AGNC - Invesco Mortgage Capital To Benefit From Fed Shift

2024-01-15 01:40:35 ET

Summary

- Invesco Mortgage Capital has faced challenges in the mortgage-backed securities market, but with the Fed expected to cut rates, the firm's prospects are improving.

- IVR primarily invests in agency MBS with low credit risk but faces risks from interest rates, prepayments, and spreads.

- The company has adjusted its portfolio and leverage and is expected to benefit from a shift to falling rates and improved spreads in the mortgage REIT space.

Invesco Mortgage Capital ( IVR ) has been battling a tough mortgage-backed securities ("MBS") market, but with the Fed set to reverse course and cut rates this year, the firm looks set for better days ahead.

Company Profile

IVR is a mortgage REIT that primarily derives earnings from interest rate spreads between MBS it purchases and its borrowing costs. It then uses leverage to boost its returns.

The firm invests mainly in the agency MBS which is backed by government agency Ginnie Mae or government-sponsored agencies Fannie Mae and Freddie Mac. These investments carry nearly zero credit risk. It also invests a small percentage of its portfolio in collateralized mortgage obligations ("CMO"), non-agency residential mortgage-backed securities ("RMBS"), and commercial mortgage-backed securities ("CMBS").

As a REIT, it doesn't pay taxes at the corporate level and must distribute 90% of its earnings to shareholders in the form of dividends.

IVR employs an active hedging strategy.

At the end of Q3, AGNC's investment portfolio was valued at $5.4 billion, with $98% that in Agency MBS.

Opportunities and Risks

Like other mortgage REITs, IVR is in the spread business, where it obtains short-term funding through instruments like repos that it uses to then go out and buy mortgage-backed securities. It then uses leverage to bolster its earnings power. It was leveraged 6.4x at the end of Q3, which was an increase from 5.9x a year ago. However, it said that in October it reduced its leverage to 4.3x. It has been taking its leverage up since then October, however.

The firm faces very little credit risk given that 98% of its investments are in agency MBS. The primary risks the company faces are interest rate, prepayment, and spread risk.

Interest rates and spread risks hampered IVR through much of 2023. This was seen in the decline in its book value, which went from $12.79 at the end of Q4 2022 to $9.93 in Q3, an over -22% decline.

Mortgage rates rose through much of 2023 as the Fed raised interest rates to help stem the high rate of inflation. This impacts the value of the MBS that IVR holds, as new MBS with higher interest coupons makes the value of older MBS with lower coupons less valuable. This is the same risk that people who invest in Treasury Bond mutual funds and ETFs face, as older bond prices move to more closely match the yield of currently issued similar debt securities.

