IITOF - Intesa Sanpaolo: A Clear Buy

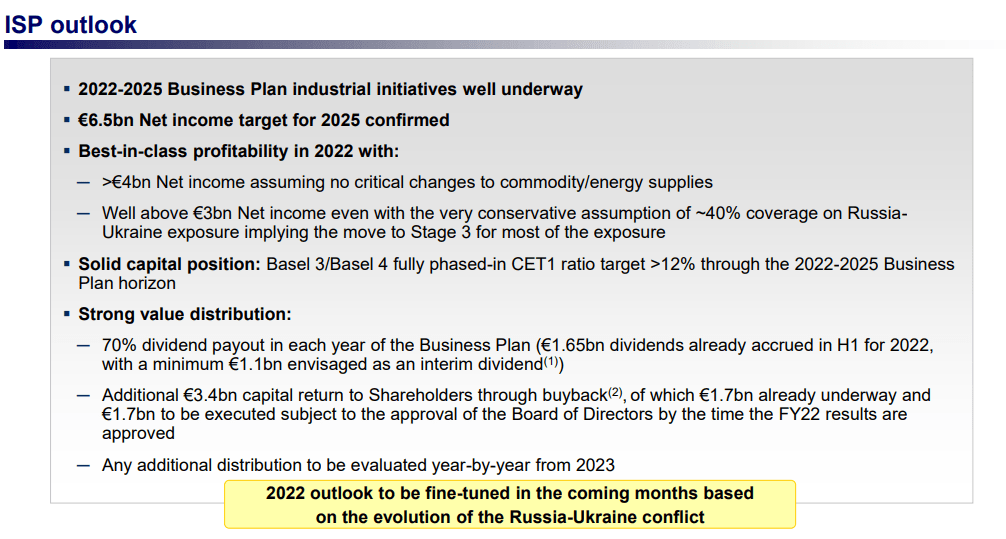

- Intesa Sanpaolo secures its exposure to Russia/Ukraine and confirms its 2025 industrial plan.

- Q2 net income was 30% above the analyst’s expectations.

- Best in class NPL and Cost/Income ratio, again a buy at this price level.

Well, we like Intesa Sanpaolo ( ISNPY ) - especially at this stock price level. Since our initiation of coverage (more than two years), our buy case recap still holds. At that time, we emphasized Intesa's dominant market position, a strong cost/income ratio and superior capital base requirements.

Looking at the just-released three-month numbers, it is evident how the company is still gaining market share despite a pandemic and an ongoing war is reducing operating costs and is well ahead of the BCE's capital requirement.

ISP cost/income ratio ISP CET1 ratio

{kind=link}

{kind=link}

Not a long time ago, we delved deeper into Intesa's Russian exposure providing some interesting considerations and initiating a new investment in the Italian leading bank.

