WPP - Interpublic Group: Price Is What You Pay Value Is What You Get

2023-10-11 10:00:00 ET

Summary

- Interpublic Group has suffered in the current macro environment due to large clients in the tech and telecom sectors' cost-cutting initiatives.

- Although IPG beat analysts' expectations on EPS, they missed revenue by a fairly large margin during Q2 earnings, causing the share price to decline.

- This along with economic uncertainty has also caused the share price to decline significantly over the last 3 months.

- IPG has raised the dividend for 11 straight years and also rewarded shareholders with share buybacks over the years.

- The company has a strong balance sheet with well-laddered debt maturities, minimal amount due in 2024, and no other maturities due until 2028.

Introduction

I feel like nowadays everyone is looking for the safest place to put their money. During times of uncertainty, it can become hard investing in the stock market. Especially now that 2023 is closing out and September & October are shaping up to be similar to 2022. Historically these months have been the worst months for the overall market. Couple that with high interest rates and surging treasury (rates), and you can see why the market has been down over the past month. Talks again of a looming recession, high oil prices, a stronger dollar, and the restart of student loan repayments don't help either in my opinion.

But through it all, I've remained calm and navigated the storm as best I can while searching for opportunities. During economic downturns, things can get bad, but these times also present favorable circumstances for those willing to go into the storm. In my opinion, this is the perfect time to snatch up great stocks trading at a low valuation. Like Warren Buffett says, "Price is what you pay, value is what you get." And now is a great time to buy stocks where their price is not reflecting their true value. In this article I discuss a stock that is not well-known but could be a great addition to your dividend portfolio.

Business Overview

I actually came across Interpublic Group (IPG) a few years back while researching their peer Omnicom Group (OMC). I had a friend who worked for them so I decided to look into the company. That's when I found out about IPG. It doesn't appear to be a popular stock amongst investors which piqued my interest. A goal of mine is to find underrated & undervalued stocks that have the potential for exponential returns years from now. That brings me to IPG.

Interpublic Group is a "values-based, data-fueled, and creatively driven provider of marketing solutions." They're actually an S&P 500 company that has been around for quite some time. They were founded in 1930 as McCann Erickson and formally changed their name to IPG in 1961. The company currently has 57,000 employees working in all major world markets. They operate in three segments: Media, Data & Engagement Solutions, Integrated Advertising & Creativity Led Solutions, and Specialized Communications & Experiential Solutions. They're one of the big agency companies along with OMC and WPP plc (WPP).

Lackluster Performance

So now that we know who IPG is, let's take a look at the company's finances and the secular headwinds surrounding the stock. As you can see below, IPG was trading over $40 a share just a few short months ago but has seen a sharp decline in price by roughly 40% since then. So the obvious question is why. During Q2 earnings the company reported diluted EPS of $0.68 and adjusted EPS of $0.74. This was a fairly large increase from Q1's diluted EPS of $0.33, and adjusted EPS of $0.38.

{kind=link}

But even though the company beat analysts' expectations on earnings, it missed on revenue by a fairly large margin and was down year-over-year. To be fair 2023 has been a rough year for the entire sector. Peer OMC also experienced some headwinds during its Q2 earnings, missing revenue by $50 million. This was due to reduced spending from clients in the tech and telecom sectors. Many clients have been experiencing a challenging period during the current macro environment, mostly due to significant cost-cutting initiatives.

