INTT - inTEST: Undervalued Profitable And A Buy After Considering Risks

2023-08-14 05:18:05 ET

Summary

- inTEST Corporation trades at a discount compared to the Information Technology sector, making it attractive from a valuation perspective.

- The company operates in the semiconductor industry, supplying testing and process technologies to both assembly plants and directly to end users.

- While inTEST has demonstrated revenue growth, there are challenges in sustaining market strength and potential risks from economic conditions and pricing pressures.

- It is also profitable and improving its cash position.

- Taking into consideration the above opportunities and risks, I have a buy rating with a 10% upside.

As shown in the one-year performance chart below, after its recent 27% slide, inTEST Corporation ( INTT ) now trades at a forward Price-to-Sales ratio of 1.6x, which represents a 41% discount with respect to the Information Technology sector.

This makes the stock attractive from a valuation perspective. Still, more research is required, namely in terms of the stock's ability to sustainably generate sales in these uncertain times together with cash position. It is precisely the objective of this thesis to chart an investment case for this semiconductor play valued at $198 million and which beat both the topline and bottom-line expectations when its second-quarter (Q2) financial results were released on August 4 .

I start by highlighting its role in the semiconductor (semi or chip) industry and how its quarterly revenues have progressed.

A Supplier of Testing and Process Technologies

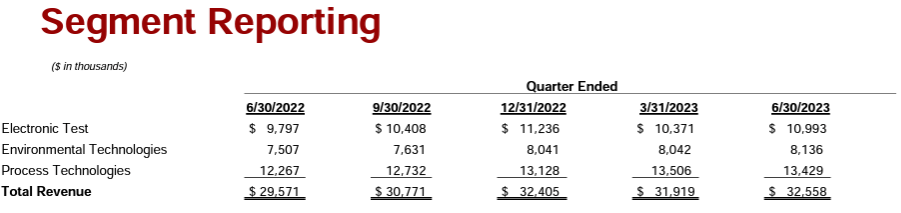

With the extensive use of everything from sophisticated smartphones, laptop computers, to digital cameras, without forgetting common consumer electronics, the semiconductor industry has evolved considerably. Furthermore, the manufacturing of all these devices in turn drives the need for semiconductor testing equipment and process technologies, which together formed 75.3% of the company's revenues in Q2. The rest is made up of the Environmental Technologies segment as shown below.

Company Presentation (static.seekingalpha.com)

{kind=link}

For investors, the chip market consists of the broader section which comprises mainly compute processing, memory, and RF communications chips. Then comes the more specialized section consisting of wafer production and automated testing equipment. This is the section where inTEST mainly operates and it sells electronic testing gears to chip manufacturers needing to quality check their products to meet certain standards as well as to OEMs (original equipment manufacturers) who embed them within their own integrated circuits before reselling. The company also sells directly to end users not necessarily operating in the chip business, but instead coming from the industrial (automotive, defense, and aerospace), and life sciences markets.

The same is the case for its Process Technologies and Environmental Technologies products which are sold both to chip assembly companies and end users. Now, as the largest segment constituting 41% of Q2's revenues, Process Technologies also saw a 9.5% YoY growth, and its products play a vital role in the production of wafers, or crystalline silicon used as the base for building up complex electronics.

