ISNPY - Intesa Sanpaolo: One Of The Best Risk-Return Banking Stocks

2023-07-03 14:39:55 ET

Summary

- Intesa Sanpaolo S.p.A. stock has exhibited scintillating form that could continue amidst a healthy Italian yield curve and softening regional credit spreads.

- The bank's asset management division's cost-to-income ratio of 22.1% and recent developments within implies that a hidden asset could be unleashed.

- A continuous residual income valuation model indicates that Intesa stock is undervalued.

- Risk factors such as the stock's high beta and Intesa's exposure to cyclical debt must not be overlooked. Nevertheless, we believe the stock's positives outweigh its risks.

It has been a pulsating year for banking stocks across Europe and North America amidst a flurry of events that laid some serious volatility onto the financial markets. However, we believe moderation is en route in certain parts of the world, as their yield curves are starting to look a whole lot better. One such area is Italy, which has seen a significant decline in credit risk and a flattening of its curve since fears of a banking crisis erupted earlier this year. As such, one of its largest banks, Intesa Sanpaolo S.p.A. ( ISNPY ), has experienced a splendid time. Moreover, our analysis indicates that the bank might achieve stellar results for the remainder of the year; here's why.

Operational Review - Credit Risk Abating

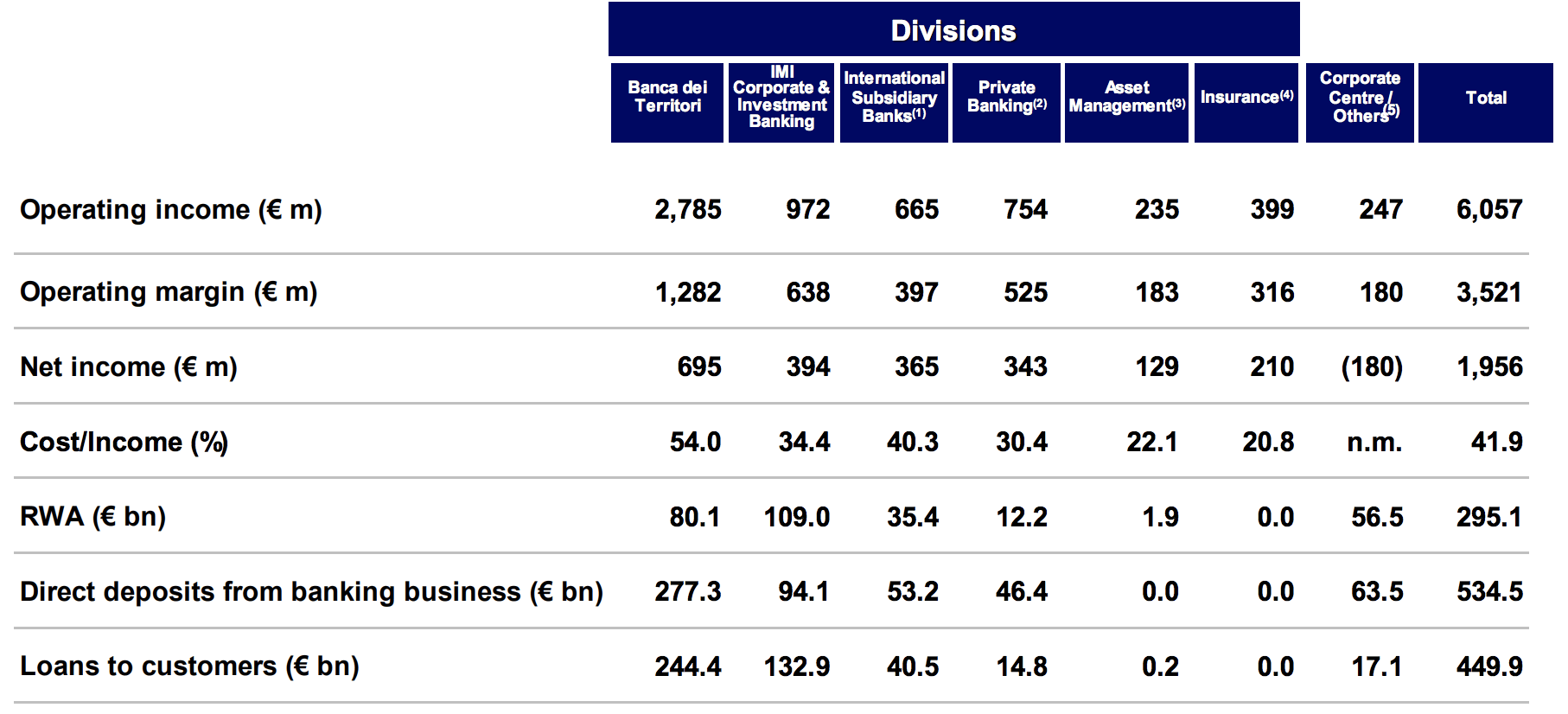

Intesa's latest financial results show that the firm is primarily reliant on banking activities, with fee-based asset management and insurance endeavors making up for merely 10.46% of Intesa's operating income. As such, today's article primarily focuses on debt-based activities, with a slight touch on Intesa's other lines of business.