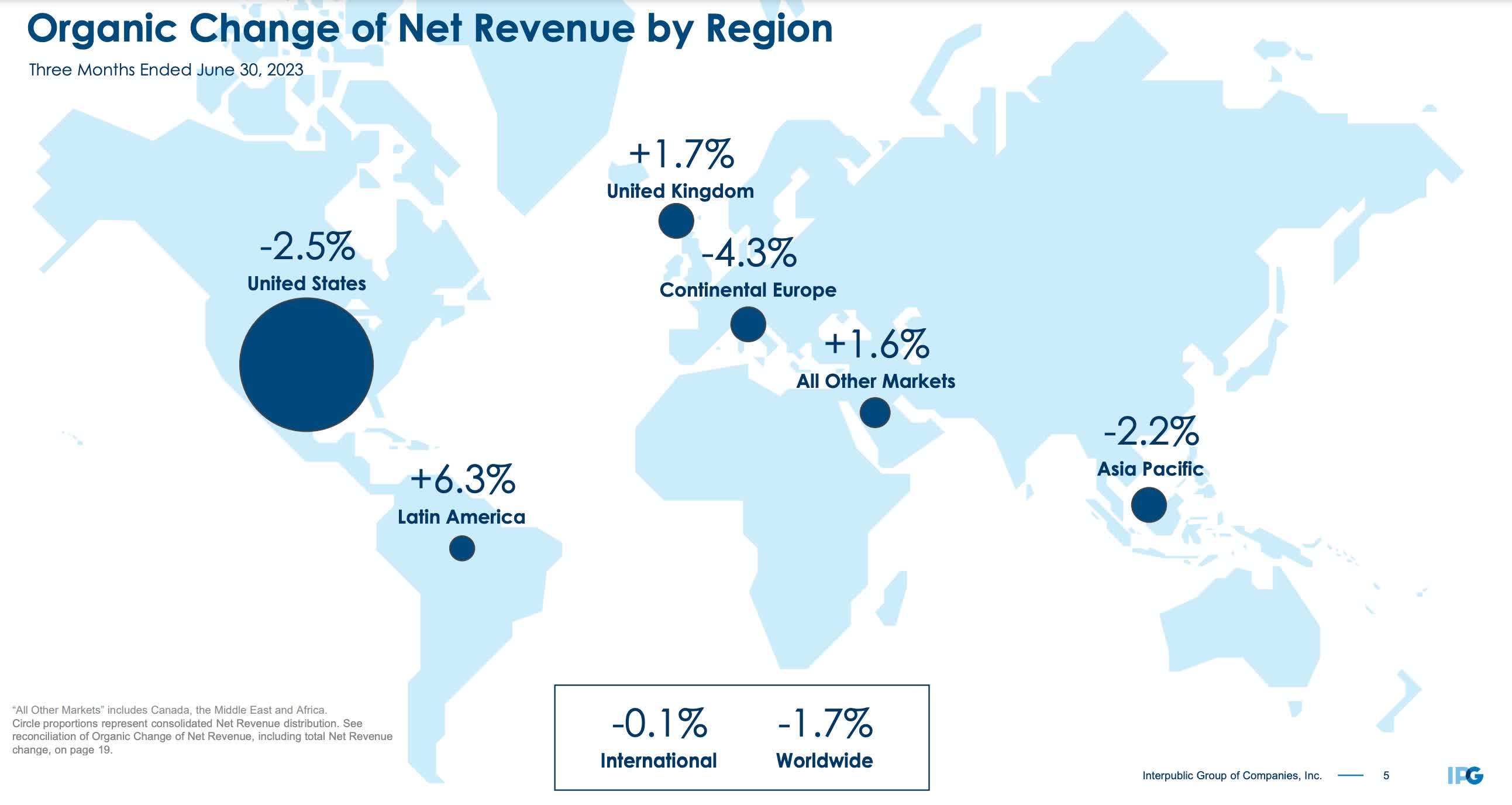

Regionally, the U.S. decreased 2.5 basis points organically while the international segment decreased by 10. The Media, Data, and Engagement segment (solutions) decreased 1.5% organically while the Integrated Advertising & Creativity Led Solutions segment decreased further by 3.8%.

