IITSF - Intesa Sanpaolo Is Grossly Undervalued Not To Mention The Dividend Yield

2023-06-02 08:48:15 ET

Summary

- Intesa Sanpaolo S.p.A. is the biggest Italian bank with a market cap of ~$40.5 billion that offers a wide range of financial products and services.

- The bank's Q1 results showcase a remarkable start to the year, with record-breaking performance across various financial indicators.

- Looking ahead to 2025, Intesa Sanpaolo expects to comfortably exceed its net income target of €6.5 billion.

- ISNPY stock is inherently 21-38% undervalued, not to mention the 6-8% dividend yield shareholders should receive during the holding period.

- I rate ISNPY stock as a Buy this time around.

The Company

Intesa Sanpaolo S.p.A. (ISNPY) is the biggest Italian bank with a market cap of ~$40.5 billion, that offers a wide range of financial products and services. It operates through 6 main segments: Banca dei Territori, IMI Corporate & Investment Banking, International Subsidiary Banks, Asset Management, Private Banking, and Insurance. The company provides lending and deposit products, corporate and investment banking services, asset management solutions, insurance products, and various other financial services. Intesa Sanpaolo serves individuals, small and medium-sized businesses, non-profit organizations, corporates and financial institutions, public administration, private clients, high-net-worth individuals, institutional clientele, and other customers. The company's headquarters are located in Turin, Italy. As of March 31, 2023, the operating structure of the Intesa Sanpaolo Group had a total network of 4,450 branches, of which 3,498 were in Italy and 952 were abroad, employing 94,667 people in total.

Since the latest financial statements are provided on the company's website in Italian, which I, unfortunately, don't speak, and the SEC filings were last updated in 2015, I'll base my analysis on presentation materials , earnings calls , and also some proprietary analytical sources and reports.

