INTT - inTEST Corporation: Time To Buy This Acquisition Machine

2023-11-29 02:19:22 ET

Summary

- inTEST Corporation, a test equipment producer, experienced a drop in share price from an all-time high of $26 to around $13.

- Cash flow growth has been driven by strategic acquisitions, with a focus on expanding into different industries and geographic areas.

- inTEST recently raised $19.3 million through the sale of shares and has a cash position of $41.7 million, which will be used for future acquisitions.

inTEST Corporation (INTT) produces test equipment that is used in manufacturing for a variety of industries, to include automotive, defense/aerospace, industrial, life sciences, security, and semiconductors. Its shares reached an all-time high of $26 this summer. With the recent drop to more typical levels around $13, I will make the case that INTT is a buy for folks who are interested in the long-term, acquisitive growth of a business that is very cash-flow positive.

Operations

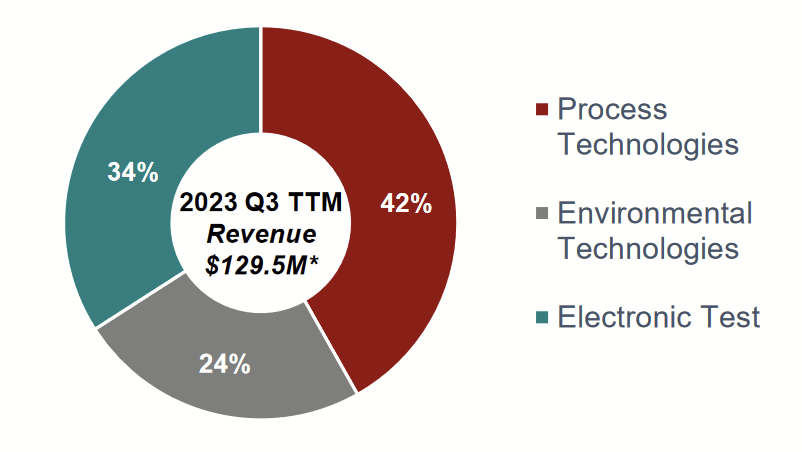

Simply put, inTEST provides the means for a wide variety of manufacturers to tests their products in development, much like we've seen in documentaries since we were kids in school. The company reports its results through three segments: Electronic Test, Environmental Technologies, and Process Technologies, which account for 34%, 24%, and 42% of revenues respectively.

{kind=link}

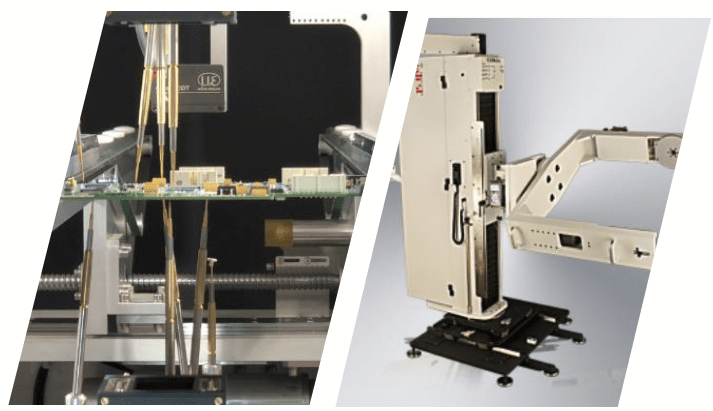

Electronic Test

A large portion of this segment is equipment for semiconductor testing. Additionally, this segment also helps with battery testing, which is expected to be an area of growth going forward with EV.

{kind=link}

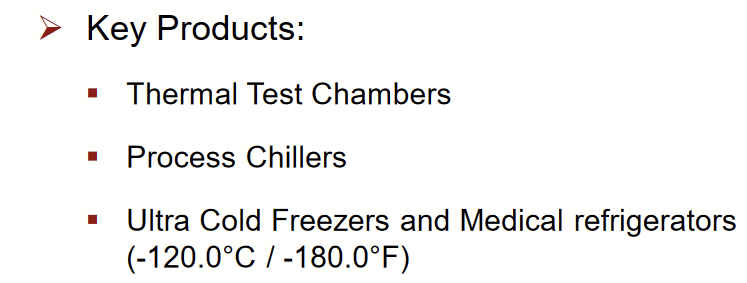

Environmental Technologies

These tests help subject products to intense temperatures (hot or cold), depending on the type of operating environment they may require them to withstand.

