BRX - InvenTrust Properties: Steady Compounder With Very Low Risk

2023-05-02 08:30:00 ET

Summary

- IVT's portfolio of well-located, grocery-anchored shopping centers overwhelmingly in the Sunbelt looks highly defensive in the current chaotic economic environment.

- About 41% of the REIT's rent derives from the fast-growing state of Texas.

- Organic growth was among the highest in its peer group last year and is expected to be the highest this year.

- The dividend may yield only 3.8%, but it is well-protected with a payout ratio of 53% and a solid dividend growth record.

InvenTrust Properties ( IVT ) is a small, grocery-anchored shopping center real estate investment trust ("REIT") concentrated almost entirely in high-quality, highly trafficked centers in Sunbelt states. The centers themselves are also generally on the smaller side. Slightly over 2/3rds of IVT's properties are neighborhood or community centers with trade areas of 5 or less miles, while the remaining ~1/3rd are power centers with trade areas of 5-10 miles.

I've written multiple articles on IVT over the past year or so, highlighting the REIT's strengths:

- InvenTrust Properties: Defensive, Recession-Resistant Dividend Growth Stock

- InvenTrust (IVT): Sunbelt Grocery-Anchored Retail With Steady Dividend Growth

- InvenTrust Properties Stock: Sleep Well At Night With Sunbelt Supermarkets

I also highlighted IVT as my top pick in retail in " Blue-Chip Real Estate Is A Bargain - Top Picks Across 5 Sectors " along with four other top-tier REITs in other sectors.

Indeed, IVT is what I would consider a "high-quality" REIT, with a strong portfolio concentrated in fast-growing markets, ample liquidity, low debt, 98% of total debt effectively fixed-rate, and only 2% of debt maturing through the end of 2024.

In what follows, I'll discuss why I find IVT such an appealing investment in the retail real estate space and touch on some of the results from the recently released Q1 2023 earnings report.

