ITJTY - Intrum: Likely No Dividend In 2024 But Superb Upside Potential - 'Buy'

2023-08-28 10:12:00 ET

Summary

- Intrum has faced challenges and its stock price has dropped, but the company's long-term potential remains strong.

- The company has made successful market exits and is focused on improving its balance sheet and reducing debt.

- Despite short-term issues, Intrum's business performance is solid, with strong financial indicators and a continued demand for its services.

Dear readers/followers

On the surface of things, it might be hard to see why Intrum ( ITJTY ) ( INJJF ) is a popular investment of mine or an investment I believe you can consider. After all, the company has absolutely crashed beyond what I believed it to be able to. But at the same time, there are reasons for this, and those reasons are logical. At least in part.

The company's earnings or long-term potential are not part of this reason, nor are the company's future plans. If you look at Intrum from a 3-5-year term, there is absolutely no reason that I can see why it should trade at the levels it's currently trading at. Problems? Sure, the company has some problems. But most of those are short-term.

In this article, I will be updating you on this company and show you why I am "long" this company, and continue to believe in its long-term potential. I've added shares both on the commercial and my personal portfolio and more than that, the company remains a favorite options play of mine, enabling an annualized RoR of over 30% during key drop days.

Let me show you why this could be a better upside than you might expect.

Intrum - More challenges than expected, but it doesn't change the thesis

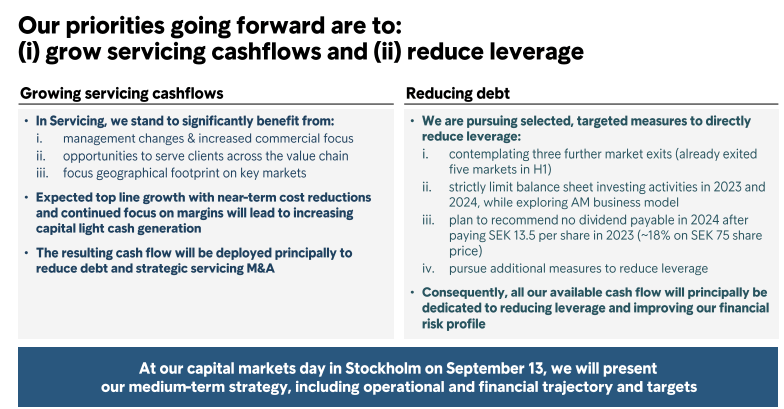

So, Intrum has certainly gone lower than I initially expected. The company has also clarified that the company won't (likely) pay a dividend for the year of 2023 - meaning its 2024 payout.

The reason for this is simple. Improving the company's balance sheet.

Results for the company were far from bad.

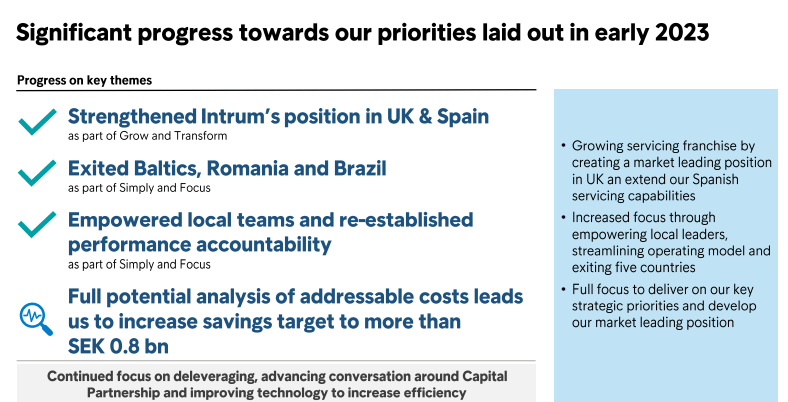

The 2Q23 period is the latest set of results we have here. Some of the main highlights include successful market exits from higher-risk markets including the Baltics, Romania, and Brazil. The company, in classic fashion, bit off more than it could chew here. It's also looking to sell the Czech Republic operations, Slovakia, and Hungary. All of these countries are non-core markets at relatively minor revenue shares for this company.

