ITJTY - Intrum Might See Opportunities In 2023 But Execution Is Critical

2023-04-03 08:03:17 ET

Summary

- Intrum is a billing partner who deals with consumer debts for things like utilities and phone bills, but also larger ticket items from financial institutions.

- More difficult macroeconomic background should support new opportunities in credit recovery as higher ticket items start picking up.

- The issue is Intrum's cash metrics, which are something we don't like to see excessive use of in business accounting.

- Intrum isn't very expensive when using 2021 results as a fathom, but while volatility creates opportunity in its end markets, we don't see the point of this risk besides the large yield for income.

Intrum ( ITJTY ) is a billing partner to a lot of corporations that issue frequent bills to consumers, things like utilities and cell phone bills. They are contracted to deal with late payments and try make collections, and in some cases they also buy the receivables to claim them on their own behalf, and this business is its own segment. Its joint ventures got seriously written down which has affected their income, but in general the good macro conditions mean less high ticket claims flowing in in their main businesses. However, they are quite exposed to the situation in consumer credit. The risk appears higher than necessary for the current environment, despite the relatively low nomalised PE. Income investors may be interested in the 10% yield proposed for 2023, and the cash economics, even from the J.Vs, seem to be set to do well despite write-downs in a tougher macro environment, but there are usually quite good reasons for yields to be this high.

A Bit on Intrum

Intrum has three segments . The one that creates some confusion in accrual accounting figures is their portfolio investments segment, which is cash intensive since they need to use investing cash flows to buy the receivables from the bad-debt balances of partnered corporations to then claim them on their own behalf. This is the reason the company uses so many cash metrics. We do not like cash metrics, it is opaque, and they spend a lot of time doing reconciliations and comparability fixes which is a little bit of a concern since overuse of non-IFRS figures tends to be a somewhat bad sign.

Cash Flows (Q4 2022 Pres)

The other segments are not capitally intensive, and simply depend on flow of cases from corporations. When billing problems arise, where for example a customer hasn't paid a phone bill, Intrum will step in and try collect the payments for their customers and they'll take a cut on that as a process intermediary. The recognise revenue on the receipt of the cash, and they earn commissions or earn on a subscription basis over the course of a service contract. They also sometimes guarantee receivables, and they earn on the provision of the guarantee, and if the receivable becomes too overdue it is purchased and added to the investment portfolio.

Segment Info Example (2021 Annual Report)

As for the investment portfolio, the assets are composed of the net values of guarantees ultimately fulfilled, or the value of the de-risked bad-debt bought from customers at cost, which are amortised over a period. If Intrum manages to collect the payments even partially, they make income. So the objective is for the collections to exceed the invested capital.

They also have substantial joint venture investments that conduct business similar to the portfolio business, and the value of those typically get revised based on the expected recovery of assets within them. But they also produce cash flows based on their collections and those cash economics have managed to improve this year despite some substantial write-downs.

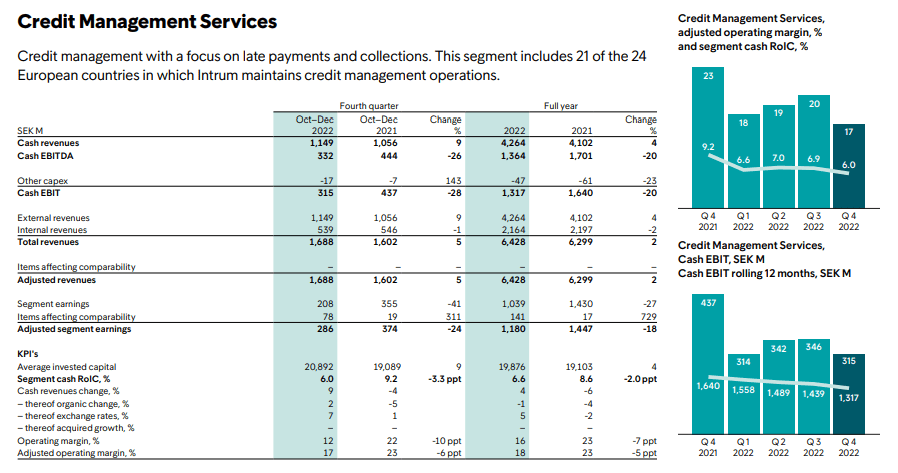

For the Q4, there was a lot of pressure on Cash EBITDA and EBITDA from the credit management segments in some of Intrum's more marginal markets, and this was primarily because cases were ageing and inflows were lower, but the company thinks that a more challenged economic backdrop in 2023 will improve things here, and also create more flow of high-ticket financial services items that have been especially slow this year, where Intrum margins are higher.