What Makes InvenTrust Unique

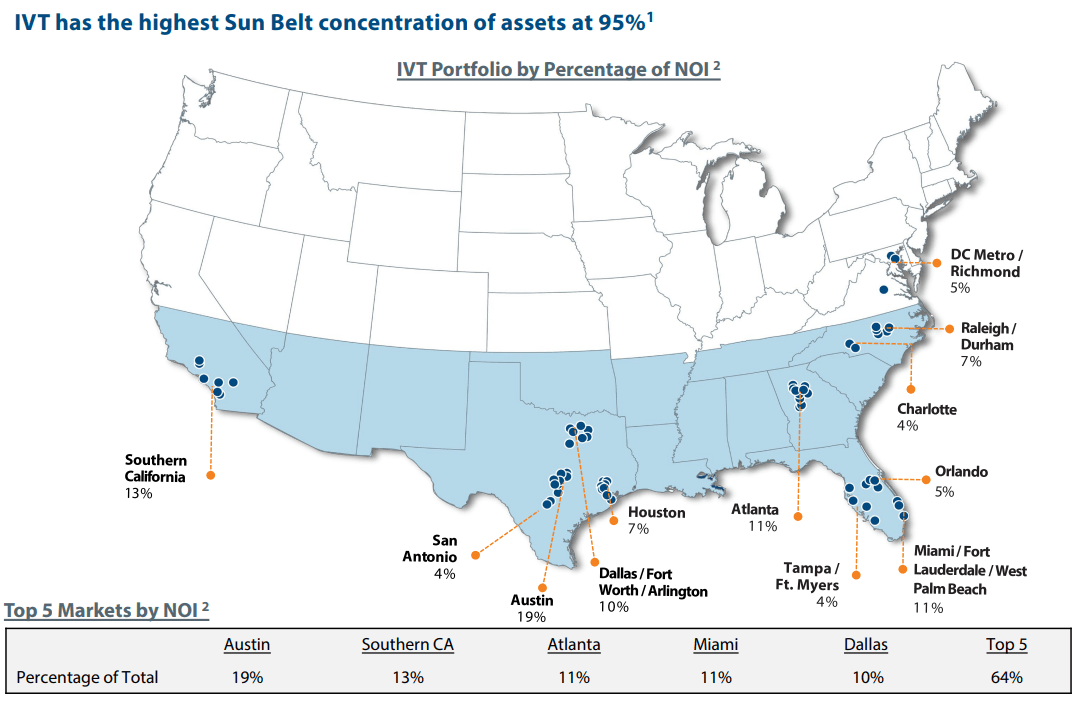

IVT's 62-property portfolio is overwhelmingly weighted to the Sunbelt region at 95% of NOI. The remaining 5% of properties are located in the greater Washington DC area and Richmond, Virginia.

{kind=link}

One downside of having a small portfolio of only 62 properties is the lack of efficiencies brought on by scale. For example, general & administrative expenses equal about 12% of total revenue for IVT, while they get as low as the mid-single-digits for some larger retail REITs.

Management does wish to continue growing the portfolio over time, though. So far this year, IVT has acquired about $100 million in property, entirely from the purchase of its JV partner's interest in several Texas shopping centers in its joint venture. Further acquisitions are difficult because the prices of high-quality, grocery-anchored retail centers in the Sunbelt remain high, but management has stated that they will be disciplined and diligent in their search for new properties.

Right now, IVT's top tenants list is dominated by many of the best retailers in the nation, with 7 of the top 15 being grocers.

IVT February Presentation

Notice that Bed Bath & Beyond ( BBBY ) is also on that list. The struggling retailer recently filed for Chapter 11 bankruptcy, which will include a liquidation of its assets and eventually a closure of its retail stores.

Is this a bad thing for IVT? No! Management have expressed excitement to get these store locations back, as the former marquee retailer of BBBY occupied many top-tier locations. Other retailers have expressed interest in these stores, and IVT has stated that they should be able to re-lease them at 15-20% higher rent rates.

To quote Chief Operating Officer Christy David from the Q1 2023 conference call :

We have already had constructive conversations with a variety of tenants for every one of our five Bed Bath locations. We continue to believe our market-dominant essential retail centers are exactly where retailers want to be, and they are waiting anxiously for this space to become available.