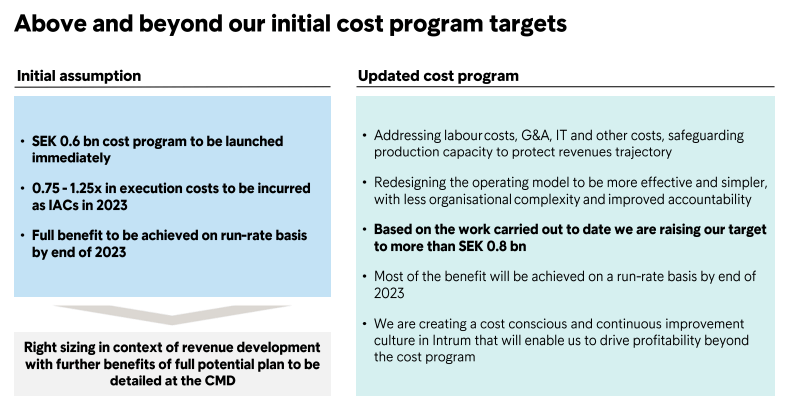

Intrum has also delivered much of its cost savings program and upgraded the target to 800M SEK.

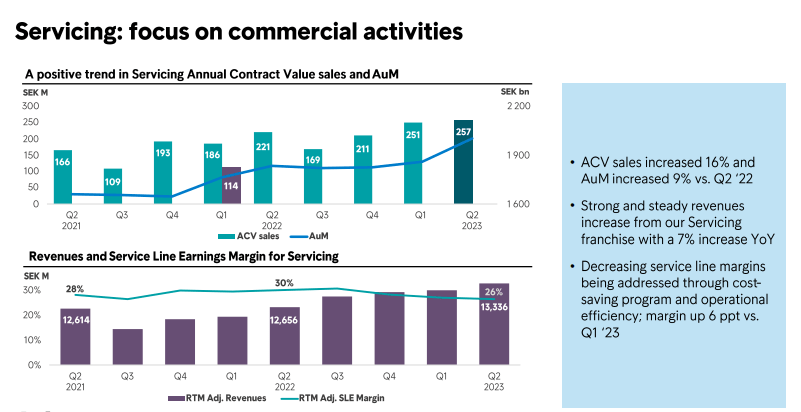

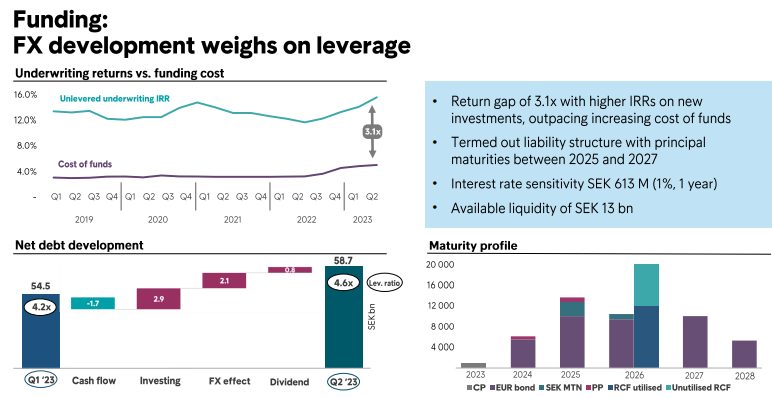

However, the underlying results were absolutely solid. They were seasonally stronger than Q1, and the company generated 92B SEK in collecting for the quarter, as well as 13.3B in revenues. AUM is up 9% YoY, which puts the company's servicing segment at 2,000B SEK, or 2T SEK, and an investing segment valued at 41B SEK in book value. Cash collection was up, cash revenues were up, organic growth was close to double-digits, and service margins were up.

The company's targets are clear and logical. Debt reduction is primarily on the schedule, as it should be.

{kind=link}

And every key performance and fundamental indicator speaks to a continued demand environment for Intrum's services. The European Payment report implies €275B in costs for payment collecting, with 5.5% inflation and 70% of businesses likely to encounter credit losses as over 70% of Europeans encounter higher costs of living.

Now guess, with Intrum being the largest credit collection company in all of Europe, who'll be harvesting much of those fees and advantages?

This is why trends, despite the share price, are absolutely solid.

