INTT - inTEST Corporation: Wait For A Better Entry Point

2023-03-23 12:01:49 ET

Summary

- INTT's service expertise in the semiconductor front-end space should find plenty of takers as wafer manufacturing becomes more complex over time.

- INTT has the appropriate balance sheet to fulfill its inorganic ambitions, and cash generation potential could pick up in the quarters ahead.

- INTT is an expensive stock to own, and the risk-reward on the charts looks unappealing.

Company Snapshot

inTest Corporation ( INTT ) is a New Jersey-based entity that provides test and process solutions for manufacturing and testing work across the globe. INTT's expertise is tapped by quite a few end markets ranging from semiconductors, defense, aerospace, autos, telcos, and pharmaceuticals. The company has four manufacturing locations across the US, with its sales and service network spread across seven countries across the world. INTT currently reports under three operating segments:

- Electronic Test (~34% of group sales)

- Environmental Technologies (~26% of group sales)

- Process Technologies (~40% of group sales)

INTT - What's To Like?

Whilst inTest offers exposure to quite a few end markets, there's no denying the fact that currently, this is still very much a semiconductor-driven business; that market alone accounts for close to 60% of group sales.

Given the ever-growing penetration of electronics and digitization over time, it's hard not to appreciate the long-term secular outlook of an INTT, which plays an integral role in the semiconductor value chain. INTT is well-positioned here as it currently services both the specialized wafer manufacturing (front-end) side, and the IC (Integrated Circuits) testing side of this market.

While INTT's back-end side of the service portfolio could likely remain pressured in the second half of 2023, I would urge investors to focus more on the long-term potential of the front-end side, given the growing pressure that semi-manufacturers feel in their attempts to extract higher production yields, even as the complexities of IC manufacturing only deepen with the passage of time.

INTT's proprietary portfolio of test head manipulators, docking stations, test interfaces, and industry heating solutions are well suited to cope with the rigors of growing texting complexity. In fact, in FY22, much of the 25% revenue growth generated by INTT's semi-business was driven by growing demand for the company's induction heating solutions for silicon-carbide crystal growth.

INTT management is also currently doing an excellent job in driving through superior operating leverage. Over the last four quarters, OPEX as a function of sales has collapsed by over 1100bps. Admittedly, much of this could be attributed to strong demand for INTT's services (Q4 was a record with $32.4m of sales, up by 45% YoY) as the cost base is still getting incremental bumps from M&A integration.

Q4 Presentation

Revenue visibility looks rather comforting in the quarters ahead, as approximately 45% of the current order backlog (~47m) could be reflected in the numbers beyond Q1-23 (In Q1 they expect to deliver $30-$32m).

Inorganic growth is also an integral part of the INTT story (going forward INTT will likely look to pick up entities specializing in induction heating, or those which give them an expanded geographic presence) and it's comforting to note that the company has the requisite balance sheet to facilitate these ambitions as its debt to EBITDA ratio is only 1x, lower than its long-term target of 2.5x).

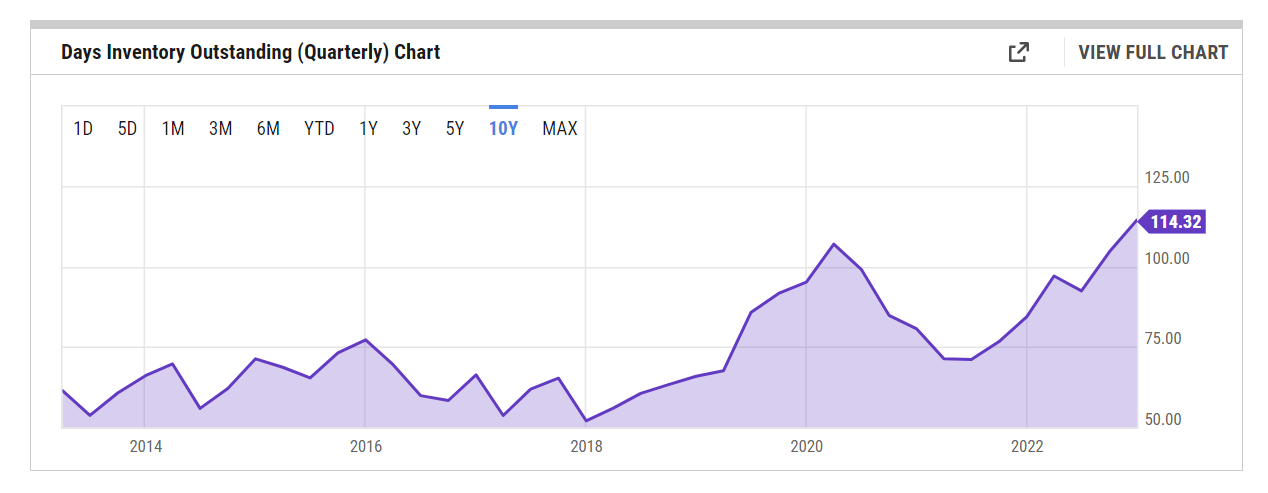

INTT could also have some support from internally generated cash flow, After the first two quarters where INTT witnessed negative operating cash flow, mainly on account of heightened inventory builds, things have turned around in recent quarters with the company generating $3.7m of positive cash flow in aggregate. Management noted that going forward they would be in a position to generate positive operating cash flow, and you'd want to believe them as the days in inventory are at exceptionally unsustainable levels (the highest in a decade); some mean reversion here should certainly abet operating cash generation going forward.

