REG - InvenTrust Properties: Sleep Well At Night With Sunbelt Supermarkets

Summary

- When I first wrote about IVT, the stock price was near $30 and the dividend yield below 3%.

- Today, the Sunbelt grocery-anchored retail REIT has become much more attractively valued with a dividend yield around 3.5%.

- This is a sleep-well-at-night company, but investors should still take care not to overpay for it.

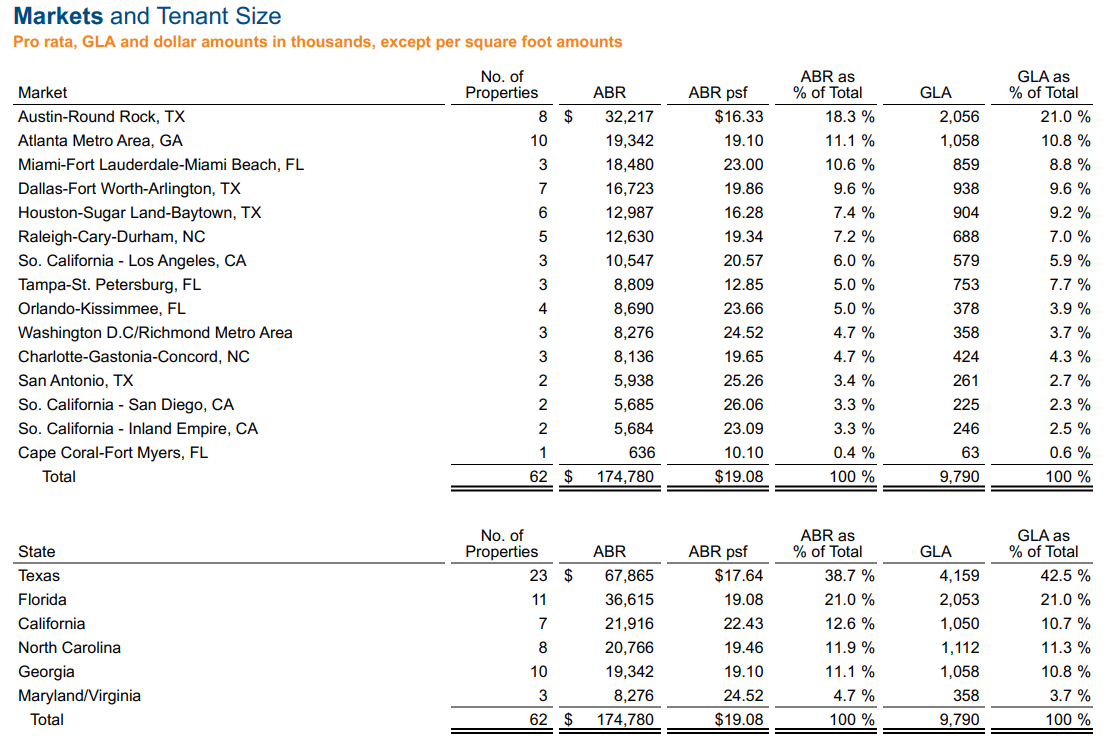

InvenTrust Properties ( IVT ) is an exclusively Sunbelt, predominantly grocery-anchored shopping center real estate investment trust ("REIT") that owns 62 properties primarily in Texas, Florida, California, North Carolina, and Georgia.

Because of the resurgence of brick & mortar retail as well as the defensiveness of grocery-anchored centers and the growing populations of Sunbelt states, I believe that IVT's portfolio enjoys some of the most defensive positioning in retail REITdom, while the REIT's balance sheet is likewise among the strongest in its peer group.

These factors make IVT one of the most, if not the most, "sleep well at night" shopping center REITs, in my opinion.

IVT recently turned in solid Q4 and full-year 2022 results , although they offer a reminder that the retail REIT is not a high-growth company. They are a moderate and steady growth company, which I would expect to turn in an average annual FFO per share growth rate in the mid-single digits.

The recently declared 4.9% dividend increase to $0.86 annually is an illustration of this expected long-term growth rate.

Putting IVT's sleep-well-at-night character together with its moderate-and-steady growth rate helps to determine a good price to pay for the REIT. Given 2023 core FFO guidance of $1.59 to $1.64 per share, IVT currently trades at a price-to-FFO of 15.1x.

Personally, I would like to buy IVT at an FFO multiple of 15x or less. As such, my "buy under" price is $24.25, which works out to a 2023 FFO multiple of 15x.