{kind=link}

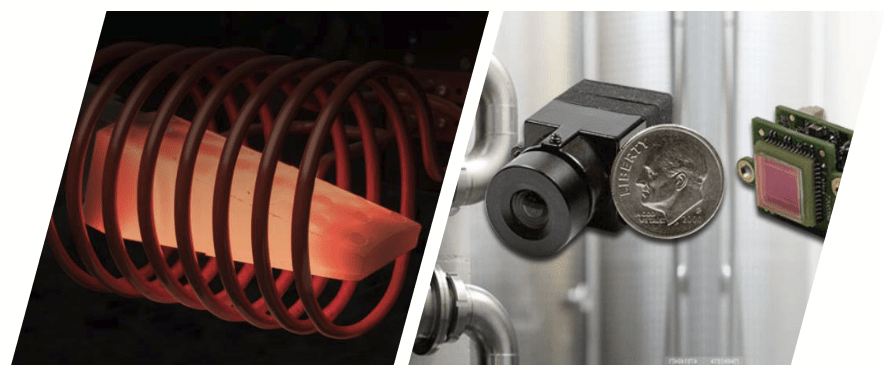

Process Technologies

This segment provides induction heating tools and camera tools for safer observation.

{kind=link}

Geographic Spread

Slide 6 of their Southwest IDEAS presentation shows their revenues for 2022 by region. 45% of revenues were in the Americas, 25% in Asia-Pacific and 20% in Europe, Middle East, and Africa.

Company presentation

As shown while sales are global, their products are manufactured in more developed and stable regions.

Recent History

Since going public in 1997, most of the company's growth has been through strategic acquisitions. The company provides a convenient list of these on their website.

A significant portion of their cash flows have been dependent on semiconductor products, leading to their acquisition of Ambrell in 2017, whose products gave it exposure to more markets. After seeing the challenges posed in 2020, the company adopted a Five-Point Strategy in 2021 .

Five-Point Strategy (2021 Investor Presentation)