{kind=link}

On a positive note, the company did report 3.7% organic growth in the Specialized Communications & Experiential Solution segment. Additionally, IPG reported growth in six of the eight client sectors along with the media offerings & the healthcare sector. They also expanded their relationship with pharmaceutical giant Pfizer (PFE), having been named the lead Global Creative Public Relations & Medical Affairs Partner. So, the company did have some wins in the first half of the year. And management expects this to be accretive in the second half of the year as it impacts earnings and revenue positively.

How AI Will Create Value Going Forward

Another way the company plans to grow is with the launch of Huge Live , a creative consultancy powered by human and AI collaboration. It is planned to accelerate the adoption of AI across the organization. And management expects this to have an impact on the industry as a catalyst for creativity. Furthermore, IPG also announced a partnership during Q2 with a leading quantum computer developer to build new software tools to solve complex data intensive problems. And the company continues to engage with AI innovators like Microsoft (MSFT), Alphabet (GOOG), and Nvidia (NVDA) to establish a matrix deployment strategy that will continue benefiting their clients going forward.

Share Buybacks

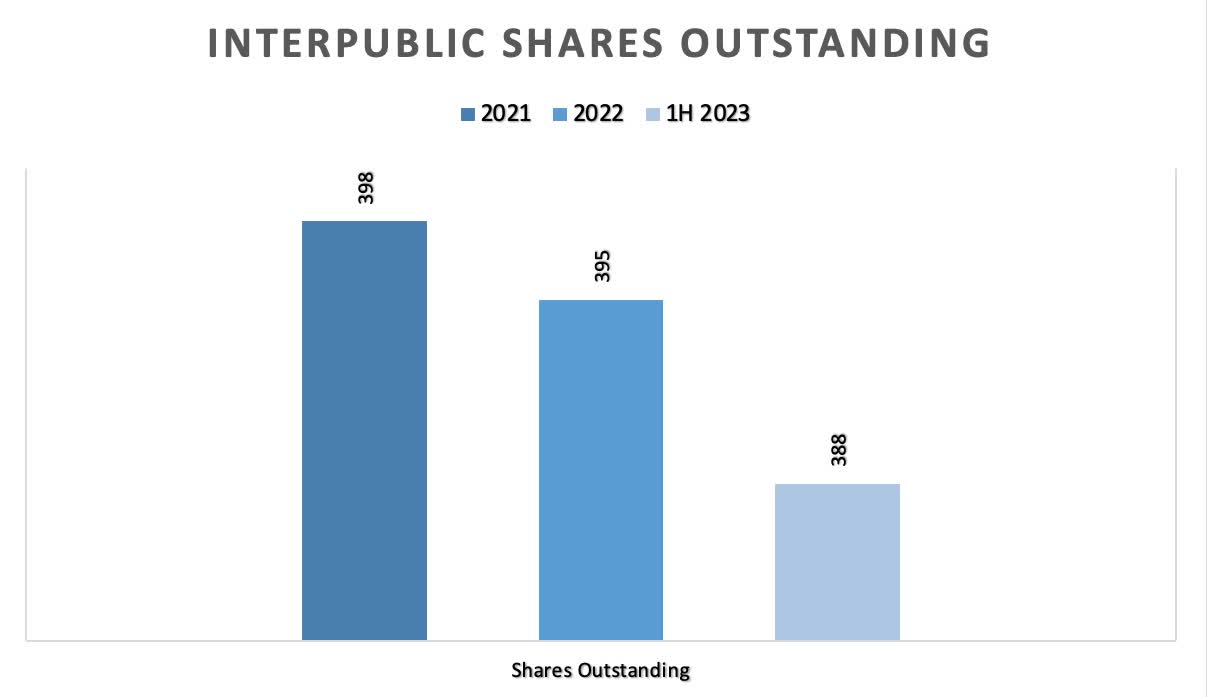

I can't think of one investor who doesn't like buybacks. Many often prefer for companies to buy back their own shares instead of paying a dividend. Companies like AutoZone (AZO), whom I wrote about recently, prefer to buyback shares instead of paying one. Something I like about IPG is that they do both. The company's ability to conduct buybacks in the current macro environment shows its strength. While many are seeing the high interest rates eat into their finances, IPG has been buying back its shares over the last few years. Below you can see the company's shares outstanding decreased by 10 million.