{kind=link}

Forward Valuations Are A Concern

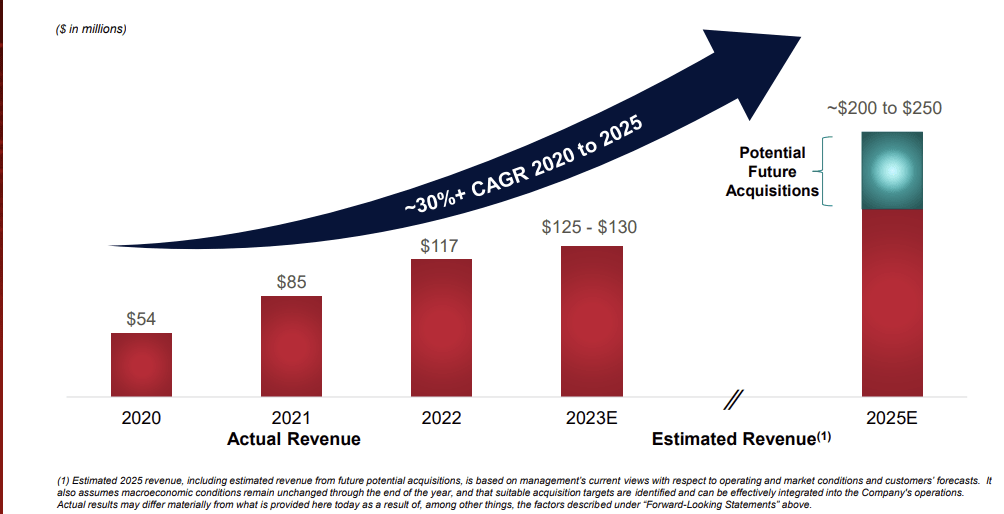

INTT's management believes that by 2025 , they could hit group sales of $200m-$250m, which would translate to a 3-year CAGR of 20-29% from current sales levels (less than $120m at the end of FY22). However, investors should also note that not all the additional $80-$130m of incremental cumulative sales will come from organic sales. Rather, the company expects future M&A to contribute more than a quarter of those incremental sales. Baking future M&A into the FY25 number feels like a wildcard of sorts, as much will depend on INTT's cash flow generation, capital structure, and acquisition multiples at any point in time.

{kind=link}

In that regard, sell-side analysts have done well not to bake in those additional M&A numbers with INTT's core organic business expected to generate only $144m of sales by FY25, which would translate to 2% revenue growth from the FY24 expected sales number.