{kind=link}

Debt Investments and Loans

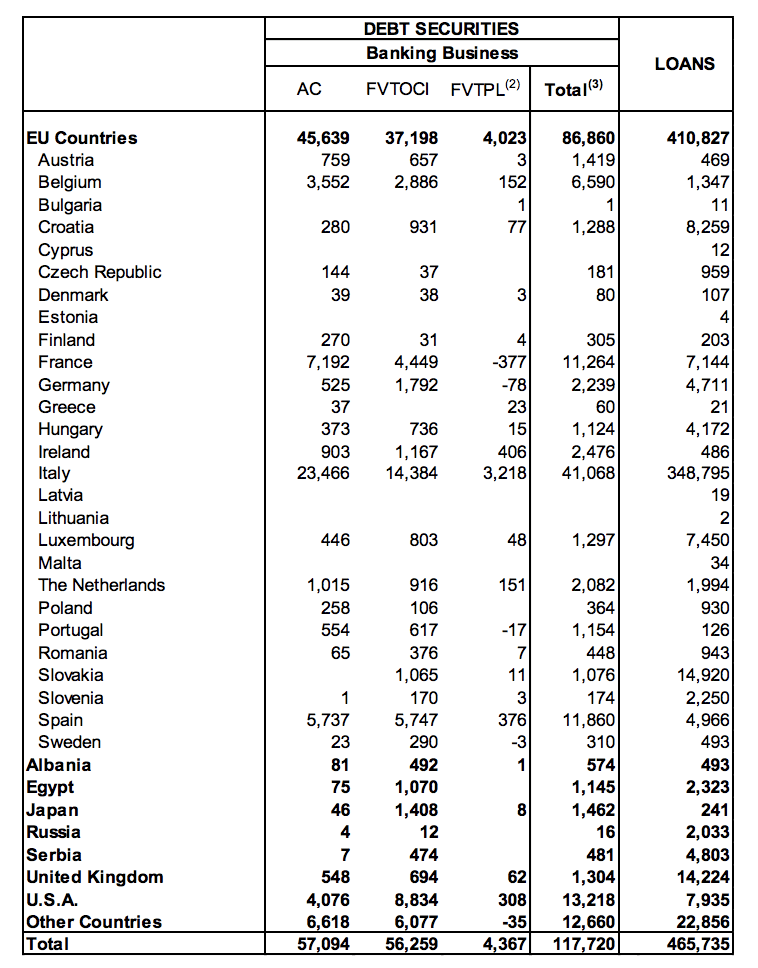

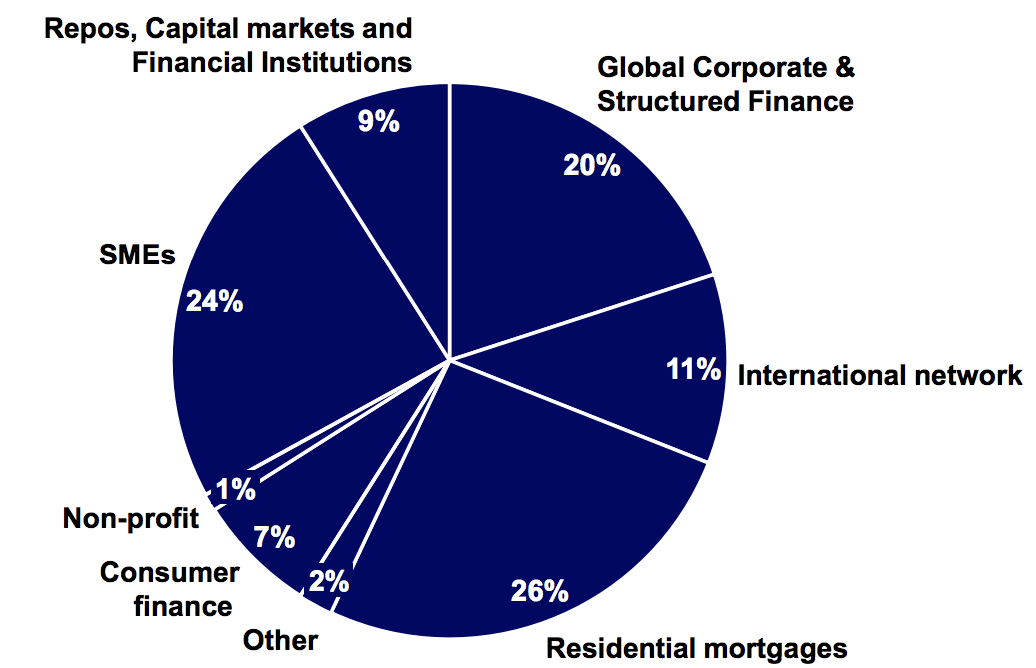

Although geographically diversified, Intesa's primary debt exposure is in Italy, with approximately 74.8% of the division's asset base located within the nation. In our view, Italy is a lucrative market for now as its yield curve is relatively flat and not inverted like most other nations. Moreover, Italy provides lucrative yields on its debt and demands moderate funding costs from banks.

The positives mentioned above were illustrated in the firm's latest earnings report, which conveyed that Intesa's net interest income surged by 66% year-over-year and 9% quarter-over-quarter.

{kind=link}

As the diagram above illustrates, 12% of Intesa's debt exposure is to trading securities (labeled FVTPL). For those unaware, these alter a bank's income statement between quarters as unrealized gains/losses are realized. We expect Intesa's trading securities to perform strongly for the remainder of the year, as receding credit risk and a softer inflation rate might adjust debt valuations upward.

