IITSF - Intesa Sanpaolo: Remarkable Results And An 11.4% Dividend Yield Projection

2023-08-06 23:51:34 ET

Summary

- Intesa Sanpaolo delivered an 80% increase in net profit in H1 2023 vs. last year.

- The company increased its 2023 net income projection with a profit of over €7 billion (and an optimistic view for 2024 and 2025).

- Low cost of risk, best-in-class cost-income ratio, zero NPL target, and an 11.4% dividend yield projection. This is a clear buy.

Before analyzing Intesa Sanpaolo's quarterly figures (ISNPY), it is essential to report the EU Stress Test results achieved by the Italian banks. Despite the stringent assumptions with a pessimistic scenario, the Italian banks recorded a solid performance at the aggregate level, with an average drop in CET 1 ratio of only -399 basis points. The result is remarkable in absolute terms and compared to the European competitors. In numbers, the European average was at -452 basis points , with countries such as Germany and France at -606 and -760 basis points, respectively. Our Italian universe coverage shows Intesa Sanpaolo and UniCredit are among the 2023 stress test winners (both buy-rated by our team). Regarding Intesa Sanpaolo, in a 2025 adverse scenario, the bank reported a decrease in the CET 1 of -268 basis points (reaching a solvency ratio of 10.8%) with a surplus in the ECB capital buffer of +205 basis points.

2023 ISP EU-WIDE STRESS TEST RESULTS

{kind=link}

We still remember a negative concern about our Intesa Sanpaolo target price at the Lab. We based our analysis on Net Interest Income Development which we believe was not correctly Priced In. In a challenging momentum in the banking system (SVB and Credit Suisse crisis, we confirmed our positive view ' Taking Advantage ' of a stock price decline. A top-down analysis supported this and was also coupled with the ISP's competitive advantages: solid balance sheet with an extremely low level of UTP and NPL, lower cost of risk, best-in-class cost/income ratio, and limited Russian exposure.

Before Q2, we raised ' Our Expectations ,' providing a 2023 net income target of €7.5 billion (we were already above the bank's internal guidance in 2023). We also emphasized how the bank " will fully benefit from rising interest rates with an expectation of 2023 net interest margin at €12 billion against a consensus of €11 billion. "

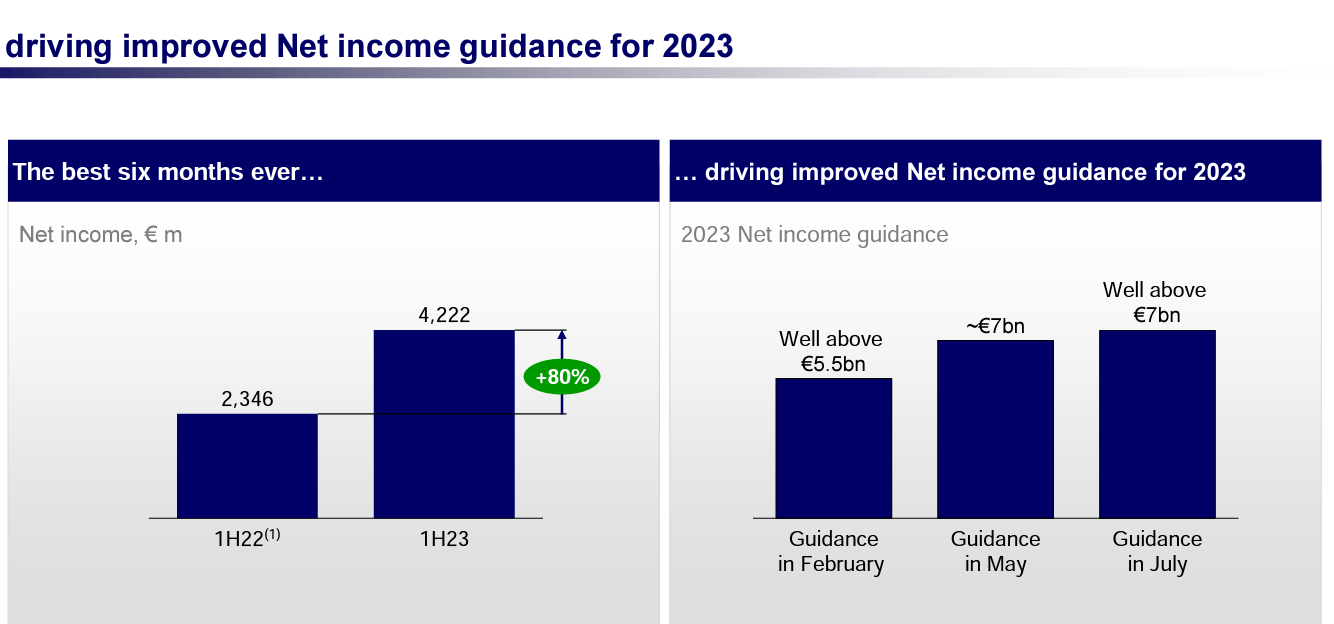

Looking at the new guidance below, we can clearly say we were right. In detail, Intesa Sanpaolo is now expecting a net interest income to exceed €13.5 in 2024 and a net profit growth well above €7 billion.