End of Year Update

I've written about IVT multiple times in the past:

- InvenTrust Properties: Unattractive For Dividend Investors (NYSE: IVT ) | Seeking Alpha

- InvenTrust Properties: Defensive, Recession-Resistant Dividend Growth Stock (NYSE: IVT ) | Seeking Alpha

- InvenTrust ( IVT ): Sunbelt Grocery-Anchored Retail With Steady Dividend Growth | Seeking Alpha

When I first wrote about IVT in March 2022, the stock price traded for around $30, putting the dividend yield under 3%. And yet, I knew this company wasn't going to be able to churn out double-digit dividend growth on a sustained basis, thus why it was unattractive for dividend investors at the time.

Today, however, the situation is different. At around $24.67 per share, IVT offers a dividend yield of around 3.5% (based on the upcoming dividend), and the valuation seems much more reasonable.

Moreover, since then, IVT has taken some steps to become a more simplified and focused REIT.

During 2022, IVT sold its three Colorado properties and reinvested the proceeds to become a truly pure-play Sunbelt shopping center REIT.

Also, in January 2023, IVT purchased the four remaining shopping centers in its joint venture portfolio with PGGM, which means that 100% of the REIT's revenues are now from wholly owned properties.

Since the JV properties are located in Texas, IVT's concentration in the Lone Star State will likely jump from the 38.7% of annual revenue it was at the end of 2022 to somewhere north of 40%.

{kind=link}

After disposing of its three Colorado properties last year, IVT is now fully concentrated in just 7 states, with Texas and Florida together accounting for over 60% (after the JV acquisition).

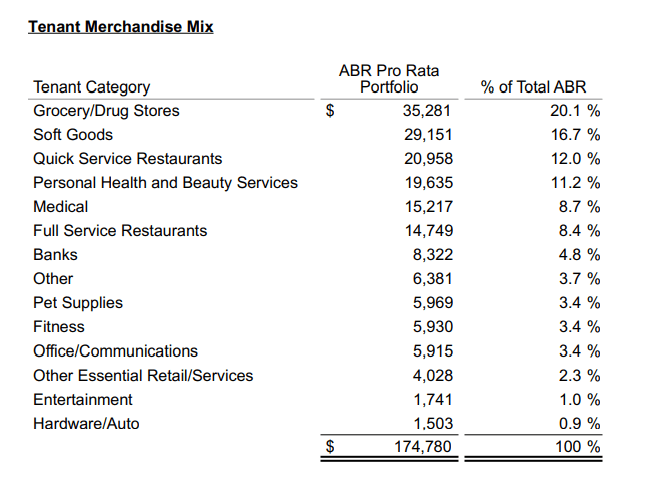

Though not every center is grocery-anchored, the vast majority are (or "shadow-anchored" by a non-owned grocer located in the same parking lot), which makes it no surprise that 20% of rent derives from grocery or drug stores.

{kind=link}

Bed Bath & Beyond ( BBBY ) makes up only 1.1% of total rent, and Regal Cinemas ( CNNWQ ) accounts for a mere 0.7% of rent. These are perhaps IVT's two most troubled tenants, but the threat of losing these tenants should not scare investors.

IVT's occupancy of 96.1% at the end of 2022 was an all-time high for the company, indicating strong demand for retail space from retailers - more space than is available.

Considering high occupancy rates and high demand for space from retailers, IVT has the opportunity this year to trade out some of its weaker tenants, like BB&B and Party City ( PRTYQ ), for higher quality tenants at 10-20% higher rent rates. That's a win-win.

