ISNPY - Intesa Sanpaolo: Buy Before Earnings (Rating Upgrade)

2023-07-13 08:23:37 ET

Summary

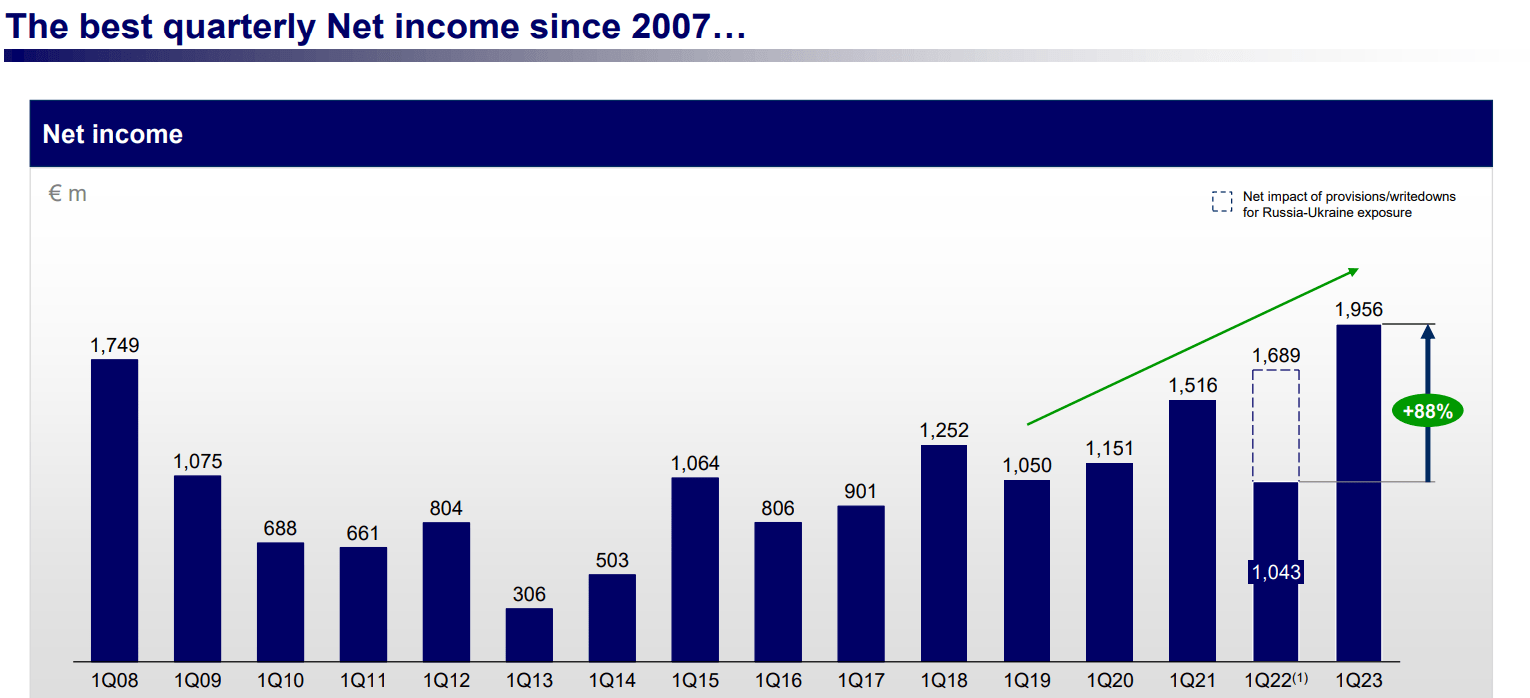

- Intesa Sanpaolo's shares are undervalued despite strong results and an improved short-term outlook, with the bank's net income reaching €2 billion, an 88% increase vs. 2022.

- Considering the current price of €2.4 per share, the dividend yield of Intesa Sanpaolo seems to be in the 11% - 13% range for arguably the most well-run Italian bank.

- Despite potential government intervention threats, I upgrade Intesa Sanpaolo shares to a "BUY" or Accumulate rating, with a target price of €3.4.

[Author's note: article refers to values in EUR and shares trading on the native Milan Stock Exchange under the ticker ISP.MI unless otherwise explicitly stated]

Following my last coverage in March, I am picking up Intesa Sanpaolo ( ISNPY ) again for a deep dive into the company's prospects ahead of the bank's mid-year results release. I have had a "Hold" rating in place for Intesa Sanpaolo, mainly because I believe the long-term trend for Italian banks remains challenging. As I stated in my prior analysis, macro factors outside Intesa's control could easily eat into the bank's profits, and I am particularly wary of the government's possible actions. In March, I floated the idea of a mortgage jubilee or the forced swallowing of troubled bank MPS because the economic outlook appeared weak. However, as we progressed the year on solid corporate results and eased fears of a recession, that scenario seems now unlikely. With Italian households holding up well to the increase in mortgage rates and banks showing record Q1 profits, Italian media is floating the idea that the government could instead impose a surtax on bank profits. While this is an apparent potential negative still weighing on Intesa shares, the bank's lackluster stock performance, despite a much improved short-term outlook, means shares have become too underappreciated by the market.

