IITSF - Intesa Sanpaolo: Great Bank Weak Macro Outlook

2023-03-23 11:12:32 ET

Summary

- Intesa Sanpaolo is the most important Italian banking group and operates a diversified bank in Italy. The group also has a small yet profitable exposure to developing Central-Eastern Europe countries.

- The bank is well-run and there is little risk that the ongoing problems in US banking will spread to Intesa Sanpaolo.

- Despite its banking business being solid, there are macro-driven and country-specific risks that give me pause and prevent me from issuing a strong buy rating.

- I see Intesa Sanpaolo shares currently close enough to their fair value. I would want a bigger discount to accept the risks.

Important note: Unless otherwise specified, I will refer in the article to the primary and most liquid, EUR-based listing of Intesa Sanpaolo on the Milan Stock Exchange [BVME: ISP]

Intesa Sanpaolo (ISNPY) (IITSF) is gaining increasing attention from Seeking Alpha investors due to its excellent factor grades, which highlight the bank's potential for delivering outsized returns. The company has been featured in a couple of SA News articles, most recently on March 20th, where it was listed among the top 10 financial stocks to hold during the banking crisis . Although I currently do not own any shares of ISNPY, I have previously invested in the company and have covered it on Seeking Alpha in the past. While I am not well-versed in technical indicators, I am fully aware of the bank's valuation and growth potential. Therefore, I believe that the SA system has helped to uncover a hidden gem for international investors.

Seeking Alpha

Bank's geographical and operational footprint

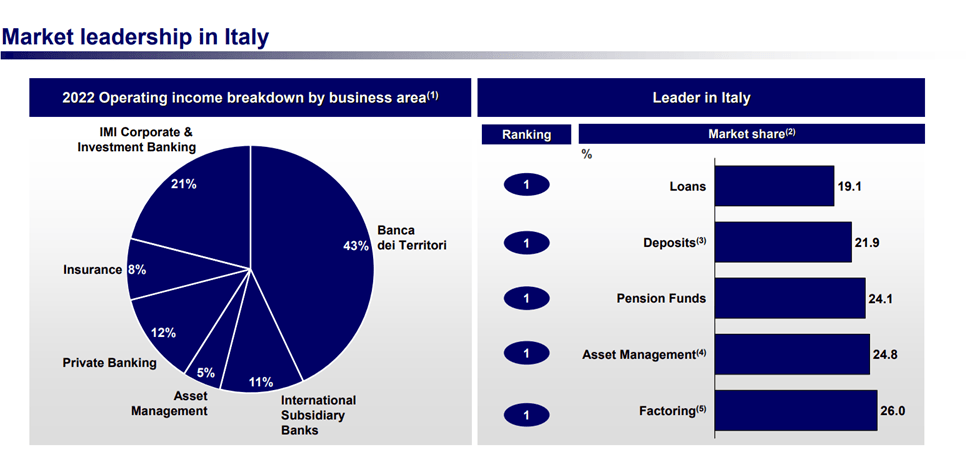

For those who are new to it, Intesa Sanpaolo is the most important Italian banking group, formed in 2007 by the merger of Banca Intesa and Sanpaolo IMI. Headquartered in the beautiful city of Torino, Italy, the Group operates a diversified bank in its home country, where it is the market leader in loans, deposits, asset management, pension funds and factoring. In Italy, Intesa Sanpaolo also offers insurance solutions and investment banking services.

Despite its geographical focus, the group also has a small yet profitable exposure to developing Central-Eastern European countries (mostly in the Balkan region) and Egypt, which contributed 11% or 610 million EUR to the bank's overall 2022 operating income.

{kind=link}

What to like in Intesa Sanpaolo

The investment case in Intesa Sanpaolo has not changed much since I last covered this stock. The company has performed well, going unfazed through the pandemic, and returning significant amounts of capital to shareholders in the form of dividends and buybacks. Although it wasn't a home run, my investment idea has performed as well as the SP500.

Seeking Alpha

I liked the bank back then, and the main reasons for an investment are mostly the same today:

- Strong operational performance. The company has spent the better part of the last decade emerging from the disastrous NPL situation Italy was facing after the Great Recession. It was not an easy task, but Intesa Sanpaolo went, in a relatively short time, from being a troubled bank to a role model and its current NPL stock is below most peers in the whole continent.

- Carlo Messina, ISNPY CEO, remains a key company asset. Messina has been voted five-times " best CEO of a European bank " by an institutional investors survey, and " CEO with the best online reputation " by an independent observatory for managers reputation. Messina has a very strong operational record, overdelivering on both the bank's strategic 2014-2017 and 2018-2021 plans. So far, developments have been positive for the ongoing 2022-2025 plan as well.