Q2 Results

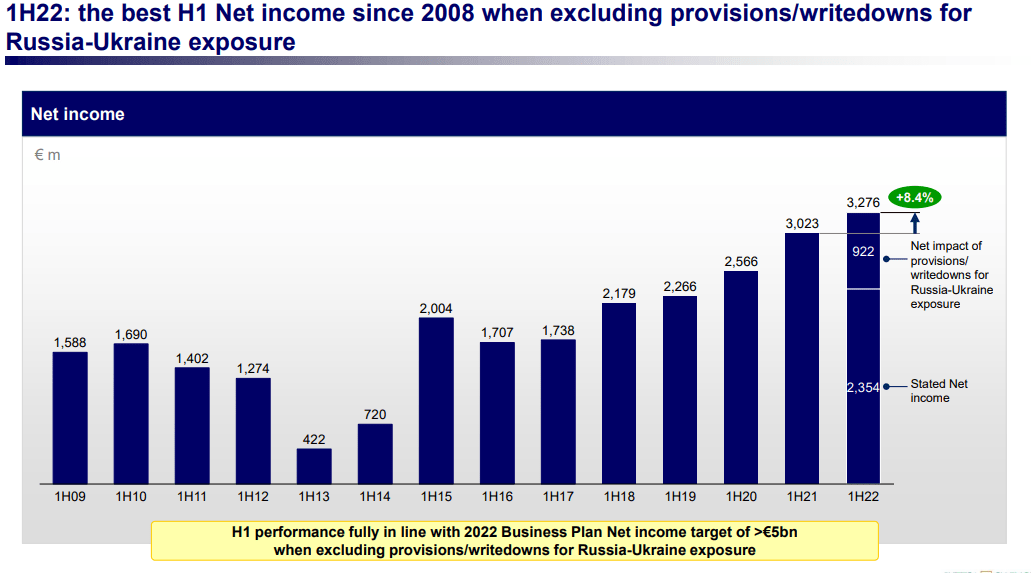

Starting from the bottom line, the bank recorded a net profit of €2.35 billion, after value adjustments of €1.1 billion related to write-offs for Russia and Ukraine. Without the latter amount, the last line of the income statement would have been €3.28 billion a plus + 8.4% compared to €3.02 billion achieved in the first half of 2021. These numbers were positively welcomed by Wall Street analysts.