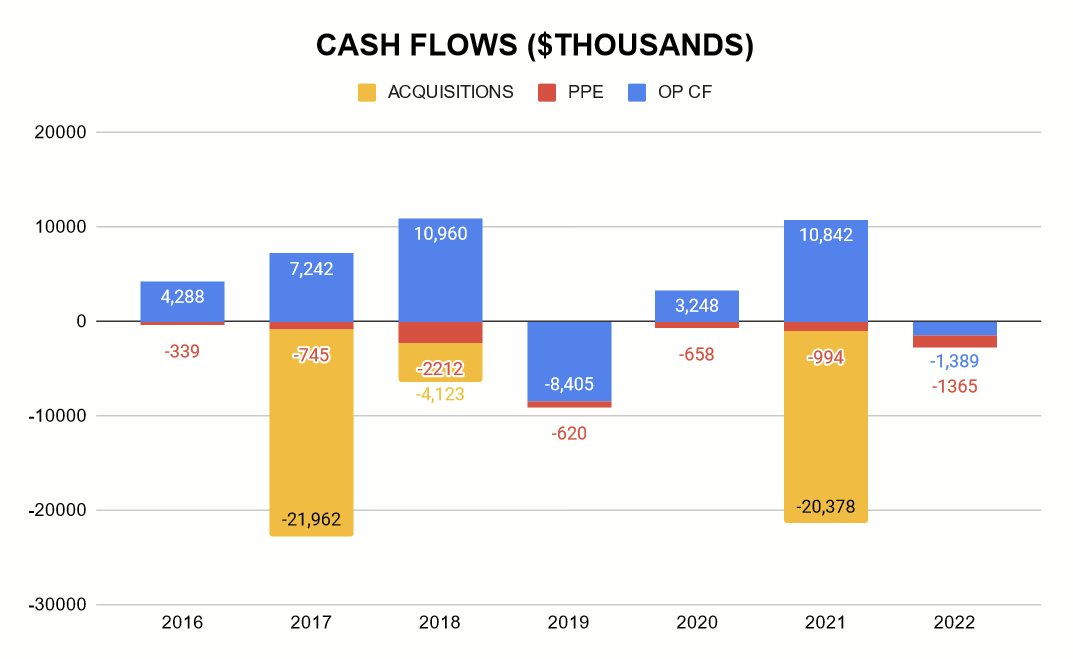

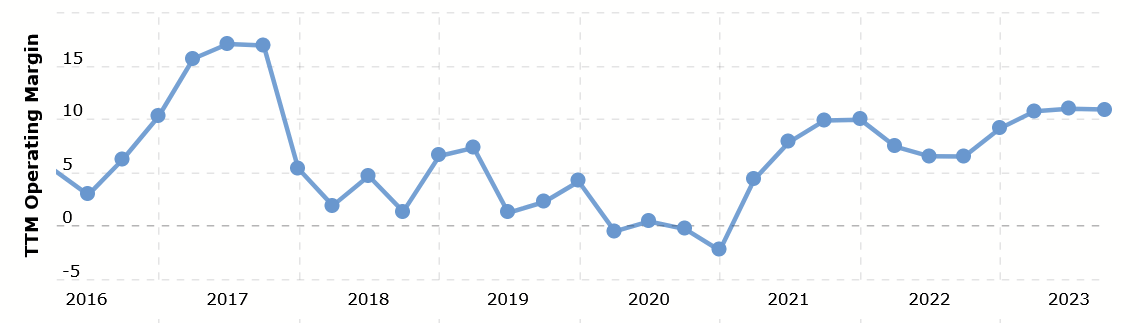

With that, the company has been working to make further acquisitions in order to expand their reach into other industries and geographic areas. InTEST went on to acquire North Sciences, Videology Imaging Solutions, and Acculogic in 2021. The following graph shows the history of their cash flows prior to this plan and directly afterward.

Author's display of 10K data (INTT's 10Ks)

{kind=link}

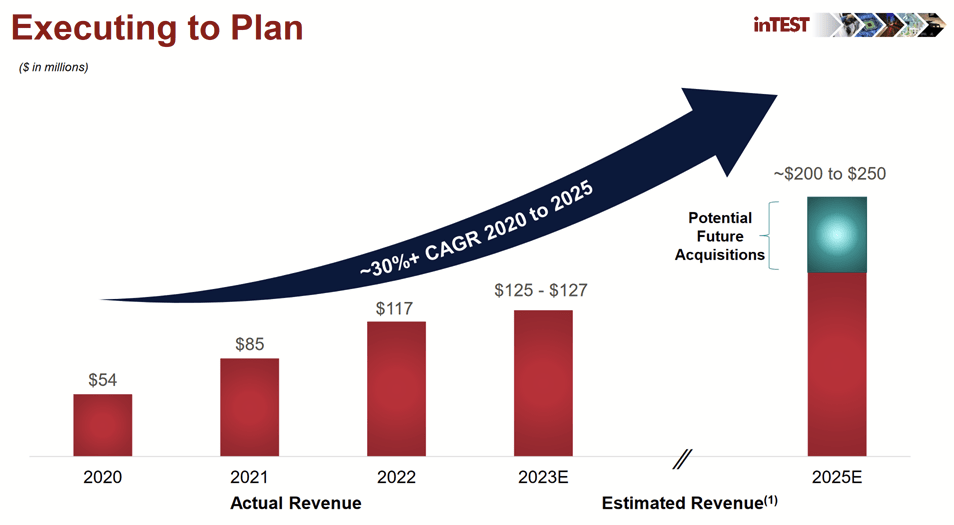

The impact can be shown with how the company's revenues and cash flows have been growing and where they expect to be. (Quick note on 2022's negative cash flows: That was largely due to accumulating inventory in an attempt to get ahead of supply chain constraints).

