IVR - Invesco Mortgage Capital: The 14.8% Yield Could Be A Trap

2023-04-08 00:53:43 ET

Summary

- Invesco Mortgage recently cut its quarterly dividend payout by 38.5%.

- The commons currently yield 14.8% but the reduced payout is still at risk with book value still declining.

- Shareholders could swap out the commons for the fixed to floating rate preferreds which currently sport a 9.8% yield on cost and are trading at a 21% discount to par.

Invesco Mortgage Capital ( IVR ) last declared a quarterly cash dividend of $0.40 per share , a 38.5% decrease from its prior payout and a 14.86% forward dividend yield. This payout has been in freefall in the years since the pandemic and is down by a 48.47% compound annual growth rate over the last 3 years. The payouts are down by 27.78% over the last 12 months and stand to fall further as a still-rising Fed funds rate works to impact the portfolio of the residential mortgage-backed securities REIT.

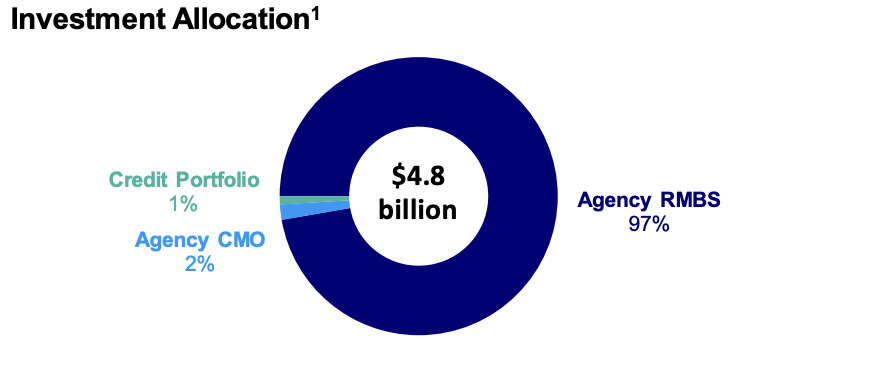

Invesco's investment portfolio as of the end of the fiscal 2022 fourth quarter was worth $4.8 billion and constituted mainly of agency residential mortgage-backed securities. Agency collateralized mortgage obligation formed the second largest component at 2%.

{kind=link}

Book Value And The Payout Ratio

The market cap follows book value and this has been on a sustained decline since the pandemic. Book value as of the end of Invesco's fiscal 202 fourth quarter stood at $505.4 million , up from $462.5 million in the prior third quarter but down 48% from $974 million in the year-ago comp. Hence, whilst the current market cap is currently below book value, BV has proved to be unstable and stands to remain volatile in response to the rise in the Fed funds rates. Indeed, post-period end Invesco updated the market that its book value per share as of March 17 was $11.96 to $12.44, down from $12.79 per share as of the end of the fourth quarter.

Earnings available for distribution ("EAD") came in at $1.46, up by $0.07 sequentially from EAD of $1.39 in the third quarter. Why did the REIT cut its dividend with the previous $0.65 per share payout forming 44.5% of EAD? Book value. Invesco's management stated during their fourth-quarter earnings call that they aim to strike a balance between keeping their yield competitive against their peers and supporting book value. Hence, the prior forward yield before the cut would have been 24%. This would have been a materially outsized yield versus other mREITs. Critically, shareholders need a stable source of income and a dividend payout policy that's fundamentally driven by peer comps and market prices is not attractive.

Exploring The Series B Preferreds

Invesco's 7.75% Fixed-to-Floating Series B Cumulative Preferred Stock ( IVR.PB ) is the better option here. They pay out a $1.94 annual coupon for a 9.8% yield on cost. Whilst this yield is 500 basis points lower than the dividend paid to common shareholders, they've been spared from the discombobulation of the last three years. They're currently trading at $19.74, a 21% discount to their $25 par value.

{kind=link}

This creates an inherent margin of safety with preferreds prices normally anchored around the $25 redemption price. The current gap has opened up on the back of stock market angst around the rising interest rates aggregated with the March mini-banking panic. Whilst these are coming up for redemption in December next year, there is no obligation for Invesco to fully redeem them.