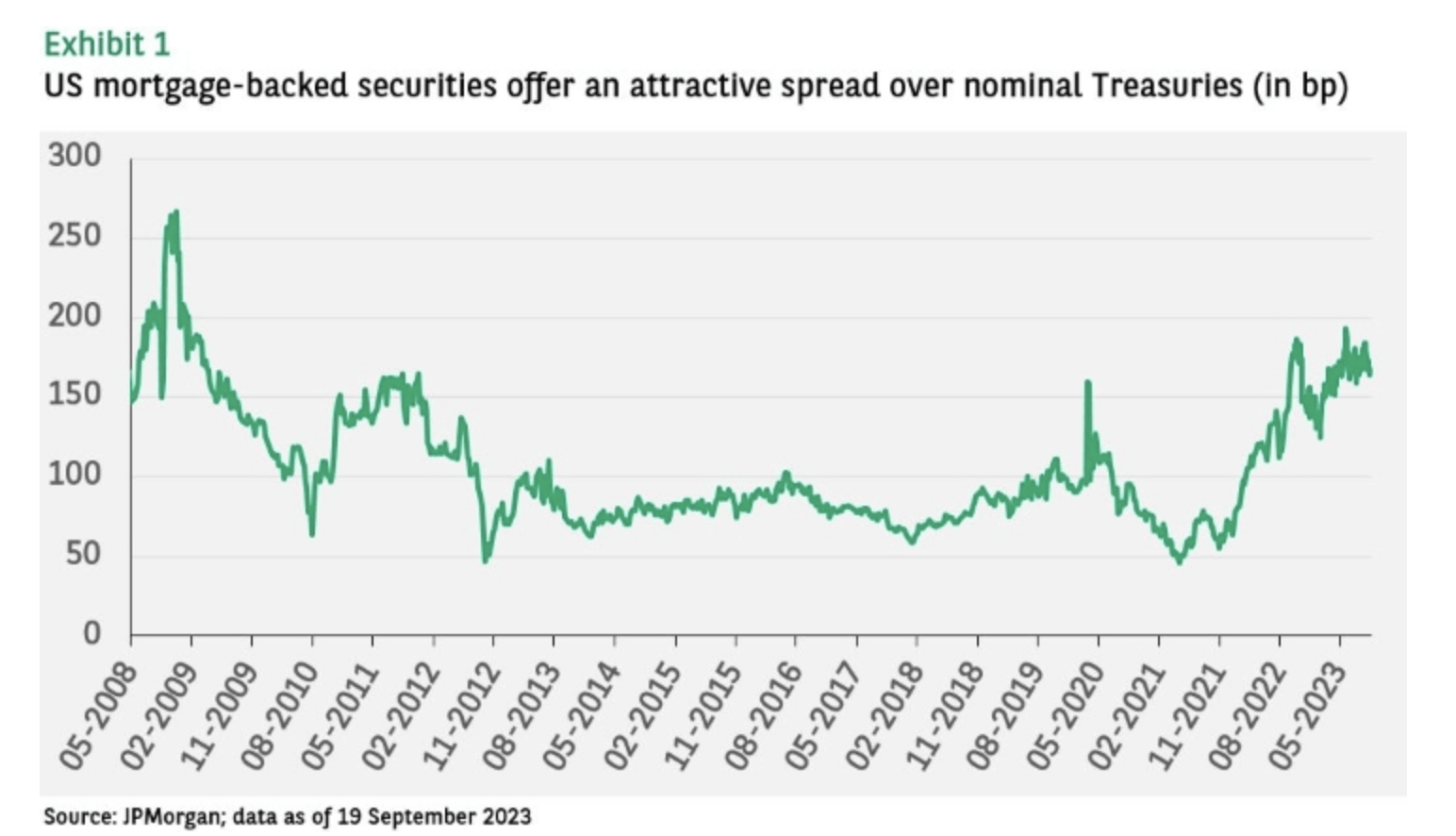

In addition to the movement in interest rates impacting book value, the increase in spread between MBS and Treasuries also widened throughout much of 2023. From 2012 to 2020, the spread between MBS and U.S. Treasuries averaged between 50-10 basis points, but blew out to nearly 200 bps points at times in 2023, with some coupons impacted more than others.

MBS-Treasury Spreads (JP Morgan; Viewpoint)

