ISNPY - Intesa: Undervaluation Leads To Sustainable 11% Dividend Yield

2023-06-12 15:34:39 ET

Summary

- Intesa is a quality bank in Italy with good fundamentals.

- It offers a sustainable high-dividend yield of 11%.

- Its shares are undervalued at just 0.8x book value.

Intesa Sanpaolo ( OTCPK:ISNPY ) offers a high-dividend yield and its shares are undervalued, being a great income play in the European banking sector.

Business Overview

Intesa Sanpaolo is an Italian bank and one of Europe's largest banks, measured by its total assets of €974 billion at the end of 2022. Its operations are spread across the financial sector, but its core business is retail and commercial banking in its domestic market. Nevertheless, it also has significant operations in other segments, namely insurance, wealth management, or private banking.

Its current market value is about $45 billion and trades in the U.S. on the over-the-counter market, but investors should be aware that its shares have better liquidity in its main listing on the Italian Stock Exchange.

Intesa is the market leader in banking in Italy, a position that was reinforced by its acquisition of UBI Banca in 2020, increasing its market penetration especially in the North of Italy. Its main competitors are UniCredit , which is the second-largest bank in the Italian banking system, while other competitors include Credit Agricole ( OTCPK:CRARY ) or Banco BPM .

Intesa's business profile follows the bancassurance business model, which means that Intesa's operations are highly exposed to both banking and insurance, providing the bank with better cross-selling opportunities compared to other banks that don't have insurance companies integrated within their group.

This business model is quite popular in France and was also followed by several banks in the Benelux, but following the global financial crisis and several state bailouts this model was dismantled for several players.

However, Intesa has followed this bancassurance model, plus it also has pushed for growth in other fee-based segments such as asset & wealth management, being a key reason why its earnings have been quite resilient in recent years, despite the low interest rate environment in Europe, given that Intesa's reliance on interest rates has decreased while the weight of fees on total income has increased.

On the other hand, the interest rate environment in Europe has changed rapidly since mid-2022, and Intesa is not a bank highly geared to rising rates due to its business model that is more geared to fees than many of its peers. Despite this, in my opinion, Intesa's business profile is more recurring over the economic cycle, which is positive for long-term investors.

Additionally, another important factor for its relatively stable earnings over the past decade has been its good credit quality compared to its Italian peers, given that Intesa's non-performing loans (NPLs) have been consistently lower than the Italian system overall, showing better than average underwriting criteria.

This is important because, historically, one of the Italian banking system's main woes has been high NPLs, which Intesa cannot escape due to its size as a large bank in the country, but has been able to manage credit risk and push for growth in other financial services segments beyond banking, which is key to having a sustainable business model over the long term.

