IITSF - Intesa Sanpaolo: Higher Guidance And 4 Reasons To Remain Bullish

2023-11-15 11:27:40 ET

Summary

- The best nine months ever in operating margin, NPL, and cost-income ratio.

- Russia's exposure was further reduced below 0.2% of the total bank's customer loans.

- Higher shareholder distribution, including buyback. Better-than-expected numbers with a guidance step-up. Our buy rating is then confirmed.

Today, we are back to comment on Intesa Sanpaolo ( ISNPY ) numbers. Here at the Lab, there are four additional reasons why we should keep overweighting the leading Italian bank. Before going into the details, we will update our readers on the Q3 results to provide a better estimate of the bank fundamentals. Then, we will move on with our updated valuation. As a reminder, Intesa Sanpaolo has always been Our Favorite Italian Bank due to 1) scenario analysis on interest rate evolution with a Net Interest Income Development Not Priced In , 2) a tasty dividend yield combined with a best-in-class cost-income ratio, and 3) a solid balance sheet supported by a CET1 evolution. In addition, looking back to our buy rating, we reiterated our overweight after the Russian/Ukraine conflict, confirming that the bank has limited exposure in the area.

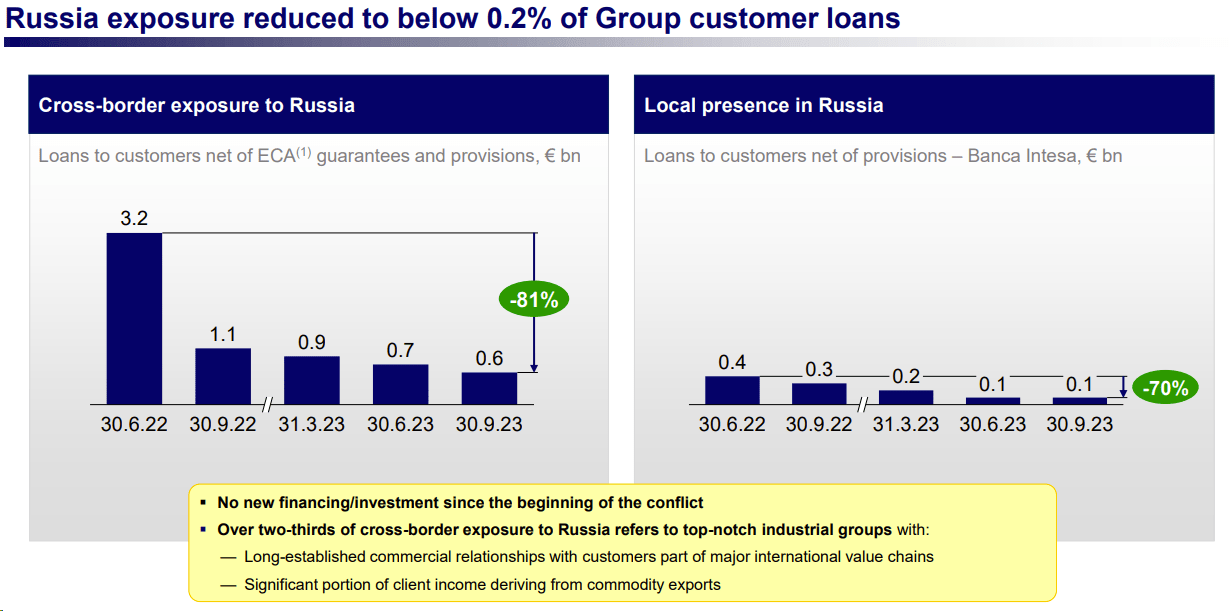

Intesa Sanpaolo's Russian Exposure

{kind=link}

Q3 Results Comment and Change in Estimate

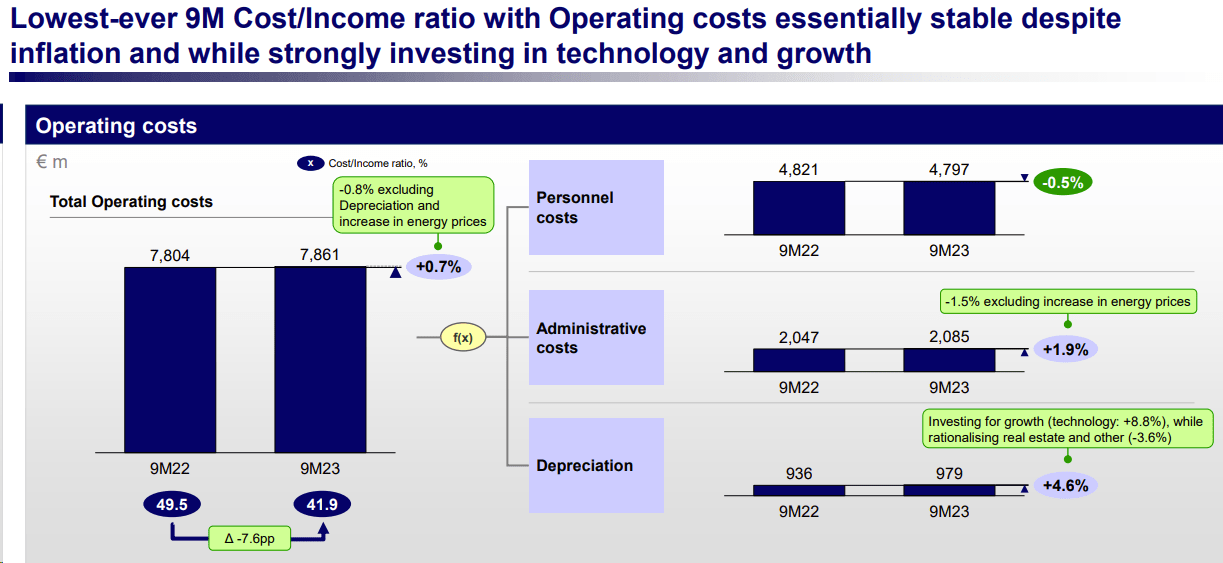

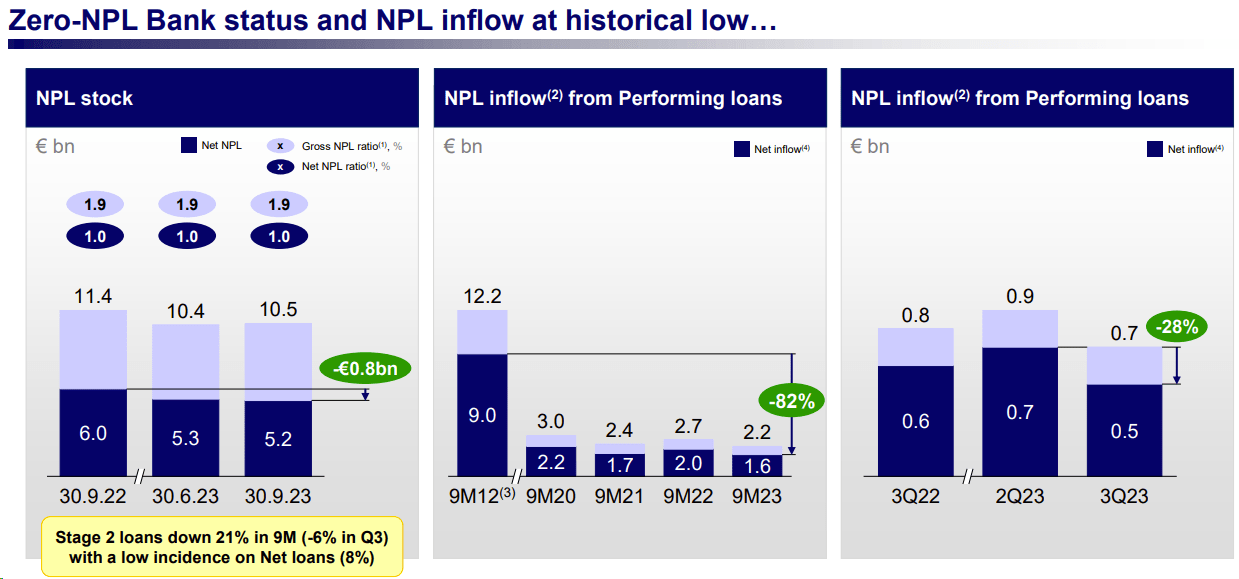

Looking at the Q3 numbers, we could not be more than satisfied. The company published robust results in the quarter, with a net interest income that beat Wall Street expectations. The company reported the best quarter ever at the operating margin level. In light of these solid performances, Intesa Sanpaolo upgraded its Fiscal Year 2023 net interest income guidance to €14 billion. The bank reported an operating income of €6.4 billion driven by NII output (plus 6.4% quarterly) and above 6% vs. consensus. On a negative note, commissions and insurance income were down by 5.5% and 8.7%, respectively. The bank's operating costs slightly increased to €2.65 billion, but they were down by -0.9% quarterly due to lower admin and personnel costs. With these positive results, the bank cost-income ratio reached 41.9% at the nine-moment level (Fig 2), confirming its leading position in Europe. Moving on to the balance sheet analysis, the bank continues to lower its non-performing loan, further reducing Russian exposure. In the quarter, the bank recorded its lowest-ever net NPL stock with a coverage ratio of 1.4 basis points every quarter (Fig 3). The cost of risk is also down to 28 basis points at the annualized level and a liquidity ratio at the highest level. The fully phased CET1 ratio reached 13.6% and was ten basis points lower than Q2. This was due to a one-off windfall tax allocated as a non-distributable reserve; however, CET1 is well above the regulatory requirements (8.8% SREP).

We are upgrading our financial estimates after Q3 results and following the bank's higher guidance (Fig 4). We now forecast a net profit of €7.6/€8.3/€8.8 billion in 2023/2024/2025. In our numbers, we project a DPS of 0.29/0.33/0.36 for the upcoming years with a dividend yield above 10%.

