IVR - Invesco Mortgage Capital Simply Doesn't Work

2023-07-10 16:04:40 ET

Summary

- Invesco Mortgage Capital, an mREIT with a 14% yield, has seen its stock drop 94% since its inception in 2009, making it a yield trap for investors.

- Government-backed mortgages aren't immune to drops in value and being overleveraged in them doesn't help either.

- Even if you ignore the poor stock performance, dividends have also been shrinking at a rapid rate, now paying a fraction of what it was paying a few years ago.

Invesco Mortgage Capital ( IVR ) is an mREIT with a juicy yield of 14%. The company invests in, finances or manages mortgage-backed securities as well as other assets related to mortgage. It specifically invests in different types of assets such as government-backed residential mortgage (also known as "Agency MBS"), commercial mortgage-backed securities (which don't have government backing), non-agency residential mortgages, and other financial arrangements and contracts.

The fund's strategy simply isn't working and hasn't worked for a long time, except for a brief period of time between 2016 and 2020. As you can see below, the stock is down -94% since its inception in 2009 and its total return (after reinvesting all dividends) is still down -61% even though we've witnessed one of the strongest bull markets in history during the same period. This investment was and still is a yield trap which should be avoided by most investors.

When people think about agency-backed mortgages, they think they can't lose money because government backs those mortgages, but this is not necessarily true. Government-backed mortgages can still drop in value and depreciate in price. Even risk-free government bonds and treasuries can lose a lot of value as many investors found out last year, so why shouldn't government-backed mortgages also lose value? When government backs a mortgage, it doesn't guarantee that the value of the mortgage will never drop. It simply guarantees that if the buyer of the house is unable to pay their debt, government will buy cover the debt, but this is no insurance against a drop in value.

You could technically hold a government bond or treasury until maturity and get 100% of your money back at the end, so technically, you aren't losing money if you hold it until maturity, even if it dropped in value 20-30% during this time. The same is also true for government-backed mortgages, but there is a caveat for funds like IVR. Most mortgages are 30 years long, so the company has to hold those bonds for a very long time to take advantage of this. More importantly, companies like IVR are highly leveraged. If you buy a bond at inception and it drops -20% in value, you can afford to hold it until maturity and recover your losses, but if you are leveraged by 300%, now that -20% loss becomes a -60%, and you have less room to wait for maturity of the loan.

This is one of the problems with not only IVR but many mortgage REITs. They are highly leveraged. How else can they pay 15-20% dividend yields when most mortgages are locked in at 4-5% rates? When a fund or company is highly leveraged in a bond or debt instrument, even a small drop in value can hurt that fund, so at this point, the fact that those mortgages are backed by the government offers little help to IVR.

That is one of the reasons I generally avoid mortgage REITs with the exception of a few high quality ones such as Arbor ( ABR ). In general, mortgage REITs should make a very small percentage of your portfolio if any. If I was retired I'd completely avoid companies like this one.

One argument I always hear from high yield investors who often find themselves locked in one of these yield traps is that they don't care for share price appreciation because they plan on holding their stock forever and never intend on selling, so they won't even pay attention to the stock price. That kind of thinking could work for high quality dividend stocks that pay a stable dividend and raise their dividend over time such as Coca-Cola ( KO ), McDonald's ( MCD ), P&G ( PG ), and Johnson & Johnson ( JNJ ) but not for companies like IVR where the dividend keeps shrinking every year because the company's assets are shrinking. At the time of its inception, IVR was paying $9 per share annually in dividends (split adjusted) and now it's only paying 40 cents per year. What a dramatic drop! Even a few years ago it was paying north of $3 per share and its dividends never recovered the COVID drop.

If you were a retiree and bought this stock anytime in the last 10 or even 5 years, your income already shrank to a fraction of what it was when you first bought the stock. If your portfolio was overweight this stock or had too many stocks like this, you might even have to go back to working after announcing retirement, which wouldn't be too great for most people.

I understand that these days, investors are hungry for yields, especially with high inflation and higher cost of living overall. This type of environment forces many retirees or income-seeking investors to look for dangerous places to generate income. A recent article by Wall Street Journal (might be behind a paywall) revealed that older investors are taking far more risk in their portfolios than they historically did. Below is a direct quote from the article:

Nearly half of Vanguard 401(k) investors actively managing their money and over age 55 held more than 70% of their portfolios in stocks. In 2011, 38% did so. At Fidelity Investments, nearly four in 10 investors ages 65 to 69 hold about two-thirds or more of their portfolios in stocks.

And it isn't just baby boomers. In taxable brokerage accounts at Vanguard, one-fifth of investors 85 or older have nearly all their money in stocks, up from 16% in 2012. The same is true of almost a quarter of those ages 75 to 84.

Investors are taking on more risk now because they are hungry for returns. This wouldn't have surprised me a couple of years ago when stocks had no alternative because bonds were yielding nearly 0%, but now, we have short-term treasuries yielding as much as 5.25% and people are still heavily invested in stocks even during their retirement years. I have nothing against investing in stocks at later ages, but if an investor wants to put their money in stocks during retirement, they should go for high-quality stocks that have a long track record of paying and raising dividends even though those stocks might not offer 15-20% yields. You'd much rather put your money into stocks and bonds that yield much less but pay a stable dividend and even raise it over time.