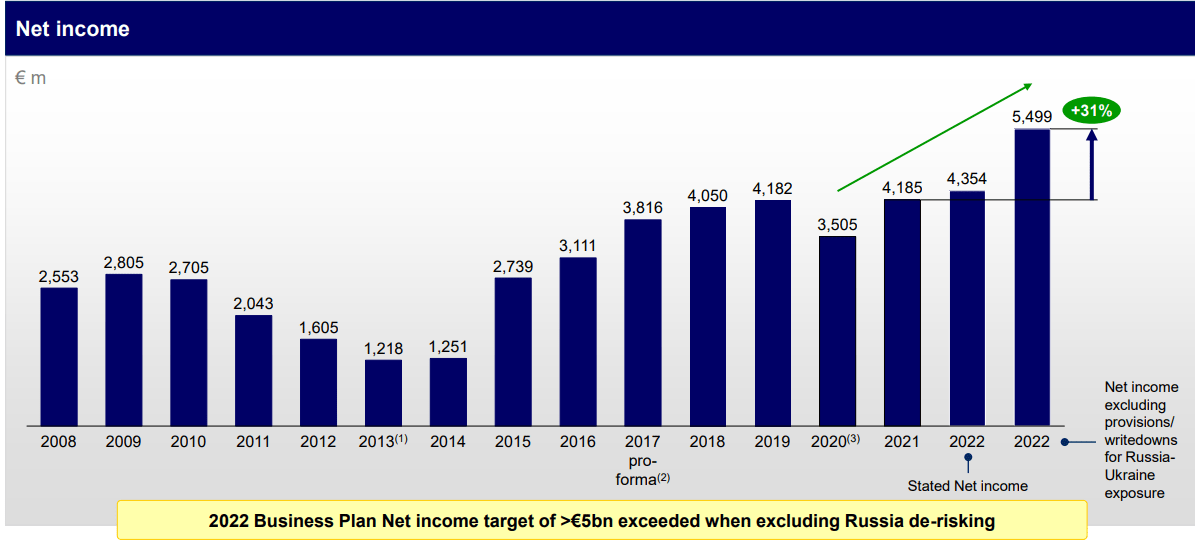

This is reflected in the bank's ability to remain profitable despite several headwinds, like the global financial crisis of 2008-09, the European debt crisis of 2012-13, and more recently the war in Ukraine, as shown in the next graph.

{kind=link}

This very strong track record is key for the bank to achieve its financial targets over the next few years, namely to reach a net income above €5 billion by 2025 and to have a net NPL ratio of 1% in the same year.

Financial Overview

Regarding its most recent financial performance, Intesa has delivered relatively positive results in recent years, despite the negative impact of Covid in 2020 and more recently the costs associated with its exposure to Russia.

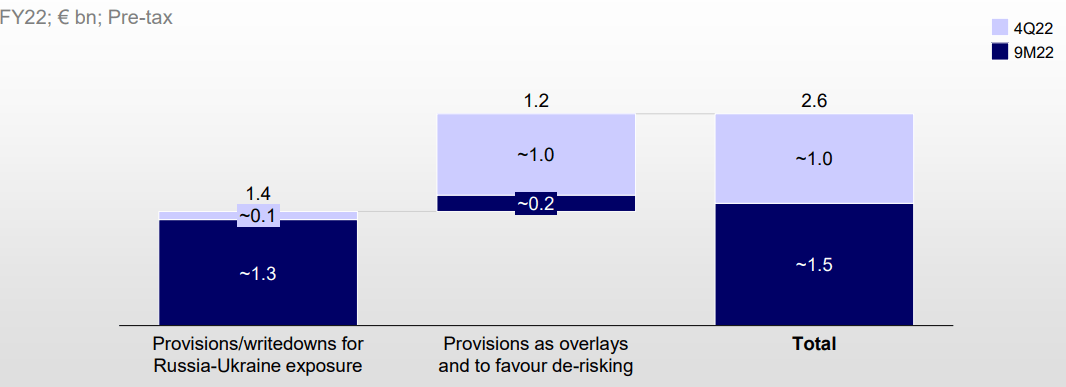

Indeed, despite a good operating performance, Intesa booked about €1.4 billion of provisions and write-downs related to Ukraine and Russia, plus additional €1.2 billion provisions to strengthen its balance sheet, negatively impacting its bottom line.

{kind=link}

Despite that, Intesa's reported net income was above €4.3 billion in the year , a small increase from the previous year. This was possible due to the rising interest rate environment, which led to a strong increase in revenues.

Intesa's net interest income increased by 20% YoY to €9.5 billion, an absolute increase of about €1.6 billion in the year, while fees and commissions decreased by 6.3% YoY to €8.9 billion. Total revenues amounted to €21.4 billion, an increase of only 3.3% YoY, despite the big jump on NII. This revenue line represents less than 45% of total revenue for Intesa, while there are other European banks where NII has a weight of about 75% on total revenue, being therefore much more geared to rising rates than Intesa.

Regarding costs, the bank reported a small decrease of 0.4% YoY to €10.9 billion, which is a very good outcome considering the inflationary environment. This led to an efficiency ratio, measured by the cost-to-income ratio of 50.9% in 2022, a very good level of efficiency among the European banking sector.

