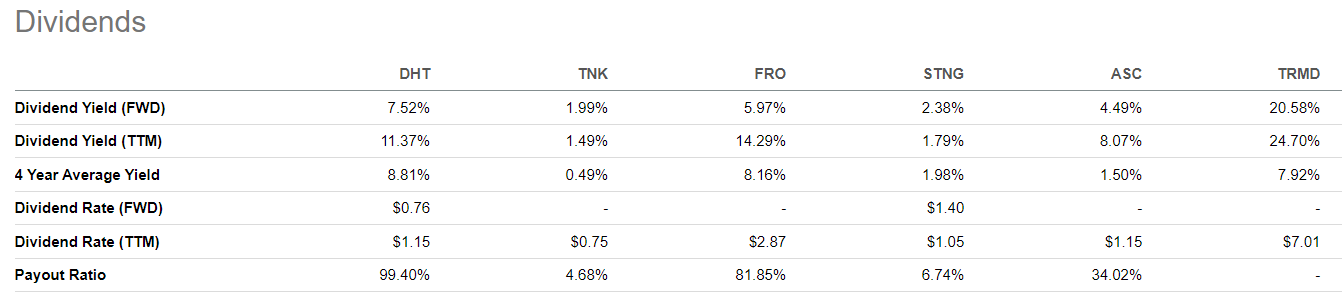

An alternative method to assess the value of INSW is through the lens of dividend yield. As previously mentioned, while INSW lacks a formal dividend policy, insights from their Q3 conference call indicate a shift towards paying around 65% of EPS, compared to the previous 40/50%. Over the last four quarters, they achieved an EPS of $12.97, implying a potential dividend of $8.43 with a 65% payout ratio. This would result in an impressive 19% yield at the current price, ranking as the second-highest among industry peers, following TORM (TRMD).

Dividend Comparison (Seeking Alpha)

{kind=link}

A common characteristic shared among major dividend payers, such as Torm, Frontline, and DHT, is their achievement of high yields by paying out approximately 100% of EPS. In contrast, INSW adopts a more conservative approach, intending to pay 65% of EPS, yet it still manages to yield higher than both DHT and FRO. Notably, these major players typically trade at or above NAV, while INSW currently trades at 0.75 NAV. Considering that INSW retains a portion of its profits, projecting a forward yield similar to DHT, at 12%, would imply a valuation of $70 per share.

Risks

OPEC+ cuts: Persistent efforts to elevate prices have resulted in multiple production cuts from OPEC+, resulting in reduced tanker utilization and rates. I don't expect them to cut further but is a possibility.

Reduction in demand: In the event of a significant recession, there is a potential for an adverse impact on tanker demand, leading to a reduction in rates.

Management's inability to rerate the stock: Over the past several months, INSW has consistently traded below its NAV. If management does not take proactive measures, this discount may persist.

Increased Orderbook: While VLCC orderbook remains notably low, other segments have been receiving several orders. With an aging fleet new tonnage is highly needed but some segments could experience a less attractive outlook.

Houthi attacks: There is a potential threat from Houthi attacks, considering Idan Ofer's 5% stake in INSW. INSW vessels may be targeted, leading them to likely avoid navigating through the Red Sea.

Fredriksen selling shares: With a substantial 16.6% ownership, the potential for Fredriksen to divest their shares could impact the stock price in the short term.

Conclusion

In conclusion, International Seaways stands as a prominent player in the global tanker industry, with a diverse fleet and strategic positioning that enables it to capitalize on opportunities in both crude oil and petroleum product markets. The company's great operational performance with better results than peers, and successful timing of fleet expansion during market lows contribute to its resilience and shareholder value creation. Moreover, dividends are expected to increase going forward.

Despite robust fundamentals in the tanker industry, INSW trades at a notable discount to its NAV, and one of the biggest discounts between peers. There exists potential for significant upside, projecting a 40% to 50% increase in share value based on the estimated NAV or dividend yield. The management's commitment to shareholder returns through dividends, coupled with the possibility of share repurchases, further underlines the company's shareholder-friendly approach. Additionally, the presence of influential shareholders like John Fredriksen could help to close this valuation gap.

In summary, International Seaways exhibits a robust business model, financial stability, and a commitment to shareholder value. The company's success hinges on effectively addressing the identified risks, closing the valuation gap, and navigating the evolving dynamics of the global tanker market.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

International Seaways: Best Risk/Reward Tanker Company With Significant Upside Potential