Intesa Sanpaolo new 2023 target

{kind=link}

Q2 results

Starting with the bottom line performance, in H1, Intesa Sanpaolo delivered a net of €4.22 billion (Fig 1), up 80% on a yearly basis (H1 2022 was €2.34 billion). This was supported by net interest income up by 68.9%, partially offset by unfavorable net commission performance that fell by 4.2% to €4.35 billion. Considering ISP's payout ratio, 2024 shareholders' value creation is already at €3 billion in dividends accruals. The CEO explained that any further distribution is to be evaluated year by year. However, he confirmed that the 2024 target is to remunerate shareholders with €5.8 billion. This includes November 2023 interim dividend, the buyback second tranche, and the usual Q2 dividend payment.

Regarding the P&L, ISP's operating margin performed well, and this (once again) was supported by a lower increase in operating expenses (only plus 0. 9%) with costs that reached €5.21 billion. Furthermore, efficiency is extremely high, with a cost/income ratio of 42% (it was 48% in 2022 H1). This is one of the best ratios among European banks (Fig 2).

Going to the cost of risk evolution, the ratio fell to 25 basis points (from 70 basis points in 2022). However, even if it was minimal, if we exclude Russian de-risking, the H1 2022 cost of risk was at 30 basis points. Despite that, this is a positive trajectory. Russia's exposure decreased by over 75% and fell to 0.2% of the group's total customer loans. Cross-border loans to Russia are mainly performing and classified in Stage 2. At the same time, liquid assets amounted to €284 billion. Therefore, the regulatory liquidity requirements were met with an LCR of 171%. Intesa Sanpaolo's credit quality has also improved, with the stock of non-performing loans down by 3.6% compared to the end of 2022 and a gross incidence of non-performing loans on total loans equal by 1.2% (Fig 3).

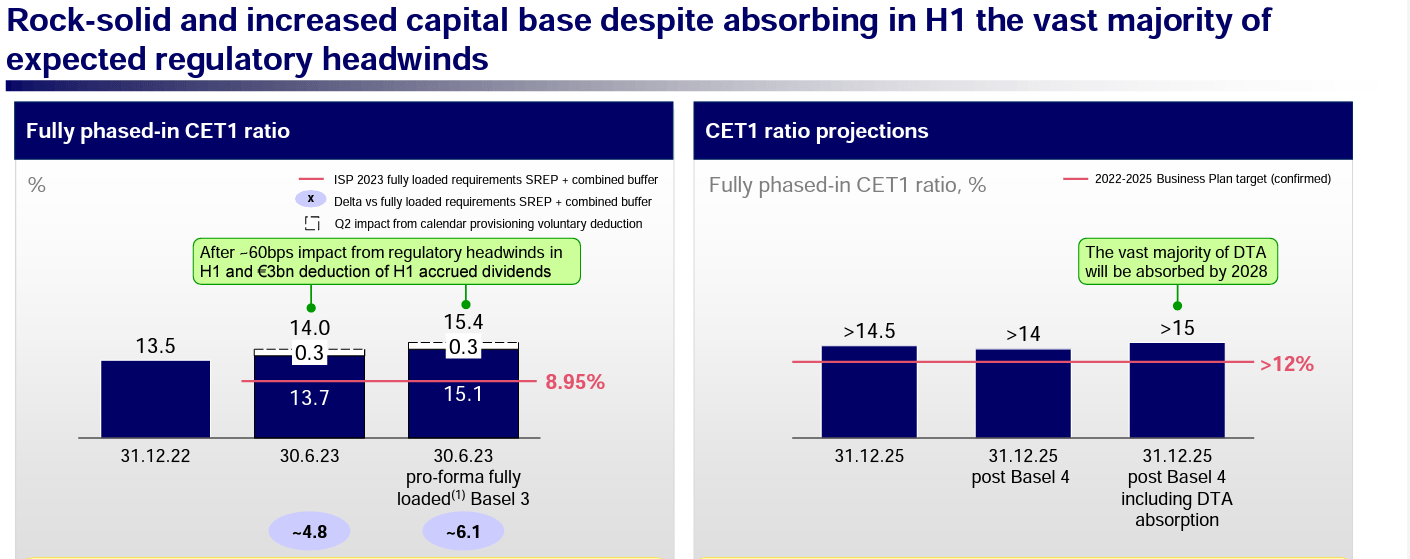

ISP capital solidity has been confirmed with coefficients on levels well above the regulatory requirements. At June-end, including the €3 billion dividend, the Common Equity Tier 1 ratio reached 13.7% (Fig 4).

{kind=link}

Fig 1

ISP Cost/Income ration evolution

{kind=link}

Fig 2

{kind=link}

Fig 3

{kind=link}

Fig 4

Conclusion and Valuation

Due to the strong H1 accounts, ISP expects a 2024 and 2025 net income higher than the 2023 projection. This is due to revenue growth, lower costs, low cost of risk, and lower taxes. Management expects revenue growth supported by a further increase in interest rate, commission recovery, and better results in the insurance business. On the other hand, costs are forecasted to decrease thanks to technology improvements (IT optimization) and branch rationalization. The bank also anticipated personal voluntary exits, which would relieve the workforce's total costs.

We were above FactSet consensus by 8%. We were above the company's internal guidance. After ISP's solid accounts and an upward revision of the 2023 guidance in line with our estimates, we decided to leave unchanged our target price of €2.7 per share . This is supported by a valuation based on a Tangible Book Value of 0.85x on the 2024 accounts with a RoTE of 14.5%. We also confirmed a 29-cent dividend in 2023, with a predicted dividend yield of 11.4%. We say no more; our buy is then confirmed.

For further details see:

Intesa Sanpaolo: Remarkable Results And An 11.4% Dividend Yield Projection