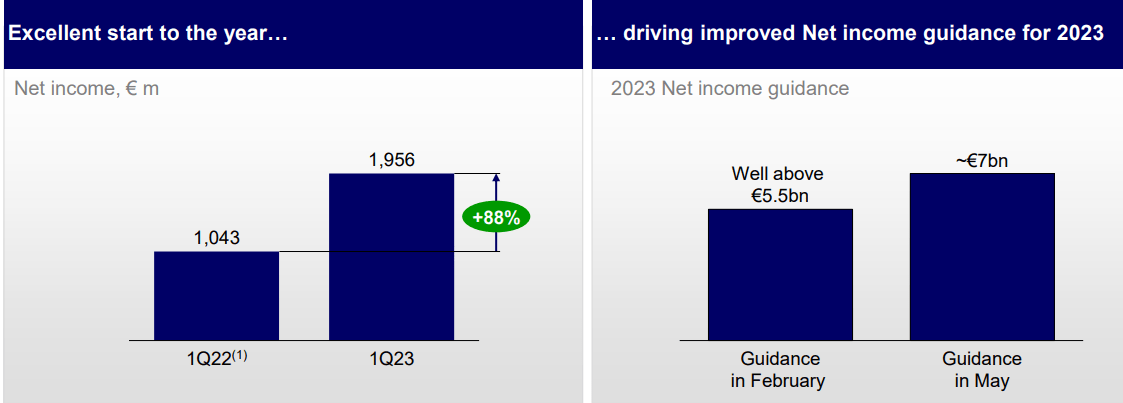

During the first three months of 2023 , Intesa has been able to maintain very good operating momentum, with its bottom line being supported both by rising rates and lower credit costs, as most of the Russia-related issues were already reflected in its 2022 accounts.

Compared to its reported quarterly profit in Q1 2022, Intesa's Q1 2023 net income increased by 88% YoY, to €1.95 billion. This was the highest quarterly profit since 2007, showing that Intesa is firing on all cylinders and is on the right path to achieve the highest annual profit in its history during 2023.

Indeed, while its previous guidance was to reach a net income of about €5.5 billion in 2023, the bank upgraded this guidance to about €7 billion this year, well above its previous target for 2025. This clearly shows that Intesa's operating momentum is much better than its management was expecting back in February 2022, when it presented its 2022-25 business plan.

{kind=link}

While this performance is quite impressive, it's not expected to last long because interest rates are expected to reach a peak In Europe over the coming months, thus higher NII is not much likely beyond 2023. This explains why, according to analysts' estimates, Intesa should report a net income of €6.93 billion in 2023, and only €7.2 billion in 2025.

This means that Intesa's rapid growth is justified mainly by cyclical factors, and much more moderate growth is likely over the coming years. Nevertheless, its profitability level, measured by the return on equity (ROE) ratio, is expected to be consistently above 11% over the next four years, which is a very good level of profitability within the European banking sector.

Regarding its capital position, Intesa has a solid position given that its CET1 ratio was 13.7% at the end of March, well above its own medium-term target of at least 12%. This means that Intesa has an excess capital position, enabling it to distribute a large part of its annual earnings to shareholders.

Indeed, Intesa aims to return some 70% of its annual profit to shareholders, both through dividends and share buybacks. Not surprisingly, considering its strong earnings history, Intesa has a good dividend history that was only affected by the temporary regulatory ban on dividend distributions in 2020.

Intesa returned to dividend distributions in 2020, and gradually increased its dividend since then. Related to 2022 earnings, it has distributed a €3 billion cash dividend, plus it also performed share repurchases of €1.7 billion until April, increasing even further its capital return. The bank distributes two dividends per year, leading to an annual dividend per share of €0.16 related to 2022 earnings, which is expected to increase to €0.26 per share due to higher earnings.

This means that, at its current share price, Intesa offers a forward dividend yield of more than 11%. High yields like this are quite attractive and sometimes can be a sign that the dividend may not be sustainable, but I don't think it is the case with Intesa.

The bank is well-capitalized and has a good earnings history, which makes its dividend sustainable. However, given that its payout is directly related to earnings, its dividend may be cut in the future if earnings also come down, justifying its current high-dividend yield.

Conclusion

Intesa is a bank with good fundamentals within the European banking sector, and its current high-dividend yield is quite attractive to income investors. While some could consider this a warning sign that dividend sustainability may be questionable, in my opinion, this reflects undervaluation of its shares rather than an issue with the dividend sustainability.

Indeed, Intesa is currently trading at 0.8x book value, practically in line with its average over the past five years, despite reaching record profits and reporting a double-digit ROE. This clearly means its shares are undervalued and its high-dividend yield is sustainable, being a good income play in the European banking sector right now.

For further details see:

Intesa: Undervaluation Leads To Sustainable 11% Dividend Yield