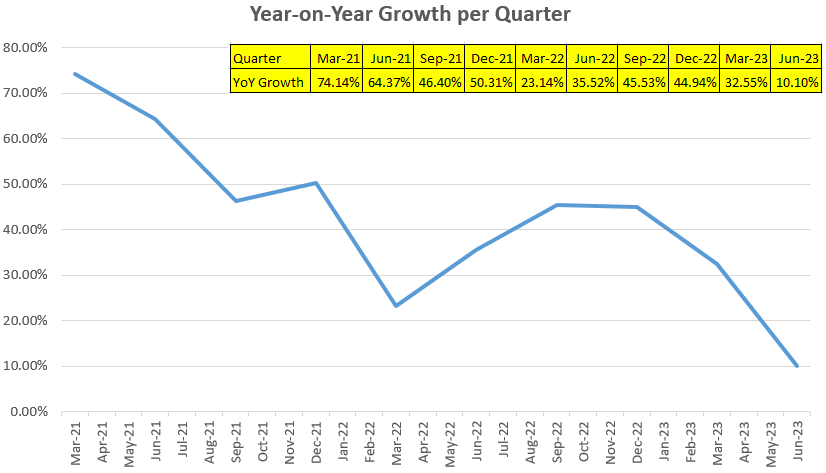

Hence, as a key player in the semiconductor ecosystem despite its relatively smaller size compared to Teledyne ( TDY ) which is currently valued at over $18 billion and also produces testing gear, inTEST delivered record revenue of $32.6 million in Q2. However, looking closer, at 10.1%, this is the slowest YoY growth in ten quarters as charted below.

Chart and table built using data from (www.seekingalpha.com)

{kind=link}

This begs the question of whether the company can sustain the same strength in its markets as before given the competition. There is also the fact that after experiencing supply chain challenges for most of 2021 and 2022 and having replenished their stocks, its customers may reduce orders.

Growth Challenges and Potential Solutions

An answer is obtained by looking at the gross margins.

At 46.2% in Q2, they increased by 0.4% YoY which was partly due to improved pricing . This shows that the company is not having to cut prices to drive sales at the moment. Furthermore, margins were also helped by a better product mix involving strong demand for innovations like the flying probe test systems in the defense and aerospace industries and image capture equipment used for security purposes.

On the other hand, with the normalization of supply chains, customers are ordering less which means that it is unlikely for inTEST to return to the same level of demand as before 2023 by relying exclusively on organic growth. Moreover, based on the mid-point of the topline guidance of $129 million for 2023, the company should grow by 1% over 2022. This represents a marked deceleration from the 37.6% and 57.7% achieved in 2022 and 2021 respectively and could be one of the reasons why investors have avoided the stock despite its low valuation.

However, even the growth of 10.1% achieved in Q2 is better than the IT sector median of 9.87% and inTEST also comes with other positives for investors looking for opportunity.

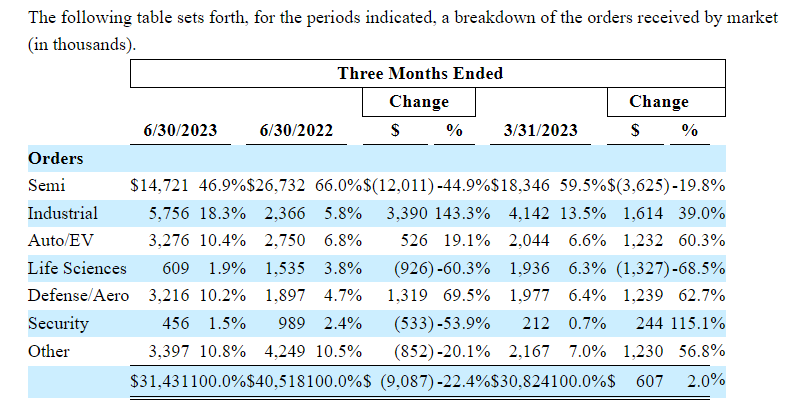

The first pertains to demand visibility, which is provided by the breakdown in orders below.

Order Breakdown (www.seekingalpha.com)

{kind=link}

Thus, total orders for Q2 were $31.4 million which decreased markedly compared to the $40.5 million for the same period last year but still represented an increase over the first quarter of 2023's $30.8 million. Moreover, despite declining, the backlog (or orders which have to be fulfilled) of $45 million still represents 1.4 times Q2's total revenues which also implies that the company has some cushion against any drastic fall in demand.

Second, in anticipation of subdued demand, the company has started to reduce its inventory levels as charted below. This in turn reduces the risks of inventory write-off in case some of the items manufactured become obsolete in light of rapid technological changes in the markets served.