- The asset management division (Eurizon capital SGR) is a crown jewel asset of Intesa Sanpaolo and has been at the center of M&A chatter in the past. Eurizon is highly profitable and well-integrated in the bank's organization, with significant operational synergies from cross-selling opportunities. Italy remains an aging country with little financial literacy and most Italians see their private banking referents as their go-to investment advisors as well.

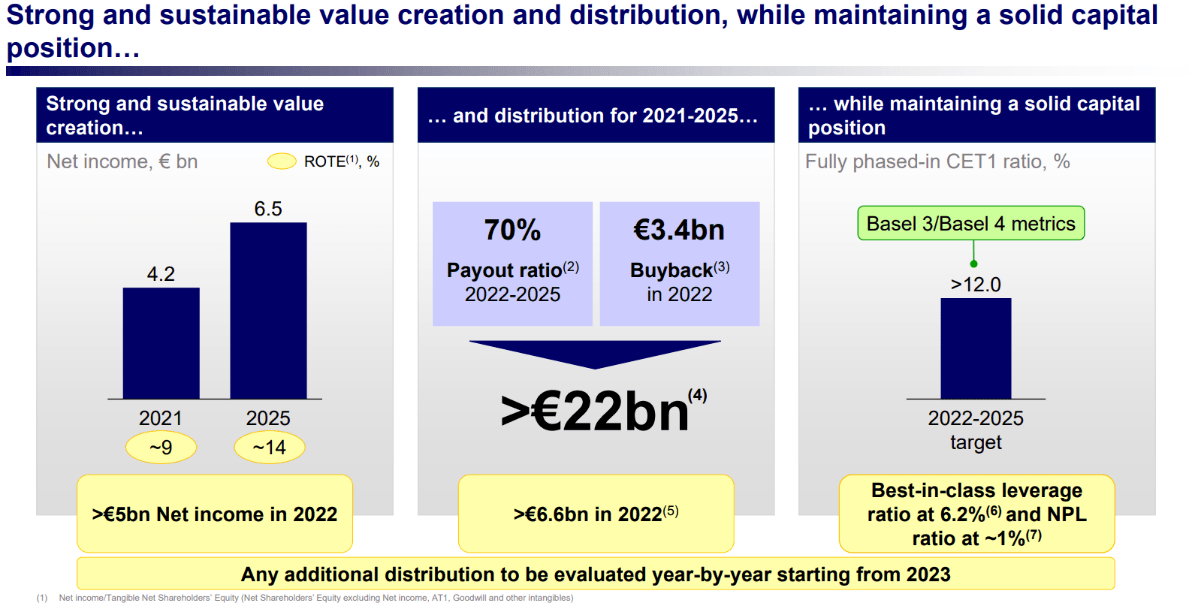

- Fully loaded CET1 ratio decreased from 13.9% in 2019 to 13.0% at the end of 2022 but remains well ahead of the regulatory compliance level (8.9%) set by the ECB. The bank has launched an aggressive share buyback plan, repurchasing 1.6 billion EUR worth of its common stock in 2022, equal to more than 3.5% of its market cap. Intesa plans to continue its buybacks and retain a CET1 ratio above 12% through 2025.

- Friendly shareholder policies. The bank paid out a total 5 billion EUR to shareholders in 2022 including 3.4 billion EUR in dividends. This is a payout ratio of approximately 115% on net earnings of 4.3 billion, but only 90% when excluding for the 1.2 billion non-cash provision the bank had to register in connection to the exit from its Russia/Ukraine operations.

- Attractive valuation with P/B ratio at about 0.7x. The market is arguably still questioning the quality of ISNPY's loan book, but the bank has demonstrated its ability to keep non-performing assets under control during Messina's tenure.