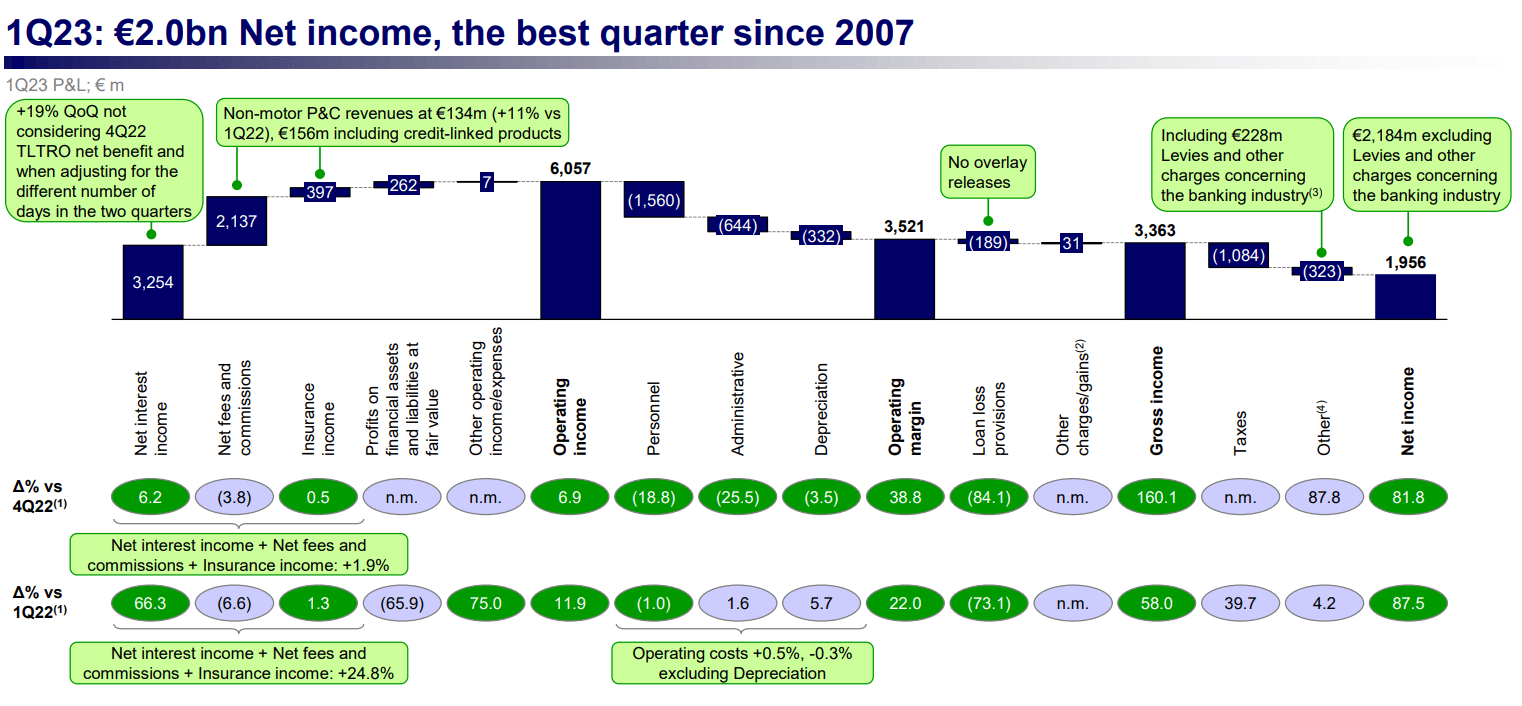

Intesa Sanpaolo's Q1 results [published in early May] showcase a remarkable start to the year, with record-breaking performance across various financial indicators. Net income reached €2 billion, the highest quarterly figure since 2007, while operating income, operating margin, and gross income were the best-ever for a quarter:

{kind=link}

Asset quality remains excellent, with low NPL inflows [unchanged from last quarter at €0.7 billion] and a coverage ratio of ~50%, positioning the bank as a leader in Europe in terms of asset quality. And client assets continue to grow - in the first quarter of FY2023, INSPY recorded an increase of 91 basis points, or €11.2 billion, compared to the previous quarter, mainly thanks to growth in assets under management and administration.

ISNPY's loan-to-deposit ratio dropped by 2% [from 86% to 84%] over the past 6 months - a lower ratio is often considered favorable because it suggests that the bank is relying less on borrowed funds and has a higher level of liquidity. The 84% looks still high, but I like the overall downward dynamic here.