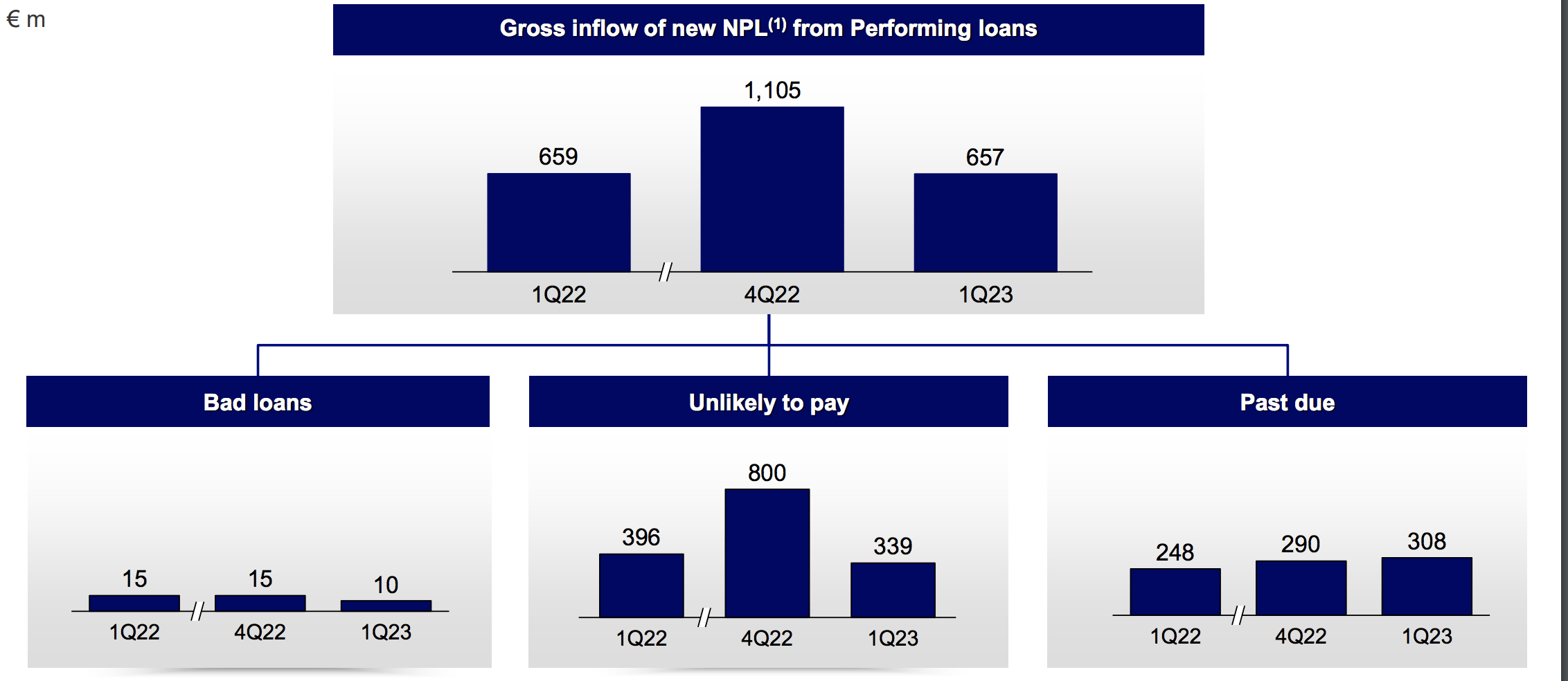

Furthermore, we think the bank's loan portfolio has struck an inflection point. As illustrated in Intesa's previous operating quarter, the firm realized fewer inflows to its nonperforming loan account and simultaneously recognized fewer bad loans. Although banks often manipulate these line items during periods of economic turmoil, we give Intesa the benefit of the doubt due to its robust realized earnings, receding credit risk exposure, and the solid yield curve in Italy.

{kind=link}

Asset Management Segment Support

Intesa's fee-based business grew by 13.3% year-over-year in its previous quarter, which is likely due to the bounce in global markets. Italy's year-over-year stock market returns have been scintillating, and we would not be surprised if a similar trajectory is realized in the coming twelve months, as the yield curve is in terrific shape. In essence, we have yet to take note of any structural breaks, meaning that Intesa could continue to benefit from high base rates and incentives.

Furthermore, Intesa's wealth management division is focused on scaling and maximizing its commissions. Initiatives such as adopting BlackRock, Inc.'s ( BLK ) Aladdin, high-net-worth client advisory tools, and digital wealth management services could enable the bank to attract a broader client base. Intesa's asset management division currently hosts a cost-to-income ratio of merely 22.1%, showing how lucrative additional investment in the division could be.