Ongoing US banking issues unlikely to affect Intesa

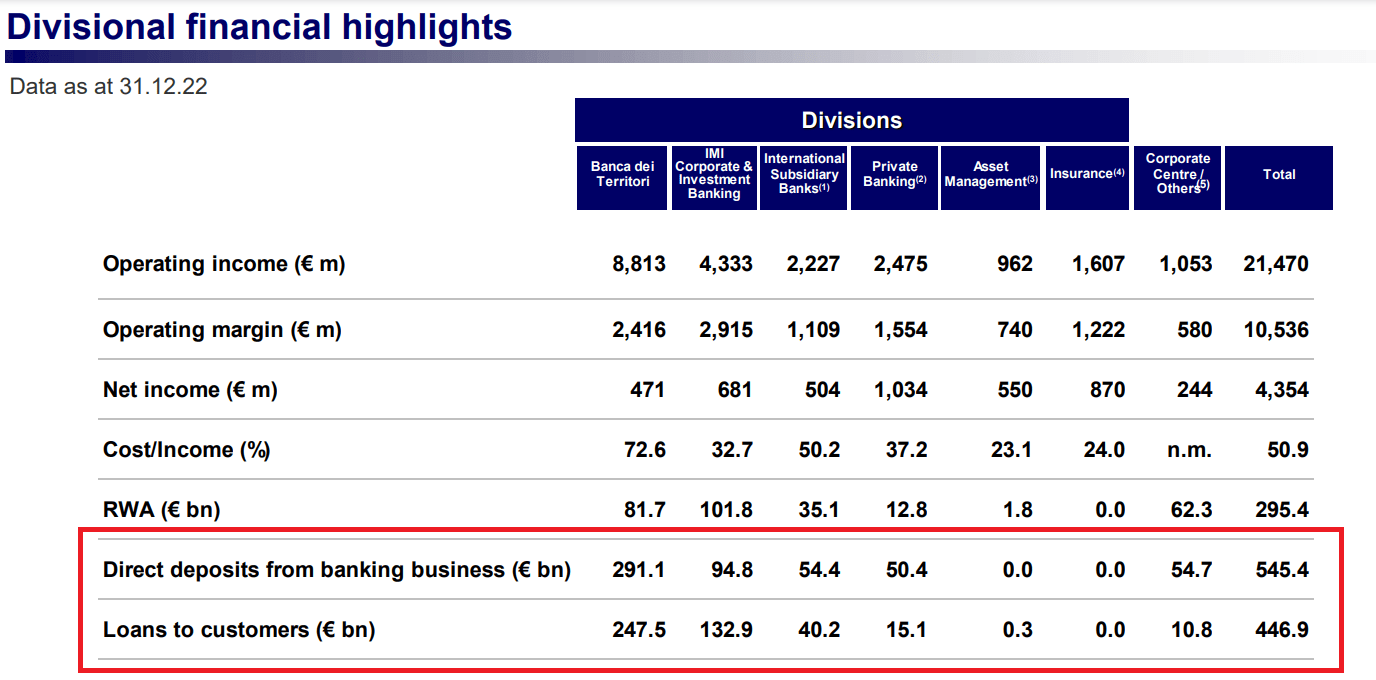

DBRS Morningstar has pointed out that European banks, compared to those that failed in the US, have several advantages, including a generally lower exposure to fixed-income securities, more stable retail deposit bases, and a regulatory framework that includes stricter interest rate risk management policies, even for smaller banks. By no means do I see a "bank run" happening in Italy. But even if such scenario played out, similarly to what happened in the US, Intesa Sanpaolo would likely be a net beneficiary of the "flight to safety" from his position of market leader in the country. At the end of 2022, ISPNY's total deposits exceeded loans by 100 billion EUR.

{kind=link}

The situation may differ in other jurisdictions where ISNPY operates, but as shown in the table above, Intesa Sanpaolo's exposure is only about 40.2 billion EUR, which is less than 10% of its total loans. This is too small to cause any significant concern. The market sentiment seems to support this view as well. Although Intesa's stock price has recently declined in line with broader market indexes, its decline has not been comparable to some of its US industry peers.

Risk factors

That said, I see several risks in the shares. Most of these risks are macro-driven and country-specific, rather than related to Intesa Sanpaolo as a business, making them harder to correctly evaluate and reflect in a grading system. This could be the reason why I am somewhat wary of investing in Intesa Sanpaolo now. After liquidating my position for a decent profit last year, I have remained on the sidelines. To be fully clear, I have little doubt that Intesa Sanpaolo is the highest quality Italian financial institution. It is stronger than its direct competitors, it is highly profitable and has great management. It also pays a nice dividend, that should be close to 7% yield based on this year's projection of 0.1606 EUR per share . That said, despite a bullish quant rating, I cannot see a catalyst that could send the shares materially higher in the short-term.

The Italian economy remains on shaky ground, with Italy's GDP growth rate among the worst in the entire Eurozone, even during times of economic prosperity. Structural reforms are urgently needed, yet the country's well-earned reputation for being ungovernable has hindered any real progress. Various governments have come and gone in the span of five years. Recent political reforms going by dubious names, such as the recently voted " incremental flat tax " can only add further skepticism in any sane-minded person. There is little hope that the current populist PM, Giorgia Meloni, will make a significant change. These developments, combined with the overall uncertain economic outlook, make me cautious about investing in Intesa Sanpaolo.