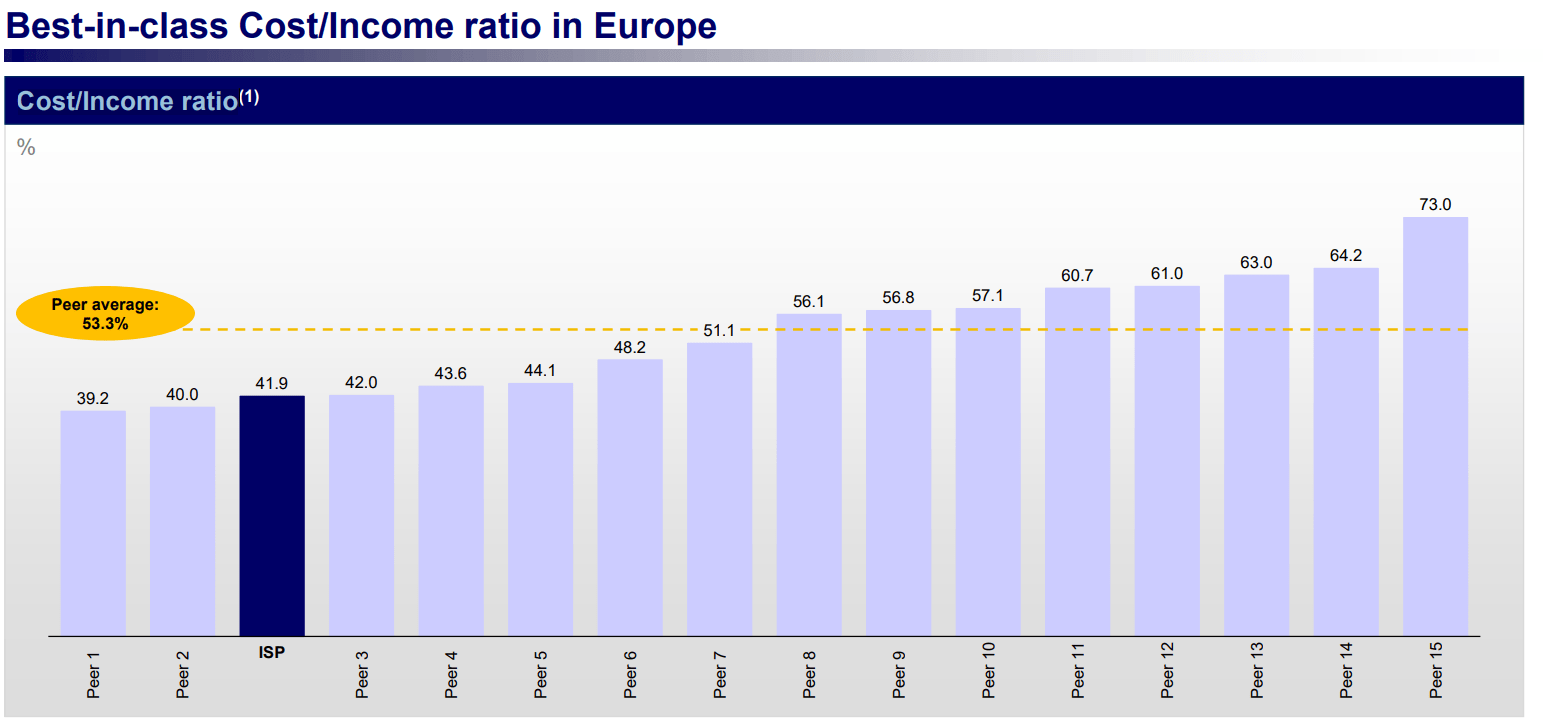

From what I see, ISNPY looks like a fairly efficient bank in terms of cost-to-income ratio. This ratio provides information on the bank's ability to manage expenses relative to the interest income generated. A lower cost/income ratio is generally considered beneficial, as it indicates that a bank is operating efficiently and has its costs under control in relation to its income.

{kind=link}

At the same time, the bank's common equity ratio increased to 13.7% in Q1 FY2023 [from 13.5% in Q4 FY2022], demonstrating resilience and absorbing regulatory headwinds, with expectations to reach 15% including DTA absorption, according to the latest earnings call. The total capital ratio that measures Tier 1 and Tier 2 by the bank's risk-weighted assets is now standing at 19.5% - that's 50 basis points higher QoQ. The CET1 ratio in itself surprised the consensus significantly to the upside, proving ISNPY's ability to absorb losses and maintain a strong capital position at a much higher level than initially expected.