{kind=link}

The investing segment also remains absolutely stellar, with the investing performance PI Index above 100%, and Gross Cash collection up 8% CAGR to over 13.5B SEK for the quarter.

That means despite what the share price performance would suggest, and it looks abhorrent at this time, the company's actual business performance remains absolutely fantastic, with only minor gripes.

The key problem with Intrum is that they failed to properly account for the severity and speed of the rate cycle, and took on too much risk back when they were acquiring portfolios and assets. This left them with too much risk, which then in the new environment, quickly turned sour and required the company to make new plans to remain "safe".

Priorities are clear, and the company is delivering on these.

{kind=link}

If we'd had another year or two before the rate cycle that began last year, we'd probably have seen Intrum do good things with some of these secondary emerging growth markets. But given the current market environment that is not something Intrum has the resources to do.

Key financial indicators are actually stronger than usual if we consider the fact that we're in a transition year and in a seasonally weaker quarter. 2Q is usually a so-so quarter, with 3Q the seasonally weakest, before 4Q usually blows it out of the park - but revenues were still up for 2Q YoY. Costs were up as well, and the dividend as well as depreciating FX led to an increase in debt. Intrum has the short end of the stick when it comes to this entire weak SEK problem.

However, positives include the cost program...

{kind=link}

... and really all of the segments in terms of the business doing better than expected. Cash EBITDA is at almost 2.8B SEK for the quarter, with a margin of 76%. Collections are improving, and while the funding costs are increasing, the unlevered IRR for underwriting is also increasing.

When I write about REITS, the money the company makes, the difference between the company's cap rates/returns and WACC is the key to good investing.

The same is true when it comes to Intrum, only with different numbers.

And these numbers are absolutely stellar.

{kind=link}

Intrum is therefore somewhat higher in debt, but as you can see they have maturities well-laddered for the next 5 years, and the company is impressively profitable even with FX weighing things down as much as we are currently seeing happening here.

The picture I want to convey in the 2Q23 here, and going into the remainder of 2023 and 2024 eventually is that the company is showing plenty of business resilience and underlying strength. Growth and margin expansion in key segments is present. The company has no choice but to aggressively address its risk profile - this unfortunately includes cutting the company's 2023E dividend - but the company will be paying out the second half of this year's dividend.

The company's declared and confirmed dividend for this year comes at a yield of over 18% for investors at the current price, annualized. My own effective yield is over 15% for the year - so the fact that the company won't pay one for this fiscal is annoying - but it's not something that breaks the thesis for me, because I can see beyond the 2023-2024 years, and where the company may arrive.

There's also the option for the company, depending on 2023 and early 2024 performance, to not cut it completely, as was voiced in the earnings call .

Jacob Hesslevik

Yes, of course it's up to the AGM, but, do you think that the Board could propose for example to cut it in half where it would pay out at least SEK 5 or something, it will have to be the same amount, or do you think...

Andres Rubio

All I can say is that today, given everything we know today, our intention is to recommend no dividend. In theory, obviously the world can change between now and next January when we have to ultimately provide a recommendation to the shareholders that will be decided upon at the AGM. But today, this is our intention, Jacob.

Things can change - and things certainly did change. But the company's "fortress" remains intact even with its current leverage. There are no breaches of covenants, no waivers, no headroom, and there are, at least theoretically, plenty of cash and debt sources that could still be used for dividends. But I would agree with management that this is not the most effective use of capital and what's best for the company at this time.

The company will provide more updates in its CMD - and I'll probably attend in person there, and seek to speak to investor relations.

But we'll see where things go and what we have. However, for now, I want to clearly state that there is no fundamental worries to me with regard to this company.

Intrum - Valuation is impacted by shorting and company performance

I'm not usually one to blame shorts or say that shorts are the reason why things are a certain way. I happen to like short-sellers quite a bit.

Why?

Because if there really is something to what they say, then their shorting and reports will usually draw my attention to it.

And if there isn't?

Then I'm getting cheap shares, knowing the business is solid and they're looking to make some money on the shorter investment timeframe -which I don't begrudge anyone, or them.

So I have no issue with this, despite Intrum now being one of the 10 most shorted stocks in all of Sweden. The current short-interest ratio of 2.0 is quite telling here, and the company's volatile 3-5% intra-day ups and downs bespeaks quite a bit about the company's current trends.