{kind=link}

Earlier this year in February, IPG's Board of Directors announced a new buyback program. This was in addition to any outstanding shares remaining from the one in 2022. One thing I like is that management did not put a time frame on the program like some companies. This is important because although repurchasing shares is great for shareholders, it may not be at opportune times depending on market conditions.

During Q2 IPG repurchased 1.3 million shares returning $50 million to shareholders in the process. For the first half of the year, they purchased a total of 3.5 million for $128 million and management plans to conduct additional purchases where they see fit. With higher for longer putting pressure on the market amongst other things, I expect management to repurchase plenty of shares if the stock continues to fall due to negative market sentiment. It is advantageous for the company to buyback its shares while they're cheap, and it also can send a signal that management thinks they're undervalued.

Low Debt & Improved Balance Sheet

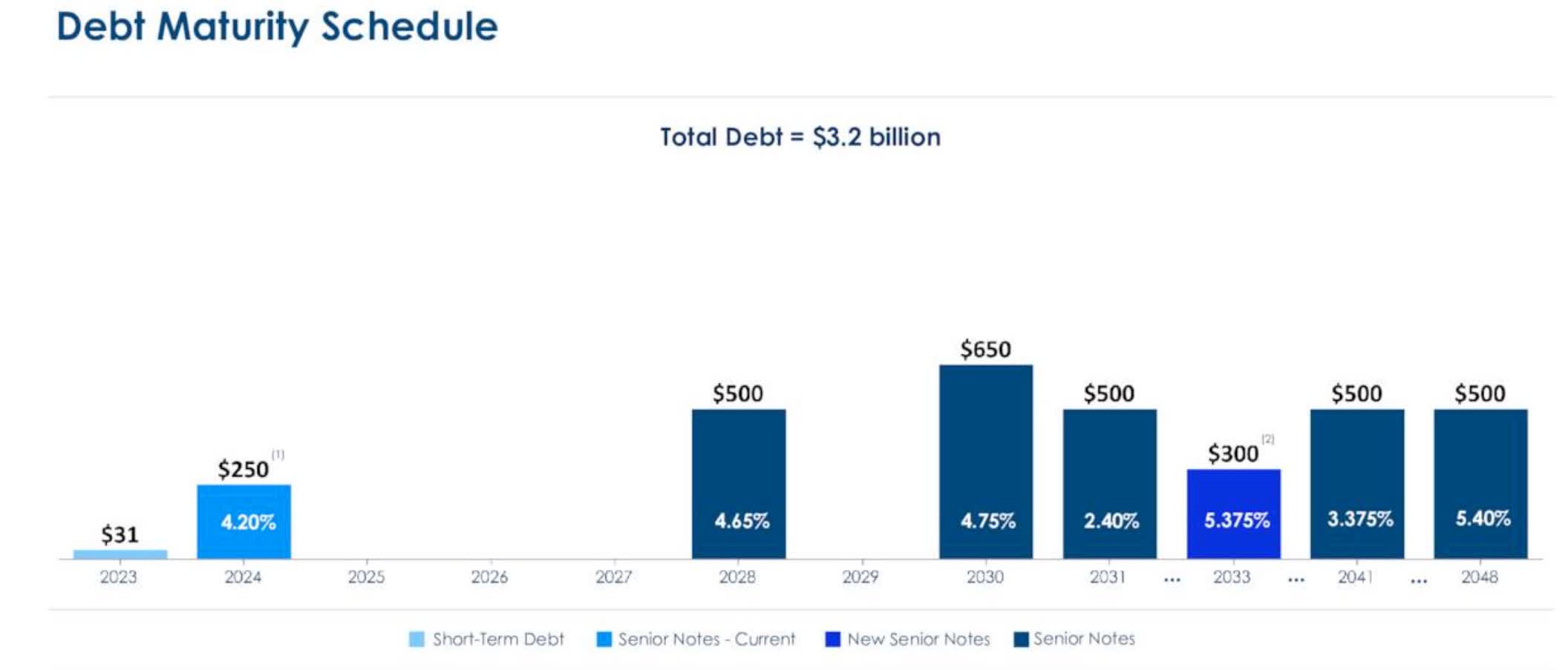

Besides conducting buybacks, the stock also has a very strong balance sheet. They have very little debt maturing with $250 million in senior notes due in April of 2024. Besides that, the company has no debt maturing until 2028. At quarter end IPG had a total of $3.2 billion in debt and $1.63 billion in cash & equivalents, meaning the company is well-positioned both financially & commercially. Furthermore, IPG has managed to decrease its debt from more than $4 billion during COVID to current. This is in comparison to their largest peer OMC, who's debt has increased slightly from $5.1 billion to $5.63 billion over the same period. So as many investors worry about several of their companies having to refinance a large chunk of their debt at higher rates, IPG is in a financially healthy position from a balance sheet standpoint.

