INSW - International Seaways: Strong Buy

2023-05-29 21:48:09 ET

Summary

- International Seaways is a medium-sized tanker company with a diverse fleet of 76 tankers.

- The company has strong earnings, with a P/E ratio of around 3, and a solid balance sheet.

- INSW is a cheap investment option for exposure to the tanker market, offering regular + special dividends, stock repurchases and debt paydowns.

- INSW is a strong buy at its current price.

Who are International Seaways?

International Seaways (INSW) is a medium-sized tanker company. This means that they are involved in the shipping of oil around the world. They own a fleet of 76 tankers; this is a mixed fleet of both crude (dirty) oil and clean (refined) product tankers; and is a mix of all sizes of ship from the very large to the reasonably small.

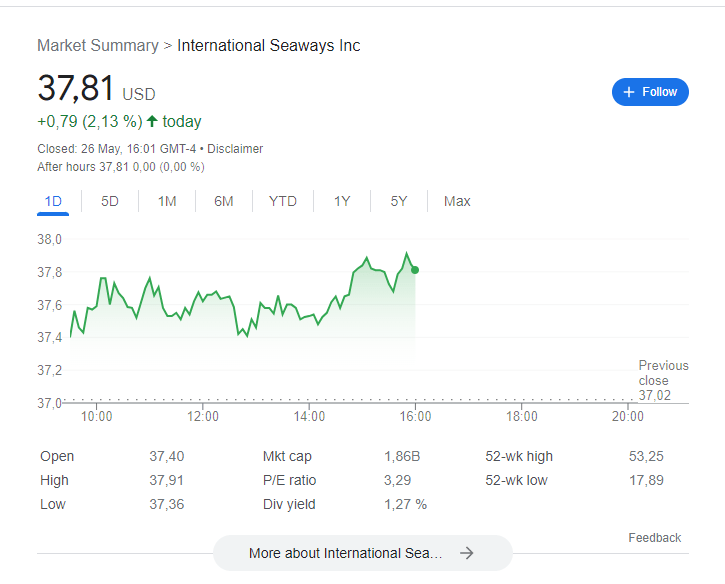

Currently valued at $1.86bn, INSW stock is a cheap investment option for anyone looking for exposure to the tanker market.

{kind=link}

Stock price (Yahoo finance)

What's in their fleet?

The below is the mix of their fleet at present:

| 13 |

| VLCC |

| 13 |

| Suezmax |

| 4 |

| Aframax |

| 1 |

| LR2 |

| 9 |

| LR1 |

| 37 |

| MR |

INSW owns a mix of dirty and clean tankers, of all sizes. This is different from other players in the space that tend to focus on individual segments (e.g. Scorpio Tankers focus exclusive on product tankers; DHT focus exclusively on the VLCC space; Euronav focus on the crude space).

Unlike these companies mentioned above, INSW is a well diversified tanker company. If you have an especially strong feeling about one particular sector, INSW may not be your stock of choice. However if you want exposure to all parts of the market then INSW may represent an excellent choice for you.

Seaways: are they cheap?

Seaways net income and adjusted net income for the last 5 quarters is below:

Net income (INSW Q1 presentation)

The current market cap is $1.86bn. Their net income of the last few quarters:

Q1 2023: $162.5mn (or 8.7% of market cap in 1 quarter)

Q4 2022: $208.8mn (or 11.2% of market cap)

-> so if the last 2 quarters are a guide to earnings, INSW is earning around 20% every 6 months, or about 40% a year. On a PE ratio, that would imply something like a PE of 2.5. Which would imply INSW is exceptionally cheap!

If we look over the last 4 quarters:

Q3 2022: $113.9mn (or 6.1% of market cap)

Q4 2022: $71.5mn (or 3.8% of market cap)

-> over the last 4 quarters, earnings have summed to 30% of the current market cap. Which would imply INSW is trading at 3.3x trailing earnings. And again, INSW would be exceptionally cheap!

Now, obviously tanker companies, like all companies, rely on their underlying markets. In the case of INSW, that means they are dependent on the rates they can charter out their ships for Q2, Q3 2023 etc.