Screenshot with addition by author (2022 10K)

{kind=link}

Showing current and projected revenue growth (INTT Investor Presentation)

{kind=link}

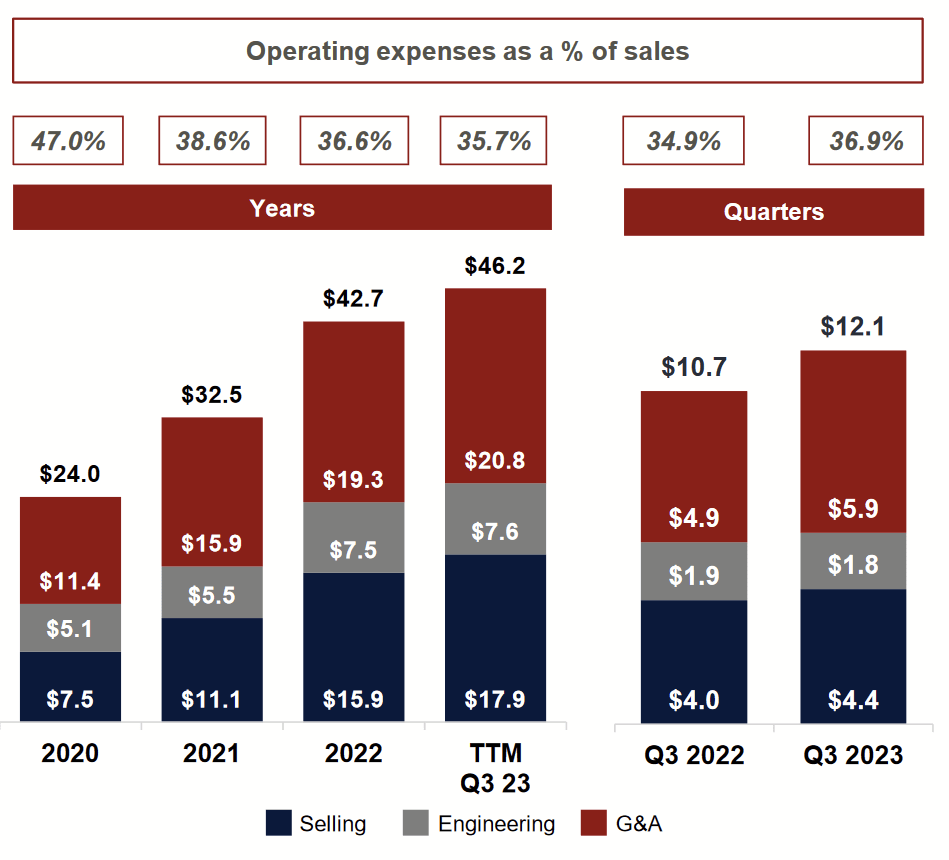

Similarly, their Q3 2023 earnings shows how operating expenses as a percentage of total sales have been decreasing.

{kind=link}

In total, while the cash flow statements since 2016 have been lumpy, we see a business that is becoming larger and leaner, realizing synergies and economies of scale. Operating margins have improved with adoption of the plan.

{kind=link}

Events of 2023

While the company has rarely issued or bought back equity, in July they announced that they had sold 921,797 shares, raising $19.3 million. They benefited from the elevated stock price during time, raising the capital at an average share price of $21.70. The purpose is to use this cash for future acquisitions, in pursuit of the Five-Point Strategy.