{kind=link}

Dividend History & Earnings Growth

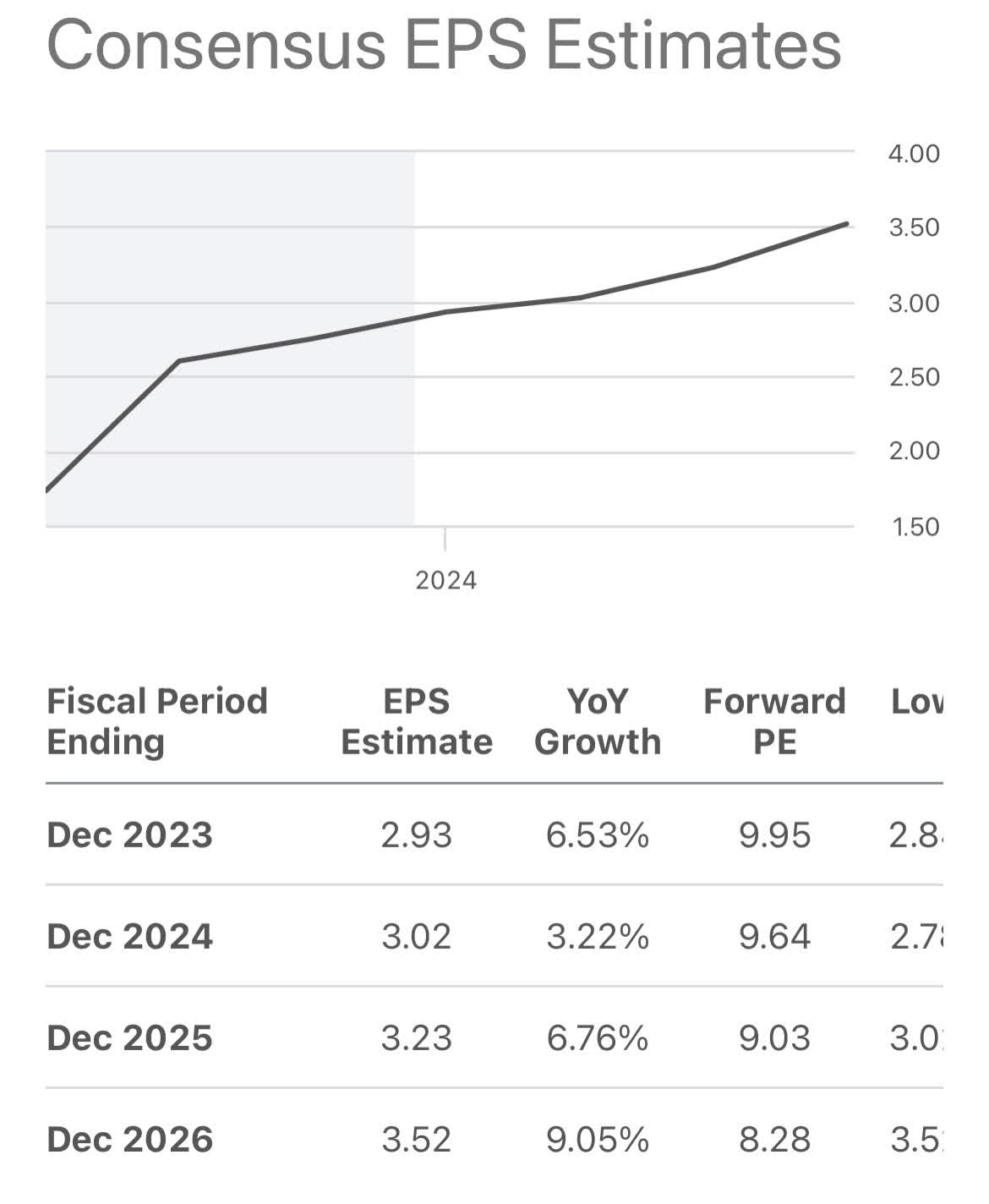

Earlier this year the company raised the dividend for the 11th straight year from $0.29 to $0.31. Since 2012 IPG has raised the dividend from $0.06 to its current dividend. Since the start of interest rate hikes, the company has continued to significantly out-earned its dividend and it currently has a low payout ratio of roughly 42%. EPS is expected to grow by 3% from 2023 to 2024, double to 6.5% from '24 to 25, and grow by almost 9% in 2026, giving shareholders some nice growth along with the buybacks the company regularly does.

{kind=link}

Valuation

At the time of writing IPG has a dividend yield of 4.26%, which is higher than its 5-year average of 3.89%. They also have a forward P/E of 10x, further indicating the stock may be undervalued. Investors with a long-term outlook should definitely consider IPG for their dividend portfolio as the stock is trading closer to their 52-week low. Furthermore, the stock offers significant upside to its price target of almost $40 a share.

For IPG I decided to use a discounted cash flow model. Although the company's FCF has declined in the last two years, I'm assuming the company will grow its FCF at an average growth rate of 3% going forward, and for it to remain flat over the next decade if we manage to evade a recession. Adding in their tangible book value which is negative, and expecting a 10% rate of return, this gives me a fair value slightly over $30.38, about 4% higher than the current share price.

{kind=link}

Risks