Q2 2023 onwards:

INSW have given an indication of the rates that they expect to see for Q2 2023 as well:

INSW spot rates (INSW Q1 presentation)

Of the 5 ship types they have, 4 look likely to achieve rates over Q1 2023. And Suezmax rates look to only slightly underperform. So Q2 2023 - at a minimum - looks to be very solid.

We don't really know how the future will look, but we do know that INSW has 3 newbuilds arriving now/shortly. And that all 3 are on reasonably long term contracts as well.

Fleet optimization (INSW Q1 presentation)

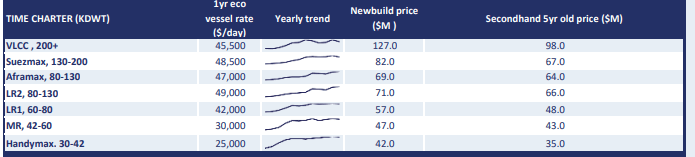

In addition, we can see from broker reports what 1 year time charters are indicating for each of these sectors. From Poten (Friday May 26 2023):

{kind=link}

Current 1 year charter rates (Poten shipbrokers)

Using the 1 year vessel rates, their fleet mix, and allowing for 90 days (approx. 1 quarter), INSW would generate quarterly income of around $265m.

| Count |

| Ship |

| TCE |

| Count x TCE x 90 days |

| 13 |

| VLCC |

| 45,500 |

| 53,235,000 |

| 13 |

| Suezmax |

| 48,500 |

| 56,745,000 |

| 4 |

| Aframax |

| 47,000 |

| 16,920,000 |

| 1 |

| LR2 |

| 49,000 |

| 4,410,000 |

| 9 |

| LR1 |

| 42,000 |

| 34,020,000 |

| 37 |

| MR |

| 30,000 |

| 99,900,000 |

| Total |

| 265,230,000 |

Note: I've used 1 year rates here, and not spot rates, as spot rates can be very volatile.

Q1 2023 saw revenue of $287m and earnings of $172m. If we project INSW to generate $265m of revenue, their earnings should land around the $150m mark as well. Given their market cap is currently $1.86mn, that's about 8% in 1 quarter. Implying they trade for a nice earnings rate of just 3.

INSW balance sheet

You may think INSW is especially indebted, or has other risks we haven't considered. But their balance sheet has never been stronger.

Total liabilities: $1.01bn

Current assets: $560mn

Net debt: approx. $550mn. I think it's fair to say that INSW's balance sheet is in an exceptional place. If required, they could easily reduce their debt position considerably.

So...what's the catch?

Honestly, I think a number of tanker stocks are trading simply "too cheap" at the minute. And I like INSW as they have a diversified fleet and don't have too much debt. But is there a catch?

Fleet age: the fleet is 12 years old That's not young. That said, these ships could work for another 10 years easily. And the company trades for a PE of around 3!

Management: they aren't shy about awarding themselves shares. That said, I think they've managed the company well. They haven't bought ships "on spec", they're paying dividends, and they've reduced their debt.

The economy : is this the reason the stock trades poorly? if the world economy "tanks" (pun intended) then tanker stocks will perform very poorly.

Will shareholders get rewarded?

The answer here is YES! It should be noted that INSW

- has a regular dividend in place ($0.12 per quarter)

- has been paying a special dividend, when they can ($1.88 in Q4; $1.50 in Q1. So Q1 saw a total dividend of $1.62 which is 4.3% of the current stock price in just that one quarter)

- has been buying stock ($40m repurchase in place at end of Q4 2022). In the last 3 weeks they have bought 300k shares, for approximately $12mn (small, but still important)

- and has regularly been paying down debt

I don't believe that INSW will suddenly burst upwards +50%. However, if market rates hold for an extended period, then INSW is frankly very underpriced. And we'll continue to see more dividends, more debt paydowns, and more stock re-purchases.

Summary

Investing in individual stocks, as opposed to ETFs or managed funds, is relatively risky. Investing in tanker companies is riskier again! However, INSW is:

- prudently managed (with low debt);

- well managed (a large, diverse fleet);

- rewarding shareholders every quarter, with large dividends.

To me, INSW represents a strong buy at this price.

For further details see:

International Seaways: Strong Buy