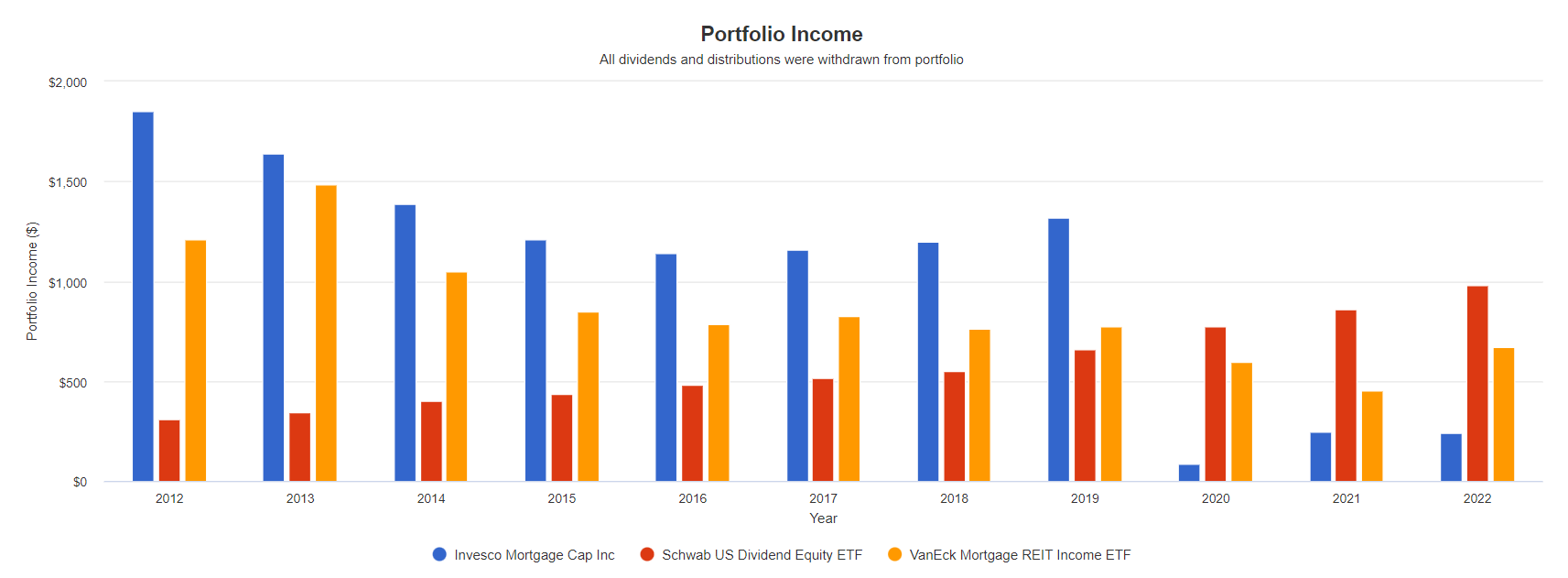

Below is an example of how your annual income would grow over the last decade if you had invested $10k in 3 different places: IVR, SCHD (a fund containing high-quality dividend growth stocks), and MORT (an ETF containing a package of mortgage funds). Notice how SCHD initially has the lowest yield out of the three but emerges with the highest yield to original cost at the end of the decade. This is because low-quality stocks keep cutting their dividends while good-quality stocks keep raising their dividends over time.

Dividend growth of 3 different approaches (Portfolio Visualizer)

{kind=link}

This is why I wouldn't recommend stocks like IVR to anyone including dividend investors or growth investors because the stock offers neither in a reliable manner. This is a classic yield trap.

IVR's financial results haven't been very impressive recently. After announcing a pretty sizeable loss in 2020, it posted improvements in 2022, but it's back to announcing losses again both in terms of EPS (earnings per share) and FFO (funds from operations). Since the company is highly leveraged, when it posts losses, those losses can really multiply quickly and one bad year like 2020 can erase multiple years' worth of gains. The company will have to post a sizeable profit very soon if it doesn't want to cut its dividends once again.

As much as valuations go, it's difficult to assign a P/E or P/FFO value for IVR because the company doesn't post profits consistently. The next thing we can look at is P/B which is the price to book value. Currently, IVR sells for 0.86 times its book value, which indicates a discount of 14%. It's pretty much in line with where the stock traded in the last 10 years if you don't count a few exceptions like the bottom of 2020 or the top of 2021 where it first sold for 0.3 times book value and then climbed to 1.25 times the book value. For most of the last decade, the stock traded somewhere between 0.8 times and 1.0 times its book value. Currently, it's closer to the lower edge of this range, but it's for a good reason due to poor performance and lack of solid profits.

In conclusion, I wouldn't recommend buying IVR to anyone, including income-oriented investors and growth-oriented investors. The stock has a long track record of underperforming, its dividend history is full of dividend cuts, share price has been dropping steadily since its inception and its highly leveraged nature makes it a very risky play. If this company can perform this badly during a period where home prices rose so much and mortgage write-off levels have been historically low, how will it perform if we get a recession and see a housing crisis? Investors should instead put their money into stocks and funds with better track record, even if they have a lower dividend yield.

For further details see:

Invesco Mortgage Capital Simply Doesn't Work