It's apparent the sector has experienced some headwinds in 2023 related to the current macro environment. Revenue decreased year-over-year and also missed analysts' expectations last quarter by a decent amount. A large part of this was due to significant cost-cutting in the relatively large tech and telecom sectors, impacting the stock's ability to grow. And although IPG continues to grow in other sectors, the heightened macro uncertainty will continue to pose challenges for clients going forward. Then there's the impact from the smaller clients on the company.

Although these clients have smaller cost cuts, they have added up over the course of the year, affecting growth for the company as well. This has caused management to revisit their full-year organic growth, and they now expect it to be between 1% and 2%. Although I expect IPG to continue to deliver beats on EPS, if the environment continues to face headwinds and fall into a recession, I expect revenue to suffer and lead to a further decline in share price.

Conclusion

Although I expect continued headwinds for IPG, especially in the tech & telecom sectors, now is a good time for investors looking to start a position to start dollar-cost averaging into the stock. IPG is a dividend champion that has rewarded its shareholders with buybacks over the years, returning cash to its shareholders including dividends. Currently the stock trades at a discount to its 5-year average P/E of 12.4x and offers double-digit upside to its price target of $38. Furthermore, the company has well-laddered debt maturities with minimal amount due in 2024 and ample liquidity. For those reasons, I rate IPG a buy.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Interpublic Group: Price Is What You Pay, Value Is What You Get