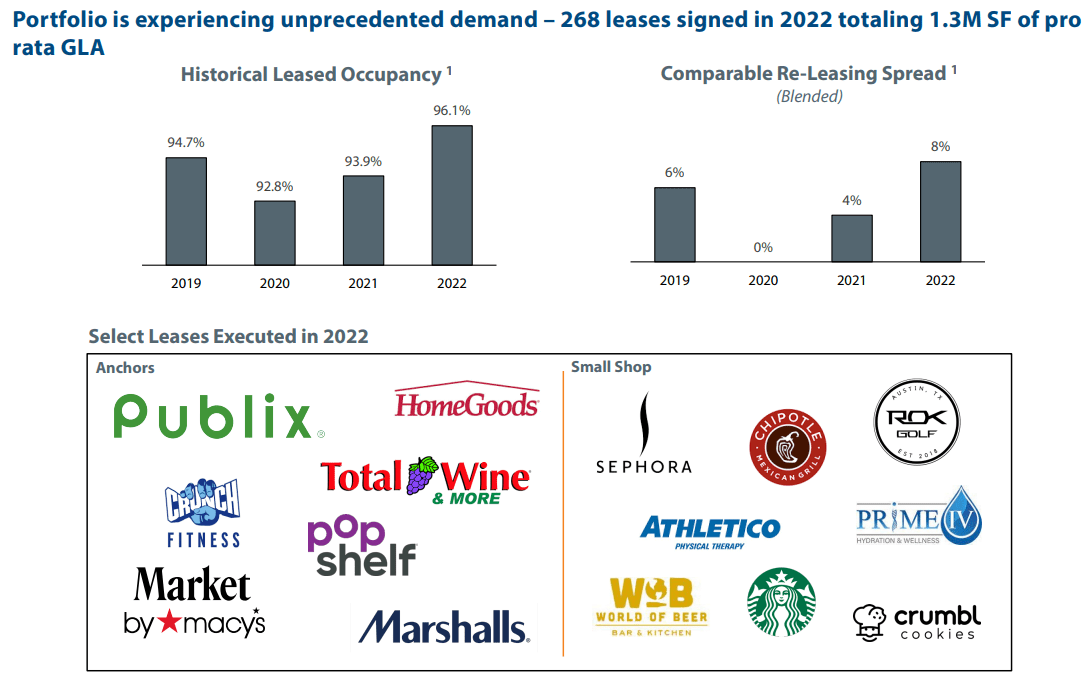

In terms of interest in its larger store spaces, IVT has done a decent amount of leasing lately with names such as HomeGoods, Publix, Total Wine, and Marshalls, among others.

{kind=link}

As of the end of March 2023, leased occupancy remained exactly the same at 96.1% from the end of 2022, and leasing spreads on new and renewal leases rose 7.0%.

During Q1, IVT same-property NOI growth came in at 3.2% (excluding out-of-period rent collection), which is below the full-year guidance for SPNOI growth between 3.5% and 5%. However, that guidance was maintained, so management is clearly expecting SPNOI growth to pick up over the course of the year.

Speaking of SPNOI growth, it's useful to note that IVT's guidance for 2023 is the highest in its retail REIT peer group:

| RETAIL REIT |

| 2022 Same-Property NOI Growth |

| 2023 Guidance SPNOI Growth |

| InvenTrust |

| 4.6% |

| 3.5-5% |

| Regency Cntrs ( REG ) |

| 2.9% |

| 0-1% |

| Kimco Realty ( KIM ) |

| 4.4% |

| 1-2% |

| Brixmor ( BRX ) |

| 6.6% |

| 1.5-3.5% |

| RPT Realty ( RPT ) |

| 4.3% |

| 1.5-3.25% |

| Phillips Edison ( PECO ) |

| 4.5% |

| 3-4% |

| Retail Opp. Inv. ( ROIC ) |

| 4.6% |

| 2-5% |

| Kite Realty ( KRG ) |

| 5.1% |

| 2-3% |

| SITE Centers ( SITC ) |

| 0.8% |

| (1%) to 2.5% |

And 2022's actual SPNOI growth of 4.6% was among the highest in its peer group.

Between contractual rent escalations, strong leasing spreads, and low move-outs, IVT's organic growth should continue to be at or near the top of its peer group going forward.

At the very end of Q2 2022 (June 30th), IVT sold its two Denver, Colorado properties for $55.5 million, recording a very nice $36.9 million gain. They sold these properties in a strong but non-core market in order to concentrate even more on their core Sunbelt markets. But these dispositions did cause a drop in core FFO per share.

| Core FFO Per Share |

| Cash |

| Net Debt To EBITDA |

| Q1 2022 |

| $0.43 |

| $25.7m |

| 5.7x |

| Q2 2022 |

| $0.42 |

| $95.9m |

| 5.1x |

| Q3 2022 |

| $0.37 |

| $216.5m |

| 5.0x |

| Q4 2022 |

| $0.34 |

| $137.8m |

| 4.8x |

| Q1 2023 |

| $0.40 |

| $86.0m |

| 5.5x |

IVT did acquire one property in North Carolina in Q4 2022 for $22.5 million, but most of the proceeds from the Denver property sales weren't redeployed until IVT acquired the four remaining shopping centers in its JV portfolio on January 18, 2023. As part of this deal, IVT assumed $92.5 million in existing JV debt, which is what caused net debt to EBITDA to spike up from 4.8x in Q4 2022 to 5.5x at the end of March.

Keep in mind, though, that while IVT only had 2.5 months of rent from these properties as of the end of Q1, it had assumed their full remaining debt, and the net debt to EBITDA metric uses trailing twelve month EBITDA. As such, run-rate net debt to EBITDA (assuming a full 12 months of EBITDA) will be much lower than 5.5x.