{kind=link}

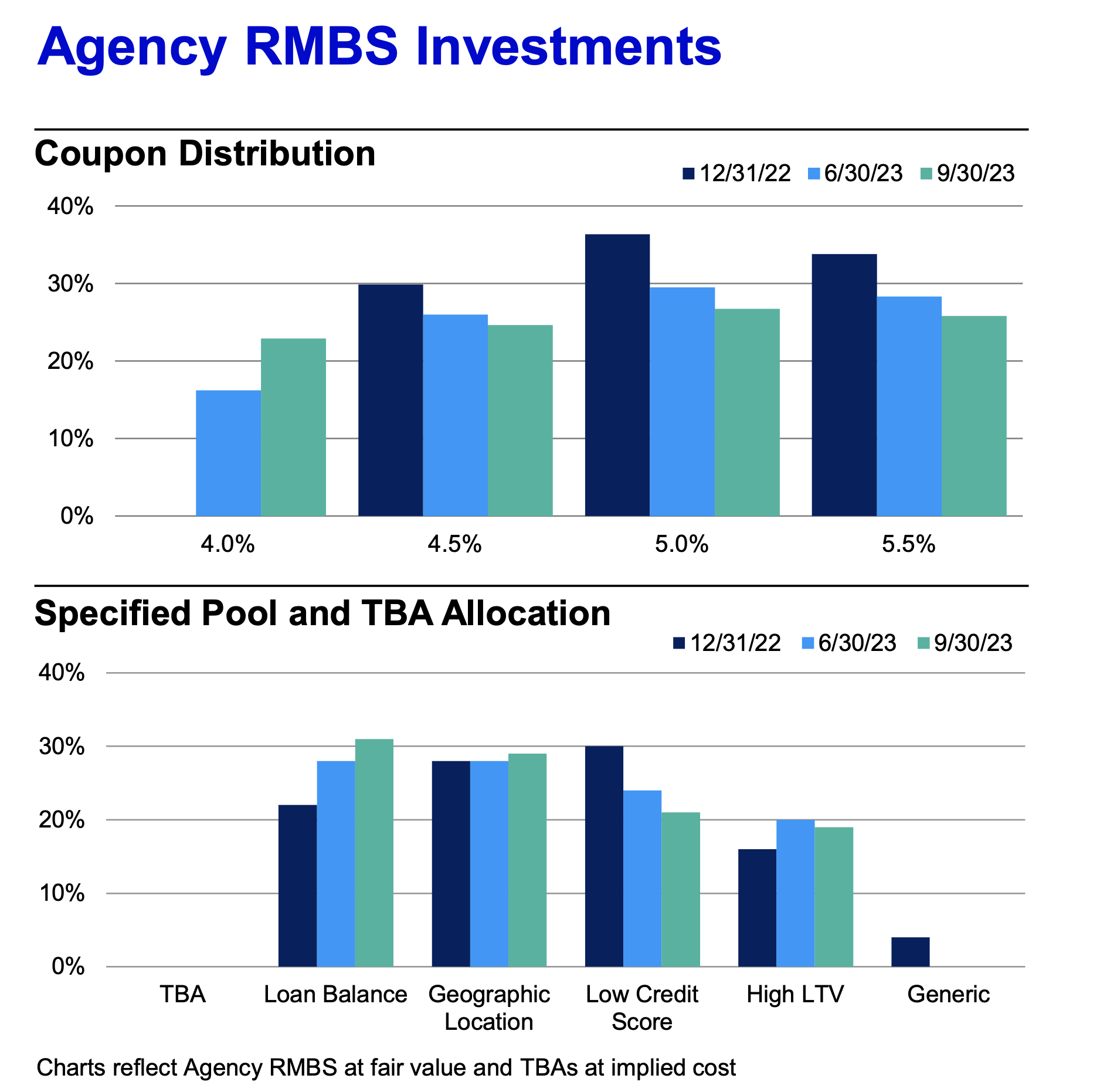

Like most agency mortgage REITs, IVR began shifting its portfolio to higher coupon MBS in 2022, taking the losses in the process. However, in the back half of 2023, it did shift some more investments down to 4% coupon bonds that had low loan balances.

IVR MBS Portfolio (Company Presentation)

{kind=link}

On its Q3 earnings call, CIO Brain Norris said:

Current coupon valuations ended the quarter significantly lower versus Treasuries and Agency RMBS spreads widened approximately 20 to 25 basis points across the coupon stack. In addition, specified pool pay-ups continue to decline as interest rates increase. The dollar roll market for TBA securities remained unattractive as more recent issuance with higher loan balance have a less attractive prepayment profile and the lack of consistent bank demand negatively impacted technicals. Although Agency RMBS underperformed in October, the market did stabilize in the latter part of the month as investors selling dissipated and volatility subsided modestly. Our portfolio of Agency RMBS decreased marginally over the quarter as the combination of higher interest rates and wider spreads led to lower prices on our assets. We remain focused on more attractively priced higher coupons, which are largely insulated from direct exposure to assets held by the FDIC and on the Federal Reserve's balance sheet. In addition, we remain exclusively invested in specified pools with no exposure to the deterioration in the dollar roll market for TBA securities. We continue to modestly improve the quality of our specified pool holdings by increasing our allocation to lower loan balance stories given more attractive valuations during the quarter."

In addition to the spread risk between Treasuries and MBS that can impact book value, there is also the risk between the yield IVR gets on its investments and the interest on its funding costs. It generally hedges, but if its effective net interest margin declines, it can impact its earnings available for distribution and its dividend.

A mortgage REIT can also face risks in a dropping rate environment with prepayment risk. This happens when people refinance to lower rates, paying off their existing mortgages more quickly than anticipated. Mortgage REITs then need to reinvest that money into securities paying lower rates. Prepayments occur in any environment, as people move and pay off loans, but the risk is higher in an environment where rates are falling and homeowners are refinancing. That is one reason why IVR's shift more towards 4% low loan balance MBS could prove to be a prudent move, as homeowners that recently obtained new mortgages at high rates are more likely to quickly refinance.

IVR is presently paying a 40-cent quarterly dividend, good for a yield of 17.4%. In mid-December, it said it expected its book value per share to be between $9.82-10.22 at year-end. During its Q3 call, the company had said it thought its book value per share had fallen to between $9.07-$9.45 as of early November. It expected its leverage to be back up to between 5.6-5.8x after taking it down to 4.3x at the end of October.

Conclusion

2023 was a difficult period for mortgage REITs, and IVR was no exception. However, with the Fed indicating the likelihood of three interest rate cuts in 2024, the fortune for the sector and IVR should vastly improve.

For its part, it looks like IVR management could have made a mistake by significantly taking down leverage towards the end of October, a month and a half before the Fed shifted gears in mid-December around its rate expectations. That said, it has put on more leverage since, and the question becomes did it miss some of the initial upside or was it re-adding leverage before the announcement.

At present, IVR trades at 0.92x the book value it said it expecting for the end of Q4 and at which it was at the end of Q3 as well. By comparison, AGNC ( AGNC ) trades at 1.07x end of Q3 book value, Annaly ( NLY ) at 1.08x, ARMOUR ( ARR ) at 0.91x, and Two Harbors ( TWO ) at 0.88x.

At this time, I expect the shift from rising rates to falling rates, combined with a return to more historical spreads versus Treasuries for MBS, to lift the entire mortgage REIT space. Expect book values to start to rise and the stocks to follow suit. IVR is trading right in the middle of the space in terms of valuation, and it should be set to go along for the ride, even if it missed some benefit by deleveraging earlier. As such, I'm going to start the stock with a "Buy" rating. My target is $12.50, as I expect book value per share to recover towards Q1 levels ($12.61) to go along with a robust dividend payout.

For further details see:

Invesco Mortgage Capital To Benefit From Fed Shift