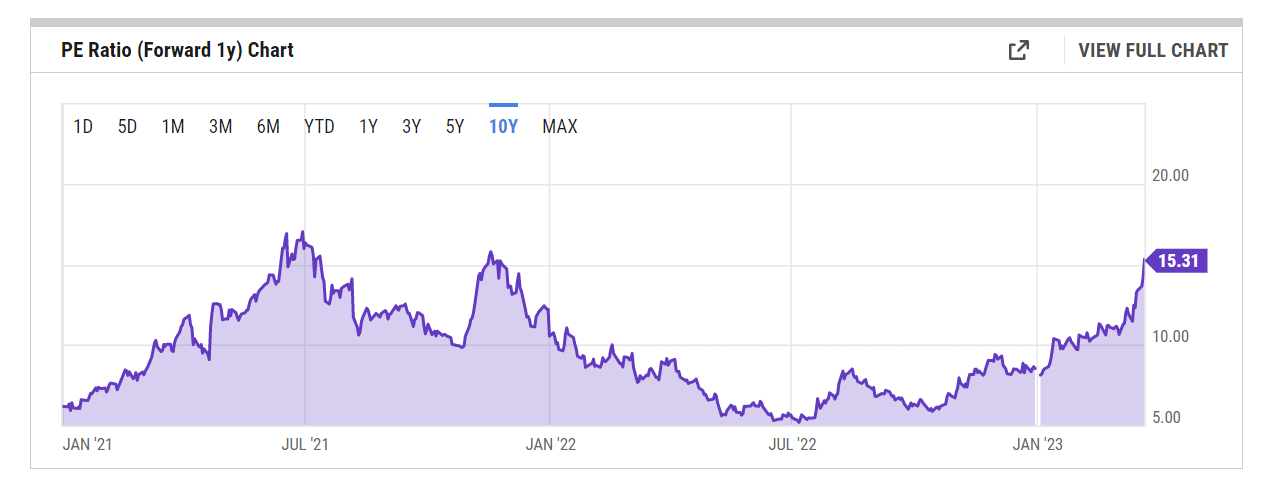

Speaking of analyst forecasts and how that translates into valuations, note that INTT is expected to deliver FY24 EPS of $1.287, which would represent earnings growth of 11% over the expected FY23 EPS of $1.157. On a forward P/E basis (based on the FY24 EPS), that would translate to quite a hefty multiple of 15.31, a 60% premium over the stock's 5-year forward P/E average of 9.6x, not to mention that the PEG (Price to earnings growth) is sub-par at 1.39x.

{kind=link}

Of course, all these multiples could look a lot more palatable if INTT is able to do a bunch of fresh earnings accretive M&A within the next 12-18 months, but as things stand, this is not a cheap stock to own.

Closing Thoughts - Stock Looks Overbought

A potentially bullish stance on INTT is also tempered by the unattractive risk/reward on the charts.

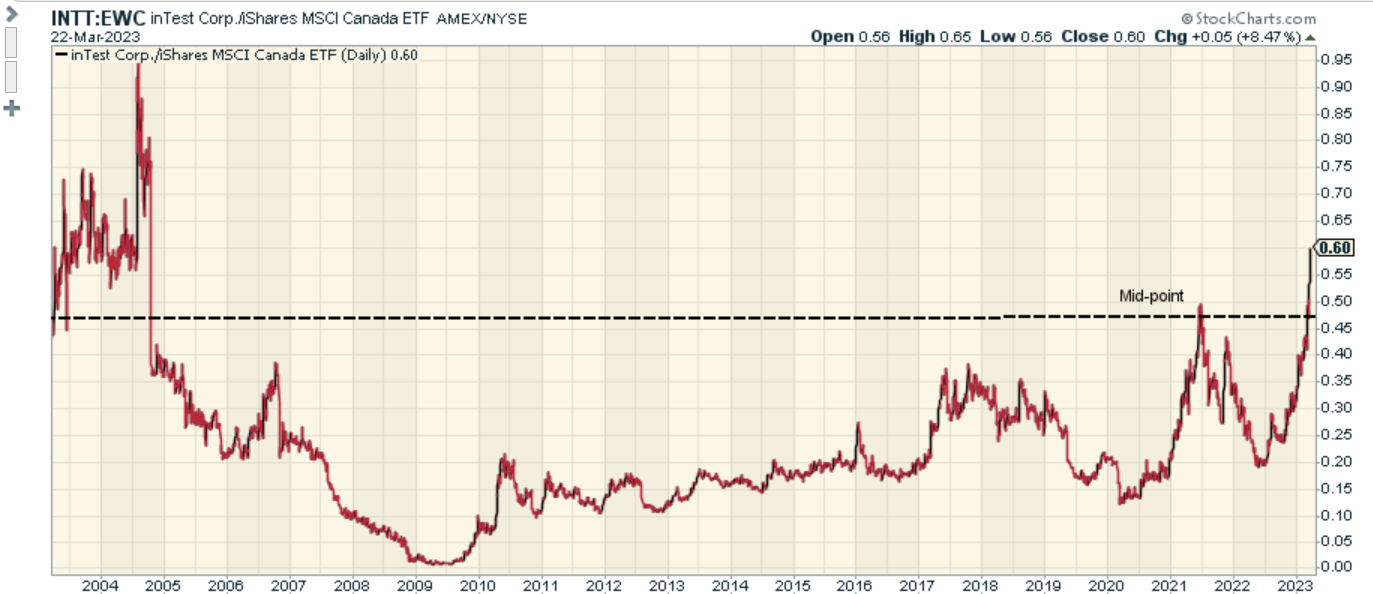

From 2009 until 2021, one could have promoted INTT as a potential mean-reversion candidate in the micro-cap space, as its relative strength ((RS)) vs other micro-cap options was well below the mid-point of its long-term range. That thesis no longer holds as the RS ratio has now crossed the mid-point, dampening the incentive for rotation into INTT.

{kind=link}

If one looks at INTT's daily price imprints, it is heartening to note that the stock has now hit its highest point in 23 years, but getting in at this juncture would be quite risky, as it looks enormously overbought. For context, the stock has now exceeded the upper Bollinger band (something which doesn't happen too often); put another way, the stock is now trading well past two standard deviations from its 20-day moving average and could stand a pullback. You don't want to be getting in when the rubber band looks enormously stretched.

{kind=link}

For further details see:

inTEST Corporation: Wait For A Better Entry Point