While IVT's core FFO per share is down YoY, it is up 17.6% quarter-over-quarter and 8.1% over the three months right after the disposition of the two Denver properties. And since Q1 2023 was not a full quarter of rent from the JV-acquired properties, we should see core FFO per share tick up a little further in Q2 from a full three months' rent contribution.

If management finds ~$50 million more acquisition opportunities over the remainder of this year, as they hope, then core FFO per share should continue to tick up further over time.

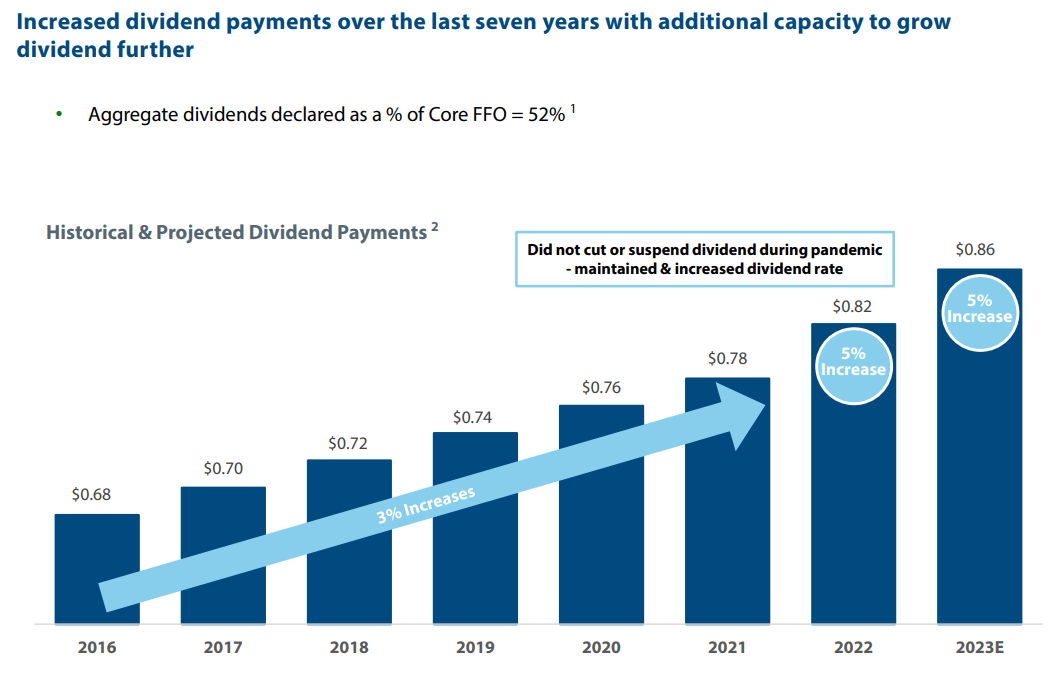

This growth in core FFO per share should, in turn, result in continued annual dividend hikes, following the company's pattern going back to at least 2016.

{kind=link}

Notice that in 2020, when the vast majority of retail REITs cut their dividends, IVT gave their shareholders a 2.7% raise. If this isn't a testament to the defensiveness of the REIT's necessity-based retail portfolio, I don't know what is.

Bottom Line

Today, IVT trades at a dividend yield of 3.8%, and that dividend is extremely well covered by a core FFO payout ratio of 53%.

Meanwhile, the only debt maturing in 2023 comes with two 12-month extension options, which management may opt to use in order to put off refinancing until November 2024. After that, the next debt maturities are two mortgages due in June 2024, together representing less than 2% of total debt. After that, nothing else matures until December 2025.

As such, IVT bears virtually zero refinancing risk, very little asset risk, and very little execution risk, because the previously acquired 4 properties were already part of its JV portfolio and there should be only a few more acquisitions this year.

IVT may be boring, but its steadily compounding returns should continue indefinitely, and I think there's value in this level of safety.

For further details see:

InvenTrust Properties: Steady Compounder With Very Low Risk