{kind=link}

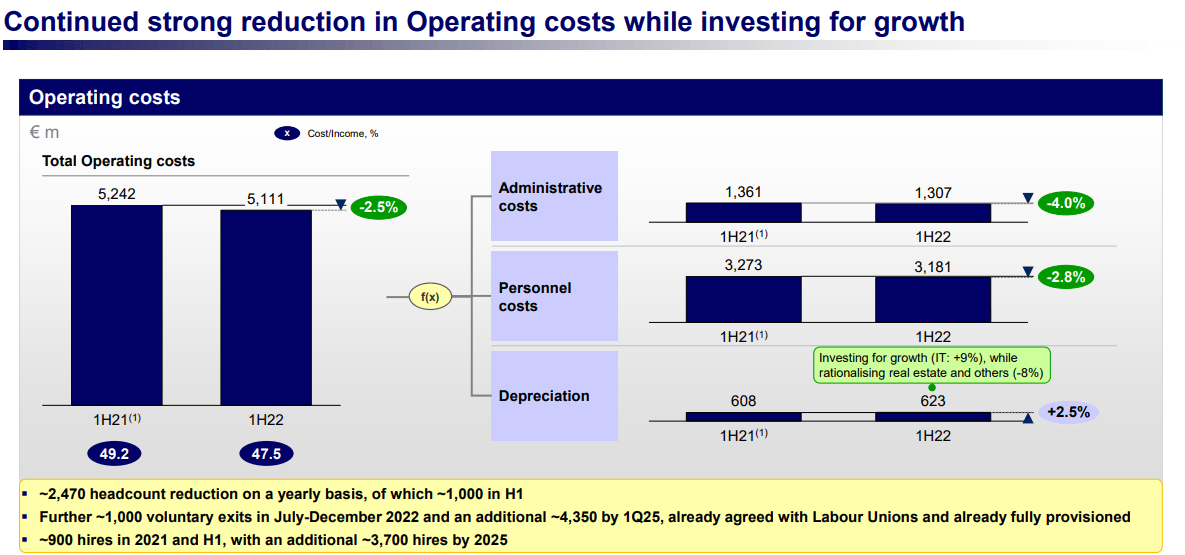

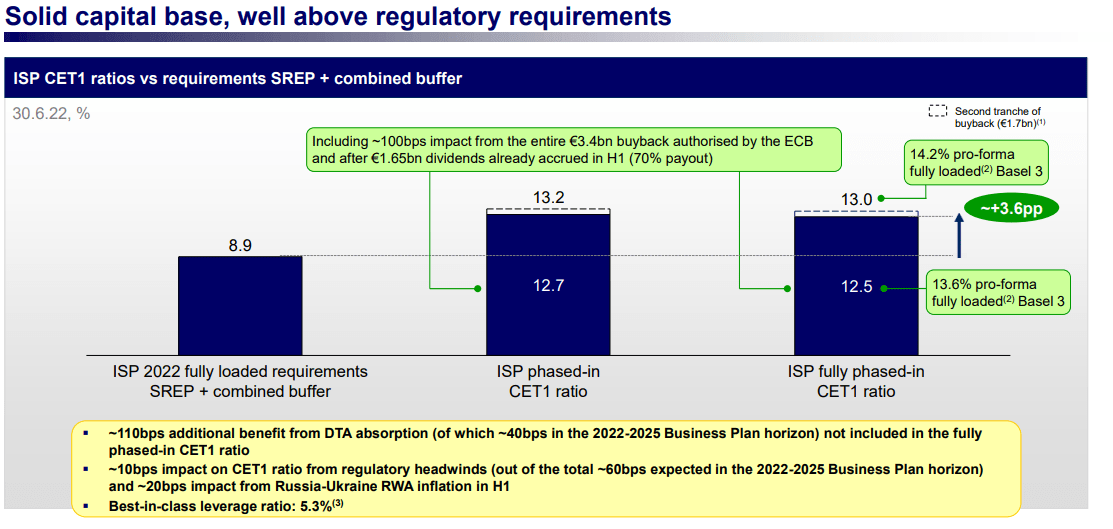

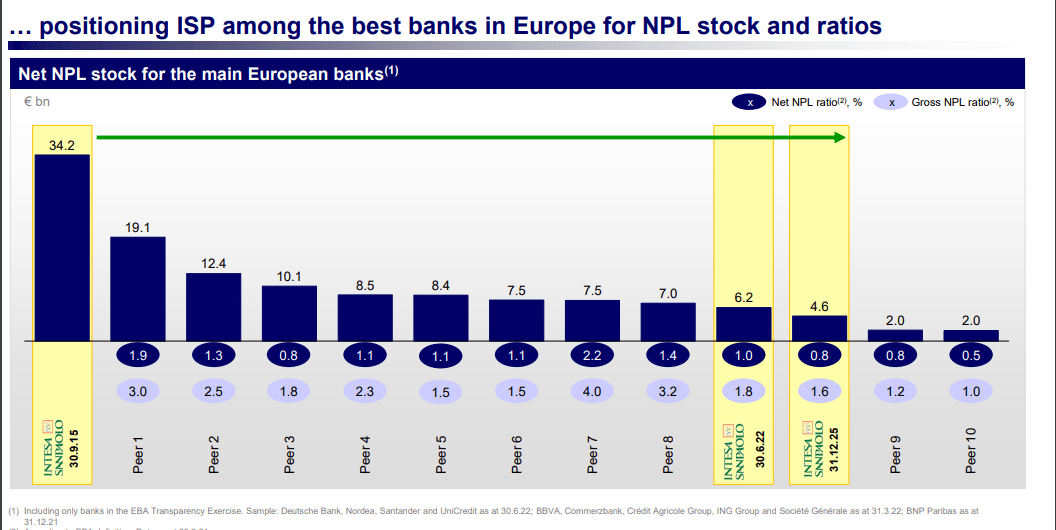

Getting back to the outcomes, Intesa Sanpaolo delivered positive numbers in almost all its operations with net operating income up 0.9% and operating cost down by 2% compared to the first half of 2021. The cost/income ratio now stands at 47.5% one of the best in Europe. Aside from the P&L considerations, we should also note how ISP is better positioned at the NPL level. ISP's asset quality is by far " better equipped " than its competitors to navigate future turbulences. The capital position is also solid with a Common Equity Tier 1 ratio of 12.5% ??when fully operational.

{kind=link}

Conclusion and Valuation

The Italian leading bank reaffirms its 2022 guidance and its 2025 industrial plan. All the objectives have been confirmed and also the net profit target of €6.5 billion by 2025. In Q2, net interest income was above consensus expectation by 7% and Intesa's profit was higher than estimates. There is a risk of deterioration for the Italian economy, but we are confident that the bank is now ready to tackle a challenging environment. In our previous note, we already adjusted the company's asset write-offs, so we continue to value Intesa at a price of €2.4 per share based on a ROTE of 13% and a long-term growth rate of 0.5%

The board also announced the distribution of €500 per employee. This was done to contrast inflation pressure and higher energy costs. The total amount of the intervention is estimated at €48 million.

{kind=link}

If you are interested, here is our view on the second biggest Italian bank.

For further details see:

Intesa Sanpaolo: A Clear Buy