The quarterly results and FY forecast

Undoubtedly, the bank has been delivering strong results, with net income reaching approximately €2 billion, an 88% increase vs. 2022.

{kind=link}

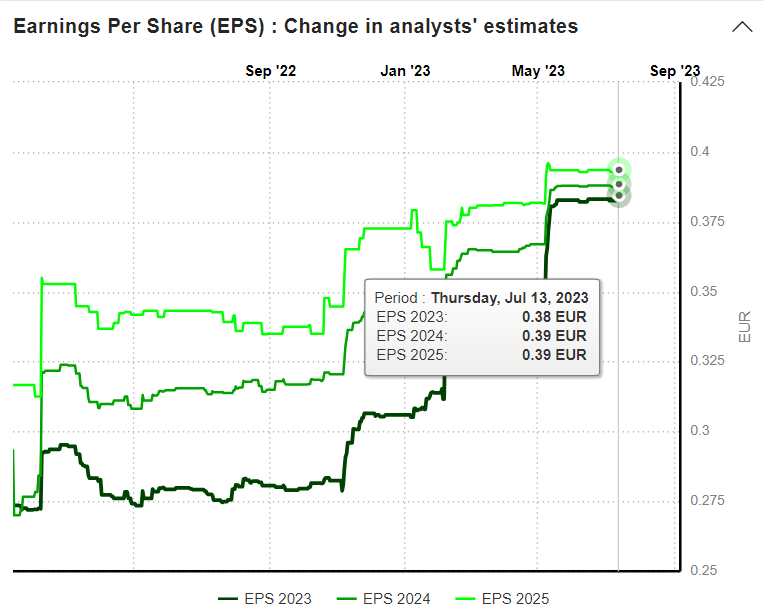

The bank also bolstered its FY23 net income guidance, moving from (above) €5.5 billion to (about) €7.0 billion. Intesa's outstanding shares are (as of June 2023 ) in the 18.3B region, which means that if Intesa achieves its guidance, we are looking at about (7/18.3) €0.38 EPS for FY23. Analysts are playing catch-up here and have revised estimates upwards several times in recent months, but they seem to agree with management. The latest consensus figure I retrieved (see chart below) supports the €0.38 assumption. However, analysts have been lazy, in my opinion, by passively accepting the company's conservative guidance.

{kind=link}

Intesa has an aggressive buyback plan in place which, starting from this Month through October, plans to repurchase shares for up to €1.7 billion. Even assuming an average price of €2.7 per share (12.5% higher than the current price), the company could retire about 630M shares before the end of the year, equal to 3.5% of the total. The repurchase plan alone could impact results positively by almost €0.02, lifting Intesa's FY EPS to €0.40.

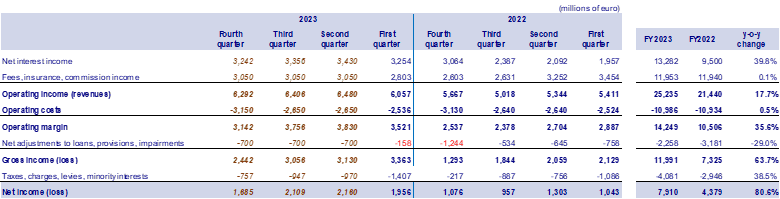

But there is more. The €7 billion guidance still seems conservative and factoring in a mild recession in H2 2023. I rerun the numbers, and I believe Intesa has a clear path to close the year higher, booking profits for almost €8 billion. While I think NII will be peaking in Q2 2023, a potential contraction in H2 won't be severe. From there, Intesa just needs year-on-year flattish fees and insurance income (for a total of €12 billion) to book revenues of more than €25 billion.

With almost flattish operating costs, the company can maintain an FY23 cost-income ratio of 43%-44%, increase its margins by 36%, and achieve north of €14 billion in operating margin. Net adjustments for the year should no longer include the large charge booked in 4Q22. Even assuming provisions of €0.7 billion for the following quarters, the FY total should be lower than in 2022.

{kind=link}

If Intesa achieves this more bullish forecast, FY23 EPS could increase to €0.45 per share, meaning shares are currently trading at only 5.3x FWD earnings.