{kind=link}

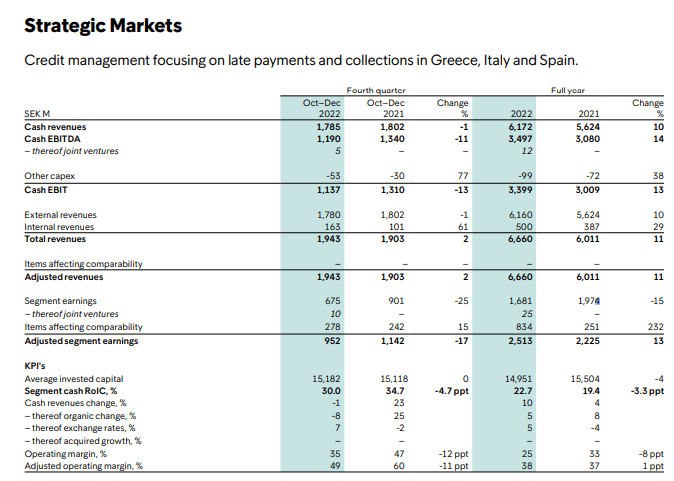

But the business focused on collections in Greece, Italy and Spain (the strategic markets) did a lot better despite some quite important contract losses in Spain with SAREB, Spain's 'bad bank', which did cause some decline in their Q4 results.

{kind=link}

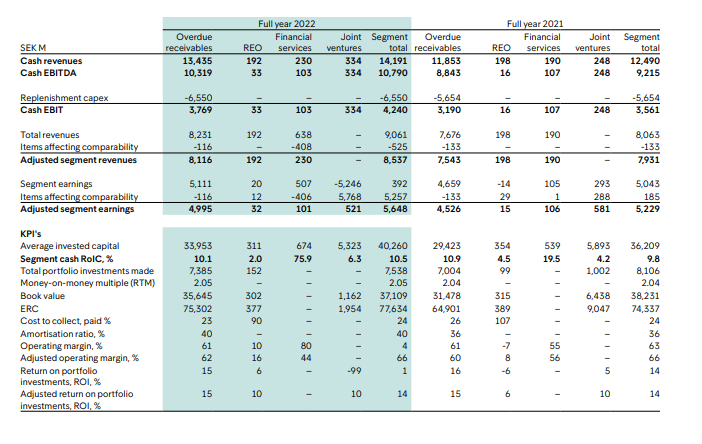

The portfolio business was weaker. While the overdue receivables business did well, the segment earnings got decimated due to some major downward revisions in some of the Italian joint ventures. The overall segment income before adjustments for the Q4 went deeply negative, and it substantially shrunk in the case of the FY results.

{kind=link}

J.V Write-down (Q4 2022 Pres)

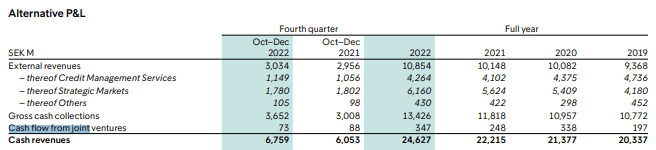

While the evolutions in the J.Vs might be a one off and technically a non-cash effect, because collections will be whatever collections have been in the quarter, it's still not a positive thing that there has been such a write-down on earnings as it signals an impact on future cash flows that can be expected on ageing cases within the J.V - it is also a signal of what can happen to consolidated investment assets due to a revision in collection expectation. However, cash flows are still coming in from joint ventures from within this segment as of now, and they are falling by a relatively small degree which means the cash metrics are much higher than the accounting figures in 2022 for the portfolio segment. Also, the J.V cash flows aren't that big. Cash EBIT went from 1,683 to 1,943 million SEK, where cash EBIT includes deductions of CAPEX associated with upkeep of an invested base of bad debt - but this could taper as collection expectations, in small part from the J.Vs, could go down on a tougher macroeconomic backdrop.

Overall, these cash metrics are alright, but they are quite lagging, since they only consider collections in the quarter and aren't focused on how the invested balances will perform from here on out. The investment portfolio segment is more than half of the adjusted earnings, so it's a concern.

{kind=link}

Comments

The company maintains that it's going to get a tailwind from a tougher macro environment, which should boost case inflows, but of course there are also higher risks of claims not being fulfilled, or at least claims having to get haircuts compared to what you could have expected these last quarters, which would impact the investment portfolio returns but also the commissions expected on case flows from customers. Ultimately, Intrum is a play that depends to an extent on consumer financing and the ability for today's consumers to settle debts. The higher margins are on larger debts, and those become more dicey in a tougher economic environment - indeed customers will likely start revising upwards their bad debt reserves to account for this. Intrum de-risks customers from the riskiest of that debt, so it's in the way of some macro danger too. In a mild but long recession, which is what most economists expect, since a violent credit crisis should be pretty unlikely, Intrum is likely to actually see these tailwinds materialise next quarters without too much punishment from a tighter credit environment. In all, a net positive evolution is not crazy to expect.

Considering adjusted EPS figures from last year, which weren't affected by J.V asset value revisions, Intrum's PE is pretty low, definitely below the 10x mark. With some catalysts for earnings growth and a measure of countercyclicality, there is a certain appeal to the company, especially as the board has proposed a dividend of 12% for 2023 on current prices. But credit risk still exists here, and there is a reason why the market is penalising this stock and keeping it at such a compressed multiple. The price has cratered since 2021, and Intrum is definitely 'in the way' of potential risks to broader markets. We may keep an eye on Intrum, but we don't love the use of cash metrics as they are a lagging indicator of results since they focus on current cash collection volumes, and we are concerned about companies with consumer credit risks in geographies where rates are coming up.

For further details see:

Intrum Might See Opportunities In 2023, But Execution Is Critical