{kind=link}

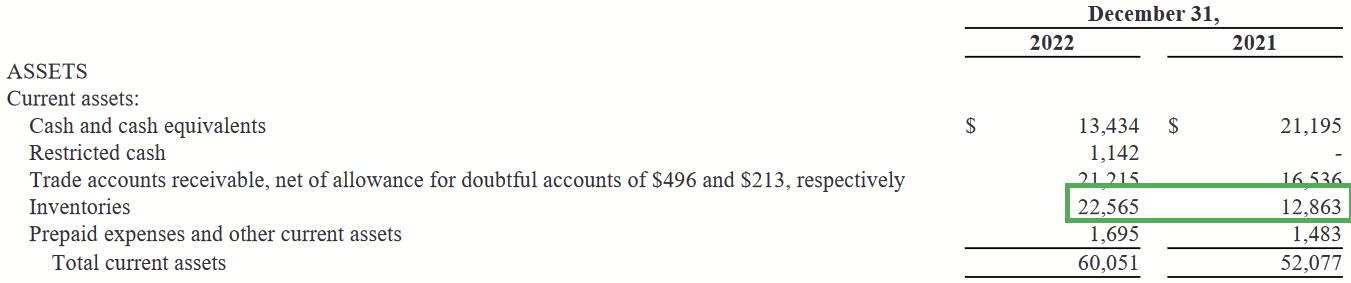

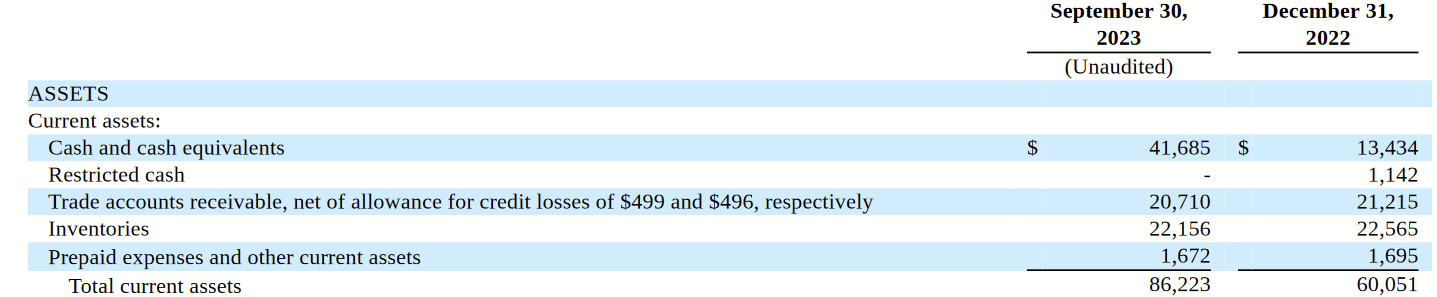

inTEST's cash position has grown from $13.4m at the end of 2022 to $41.7m now. Nevertheless, the company is sitting on that cash until they see the right opportunity to make an acquisition.

Future Outlook

The company is working to diversify its portfolio of products to minimize its dependence on semiconductor tests. That is why they have been actively acquiring new subsidiaries and continue to do so.

{kind=link}

While the company sees growth in semi, not decline, it sees more ambitious growth in other markets.

Additions to Property, Plant, and Equipment (PPE in my bar chart earlier in this article) have been much smaller than capex used for acquisitions, usually only between 1% and 2% of annual revenues. If their business really is so capital-light, then acquisitions are the key to growth and increased cash generation.

Acquisitions

In the Q4 2022 earnings call , President/CEO Nick Grant explained to analysts:

So, yes, our teams remain very active on M&A. As we've commented in the past, the business that -- the approach we take is really more of a bottoms up, where the each of the three technology divisions are driving pursuits and targeting companies and trying to build the right relationships to get them to see the benefits of being part of inTEST. And that activity continues. As for timing, it really comes down to when you got agreed upon seller, price -- agreed upon price and due diligence has been fully vetted.

This gives some insight into why inTEST hasn't spent the cash that it raised earlier this year for M&A. It clearly wants the capital ready to deploy, but it takes a patient approach in its acquisition, getting not only a good price but making sure the acquired understand their stake in the deal. In the long run, I think this will serve the company well. Grant elaborated this further for Q1 2023:

So, yes, as we've noted that these acquisitions were really the lifestyle businesses ran to a certain level, and we saw the ability that being part of inTEST, getting them integrated into our processes and procedures and the way we operate, we believe we could scale these things. And each one is a little different in some areas where investments were needed.

But in general, it's about driving innovation into these businesses, building robust product road maps that are market-driven as one of the key avenues for growth that we're driving across all three. And I'll give you an example. The North Sciences freezers and chiller refrigerators that you were referencing there.

We completely rebranded, I would say, upgraded some of the designs and launched the new product lines after acquiring that business and then have continued to expand our capability and functionality at these products with adding cloud-based monitoring, et cetera, into the products.