Jefferies [proprietary source], May 2023

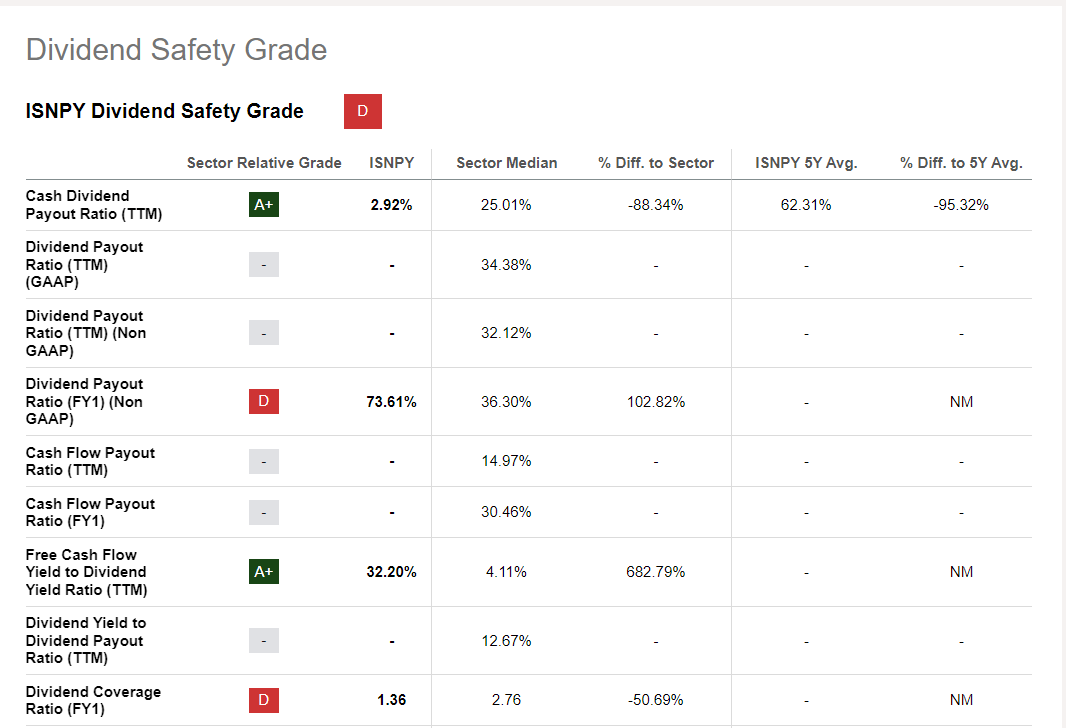

This exceptional performance of Q1 allowed Intesa Sanpaolo's management team to raise its net income guidance for the 2023 full year to €7 billion. Looking ahead to 2025, Intesa Sanpaolo expects to comfortably exceed its net income target of €6.5 billion , driven by interest rate boosts. It's important to note here that ISNPY is a very shareholder-friendly bank: according to IR documents, €1.4 billion in cash dividends have already been distributed in the first quarter and a share buyback of €1.7 billion has been carried out in the period from February to April 2023. It means that going forward the dividend yield that we see today [7.5-8.4%, TTM-FWD] is likely to stay with us even though Seeking Alpha's Dividend Score system shows little conviction in that conclusion:

{kind=link}

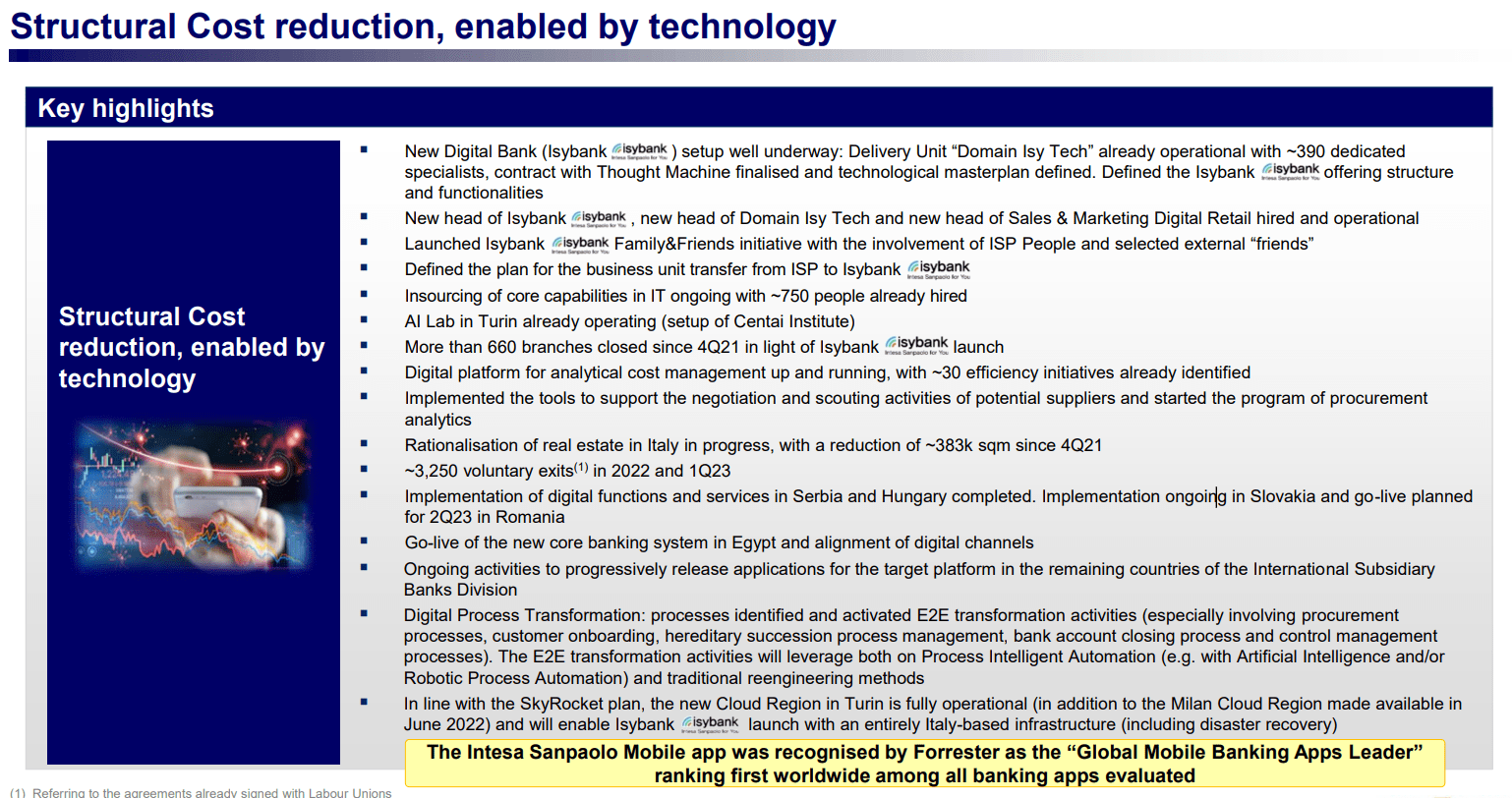

Thinking long-term, I was overwhelmed to see that the bank's technology evolution is progressing rapidly, with the launch of its digital bank, Isybank , planned for the summer.

{kind=link}

Also, Reuters reported a few days ago , that Intesa Sanpaolo has developed an artificial intelligence tool called Lisa (Linguistic Intelligence for Supervisory Awareness). This tool uses advanced algorithms to analyze thousands of banking supervision publications. The head of Intesa's supervisory strategic steering department, Chiaradonna, highlighted the challenges posed by an overwhelming amount of information that is difficult to handle without proper assistance. Chiaradonna emphasized the need for effective support to navigate through practices, interviews, statements, texts, and in-depth studies, which generate an excessive volume of information. By scanning this information, Lisa identifies connections and meanings to forecast upcoming trends in the industry. Thanks to the introduction of this technology, I expect cost optimization to continue - staff can be further reduced, which should have a positive impact on NII and thus on buybacks and dividends.

Valuation & Expectations

Although the company presented good figures for the first quarter, its share price came under pressure, as did the share price of many other European banks:

Jefferies [proprietary source], May 2023

I think the market believes that the macro economy is uncertain today and that most European banks' NIMs, which have improved greatly due to a period of higher interest rates, have now peaked. This is most likely the case if we recall management's guidance - the FY2025 target of €6.5 billion is 7.1% below the FY2023 guidance. This is most likely why the market is pricing ISNPY stock at a next-year P/E ratio of ~6x which is roughly the same as in 2019, while the gap to the TTM's multiple reaches 41%.