Hence, they could trade perpetually to form a source of forever income against a cumulative clause that materially reduces the likelihood of Invesco interrupting their quarterly distributions. It's important to note that the distribution was maintained during the pandemic with common shareholders bearing the brunt of the disruption.

{kind=link}

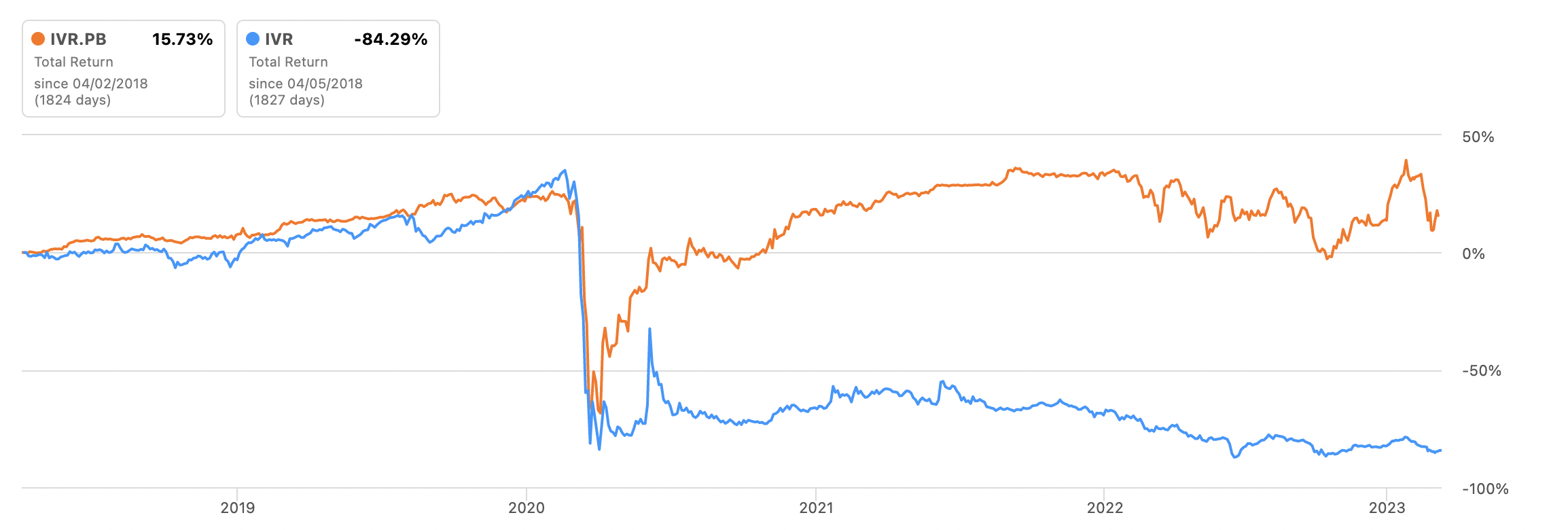

The performance dichotomy between both securities is stark. Essentially, a book value in freefall has seen the commons shed 84% of their value over the last five years on a total return basis versus a gain of 15.7% for the preferreds. Over the last three years and the commons are down 16.8% versus a gain of 158% for the preferreds. Crucially, the preferreds currently sport a 22.78% yield to call. Not only is this in excess of the yield on the commons, but it's also a potential rate of return that's in excess of long-run inflation and the average returns of the S&P 500.

They'll also float at redemption at a rate equal to three-month LIBOR plus 5.18% per year. Whilst LIBOR is set to change to SOFR by the end of June, it currently stands at 5.22%. As the rate when the Series B float will be driven by the inflation and Fed funds rate dynamic at that time, it's likely that LIBOR-SOFR at float will be materially lower with inflation forecasted to fall close to the Fed's 2% target rate in the second half of this 2023 and for the Fed funds rate to peak by the end of spring this year.

I think the commons should be avoided with a book value in decline and with the near-term outlook for the dividend remaining poor even after the cut. There are fundamentally better mREITs out there. The preferreds offer more value here with a move back up to par more likely once the Fed pivots and inflation comes back down to its target 2% rate. This will take some time but the near-double-digit 9.8% yield provides an incentive to wait.

For further details see:

Invesco Mortgage Capital: The 14.8% Yield Could Be A Trap