I have been trading this both on the common share basis, as well as on the options side. I have running cash-secured puts with a strike of 60 and an effective premium that puts my cost basis below 56 SEK/share. That's an annualized return, based on the expiration, of over 42%. I couldn't be happier about the trades this lets me set up. The company ended last week by going up almost 3% again.

If you don't believe in Intrum, now is obviously not a good time to invest.

However, if you seek to make a case against Intrum based on fundamentals here, then I want you to be aware of the following things:

1. This company sees such de-valuation trends with recurring frequency.

2. There is absolutely nothing fundamental about the company that is not working here, or indications that earnings performance is going to decline. The company is projected for double digit growth.

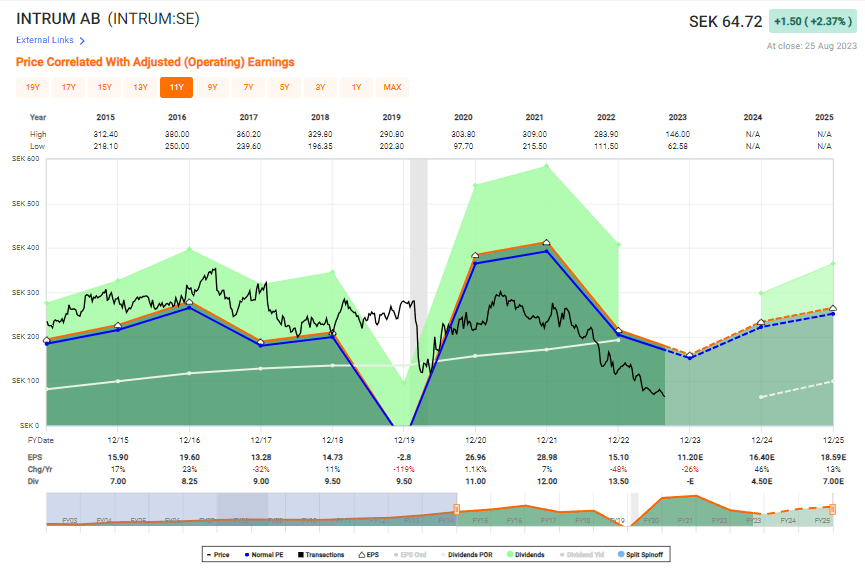

Intrum Upside (F.A.S.T Graphs)

{kind=link}

An upside to a normalized P/E of 10x here, which is still below the company's historical average, implies a 200% upside, or 61% per year. A normalized upside to 15x P/E is over 350%, or 90% annualized.

I don't consider this unrealistic once the double-digit percentage shorting stops for this company, and once earnings improve and the companies gets its issues under control.

I see a zero-percent or equivalent risk of the company encountering enough difficulties to where it needs to look at more serious measures. Business performance is already solid, and rate increases won't impact this company severely as it already hasn't.

Intrum is a high-risk speculative "BUY" on the basis of its dividend cut for 2024E - but you're still getting the November dividend. Even if you go in at this time, that's still over a 10% yield for this year.

And if this does normalize, my 3-4% allocation both on the commercial and private side, will give me 10-15x P/E returns of 200-350%. At that point, Intrum will make up over 10-12% of my current portfolio, and I will trim it.

My conviction that this will happen is high - but the timing is a different issue. I will revisit this play at key intervals, for now, I say that this company is a significant "BUY" if you're risk-tolerant.

Morgan Stanley ( MS ) recently sized up its position above 5% ( Source ). I'm also sizing up.

Thesis

- Intrum is a market-leading debt collection and credit company. In Europe and LATAM, it's one of the more significant ones. The company is currently trading down due to a mix of headwinds, primarily from assets it got as part of an M&A.

- I view these issues as temporary, even if that "temporary" could turn into 1-2 years prior to normalization, given the pressures on the company to de-lever, and do so quickly.

- I rate Intrum a "BUY" here, at any time the native share price is below 140 SEK. My long-term expectation is for the company to go above 200 SEK again.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Despite the cancellation of the dividend, I am unfazed. This company remains a "BUY".

For further details see:

Intrum: Likely No Dividend In 2024, But Superb Upside Potential - 'Buy'