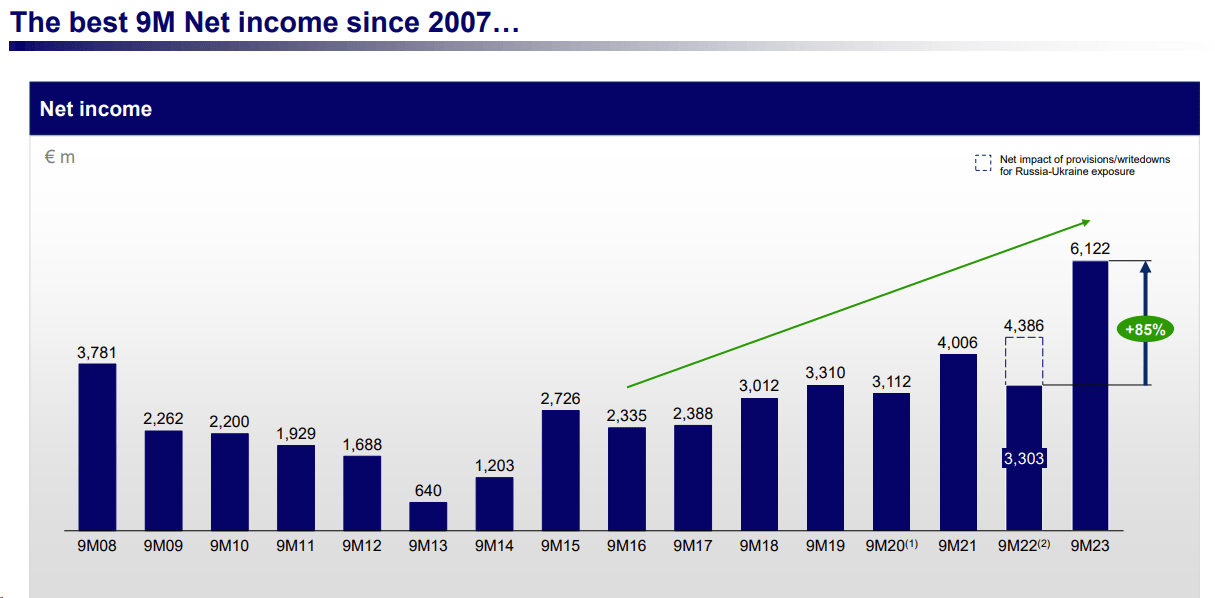

Source: Intesa Sanpaolo Q3 result presentation - Fig 1

Intesa Sanpaolo's Q3 Net Income Development

{kind=link}

Fig 2

Intesa Sanpaolo's Operating Cost

{kind=link}

Fig 3

Intesa Sanpaolo's NPL Evolution

{kind=link}

Four Reasons to Buy

-

In the last decade, some of Intesa Sanpaolo's competitors decided to exit divisions such as Insurance, Private Banks, and Asset Managers. This was not the case for the leading Italian bank, which decided to retain the total value chain in-house. Even if we project interest rates higher for longer, we know that rate hikes will come to an end, and non-interest income will (again) become more valuable. For this reason, Intesa offers downside protection, which we believe is not very well priced in by the sell side;

-

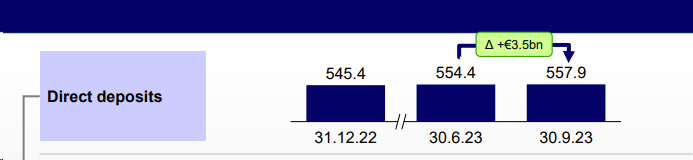

Here at the Lab, we believe the market underestimates the bank's deposit ability. Italians usually leave in their bank accounts a lot of cash (with low remuneration in deposit). This leaves an implicit upside to the bank and provides a further net interest income optionality, which is not priced in by consensus expectation (Fig 5);

-

Intesa Sanpaolo's earnings projection is set to increase, and the bank's organic capital generation is significant. With a minimum CET1 requirement of 12%, any cash excess might be distributed to shareholders. In our numbers, looking at the net profit evolution, this might be a round number of €5 billion in the cumulative three-year forecast period. In 2023, we forecasted a €1.5 billion buyback, and we believe a similar number could be replicated in 2024. This is on top of the 70% payout ratio on the ordinary dividend. Including the share repurchase, Intesa's total yield is estimated to be higher than 15% annually until 205. This is one of the highest within our EU banking coverage;

-

Year to date, the company has underperformed Italian banking peers by almost 20%. According to our estimates, the bank offers a good balance between net interest income evolution, non-interest income growth, and deposit beta resilience.

Fig 4

Intesa Sanpaolo's Net Income Higher Guidance

Fig 5

Intesa Sanpaolo's Deposit Evolution

{kind=link}

Conclusion and Valuation

The organic capital generation will support distribution to shareholders. The dividend yield should also be considered in the context of a relatively defensive activity compared to other banks, supported by the results of the latest ECB stress tests in which the bank confirmed one of the levels of CET 1 reduction in the adverse macroeconomic scenario. Following our revision of net income projection, we forecast an EPS of 0.45 for 2024. Valuing the company with a 7x P/E, we have reached a valuation of €3.15 per share (from €2.7 per share ). This valuation is also supported by a RoTE of 15% and a price-to-book value of 0.9x (in line with BNP Paribas and KBC Group ).

For further details see:

Intesa Sanpaolo: Higher Guidance And 4 Reasons To Remain Bullish