Valuation and Dividends

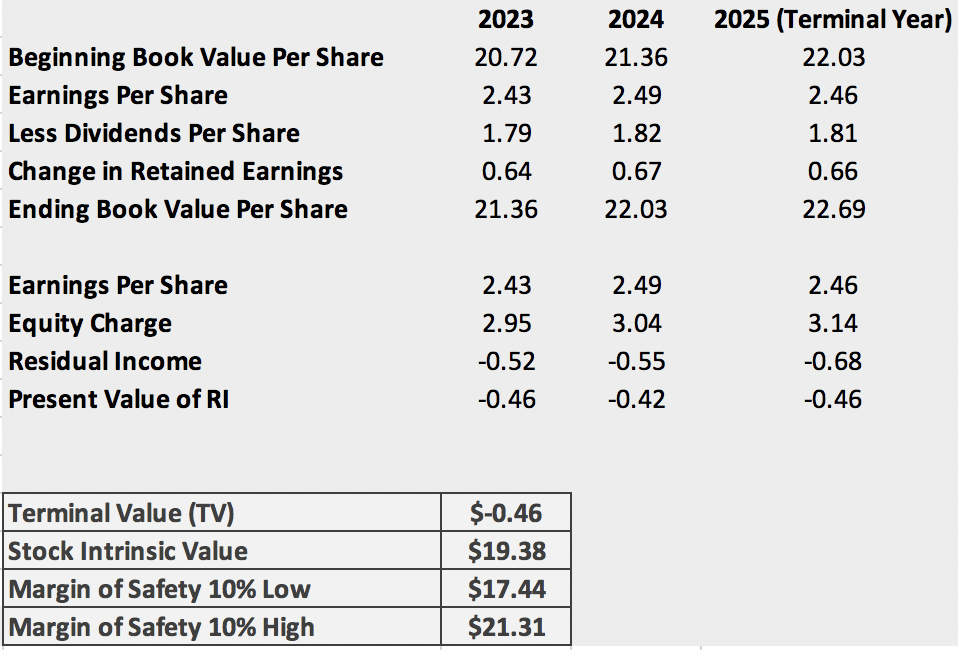

Residual Income Model – Model Output

A continuous residual income model was utilized to value the stock, as investors often emphasize a bank's book value. Based on our model, Intesa's stock was undervalued by approximately 29.82% at the time of writing the article. Although the residual income model does not provide a guarantee of returns, it is widely utilized as an indicator by financial analysts.

{kind=link}

Model Inputs

The inputs utilized for our residual income model were as follows.

- Intesa's stock price was divided by its price-to-book ratio to formulate a baseline book value.

- Seeking Alpha's earnings and dividend forecasts were extracted for the years 2023 and 2024. A normalized average was used for the year 2025.

- The equity charge was assumed at Intesa's current CAPM, provided by YCHARTS.