Outlook for 2023

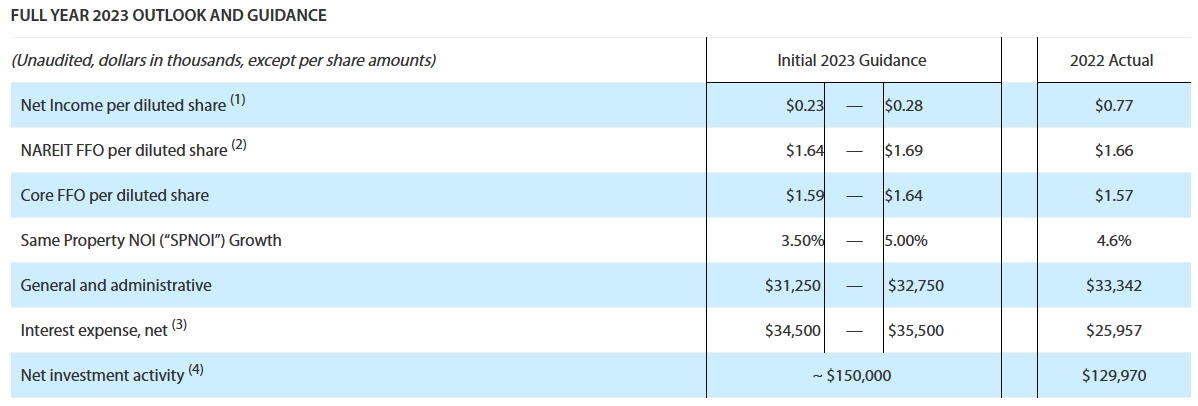

In 2022, core FFO per share of $1.57 increased 12% year-over-year from 2021's $1.40. About 32% of that growth came from same-property net operating income ("NOI") growth, while 14% came from acquisitions, 25% from G&A savings, and 29% from share buybacks executed in late 2021.

The midpoint of 2023 guidance calls for 2.9% core FFO per share growth this year to $1.615.

{kind=link}

Given the $0.86 annual dividend, 2023 should come with a payout ratio of 53.3%, compared to 2022's payout ratio of 52.2% and 2021's payout ratio of 55.9%.

As for same-property NOI growth, IVT achieved 0.4% in Q4 and 4.6% for the full year. "Achieved" might not be the right word for a mere 0.4% same-property NOI growth, but if you exclude "out of period rent collection" (collection of deferred rent), IVT's Q4 SPNOI growth would be a more respectable 2.1%, while full-year SPNOI growth would be 6.0%.

This softening SPNOI growth is mainly a result of moderating rent growth. Blended (new and renewal) leasing spreads were 6.1% in Q4 and 8.4% for the full year.

Softening in SPNOI growth is expected to continue into 2023, hence guidance of SPNOI growth of 3.5% to 5% in 2023.

And while G&A expenses (the "management fee" for internally managed companies) is set to decline a bit, a spike in interest expenses will more than offset this.

Balance Sheet & Available Cash

IVT is one of the lowest leveraged shopping center REITs with a net debt to EBITDA multiple of 4.8x. Only blue-chip grocery-anchored retail REIT Regency Centers ( REG ) has a lower net leverage multiple.

IVT enjoys a fairly low weighted average interest rate of around 4.1% at an average maturity of about 5 years.

At the end of 2022, IVT had total liquidity of $514 million. Excluding the $350 million available on the credit facility, which is not a form of long-term financing, the REIT had funds available for long-term capital deployment of $164 million.

However, in mid-January, IVT purchased the remaining JV portfolio using about $129.8 million of that available cash, which brought the REIT's cash position down to about $34 million. Afterward, though, the JV began the liquidation process and is expected to distribute $71.4 million back to IVT, which should raise IVT's cash position back to $105.6 million.

Beyond the JV acquisition, IVT expects to perform another $50 million of acquisitions for the remainder of 2023.

As such, most of the external growth action has already taken place for IVT for 2023. Most of the rest of its growth is expected to come from marking to market the rents on expiring leases.

Bottom Line

IVT oozes conservatism and defensiveness in at least three ways:

- Location : Geographic concentration in some of the fastest growing states like Texas, Florida, North Carolina, and Georgia.

- Grocery-Anchored : Most rent derives directly from necessity-based tenants, and the vast majority derives from tenants located in centers anchored by necessity-based retailers.

- Balance Sheet : Low debt, plenty of cash, and ample retained cash flow (payout ratio barely above 50%) give IVT one of the strongest balance sheets in the retail REIT space.

Admittedly, the management team led by DJ Busch is relatively young and untested by a recession, but as far as I can tell, the portfolio and balance sheet they have constructed are top-notch.

As a resident of Austin, TX, which is IVT's largest market, I can attest from firsthand experience that IVT's property selection criteria is strong.

And yet, despite strong locations, defensive properties, and a fortress balance sheet, IVT stock has underperformed its larger and more geographically diversified peer REG over the last year:

At this point, REG is trading at a full point higher FFO multiple of 16.1x, compared to IVT's 15.1x, despite the latter being (in my opinion) more attractive than the former.

I am a buyer of IVT at $24.25 or under, and if the stock price dips significantly below that price, I'll be happy to build it into a large position in my portfolio.

For further details see:

InvenTrust Properties: Sleep Well At Night With Sunbelt Supermarkets