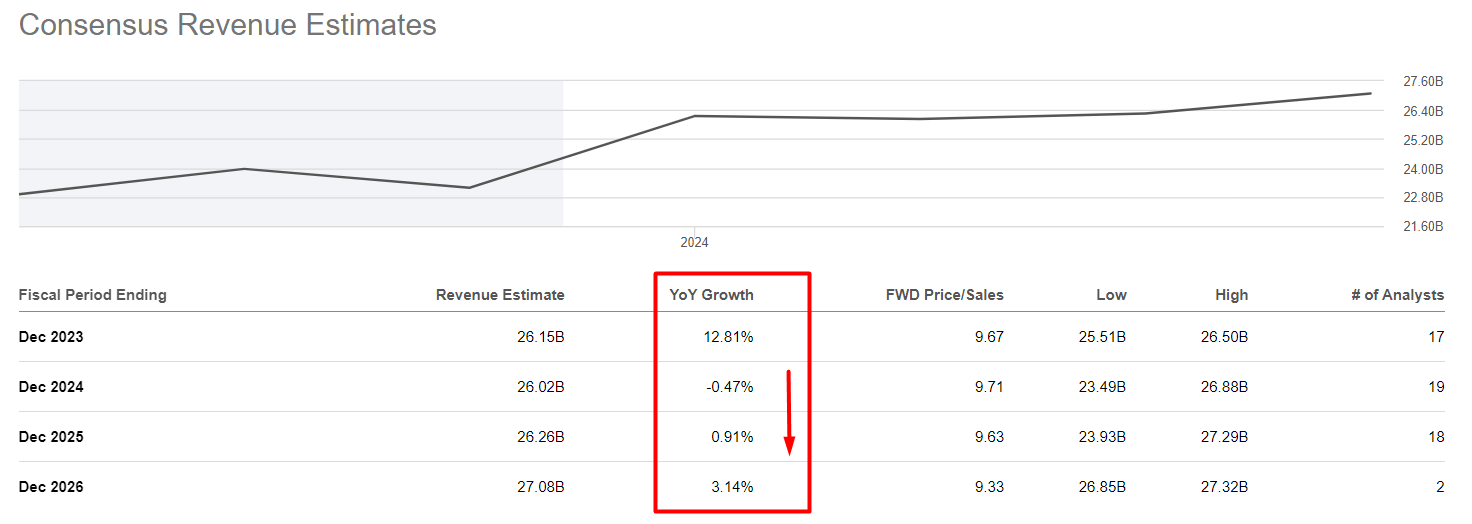

For this reason, Wall Street analysts' consensus forecasts ISNPY's revenue to stagnate over the next 2 years after a sharp increase in FY2023:

{kind=link}

EPS forecast for FY2024 results in an implied P/E of 5.79, with no data provided for FY2025 and beyond.

Indeed, the banking sector tends to exhibit cyclical patterns that are closely linked to the general economic cycle. Declining economic activity, rising unemployment, and financial distress among borrowers may lead to higher loan defaults, credit losses, and a decline in demand for new loans. But the management noted during the most recent earnings call that the Italian economy is showing better-than-expected growth, and Intesa Sanpaolo remains positive about its recovery, offering support to families and businesses.

Predicting macroeconomics is a rather difficult task that not everyone can do. The only thing left for retail investors who are unable to build their own econometric macro models is to listen to the big banks or ignore the macroeconomic argument altogether. In recent reports, I found an analysis by Goldman Sachs [proprietary source] that shows that the European economy is likely to expand slightly compared to FY2023 if we focus on GDP:

Goldman Sachs [proprietary source], June 01, 2023

If so, then the relatively high loan-to-deposit ratio of ISNPY should be an advantage to the bank, not a risk factor.

If management's forecast of €7 billion net income for full-year 2023 comes to pass, we arrive at $7,540 million at a EURUSD of 1.0771. The resulting price-to-earnings ratio of ~5.8x is quite low due to the high cyclicality of the industry and is likely to increase as growth slows. However, as we don't expect ISNPY's EPS to decline materially over the next few years, the mean-reversion process should result in a share price of $17.43-19.92 by the end of 2024, assuming a P/E ratio of 7-8x. ISNPY stock is therefore 21-38% undervalued, not counting the 6-8% dividend yield that shareholders should be able to get during the holding period.

It's important to keep in mind, however, that nothing is stopping ISNPY stock from extending its undervaluation. All potential investors need to know other risks than the ones I've outlined today - click here for more of Seeking Alpha's Analysts' views. And the most important thing is to do your due diligence before buying.

The Bottom Line

Of course, buying shares in a European bank - even such a high-quality one as ISNPY - carries a lot of risks [from geopolitics to macroeconomics]. The high loan-to-deposit ratio could play a nasty trick on Intesa in the event of a bank run, similar to what happened with U.S. regional banks. Money market instruments with very high yields will probably continue to attract depositors - the risk of a liquidity imbalance could make itself felt.

However, I believe that all these risks are already factored into the valuation of Intesa Sanpaolo. The current valuation of ISNPY's stock indicates that the economy has reached its local peak in the cycle, but there is no significant decline in net income expected in the near future as far as I see. I anticipate that this perceived imbalance will resolve itself at some point. Additionally, the generous dividend yield and buybacks serve as a welcome bonus for investors while they wait for the undervaluation to dissipate. I rate ISNPY stock as a Buy this time around.

Thanks for reading!

For further details see:

Intesa Sanpaolo Is Grossly Undervalued, Not To Mention The Dividend Yield