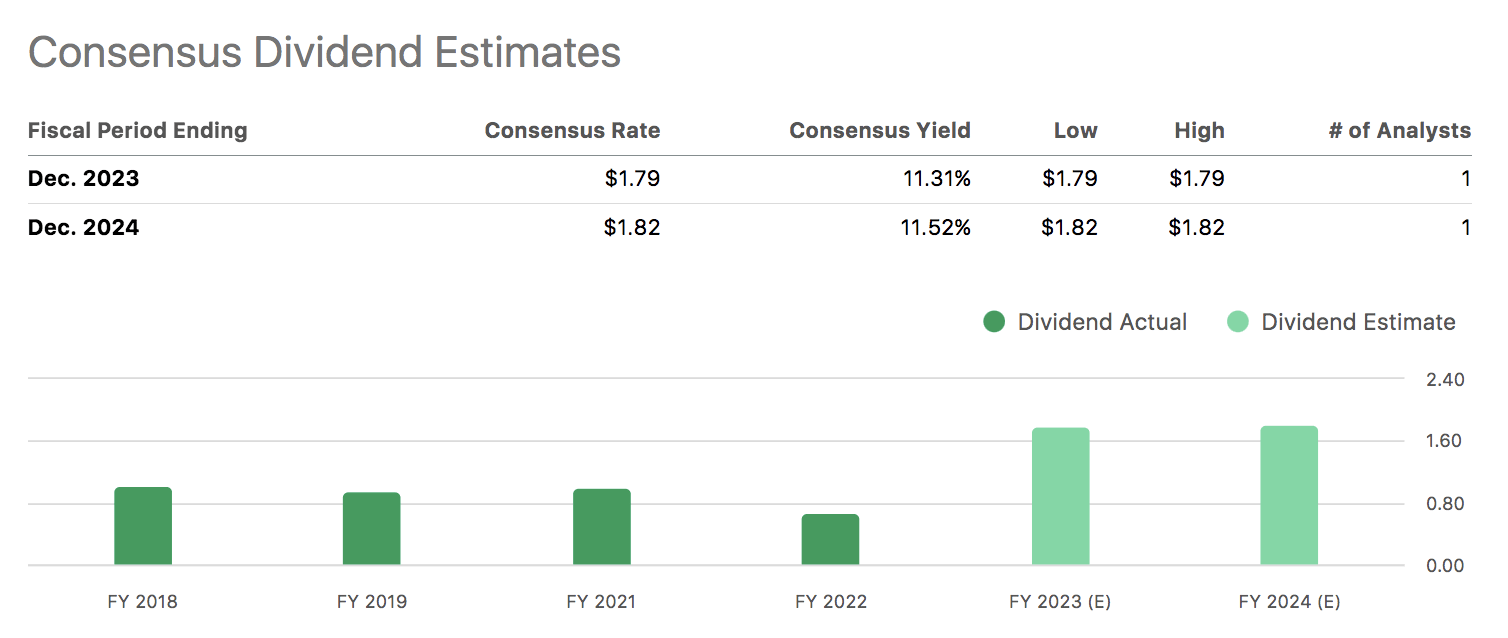

Dividends

Intesa Sanpaolo has a five-year average dividend yield on cost of 6.03% , a forward dividend yield of 7.36%, and a dividend coverage ratio of 1.36. Collectively, it can be argued that Intesa has a lucrative dividend yield with reasonable assurance. Moreover, our qualitative analysis of the company's fundamentals tells us that income-seeking investors might be looking at a best-in-class pick here.

{kind=link}

Risks – Cyclical Debt Exposure and High Beta Sensitivity

Although our general outlook on Intesa's debt portfolio is bullish, there are a few risks that investors need to be wary of. Firstly, the company's customer loans portfolio is very cyclical, which could haunt it if the economy takes a turn for the worse. Moreover, Intesa's customer loans portfolio is very focused on SMEs, which are usually the first to falter during trying economic periods, as witnessed by the Silicon Valley Bank collapse .

In essence, economic tail risk is still a primary risk factor for many banks as we reach the higher end of the interest rate cycle, and Intesa is no exception.

{kind=link}

Another factor to consider is Intesa's high beta sensitivity and the possible effect a potential market correction could have on the stock. Certain Wall Street analysts believe the market is overvalued after its early-year rally; a correction could drag high-beta stocks like Intesa down into the abyss.

Final Word

Intesa Sanpaolo S.p.A. stock seems undervalued, as its exposure to an appealing Italian yield curve suggests its net interest income might continue to surge. Moreover, momentum within the firm's asset management segment and potential support from its held for trading securities could unlock additional value.

Factors such as economic tail risk and a potential broad-based market correction remain of concern. However, we think Intesa's positives outweigh its negatives and deem its stock undervalued.

For further details see:

Intesa Sanpaolo: One Of The Best Risk-Return Banking Stocks