Third, after accounting for 47.6% of total sales in Q2-2022, the share of the U.S. dwindled to only 30.4% in the last reported quarter as shown in the table below. Thus, with more sales coming from the rest of the world and the dollar index down by more than 2% in the last year, the company is benefiting from forex-related gains. This lower dollar trend could continue given that the latest CPI data shows that inflation has risen less than anticipated and also supports the case for the Federal Reserve to exercise a pause in the process of rising rates, normally unfavorable to the greenback.

SEC filing for Q2-2023 and Location of inTEST's assets (seekingalpha.com)

Moreover, the above figure also shows that inTEST's assets are mostly U.S.-based as its manufacturing operations are located in America, Canada, and the Netherlands. This signifies that the company will not be impacted by the recent Executive Order which specifically targets American investments in China and covers semiconductors, electronics, and AI.

Potential for Inorganic Growth and Cash Position

Another ingredient that could potentially support growth is the $19 million obtained through the ATM equity offering which has raised the cash position to $37.4 million giving a boost to the company's inorganic growth ambitions, in order to achieve the 2025 revenue goal of $200 million to $250 million whose mid-point represents a 76% surge over 2022's $127.7 million.

In this respect, the acquisition of Acculogic for about $9 million in December 2021 not only contributed to beefing up sales by 37.7% during the subsequent year but also enabled inTEST to improve demand visibility by being able to sell products to end customers directly. Therefore, an acquisition could help both in topline growth and diversification into new target markets.

Talking liquidity, the Acculogic acquisition has proved beneficial for the cash generated from operations perspective from 2022 as shown by the pale blue chart below. Now, given the modest Capex incurred to grow the business (deep blue chart), this uptrend is proving beneficial to the free cash flow, which was $2.9 million at the end of June.

Now, spending on growth impacts the balance sheet, and for this matter, I calculated the ratio of total debt to total equity as 21.5% at the end of Q2. Also, the debt stood at $14.1 million, after a repayment of $1 million.

Profitable and a Buy after Considering Risks

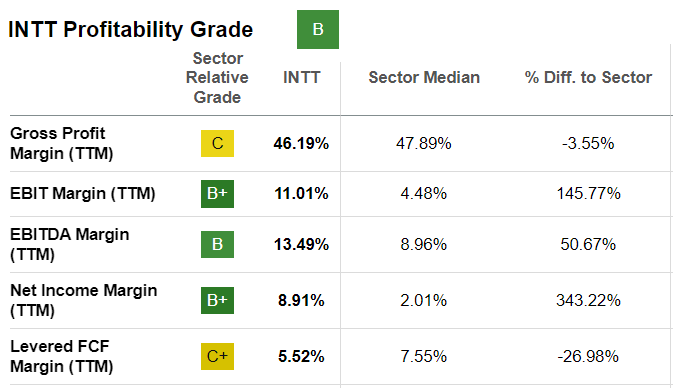

Therefore, inTEST does have the means to grow organically without weighing down too much on its balance sheet. In this respect, its profitability grade of B also provides some comfort as to the way costs are managed, especially for those willing to put their money into the stock.

Profitability Grade (seekingalpha.com)

{kind=link}

Thus, the stock is a buy, and assuming only a 10% upside given its 27% one-month slide and 41% valuation discount, I have a target of $18.5 (16.83 x 1.1). Now this represents moderate gains but accounts for the following risks.

First, revenues can be impacted by economic conditions in the rest of the world where inTEST obtained nearly 70% of its revenues in Q2 being less favorable than last year. By comparison, the U.S. economy is proving to be more resilient . Second, given that demand is no longer what it used to be in 2022, customers may exert downward pricing pressures which may prove detrimental to the company since it relies on relatively few customers for a significant portion of sales. Third, in a worst-case scenario, the company may have to liquidate inventories to avoid product obsolescence in case the assembly plants which purchase its products switch to competitors' technology.

In conclusion, this thesis has shown that inTEST is a buy as it has the potential to compensate for lower organic growth through M&A, and the management update provided during Q2's earnings call support this possibility. Also, the business model uses relatively less capital, and with more cash generated through operations, it can further improve FCF and profitability.

For further details see:

inTEST: Undervalued, Profitable, And A Buy After Considering Risks