Given the circumstances, I believe Intesa's policy of returning 100% of ongoing earnings to shareholders is appropriate. Despite the challenging environment, Intesa's plan to grow net earnings from (adjusted) 5.5 billion EUR in 2022 to 6.5 billion EUR in 2025 is impressive, representing a satisfactory CAGR of almost 6%. Although much of this growth is expected to come from cost-efficiency initiatives and an increase in ROTE from 9% to 14%, rather than organic growth

{kind=link}

Considering past ROE trends, I see high execution risks here, even for a seasoned leader like Messina. However, there is another risk that is particularly difficult to price in, and that is the political risk. While Intesa Sanpaolo is a well-run market leader, what would happen if the Italian government called upon it to rescue a sub-par competitor? I have no doubts about Intesa Sanpaolo's ability to avoid becoming another Credit Suisse ( CS ), but I worry that it could risk entangling itself in unwanted business transactions like UBS Group ( UBS ). In recent years, Intesa Sanpaolo and other Italian banking groups have repeatedly ruled themselves out of M&A speculation regarding the acquisition of troubled bank MPS ( OTCPK:BMDPF ). The government has decided to play ball since the overall economy is afloat, but in the event of a recession, it is harder to foresee what could happen.

It is possible that the government may not mandate any banks to take over MPS to avoid contagion risks. However, there are other measures that a government could take that could potentially harm banks. A populist government, for example, may force banks to take losses in various ways. An instance of this occurred in Poland with the recent mortgage payments jubilee . It appears that the EU and ECB did not have much influence over the situation, and it is reasonable to assume that similar events could occur in other EU countries.

Valuation

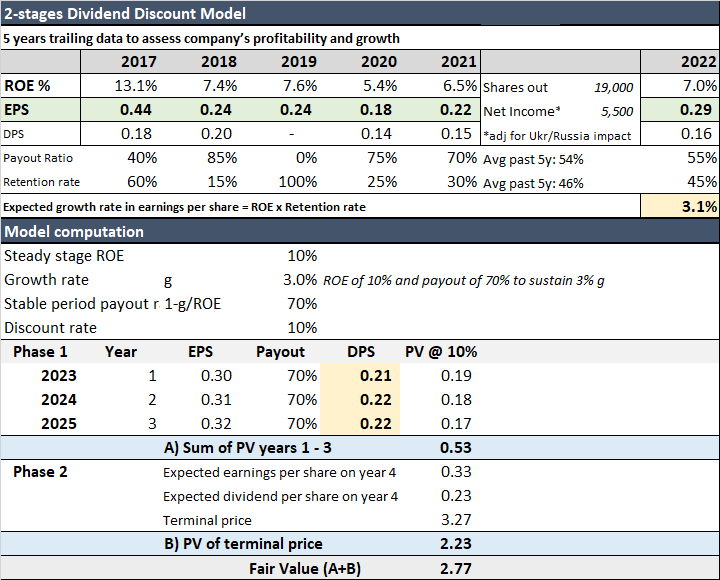

I will now attempt to reassess Intesa Sanpaolo fair value using the same 2-stage dividend discount model I used back in my 2019 article . It is arguably not the most precise methodology but has served me well in the past for a "quick and dirty" valuation of financials.

Compared to 2019, I tweaked the discount rate upward, as capital is now more expensive. I also adjusted this FY2022 EPS to exclude for the one-off impact of Russia/Ukraine write-offs. Based on a sustained 70% payout ratio, I expect the company's long-term growth potential to be fairly limited to 3%. To achieve it, Intesa Sanpaolo will have to improve its ROE, which is a clear objective stated in the company's 2022-2025 plan. I am willing to give some latitude to the management here and factor in such improvement based on Messina's track record, though I certainly see some execution risk.

{kind=link}

The result is a fair value of approximately EUR 2.77 per share, suggesting Intesa Sanpaolo is modestly undervalued against current market price of EUR 2.34.

Conclusion

Despite a nice dividend, a potential 18% upside and no clear faults of its own, I do not feel ready to issue a buy rating for Intesa Sanpaolo at this moment. Call me overly pessimistic on the prospects of my own country, but even if I see no problems from the ongoing US banking crisis, I see too many country-specific risks floating around as Italy likely enters an economic downturn in 2023/2024. With risks such as the political one very difficult to price in, I would remain on the sidelines until I see an improvement of the macro outlook or a larger discount before upgrading my rating.

For further details see:

Intesa Sanpaolo: Great Bank, Weak Macro Outlook