This explains why operating expenses continue to decline as a percentage of revenues. They make acquisitions with the knowledge , not merely the confidence, that there is room to create new value where it did not previously exist. Then they execute accordingly.

Valuation

inTEST generates cash and is compounding INTT's value with every acquisition. Inventory that made 2022 negative has been selling, with free cash flow of over $10 million for YTD in 2023 ( see cash flow statement ).

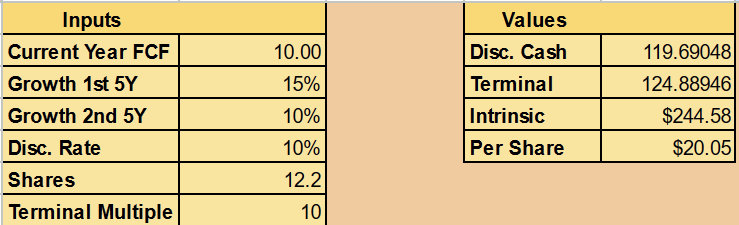

I believe that the company is capable of generating at least $10 million in cash each year going forward, and so I will use that as the basis for my Discounted Cash Flow analysis. Here are my assumptions:

- 15% growth for the next five years with abundance of M&A candidates before them.

- 10% after that to allow for slowing of M&A.

- A terminal multiple of 10 since the company's acquisitive nature and small size allows for steady growth into the future.

Author's calculation (Based on 10K data)

{kind=link}

With these assumptions, I believe a fair market cap puts the company just over $240 million and shares of INTT at $20.

Risks

Let's talk about the various things that could undo or complicate this thesis.