The valuation

I believe shares are worth at least 7.3x, pointing to a potential fair value of €3.4 per share and approximately 40% upside from the current levels. This price is also roughly in line with the €28 target I recently assigned to Intesa's main competitor and peer, UniCredit ( UNCRY ), which would also value the bank at approximately 7x fwd earnings. Intesa is, in my opinion, a higher quality institution and deserves a slight premium compared to UniCredit. Still, it would be hard to justify the bank trading at significantly higher multiples than its closest peer.

As a diversified bank, Intesa owns assets that analysts routinely highlight as being undervalued. Eurizon, the asset management arm of Intesa, is one of these. BlackRock ( BLK ) reportedly tried to acquire a 30% stake in 2018, but the talks stalled, and the acquisition ultimately went cold . Eurizon reported a net income of €570 million for FY22. Considering listed peers Amundi ( AMDUF ) and Anima Holding ( ANNMF ) command higher P/E multiples than banks at approximately 10x-12x, Eurizon should be worth at least €6 billion standalone.

Another one could be Isybank, the digital bank of Intesa Sanpaolo just launched last month. If Intesa plays its cards right, there is undoubtedly some value to unlock here, but it is still too early to tell how this will fare. Peer Illimity Bank (, listed in 2019 and run by former Intesa Executive Corrado Passera, has a market capitalization of about €0.5 billion, and shares have gone sideways since its IPO.

However, pioneer online-first bank FinecoBank ( FNBKY ) is arguably a gem in the Italian banking sector. Listed in 2014, the company has grown capitalization over 3x since. From an IPO value of €2.7 billion, the bank spun off from UniCredit as a non-core asset (a fate that Isybank one day might share) and now capitalizes more than €8 billion on the Italian stock exchange. If Isybank can repeat the successful case study of Fineco, Intesa could stand to book a nice profit, as UniCredit did .

The dividend

The bank seems well suited to fit in an income portfolio, with generous payouts distributed to shareholders. As a general policy, the bank plans to allocate 70% of its net income to dividends, with the rest allotted by management freely to a mixture of buybacks, special dividends, or growth purposes. So, in connection with the €2 billion earned in 1Q23, Intesa already booked €1.4 billion accrual for dividend payment. Based on management guidance, Intesa should be able to pay (next year) at least €0.38 x 70% = €0.265 in DPS. Under the more bullish scenario I highlighted, the payment could stretch to €0.45 x 70% = €0.315 per share. Considering the current price of €2.4 per share, the forward dividend yield of Intesa Sanpaolo seems to be in the 11% - 13% range for what is arguably the most well-run and strongest diversified bank in Italy.

The risk

Besides the already-mentioned government intervention threats, Intesa (and other Italian banks) will likely face challenges in maintaining its net interest income beyond 2023 because NII has grown due to net interest margin expansion rather than organic growth in lending. I believe such a large spread can't last.

Intesa's model should, in theory, be safe from a shock similar to the one hitting earlier in the year US regional banks. The liquidity coverage ratio stood at 176%, with retail funding (guaranteed by the local Deposit Guarantee Scheme) covering about 83% of the bank's needs. However, the problem is that Italian bank accounts typically do not earn any interest. Even with the ECB's deposit rate of 3.5%, Italian banks stubbornly refuse to pay anything to account holders. Inflation has, however, hit Italy as much as the other EU countries. Italians are painfully discovering at their expense that leaving money asleep in their bank accounts earns real negative returns. While the few financially savvy have already found alternative solutions, most have yet to make a move. Still, deposit accounts and government bonds are slowly making their way back into Italians' portfolio allocations, and the action will drain banks' oversized NII.

Closing remarks

Despite the lingering uncertainties, I am upgrading Intesa Sanpaolo shares to a "BUY" or Accumulate rating, with a target price of €3.4. The stock is too cheap to ignore. Further upward earnings revision could come just after the Q2 earnings release and act as a catalyst, accelerated by the company's ongoing buyback plan. I also see good momentum with positive Quant and Street ratings and strong factor grades supporting the bull case.

Seeking Alpha

Even if I see a high short-term return correlation with UniCredit, which I also rate as a "Buy," I favor Intesa as the better pick for income investors. The company's straightforward shareholders-friendly policies include a 70% dividend payout ratio, allowing Intesa to consistently rank among the top-yielding firms listed on the Italian stock exchange. While I see favorably some buyback activity as well, I argue that centering investors' return on share repurchases like UniCredit is currently doing is a risky policy in banking. Banks are sensitive to economic shocks and prone to capital raises during recessions. Hence, I believe the capital allocation policy of Intesa Sanpaolo is reasonably superior to UniCredit's one. Even if such a strategy means higher taxes, a bird in the hand is worth two in the bush.

Also, Intesa has historically proven to be a more resilient institution with well-run insurance and asset management divisions. While UniCredit has a broader footprint in the EU area, I do not believe this to be an advantage.

For further details see:

Intesa Sanpaolo: Buy Before Earnings (Rating Upgrade)