Semi Market

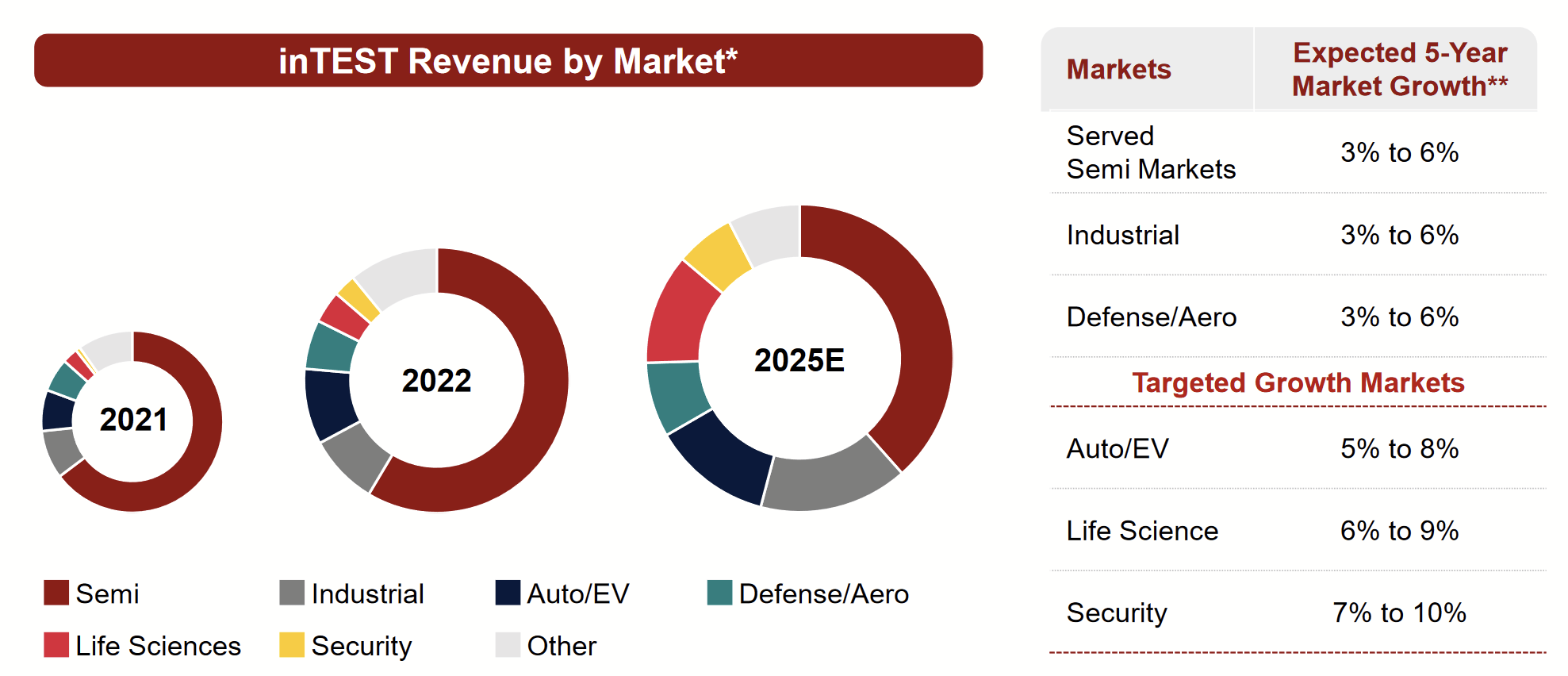

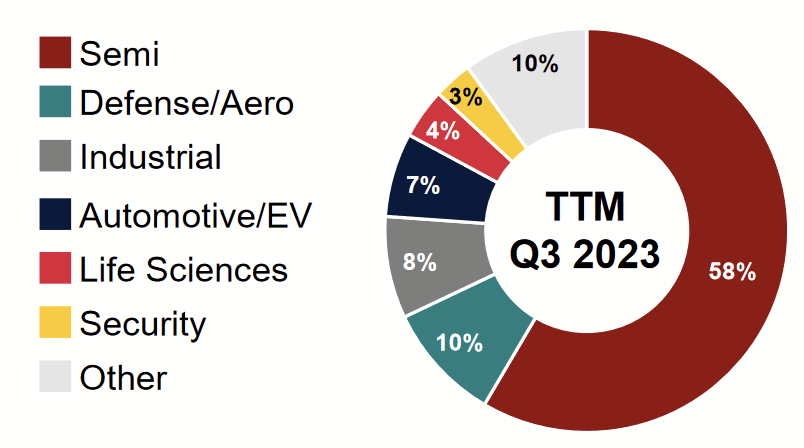

With their acquisitive model funded largely by operating cash flows, anything that might disrupt the semiconductor industry could hurt demand for their tests, reduce sales, and thus delay their ability to continue M&A. This may not wipe the company out, but cash for growth is really part of the story here. Let's look at some data to illustrate this better.

{kind=link}

A majority of their current revenue comes from products that serve the semi market. A disruption for their semi customers before valuable acquisitions can be made would set back their ability to grow and compound. I believe that each successful acquisition is a step toward lessening this risk and opening more doors for capital deployment, so it's worth reviewing each successive year.

Takeover

Sometimes a company is too good to overlook. As a microcap, inTEST could easily be gobbled up by a conglomerate. While this would probably mean a profit for today's buyers, it also means that the full upside may not be realized, forcing some folks to rethink their portfolios suddenly.

Lumpy Cash Flow

DCF is run with an idea to stable or average cash flows. inTEST cash flow growth may not go that way, even if does average out that way. Cash flows could be much lower in certain years (as has happened), causing the market to worry and beat the stock price down. The market gets especially nervous when microcaps have years like those.

Those who buy today must be willing to hold the shares for several years and to take advantage of such declines.

Buybacks

Buybacks are low on the company's priorities and have been rare, but the company will pursue these opportunistically. If they occur, investors need to figure out why. Is it because INTT prices happened to be unusually low? Is it because they are running out of M&A opportunities? That answer can make a big difference for long-term returns, and I think the latter is the more concerning of the two.

Conclusion

Everyone needs to test their products on the assembly line. We've seen it in all those educational videos since we were kids. This is the company that makes that possible. With positive cash flows, high-return acquisitions, a flexible product line, and strong operating margins, inTEST provides an opportunity for long-term capital appreciation to today's buyers.

For further details see:

inTEST Corporation: Time To Buy This Acquisition Machine